SCS - Steelcase Q2 Earnings: A Stellar Quarter Reaffirms The Bullish Case

2023-09-21 13:15:41 ET

Summary

- Steelcase's shares rose 19.3% after exceeding expectations in Q2 and providing favorable guidance for Q3.

- While sales did fall year-over-year, earnings handily surpassed expectations, with the rise caused by higher pricing and its impact on margins.

- SCS stock still looks attractively priced and it's likely the stock will continue to rise over the long run.

The past couple of days now have been incredibly positive for Steelcase ( SCS ), an enterprise that focuses on the production of furniture, as well as architectural products, and various technologies. On September 20th, after initially rising as much as 29.2% during the day, shares closed up 19.3%. And as of this writing on September 21st, shares are up nearly 2% compared to where they closed at the previous day. This movement higher was driven by financial results covering the second quarter of the company's 2024 fiscal year. Steelcase exceeded expectations on both the top and bottom lines and also provided favorable guidance for the third quarter. When all is said and done, the company seems to be doing incredibly well from a fundamental perspective. Although the stock is not particularly cheap relative to earnings, it does look cheap on a cash flow basis. On top of this, shares of the company are also cheap relative to similar firms. When all of this data is combined, it makes me feel confident in assigning the company a soft ‘buy’ rating at this time.

A stellar quarter for Steelcase

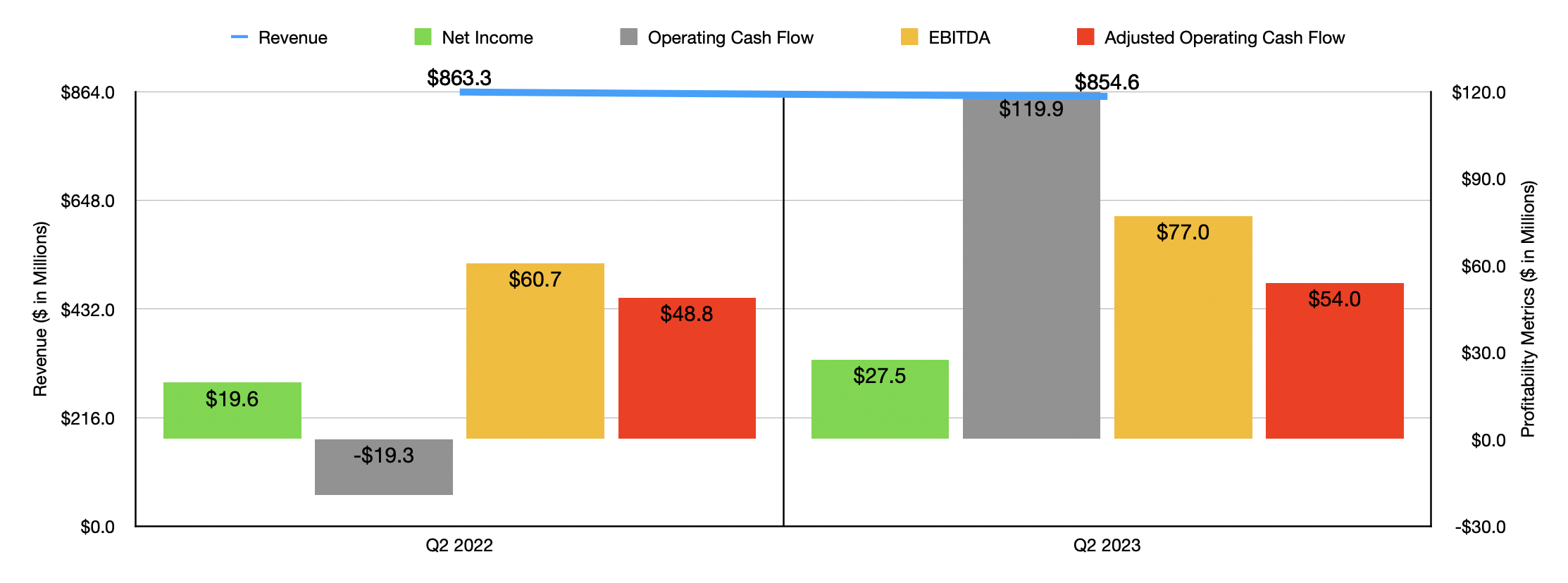

It's truly difficult to overstate just how amazing Steelcase performed during the second quarter of its 2024 fiscal year . For starters, while revenue did fall year over year, dropping from $863.3 million to $854.6 million, the sales ultimately reported by management exceeded analysts’ expectations by $25.8 million. The drop reported by management came about even though organic revenue in the Americas grew about 1% year over year. This 1% increase was caused by lower volume that was more than offset by higher pricing. Internationally, however, the picture was different. Driven by a 5% decline in organic orders, total international organic revenue dropped 8%.

{kind=link}

In discussing the causes behind this, management made clear that the macroeconomic environment has resulted in mixed performance in the firm's international markets. Keep in mind that Steelcase is incredibly diverse on this front. After all, while its international operations account for only 20.5% of the company's revenue, it operates locations in 17 different countries across the globe. So while one market might be achieving great performance, another one could more than offset this. Meanwhile, in the Americas, the company attributed its improved results to double digit growth in the continuing business. But there was a weak spot when it came to project business.

{kind=link}

On the bottom line, performance was far better. GAAP earnings per share came in at $0.23. In addition to beating out the $0.17 per share the company reported during the second quarter of 2022, earnings also exceeded analysts’ forecasts by $0.09 per share. On an adjusted basis, management also beat out expectations. Earnings there came in at $0.31, which was up from the $0.21 per share seen the same time last year. And this was enough to exceed analysts’ forecast by $0.11.

The earnings per share that the company generated translated to net profits of $27.5 million. That compares favorably to the $19.6 million reported during the second quarter of 2022. Other profitability metrics also followed suit. As an example, operating cash flow skyrocketed from negative $19.3 million to positive $119.9 million. If we adjust for changes in working capital, however, we get a more modest, but still impressive, rise from $48.8 million to $54 million. And lastly, EBITDA for the company expanded from $60.7 million to $77 million. Normally, in a low margin business like this, you would expect a drop in revenue to be accompanied by a drop in profits. However, the enterprise benefited significantly from gross margin expansion. The firm's gross profit margin jumped from 29.1% to 33.2% in the course of a single year, with higher pricing on the goods that it sold helping the company to the tune of $80 million. Management did also say that operational improvements bore some of the responsibility for improved results. But they did not disclose the extent to which this was the case.

{kind=link}

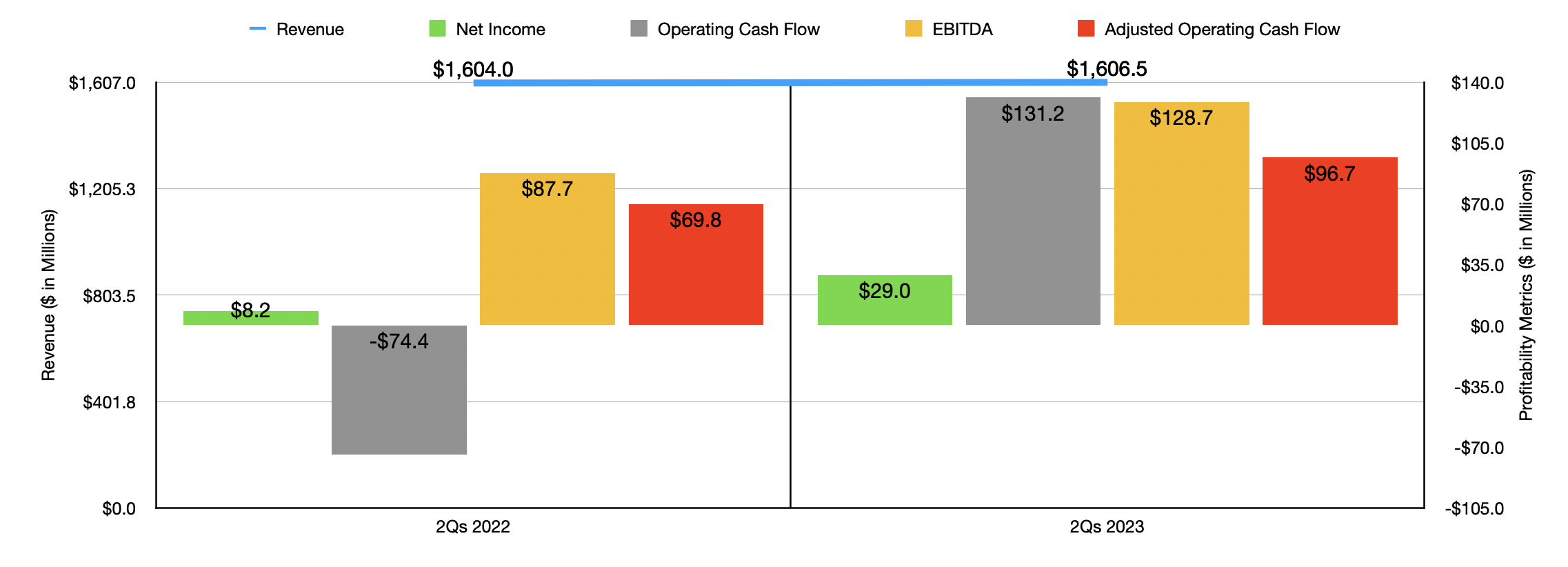

As you can see in the chart above, the bottom line strength demonstrated during the second quarter aided significantly in pushing up year to date results. Although the sales side of things worsened because of the second quarter, net profits and cash flows all benefited tremendously. When it comes to the rest of the year, management has not provided much in the way of guidance. They did say, however, that revenue in the third quarter should be between $780 million and $805 million. This would translate to a decline, perhaps a meaningful one, compared to the $826.9 million reported the same time last year. On the other hand, net profits should soar from $0.10 per share last year to between $0.19 and $0.23 per share this year. On an adjusted basis, we should see an improvement from $0.20 to between $0.23 and $0.27.

One of the great things about the robust performance demonstrated by management is that the company has been able to reduce debt. Net debt at the end of the 2023 fiscal year totaled $390.8 million. It actually grew to $406.3 million by the end of the first quarter. Today, however, it is significantly lower. Based on the data available, net debt totaled $297.5 million at the end of the second quarter. If management can come through on the aforementioned guidance, it wouldn't be surprising to see debt fall even further.

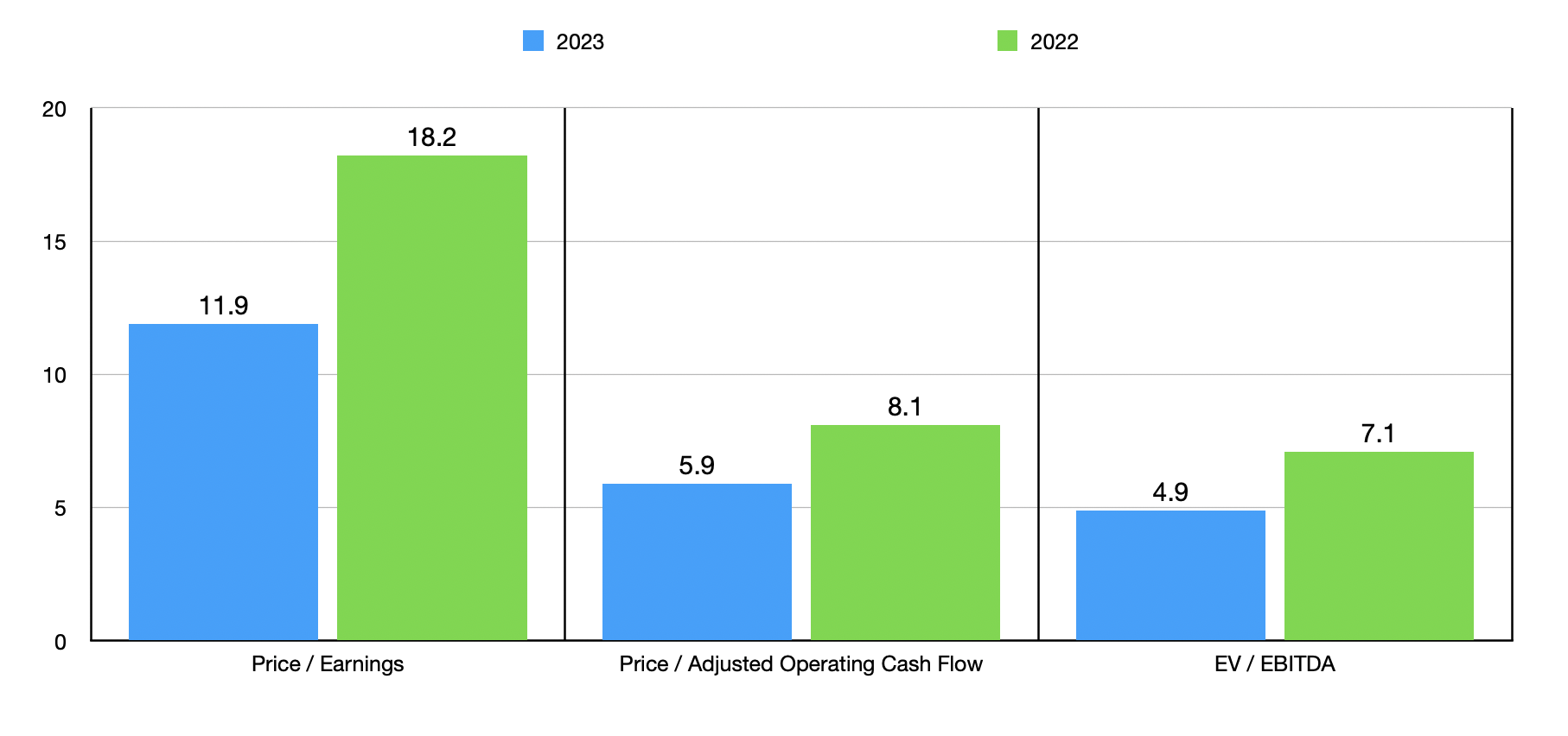

When it comes to pricing the company, we don't have a lot to go on. Management did forecast that overall net profits per share, on an adjusted basis, should be between $0.80 and $0.90. Usually, I am hesitant to use adjusted earnings in any valuation that I perform. But I approach this kind of thing on a case-by-case basis. The reason for my hesitancy is that many companies like to throw in things like stock-based compensation, which really gets us closer to cash flow than it does profits. But that is not the case with Steelcase. Instead, it is adding back reasonable items like restructuring costs. If this guidance comes to fruition, it should translate to net profits, at the midpoint, of $101.2 million. That would be substantially higher than the $0.56 per share, or $65.9 million, in adjusted earnings reported in 2023.

{kind=link}

If we annualize results experienced for the rest of the profitability figures, we should get adjusted operating cash flow of $204.5 million and EBITDA of $308.2 million. They should stack up nicely against the $147.6 million and $210 million, respectively, that the company generated in 2022. In the chart above, you can see the end result here in terms of pricing. The company should go from a price to adjusted earnings multiple of 18.2 to one that is 11.9. The price to adjusted operating cash flow multiple should drop from 8.1 to 5.9, while the EV to EBITDA multiple should decline from 7.1 to 4.9. Using these metrics, I then compared the company to five similar firms in the table below. On both a price to earnings approach and an EV to EBITDA approach, I found that our prospect was the cheapest of the group. Meanwhile, using the price to operating cash flow approach, two firms ended up being cheaper than it.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Steelcase |

| 11.9 |

| 5.9 |

| 4.9 |

| Interface ( TILE ) |

| 124.5 |

| 5.6 |

| 10.2 |

| NL Industries ( NL ) |

| 32.2 |

| 6.8 |

| 8.2 |

| ACCO Brands ( ACCO ) |

| 29.4 |

| 4.1 |

| 11.5 |

| HNI Corporation ( HNI ) |

| 20.7 |

| 9.8 |

| 11.1 |

| Kimball International (KBAL) |

| N/A |

| 7.8 |

| 40.6 |

Takeaway

Based on the data provided, I must say that I am very impressed with how Steelcase performed. Management did report lower sales year over year. But what's most important is that financial performance handily exceeded analysts’ expectations. Profits and cash flows also came in remarkably strong. When you add on top of this the fact that shares look attractively priced, both on an absolute basis and relative to similar firms, it should come as no surprise that I have decided to keep the company rated as a soft ‘buy’ for now.

For further details see:

Steelcase Q2 Earnings: A Stellar Quarter Reaffirms The Bullish Case