SCS - Steelcase: Improving Profits And Strong Cash Flow Generation (Rating Upgrade)

2023-12-24 07:33:05 ET

Summary

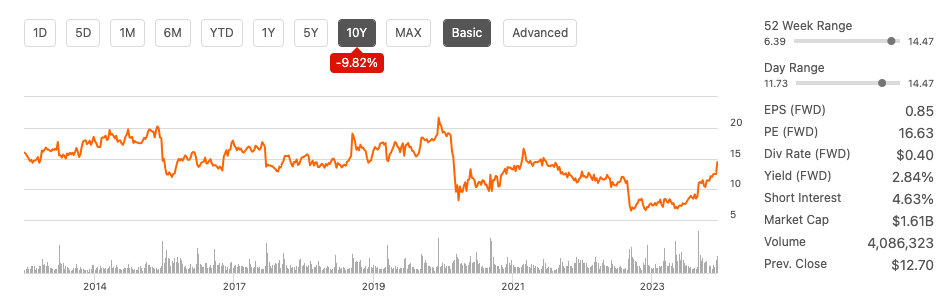

- Steelcase Inc. stock has increased by 105.69% in the past year but is still below historic levels.

- The company's Q3 earnings per share beat expectations by $0.70, but revenue fell short.

- Steelcase has seen a 15% year-over-year increase in orders and has shown improved gross profit margin and liquidity.

Steelcase Inc. ( SCS ) has seen its stock increase by 105.69% over the last year but is still trading below its historic levels. It recently released its Q3 2024 earnings report , beating EPS expectations by $0.70 to reach $0.30 while missing revenue expectations. The company has also declared a $0.10 per share quarterly dividend, which aligns with its previous dividend. While the company’s top line has remained relatively flat, its EPS has seen a promising upward growth path; orders grew 15% YoY, and we see a strengthening gross profit margin and an improved liquidity YoY. While it is essential to realise that the company is not delivering the top and bottom line as it was before the pandemic disruption, there have been some significant financial improvements since my Hold rating in my previous article . Some more substantial tailwinds exist as more companies seek to incentivise workers to return to the office. Furthermore, studies have found that workplace investments were a priority even during these more uncertain economic times. Therefore, I am upgrading my thesis to a bullish recommendation.

Ten year stock trend (SeekingAlpha.com)

{kind=link}

Company overview

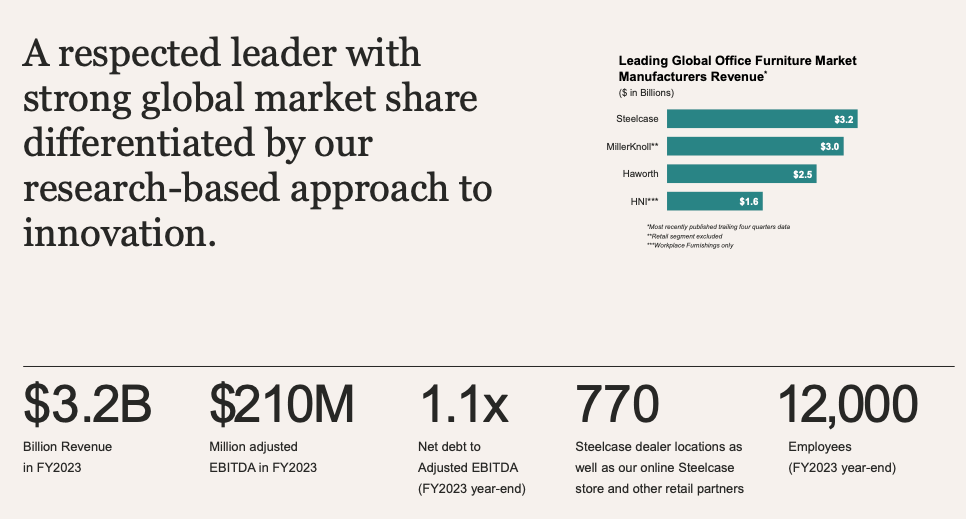

Steelcase is a company that offers furniture and architectural products. It was founded in 1912 and has a strong presence in the office furniture market. The company is known for its research-driven innovations. Steelcase serves customers in the US (which accounts for 75% of its revenue ) and internationally. Its customers come from various industries such as corporate, government, healthcare, education, and retail sectors. Steelcase distributes its products and services directly to customers through a network of 770 independent and company-owned dealers.

Company highlights (Investor presentation )

{kind=link}

The success of Steelcase, is directly linked to its customers' investment in their workplaces. As companies adopt new ways of working and integrate them into their layouts, Steelcase sees an increase in orders. This is evident in the latest Q3 2023 results, which show a 15% year-over-year increase in orders. Steelcase is experiencing growth through its large corporate customers in the Americas, both in continuing and project business. Additionally, the company's international growth is primarily driven by the Asia Pacific region.

Revenue by customer mix (Investor presentation 2023)

Studies show that even in economically uncertain times, 54% of companies increased their workplace investments. As companies push for employees to return to the office, they are incentivized to make it more appealing and productive for employees. Going into the last quarter of the year, Steelcase has a backlog of $699 million in customer orders, a decline of 10% YoY. However, orders in the early weeks of Q4 have grown by 7% YoY. With these action points, the company expects Q4 revenue to be between $765 and $790 million, which falls under last year's results. At the same time, its EPS is expected to increase from last year to between $0.16 and $0.20 for Q4 2024.

Financials

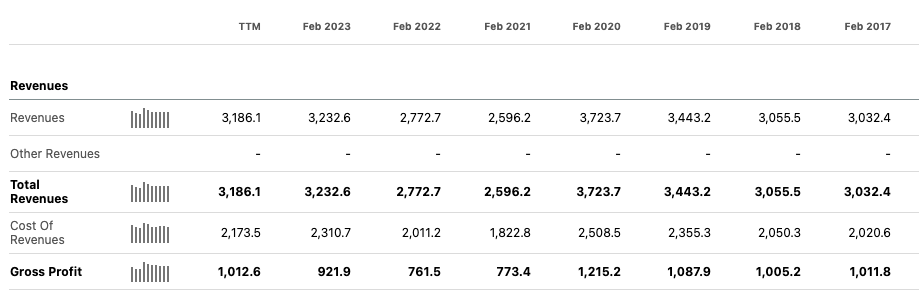

Since the onset of the pandemic and the rise of remote work, the company has faced a revenue decline. Over the past three years, there has been gradual improvement, although it hasn't reached the heights of FY2020. In Q3 2024, it reported a revenue of $777.90 million, reflecting a 6% year-over-year decrease.

Annual revenue and gross profit (SeekingAlpha.com)

{kind=link}

The company's earnings mirrored this trajectory, with notably higher figures pre-FY2020, followed by a substantial drop in FY2021. Despite maintaining positivity, analysts anticipate an upward trajectory in earnings, though it's improbable to reach pre-pandemic levels.

Annual earnings history (SeekingAlpha.com)

{kind=link}

The company's net income TTM is $75.5 million, and it has been increasing over the past four years. In Q3 2024, the company reported a net income of $30.8 million. This trend indicates the company's ability to generate increasing profits, reflecting a promising opportunity for potential investors.

Annual net income (SeekingAlpha.com)

{kind=link}

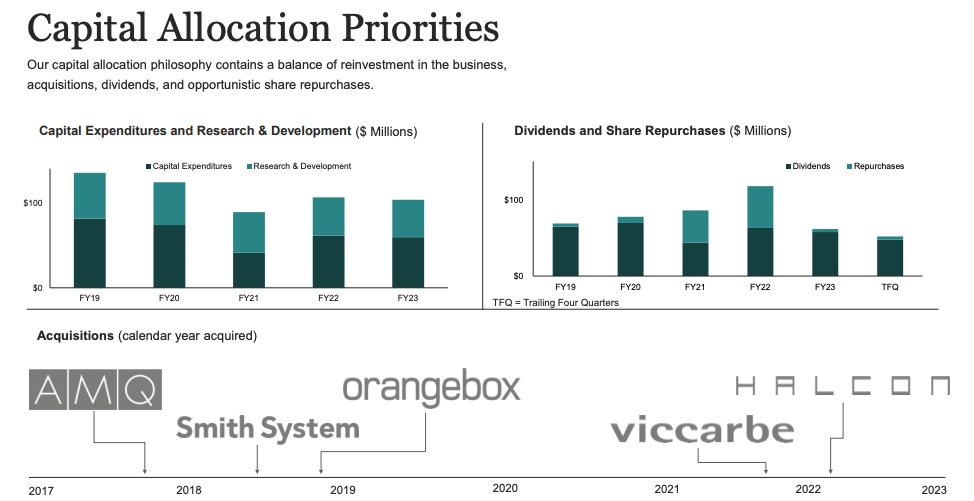

The company's positive levered free cash flow of $308.63 million TTM, alongside a robust cash from operations figure of $339.30 million TTM, signals a healthy financial position. The consistent increase in levered free cash flow over the past three years is particularly encouraging. This surplus cash allows for strategic reinvestment in the business and provide returns to investors. It reflects a solid foundation for sustained growth and financial management, as seen during the Q3 2024 presentation.

Capital allocation (Investor presentation 2023)

{kind=link}

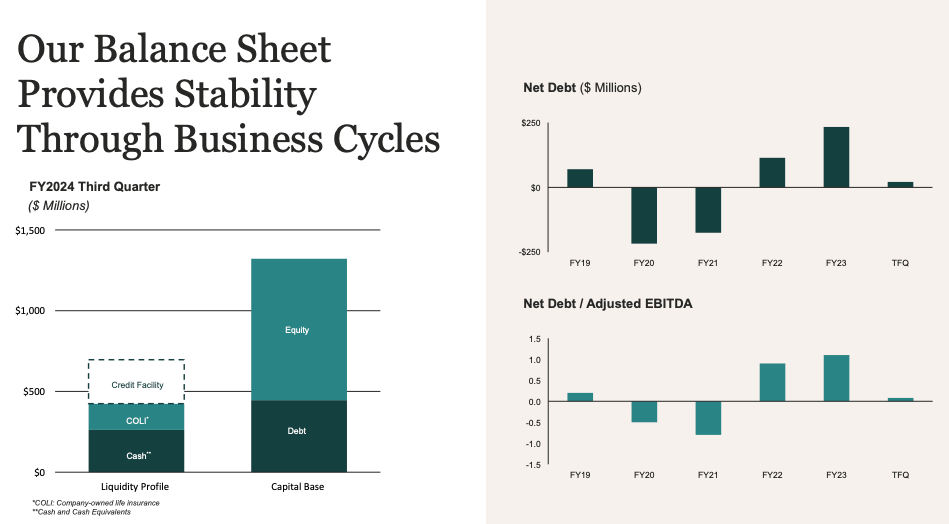

The company has a dividend program, and an ex-div date is set for January 3rd, with a FWD yield of 3.15%. It has declared a $0.10 per share dividend for the quarter. However, the dividend growth has not been consistent over the past three financial years. If we look at the company's liquidity, we can see that it has increased YoY, with total liquidity at $446.1 million, including the cash surrender value of company-owned life insurance, up from $110.1 million in the previous year. The company's total debt was $446.1 million.

Balance sheet overview (Investor presentation 2023)

{kind=link}

Valuation

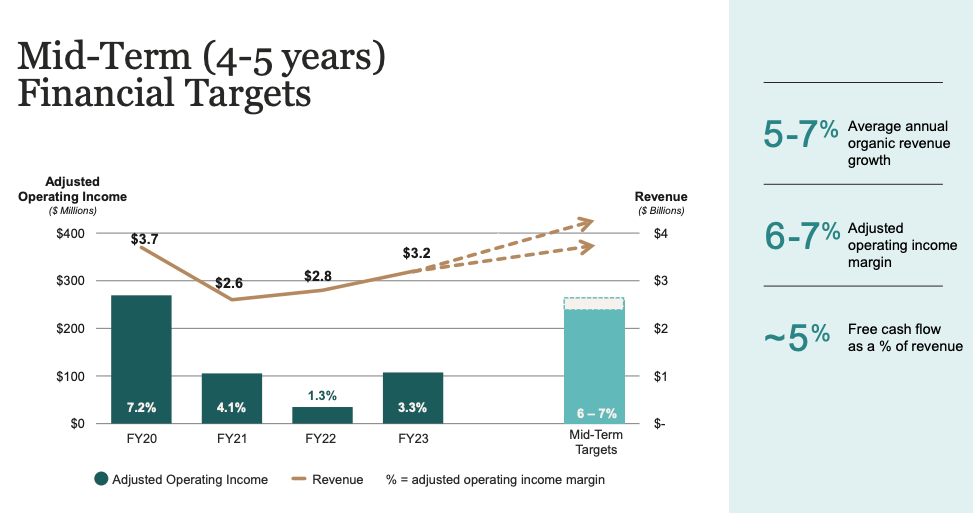

Steelcase has faced significant disruptions in recent years due to the transformation of office work dynamics. However, these changes have created new opportunities, leading to the company's resurgence amid the return-to-office trends. Their five-year growth targets indicate a consistent upward trajectory in both revenue and profitability, with a mid-teens growth expectation. This is an encouraging prospect for investors looking for long-term potential.

Five year growth targets (Investor presentation 2023)

{kind=link}

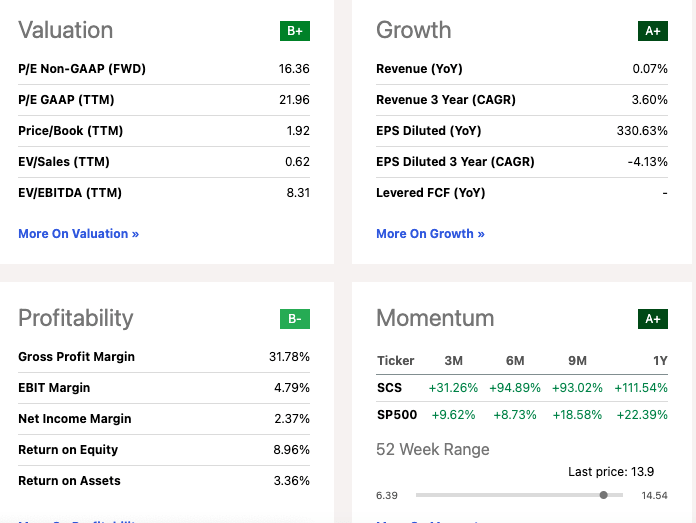

Seeking Alpha's Quant grading system's B+ rating reflects positive market sentiment. The forward price-to-earnings ratio of 16.63, lower than the industrial sector median, signifies a more attractive valuation. Additionally, the price-to-sales ratio under one suggests investors are paying a favourable price relative to the company's sales. The TTM dividend yield of 2.84% surpassing the sector median is another appealing aspect for income-oriented investors.

Quant valuation (SeekingAlpha.com)

{kind=link}

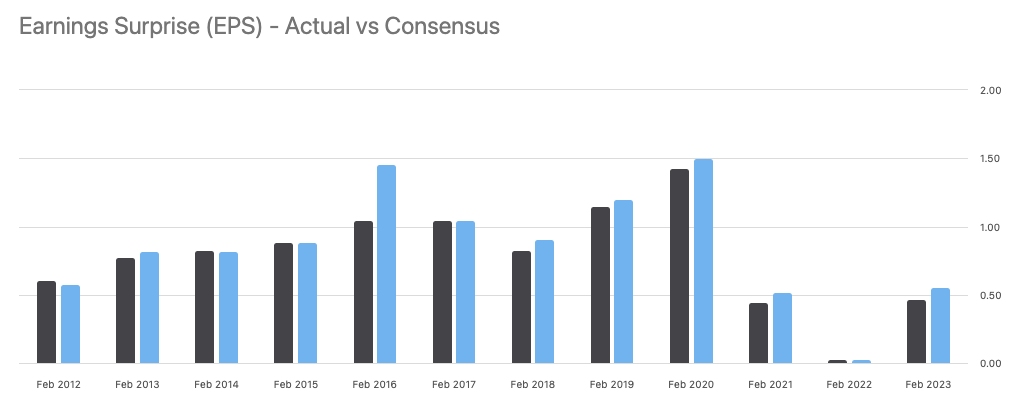

The stock's impressive momentum consistently outperforms the S&P 500, which is notable. The company has surpassed EPS estimates for seven consecutive quarters, showcasing its robust performance. Analysts' revised predictions, which foresee earnings growth of $0.85 for FY2024 and $0.98 for FY2025, align with the company's outlined growth targets, further bolstering confidence in its future prospects. Overall, Steelcase's strategic recovery plan and projected upward trends make it an enticing proposition for investors seeking potential growth and value.

Risks

It is important to be aware of the risks associated with investing in Steelcase. One of the major concerns is the impact of supply chain issues on the company. The delivery times may be affected due to disruptions from third-party suppliers, which can negatively impact the business performance. Unfortunately, these disruptions are beyond the control of the company. Another risk is that Steelcase's market sensitivity to economic cycles and geopolitical uncertainties may pose a threat to the company. Fluctuations in the global economy, governmental policies, or geopolitical tensions can affect customer spending patterns, resulting in a decrease in demand for workplace solutions. Furthermore, the furniture industry is highly competitive, and it is essential to meet the ever-changing customer demands for innovation, sustainability, and cost competitiveness. Despite ongoing investments in research and development and product expansion, it is crucial to continually innovate to align with changing workplace trends. Failure to adapt swiftly or provide differentiated products may affect market share, challenging the company's competitiveness against both established competitors and emerging disruptors.

Final thoughts

Steelcase has delivered strong EPS results in its latest Q3 2024 earnings report, and we can see that the company is benefitting from growing demand with increased orders. This is a different picture from what the company painted at the start of the year. As companies seek to increase the number of office workers and adjust to new working methods, Steelcase plays an important role in facilitating these changes. Although top-line growth remains flat, the company is improving its gross profit margin and liquidity position and has upward-trending positive cash flow generation while rewarding investors with a dividend program. Therefore, I am upgrading to a bullish stance.

For further details see:

Steelcase: Improving Profits And Strong Cash Flow Generation (Rating Upgrade)