EXXRF - Stellantis: Buy For The Income Hold For The AI-Powered eVTOL Revolution

2023-07-18 13:04:04 ET

Summary

- Stellantis, a European carmaker listed on Euronext Milan and Euronext Paris, is undervalued by the market despite its 8% dividend yield and plans for long-term growth through AI and electrification.

- The company, resulting from the 2021 merger of Fiat Chrysler and PSA Group, has strong margins, a solid balance sheet, and plans to invest heavily in electrification and software by 2025.

- Despite competition and execution risks, Stellantis has the potential for significant returns for investors, with a strategic plan to double its revenue base.

Welcome to my 100th analysis published on Seeking Alpha!

Although it feels like yesterday, it has already been seven years of fruitful investing since my first contribution in June 2016. Despite never picking a specific market niche, my research has primarily covered REITs, high-yield picks, and European companies.

In today's article, I will indeed stick "to the basics" of my coverage, deep diving into a high-yielding European company: Euronext Milan and Euronext Paris-listed European carmaker Stellantis ( STLA ). With a well-covered 8% dividend yield, Stellantis is a core holding of mine for the high-yield basket allocation. The stock remains underappreciated and undervalued by the market, and I expect double-digit returns for patient investors over the long term.

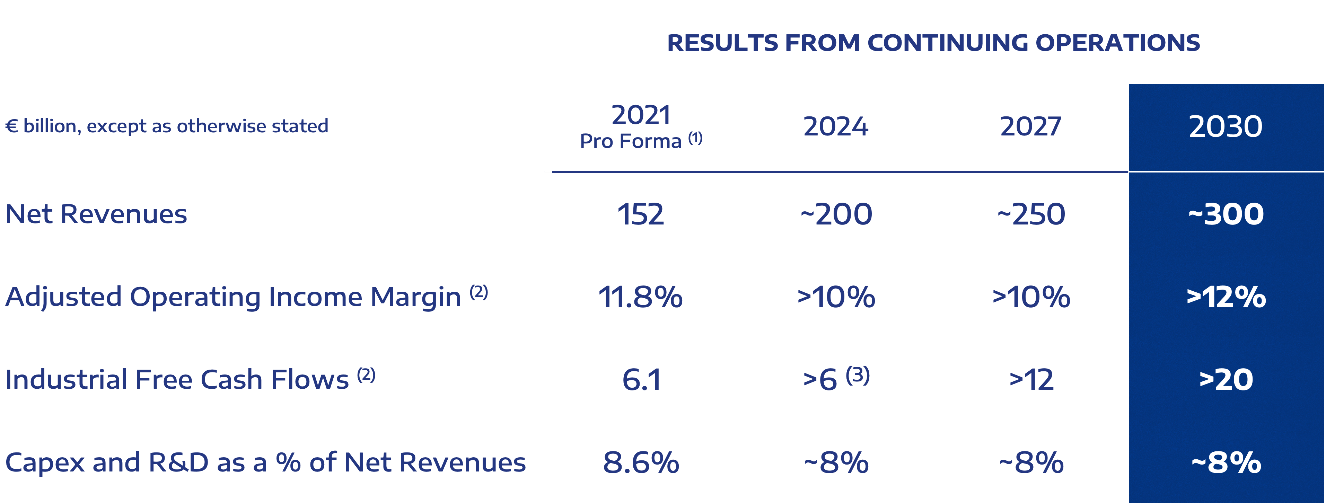

However, there is more than meets the eye of this traditional ICE incumbent player. Beyond car sales, Stellantis is preparing for long-term success, transforming itself into a " mobility tech company " that produces "intelligent vehicles" thanks to widespread AI advancements and adoption. The company plans to invest more than €30 billion in electrification and software through 2025, which it expects to pay back quickly and generate revenues of €60 billion for Stellantis by 2030. That's a decade-long 14.3% CAGR vs. the 2021 baseline!

But let's take one step back and understand why Stellantis is a bargain today.

The investment thesis today

Stellantis is the company that resulted from the 2021 merger between Italian-American Fiat Chrysler ((FCA)) and French PSA Group. Anchor shareholders include the Italian Agnelli family, which controls about 14% of the shares through the family's holding Exor NV ( OTCPK:EXXRF ), and the Peugeot family, which owns about 7% of STLA shares. The investment case revolves around a few key points:

- The synergies: the consummated merger between FCA and PSA can produce additional savings. Management's initial objective called for €5.0 billion in annual run-rate cash flow synergies, of which €4.0 billion by the end of 2024. The company announced the achievement of €7.1 billion at the end of 2022. Still, synergies obtainable through the combination of technology and vehicle platforms are yet to unfold fully, as it takes 2-3 years to bring new products to the market.

- The CEO: Carlos Tavares is an industry veteran who transformed the PSA Group from a loss-making carmaker facing bankruptcy risks to a top-performing firm, all within six years. Between 2014 and 2018, PSA's operating income increased more than five-fold. Tavares' can unlock significant value in Stellantis by following a similar process.

- The margins: Stellantis' revenues have dwindled in recent years. The company shunned unprofitable growth, and now its operating margins rank extremely high among automaker peers . The FY22 adjusted operating income margin hit 13%, driven by a 16.4% AOI margin in its North American segment and a 9.9% AOI margin in the more competitive European market. The company has minimal exposure to China, which I also view as a positive considering the ongoing tensions with the US.

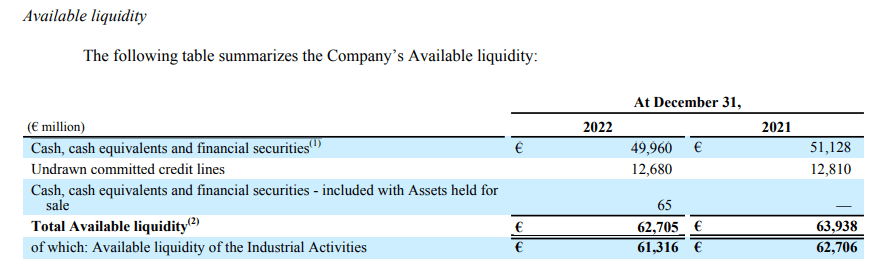

- The balance sheet: while arguably not as strong as the A+ credit rating of Toyota ( TM ) , Stellantis has a solid investment-grade BBB credit rating from S&P and Baa2 from Moody's. What is even nicer, the company closed 2022 with €50.0 billion in liquidity against €18.4 billion in long-term debt. I expect the solid cash position to shield the company against even the most severe macro downturn.

{kind=link}

The FY22 results indicate FCF generation of €10.8 billion, which against capitalization €52.6 billion, implies that Stellantis offer investors a free cash flow yield in excess of 20%. When considering its market cap and sales, the company appears undervalued vs. peers, suggesting a potential immediate upside of about 50% up for grabs. Indeed, an FCF yield of 13%-14% could be appropriate, considering that automotive is (traditionally) a highly cyclical industry. While the high level of indebtedness could justify Volkswagen ( OTCPK:VWAGY ) trading at the lower range of the below table, I don't find any acceptable reason for Stellantis to trade as low.

And Value For All / Seeking Alpha data (Jul17th)

Buy and hold!

Even though the current valuation appears more than reasonable, I am not too concerned about determining precisely how much Stellantis is worth today. Stellantis' fair value today could be approximately €25 per share, but even if shares eventually reach that price, I'd advise against selling.

The next decade is shaping up extremely promising for STLA shareholders. Like its controlling families, I plan to hold Stellantis in my portfolio for the long term, as the company is making the right moves in evolving beyond car manufacturing.

Stellantis has published a long-term strategic plan, "Dare Forward 2030," in which the company highlights its vision of transforming into a sustainable mobility tech company, with electrification and software playing a pivotal role:

{kind=link}

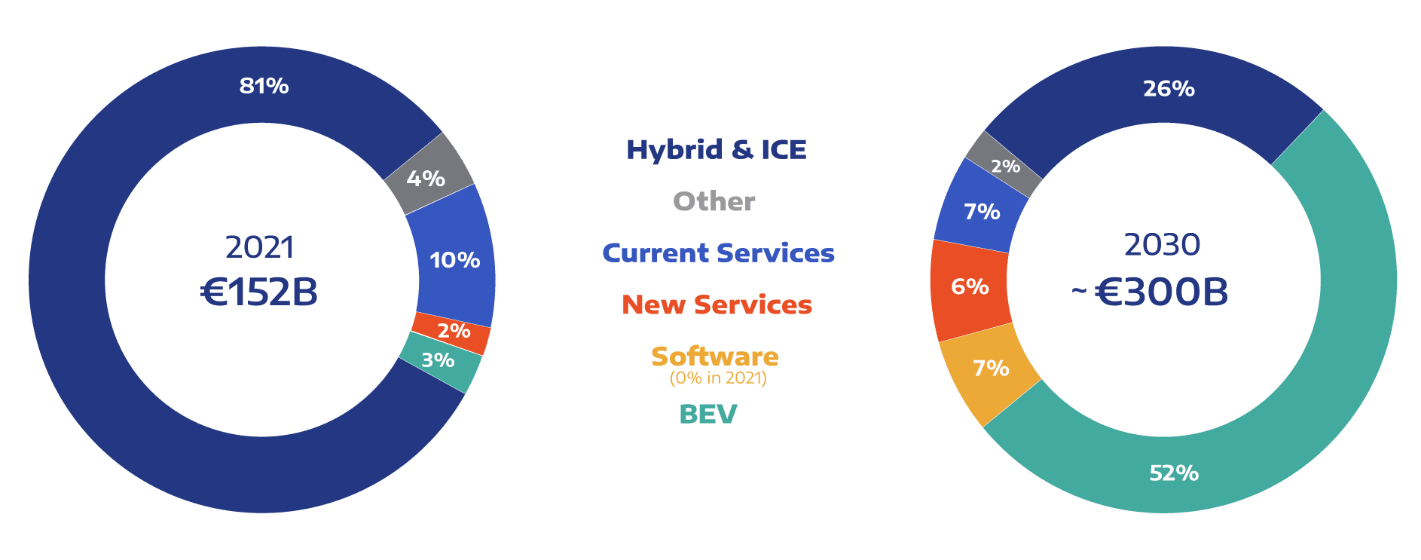

The company aims to double its revenue base by 2030, reaching €300 billion in sales. However, shareholders should not worry about profitability because Stellantis plans to double its industrial free cash flow and reach an FCF of €20.0 billion by the end of the decade, representing an 8% CAGR.

Can Stellantis get there despite the increasingly competitive space, with new EV makers trying to steal market share from the ICE incumbents?

I believe so. Stellantis' strategic vision for 2030 centers on two pillars: converting ICE sales to BEV and expanding service and software revenues. In particular, Stellantis expects to generate 20% of its total sales, or approximately €60 billion, from services, up from €18 billion in 2021.

Quietly moving behind the scenes, the spotlight perennially stolen by younger EV players and their CEOs, Stellantis has made significant moves to jump ahead of competitors. The company has been investing in new technology development centers, opening new ones in Europe and Asia just in the last twelve months, and signed strategic partnerships with Qualcomm ( QCOM ), Amazon ( AMZN ), and Waymo ([[GOOG]], [[GOOGL]]) to support its tech-fueled long-term strategic plan.

The Midnight Project

Stellantis announced back in January its commitment to support Archer Aviation ( ACHR ) in building the first commercially viable eVTOL aircraft, the Midnight. Under the agreement, STLA will contribute the necessary manufacturing technology, capital, and personnel.

With rising interest rates making access to corporate debt more difficult, Archer could need to raise additional equity to make it to the finish line, and STLA is keeping an opportunistic approach. On the one hand, Stellantis committed to extending $150M of equity capital for a potential draw by Archer at its discretion in 2023 and 2024. That represents approximately 12.5% of Archer's current valuation. On the other hand, the company also reportedly kept an interest in further purchasing ACHR shares on the open market. Fast forward six months and STLA quickly sealed the deal by disclosing a 10.6% ownership stake that sent ACHR stock flying well before its aircraft.

{kind=link}

We've been working closely with Archer for the past two years, and I am continually impressed by their ingenuity and unwavering commitment to deliver - Carlos Tavares, CEO of Stellantis.

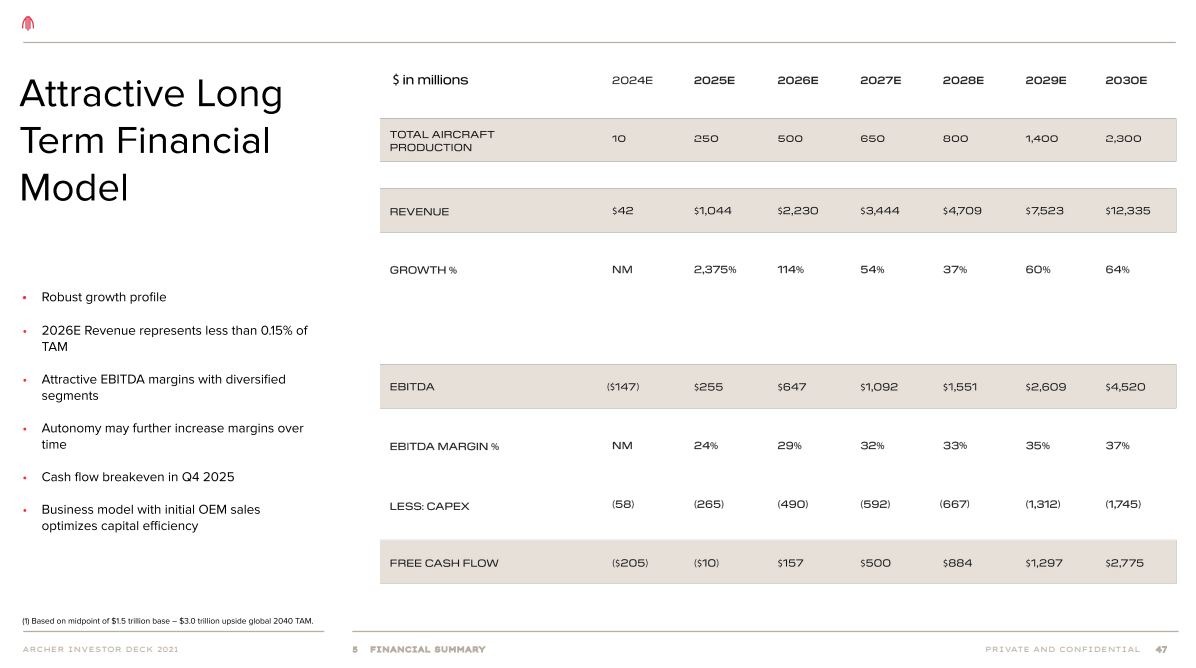

In its 2021 investors' deck, ACHR made bold financial predictions to reach approximately $12.3 billion in revenues, $4.5 billion EBITDA, and $2.8 billion FCF by the decade's end. With STLA ownership (acquired and committed) potentially already hovering around 20%, my bold prediction is that, before 2030, Stellantis could move in to own 50% of this company and proportionally consolidate results or even try to take it private, depending on how well things go with the Midnight.

{kind=link}

A 50% ownership would capture about $1.4 billion (€1.2 billion) of the projected free cash flow, representing 6% of Stellantis' forecasted total for 2030.

After all, it makes total sense to envision a future where the thin line between cars, hybrid flying cars, and aircrafts gets increasingly blurred, with the products being 100% electric. The big question to answer to unfold the revolution is one: who is the pilot?

An AI-powered revolution

While it may seem farfetched now, I do not think imagining AI taking over piloting functions in a decade or so is too much of a technological leap. Indeed, I'd expect the biggest hurdle to overcome in realizing such a scenario will probably be developing the related legislation rather than the technology. Autonomous driving (on roads) is already just a few steps away, but legislation is still lagging.

Potentially, here lie the advantages of AI-powered flying cars over "normal" ones. If the entire fleet had an AI pilot, there wouldn't be a need to regulate accidents between human-driven and AI-driven vehicles. Probably, road accidents could also become a thing of the past. DUI will not happen with AI. The change could happen much more quickly because while almost everyone has a driver's license and can drive a car just as well, not many people have a pilot's license to show for it.

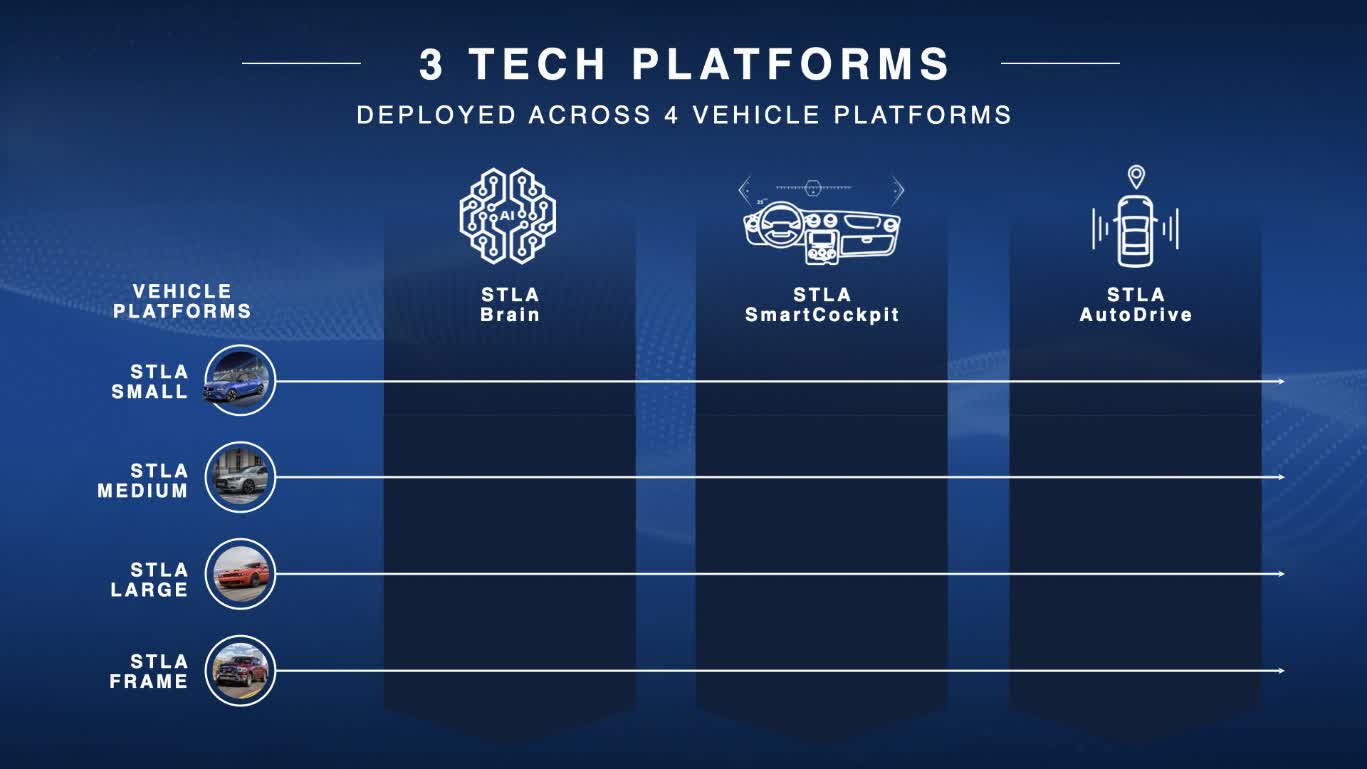

Even if autonomous driving has a slow adoption rate, it remains the first step toward an AI-driven future, and starting in 2024, Stellantis will begin deploying three all-new AI-powered technology platforms across its four global vehicle platforms:

{kind=link}

The centerpiece of the new Stellantis platform is the STLA Brain. This service-oriented architecture is entirely cloud integrated and allows real-time delivery of features and services through OTA updates. The chosen partner in cloud computing for this always-connected feature is Amazon. The STLA brain will integrate with the AutoDrive feature, which enables advanced driver assistance (ADAS) today and will allow for autopilot driving soon.

Stellantis has already tested the L3 autonomy level, driving nearly one million kilometers on public roads, and a broader roll-out of this autonomy level is scheduled for 2024. The next step is L4/L5 intelligent vehicles, for which the company is partnering with Waymo and BMW ( OTCPK:BMWYY ).

The third and final element of the new tech-driven Stellantis is the SmartCockpit, developed in partnership with Foxconn ( OTCPK:HNHAF ). I rate the partnership choice again top-notch, considering their experience with smartphones. After all, the SmartCockpit will likely evolve into an advanced entertainment system that also syncs with our other tech gadgets once AI does all the driving.

While waiting for AI-based piloting on flying cars, the SmartCockpit will use AI applications to deliver features and services such as navigation, voice assistance, e-commerce, and payment services. With all the moving parts coming together, I see how AI represents an opportunity for Stellantis here, and as a first step, it will help triple STLA service and software revenues by 2030.

Long-term valuation models

The Dare Forward 2030 financial assumptions are probably a good start to assess the full return potential of an investment in Stellantis:

{kind=link}

I don't think expecting STLA to trade at 7x-8x its 2030 FCF is preposterous. Even if the current 5x multiple seems frankly too low, not many automakers manage to steadily command a premium, with Ford ( F ) and Toyota coming to mind. However, with 20% of 2030 sales coming from SAAS/subscription software-based services, these steady revenues would naturally command higher multiples than cyclical hardware sales. Thus, I don't think such a re-rating would be a stretch. Considering that STLA has a net cash position, the market cap would be at least €160B, a 3x return toward $55-$60 per share.

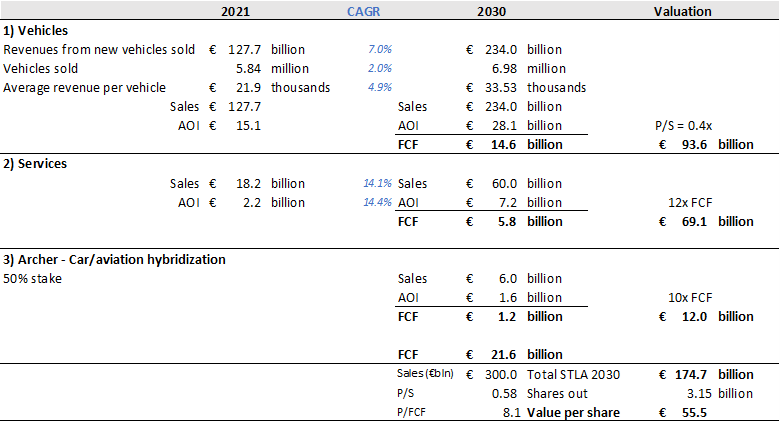

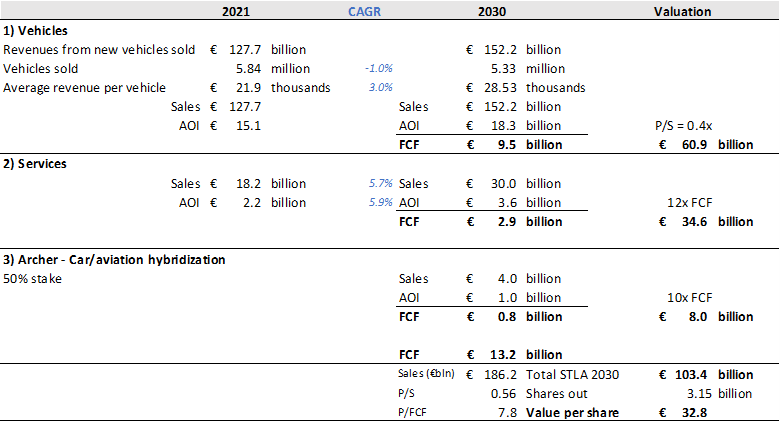

In my SOTP model, I tried to break down the value of the various moving parts, but I maintained the top-line assumptions of the Dare Forward strategy. The first part is the traditional auto manufacturing part, which should grow at a 7% CAGR through 2030. With €234 billion in sales and approximately €14 billion in FCF, I value this business division at about 6.5x 2030 FCF or 0.4x P/S.

The second moving part is the AI-enabled service division, which will grow at about 14% CAGR through the decade, eventually reaching €60 billion in revenues and almost €6 billion in free cash flow. I value this division at a modest 12x FCF or 1.15x sales and argue it will be worth about €70 billion.

The third and final part is the Archer investment/eVTOL business I discussed earlier in the analysis. The eVTOL opportunity is an optionality on top of the Dare Forward plan, which could increase the total FCF by about €1 billion and STLA valuation by €12 billion based on a 10x FCF multiple.

{kind=link}

According to this model, total STLA P/S would move towards 0.58x and P/FCF to about 8x in light of the increased weight of services and aviation.

The value per share would move towards €55.5 ($63) without even accounting for the share repurchase plans that STLA has been carrying, which I expect, at a minimum, to cancel out any effect of share dilution. Still, it could potentially propel total return even higher.

The presented bull case for Stellantis implies that if everything goes well, investors could book annualized total returns through 2030 of 25%-30% as the sum of dividends (currently 8% yield), growth (8%, in line with FCF growth as STLA will continue to pay out DPS as a fixed proportion of FCF to shareholders) and 10%-15% share price appreciation on top, coming from valuation multiple expansion and realignment to fair value. While this is a massive upside, it is far from devoid of risks.

Downside risks

I see substantial execution risks for STLA on its way to achieving €60 billion in revenues from services and software by 2030. While STLA already earns a decent amount from financing and AS services (under the "services" categories in the 2021 pie graph, representing 12% of the total), the current software revenue is zero. Although heavy investments should eventually start to pay off, the company has a long way to go.

Competition in the automotive space has always been fierce. For some context about how difficult it is to succeed in this industry: before becoming FCA, Fiat was a severely distressed business , and in 2004 the company was about to sell out to General Motors ( GM ). Fiat eventually became Chrysler's owner (and transformed into FCA Group) because the Detroit firm filed for Chapter 11. As already said, PSA Group, before Tavares, was also on the brink of bankruptcy.

Incumbent ICE players who have survived the M&A frenzy have recently enjoyed several years of robust margins. However, a new wave of pure-EV competitors, led by the apparent frontrunner Tesla ( TSLA ), has emerged and will again put incumbent players to the test. Stellantis owns several appealing brands, although it arguably lacks a leading brand with worldwide recognition. Even for STLA brands well positioned in both NA and Europe, like Jeep, these generally lack the depth of rivals, focusing on one market segment (e.g., SUVs and Crossovers in Jeep's case). The company entered the post-merger phase with 14 brands, to which Tavares has pledged support for the rest of the decade:

{kind=link}

Arguably, struggling brands, such as DS and Lancia, will have a hard time surviving beyond 2030. For others, like Chrysler and Vauxhall, they are also most likely a "maybe." [For more info about STLA brands and their long-term survivability chances, readers may find an interesting Reddit discussion here ].

In my opinion, the situation is not overly concerning but, at minimum, contributes to creating a sub-optimal situation in which marketing efforts are fragmented, must be geographically targeted, and can't be as effective globally as STLA's competitors.

The forecast I presented expects overall sales volumes to increase by 2% annually through 2030. I set the bar relatively low and believe STLA could attain such growth without stealing market share from the competition. On the plus side, I think the correct execution and revamping of brands such as Maserati and Alfa Romeo could offer some upside. Conversely, an apparent threat is coming in the BEV space from brands such as Tesla that could dilute STLA's market share. There is also some risk in expecting pricing to firm up at a CAGR of 5%, especially with inflation cooling off, but with the increasing amount of technology incorporated into new vehicles, it is foreseeable that future car purchases could take up a slightly higher fraction of the households' budget. Regardless of its theoretical viability, a 7% CAGR scenario should be considered a bullish scenario that may not come to light. But here comes the beauty of this stock: even by stress-testing it with much more baseline assumptions, STLA still comes out as a decent investment:

{kind=link}

Under this bearish scenario, I calculated volumes to fall by 1% and pricing to grow more in line with inflation, resulting in a sales CAGR through 2030 of only 2%. Service revenues only grow at a modest 6%. Considering the CAPEX to develop AI-powered services poured in by STLA to increase these numbers, that would be a disappointing result. Also, I reduced sales and valuation gains from the Archer ownership stake by 1/3.

Still, even after all these negative adjustments, I can see a path for Stellantis to return an annualized 10.5% to buy and hold investors from its 8% dividend yield and 2.5% FCF CAGR, and that still disregards any capital gains from a sale. However, the share price could almost double from €16.6 to €32.8.

Conclusions

Despite the challenges, Stellantis is an incredible cash machine today. The company has one of the best margins in automotive and has a solid balance sheet with negative net debt, yet trades at extremely cheap multiples despite the obvious positives.

I like the investment case here a great deal and assign a "Strong Buy" rating to STLA shares. While the short-term target could be €25, I am more interested in this company's long-term attractive total return potential. Even if the company achieves mediocre results, trims some brands, and grows mainly through pricing, shareholders should see attractive returns from the high dividend yield and modest free cash flow growth. STLA shares are cheap and unloved today, arguably because the company lacks a global brand in its portfolio capable of catalyzing attention. Nevertheless, most of Stellantis' brands are quite attractive at a regional level, plus some long shots that still have a fan base among motor enthusiasts could see a comeback.

The significant upside comes from Stellantis' focus on transforming itself into a mobility tech company and the €60 billion revenues from services it envisioned in its 2030 strategic plan. If STLA successfully transitions to this new growth phase, I believe there could be "blue skies ahead." This reasoning comes from my belief that, in the 2030-2040 decade, AI and eVTOL will likely fuel the "real" revolution in e-mobility. I expect AI-piloted eVTOL technologies to rapidly mature and become available for the upper middle class (probably the top 10% of earners). Stellantis seems to be playing chess with the competition playing checkers, pushing ahead with smart investment decisions, and enjoying a significant first-mover advantage when the time comes.

If that goes as planned, STLA shares could really take off by then.

Editor's Note: This article was submitted as part of Seeking Alpha's Best AI Ideas investment competition , which runs through August 15. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Stellantis: Buy For The Income, Hold For The AI-Powered eVTOL Revolution