SCS - Steelcase: Back To Office Back On Growth

2023-10-15 06:24:57 ET

Summary

- With more workers expected to return to the office, Steelcase is likely to experience a favorable environment for revenue recovery.

- Margins are also expected to improve further due to lower raw material prices.

- Despite the absence of a specific triggering factor, the company appears to be undervalued and is likely to attract investors' attention.

- Despite ongoing macroeconomic headwinds, I believe it is manageable.

Thesis

Steelcase (SCS) is a furniture company founded in 1912 that mainly serves corporate customers. I believe current price offers an attractive entry point for investors for several reasons. Firstly, despite the slow return, workers are gradually returning to the office and this trend is expected to lead to an increase in revenues. Secondly, with higher revenue, the company would achieve better profitability, thanks to the softening in commodity inflation. Thirdly, the company's valuation provides a margin of safety.

Overview of the business

{kind=link}

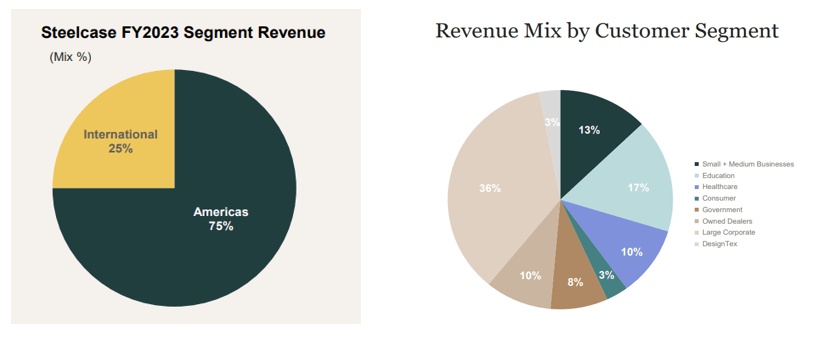

Steelcase is a leading global furniture manufacturer with two operating segments: Americas and International. 75% of its revenue is generated by the Americas segment, which serves customers in the U.S., Canada, Latin America, and the Caribbean Islands. The international segment accounts for 25% of the total revenue, focusing on customers in Europe, the Middle East, Africa, and Asia. When segmented by customer type, large corporations contribute 36% of the total revenue. In fact, Steelcase primarily serves institutional customers such as governments, educational institutions, and other businesses.

Competitiveness

Steelcase

When compared by revenue, Steelcase is one of the leading global office furniture manufacturers. With various brands such as Smith System, Halcon, and others, it produces top-tier chairs, desks, and other office-related products. I believe its popularity and the quality of its products are high-end. However, if compared to other leading brands such as Herman Miller, I think it's hard to say that Steelcase products are the best of all others. It would simply depend on the buyers' taste.

Financials

{kind=link}

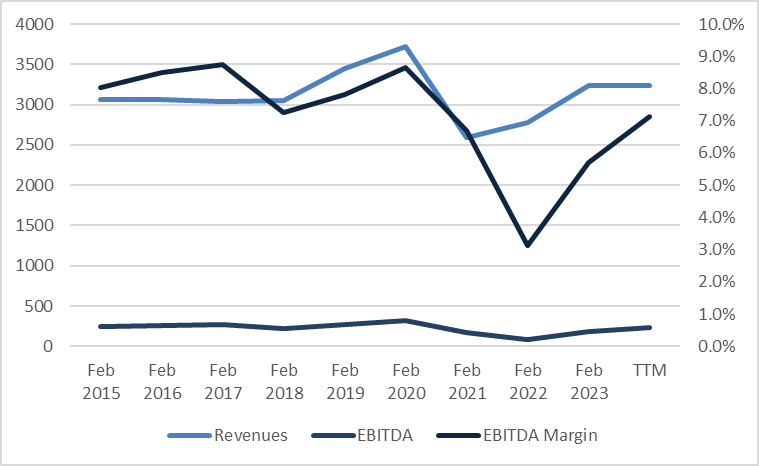

Steelcase is not a company with a stellar growth rate, but it records steady revenue growth. Before the corona pandemic, the company had two growth engines: organic growth and small acquisitions. It expanded by acquiring companies including AMQ in 2017, Orangebox in 2018, VICCARBE in 2021 and other brands. However, as the pandemic hit the commercial real-estate markets and companies allowed employees to work from home, revenue dropped by more than thirty percent from 2020 to 2021 due to reduced demand for office furniture. On the margin side, the business is highly influenced by the prices of raw materials such as steel, lumber, and labor costs. With high inflation, the EBITDA margin decreased from 8.6% in 2020 to 3.1% in 2022. As workers slowly return to the office and inflation has alleviated, the company is on its way back to growth and higher margins, although it is still below its peak.

{kind=link}

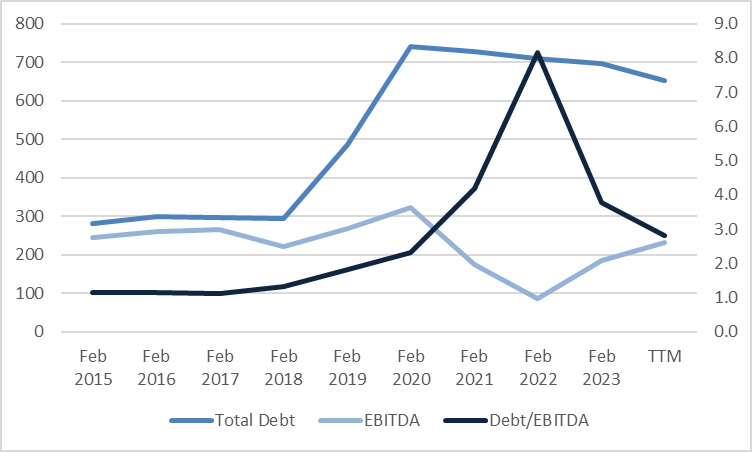

Moreover, I believe the company is unlikely to encounter serious credit problems in the near future. Even though the total debt amounts to $651.4 million, it holds about $153.6 million in total cash & short-term investment. As the company recorded roughly $230 million EBITDA in TTM, net-debt/EBITDA ratio would be about 2.5. When it comes to interest burden. The company is paying roughly $30 million in interest expenses. However, its operating income and EBITDA are higher than the expense. These factors show that the company is capable of managing its debt.

Q2 Earnings

{kind=link}

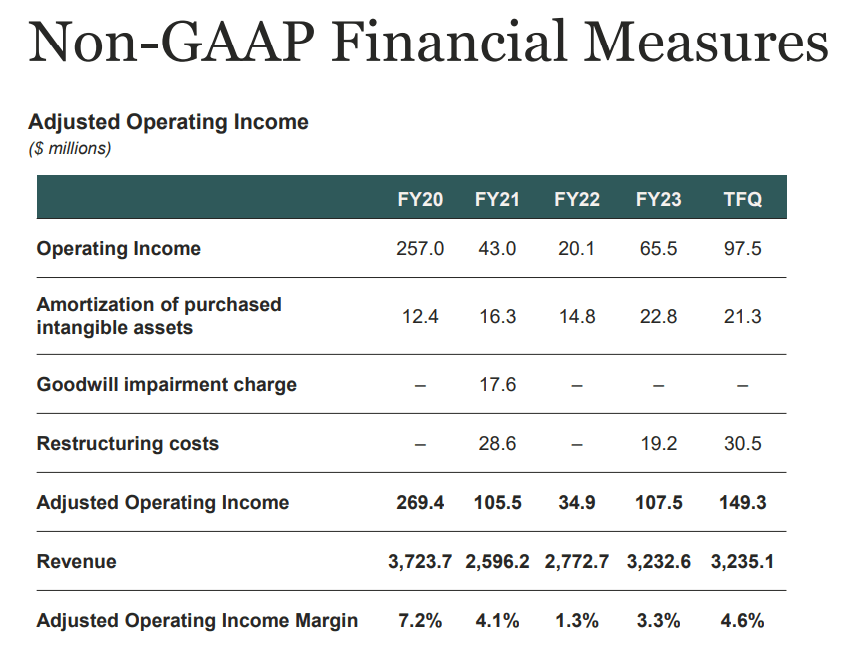

Based on recent second-quarter earnings, I believe the company's improvement in the margin side shows that it is steadily recovering from the pandemic and inflation-related issues. Even though the revenue declined 1% year to year, from $863.3 million to $854.6 million, it has beaten the analyst consensus by $25.78 million. The gross margin and operating margin in the second quarter were 33.3% and 5.1% respectively, increasing from 31.4% and 2.9% respectively in the previous quarter. As the gross margin in 2019 and 2020 was 31.6% and 32.6% respectively, the company has recovered to the margin levels before the pandemic. For the third quarter, the company expects the revenue would decline by 3-6% with the gross margin around 32%. A decrease in revenue is a concern, but I believe the company would be able to get back on growth when more workers return to this office. I will further explain this in my investment thesis.

Investment Thesis

{kind=link}

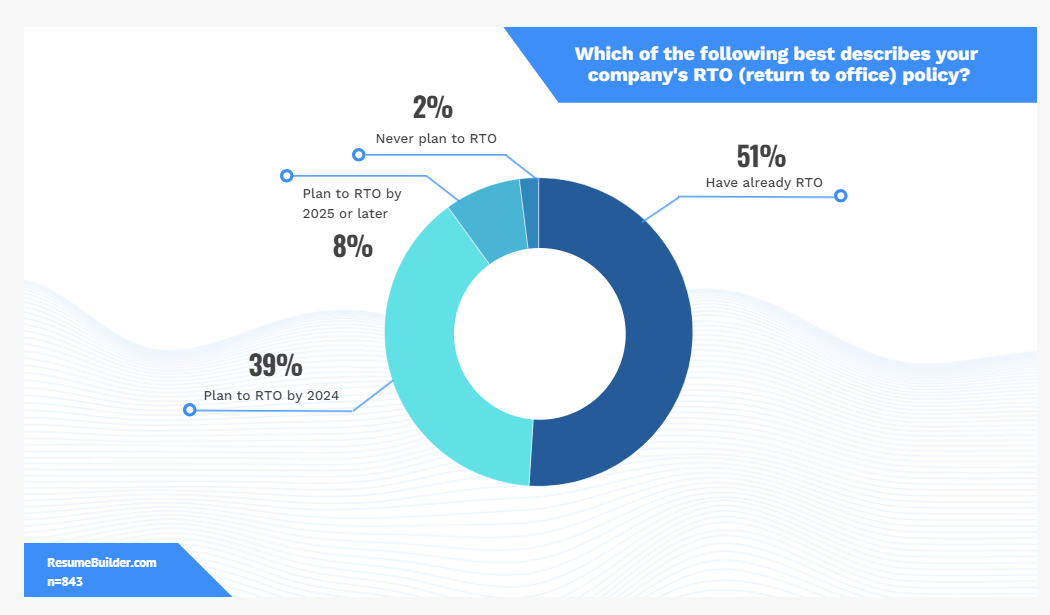

Source: ResumeBuilder ( 90% of Companies Will Return to Office By the End of 2024 - ResumeBuilder.com )

Firstly, revenue is expected to increase as more workers are likely to return to the office. During the COVID-19 pandemic, the narrative surrounding working from home was positive, with many publications arguing that remote work is efficient, saving commute time, and enhancing employee productivity. However, employers are now skeptical about the effectiveness of remote work and are mandating employees to return to the office, despite strong opposition. According to a study by ResumeBuilder.com, 90% of companies want their employees back in the office by 2024 and 75% of respondents believe that RTO (Return to office) has led to improvement in revenue and productivity. Even major tech companies such as Google (GOOG) and Amazon (AMZN), which previously encouraged remote work, are now requiring employees to work in the office. In my opinion, employees will still be allowed to work from home to some extent, but eventually, most workers will return to the office. Consequently, the demand for Steelcase is likely to increase gradually as physical office spaces will remain necessary.

{kind=link}

Secondly, higher revenue would lead to higher margin as the price of raw materials has been stabilized. With low interest rates and high demand, prices of lumber, steel, aluminum and other raw materials skyrocketed during 2021-2022. However, as Chinese demand has softened due to economic downturn and high interest rates absorbed excess liquidity, the prices of raw materials dropped from the peak. As shown in the chart above (Source: Trading Economics), price of lumber, steel, aluminum dropped sharply from the levels seen in 2021. I believe such environment would persist, suppressing raw material inflation.

{kind=link}

Despite recent rally, Steelcase is undervalued and there is more room for stock returns. In my opinion, as the company is not a stellar high growth company with interesting technologies such as A.I. and related to commercial real-estate market, it is undercovered by investors. As a result, the stock price did not respond to the company's recovery in revenue and margin until recently. As I believe the company's revenue would recover to 2019-2020 level, thanks to the reasons I explained above, current market valuation would increase further.

Valuation

In my opinion, the purpose of doing valuation of a company is not to calculate the exact future stock price, but to check whether the probability to earn money is higher than losing when investing in the stock.

Peer Analysis

| Steelcase |

| MillerKnoll, Inc (MLKN) |

| HNI Corporation (HNI) |

| EV/EBITDA (fwd) |

| 13.46 |

| 14.58 |

| 28.27 |

| P/E Non-GAAP (fwd) |

| 7.31 |

| 8.4 |

| 9.94 |

| Price/Cash Flow (fwd) |

| 6.49 |

| 5.75 |

| 7.71 |

Source: Seeking Alpha

During the pandemic, the office furniture industry witnessed significant M&A activity, with companies like Knoll being acquired by Herman Miller and Kimball being acquired by HNI Corporation. HNI Corporation appears to be overvalued. However, a direct comparison with Steelcase is challenging due to HNI's involvement in residential building product segment. The surge in stock prices of residential builders and related companies in 2023 has likely to contributed to HIN corporation higher valuation. In terms of valuation, Steelcase and MillerKnoll are fairly comparable. This shows that Steelcase is neither overvalued nor undervalued when compared to competitors. Moreover, based on my research on reviews of those office furniture brands, determining the number one brand is almost impossible as preference vary among buyers. Consequently, I believe the valuation of office furniture companies would move in a similar manner. To be exposed to the stock that focuses on office furniture, Steelcase would be the top pick as it has higher revenue in the sector.

Earning*Price & My Strategy

In my view, market valuation is based on the formula of Earnings * Price. I made three assumptions.

Firstly, EBITDA margin would rise to 7-8% level thanks to the softening raw material inflation.

Secondly, revenue would increase more than 2-3% in the short term after modest decrease of 1% from 2023 to 2024 as more workers would return to the office. The company's mid-term average annual organic revenue growth is in the range of 5-7%.

Thirdly, the stock valuation would respond accordingly to the improvement of revenue and margin.

Seeking Alpha/Author

With a 2% and 3% increase in revenue in 2025 and 2026 respectively, along with an 8% EBITDA margin, Steelcase would recover to the levels seen in 2019. Since the stock price of the company in 2019 was about $18-19, there is roughly more than 60% upside potential. However, I recommend investors approach this stock with a 1-2 year investment horizon, rather than a buy-and-hold strategy or regarding it as a dividend stock. When the stock reaches its intrinsic value, it is unlikely that the stock price would increase further, as the office furniture industry is not a high-growth sector. Moreover, as the industry does not present an interesting business model, it may not be able to grab investors' attention. As I believe the company's revenue would fully recover to the levels seen before the corona pandemic within 2 years, it is worth waiting to see the market's reaction, but no longer than that.

Risks

Firstly, the economic downturn may start to accelerate as the Fed is expected to maintain high interest rates for an extended period. Due to the hawkish stance of the FOMC and a higher GDP projection for 2023, the interest rate for U.S. 10-year bonds has risen to the 4.6-4.7% range. High interest rates could negatively impact business sentiment, potentially discouraging investment in office furniture. However, in my view, the Fed may halt further rate hikes after a one-time increase in November. Given that the market has already priced in this one-time hike, bond interest rates are expected to stabilize over time.

Secondly, oil prices could trigger overall raw material inflation. While it's challenging to predict the exact level of WTI prices, considering past instances like the demand destruction in 2008 and 2022 when WTI prices exceeded the $100 level, it's anticipated that oil prices will remain within the $70-80 range.

Thirdly, Steelcase may remain undercovered by the market. For the undervalued stock price to increase, I believe there needs to be a triggering factor. One example could be A.I. implementation in the semiconductor industry. However, Steelcase lacks such a trigger beyond earnings reports. This is why I recommend short-term strategies rather than a long-term buy-and-hold approach.

Conclusion

As Steelcase is expected to demonstrate higher revenue with improved margins, the stock price is likely to recover to the levels seen in 2019. Therefore, despite the current rally in the stock, the upside potential exceeds the downside risk.

For further details see:

Steelcase: Back To Office, Back On Growth