OCSL - Stellus Capital's 13% Yield Might Not Be As Safe As It Looks (Downgrade)

2023-12-05 00:21:38 ET

Summary

- Stellus Capital Investment Corporation has comfortably covered its dividend with core net investment income in Q3.

- The BDC's net investment income is expected to decrease next year due to changing rate policies, potentially leading to a lower dividend margin of safety.

- Stellus Capital Investment's large percentage of assets invested in floating-rate loans poses a risk in a low-rate environment, potentially impacting its dividend.

Stellus Capital Investment Corporation ( SCM ) covered its dividend as comfortably with core net investment income in the third quarter as it did throughout the last year.

Even though the BDC’s per share net investment income has gone up a whopping 40% YoY, thanks to higher interest rates in the U.S. economy, Stellus Capital Investment is probably going to see lower net investment income next year as the central bank’s changing rate policy is set to hurt particularly floating-rate BDCs.

Though Stellus Capital Investment’s dividend coverage looked solid in the last two quarters, the BDC might see a net investment income contraction and a lower dividend margin of safety next year. This might be reflected in a higher net asset discount as well.

My Rating History

If you go back to my last article on Stellus Capital Investment, I pointed to strong dividend coverage, a generous dividend raise, and net investment income upside in a rising-rate environment as reasons to buy the BDC’s 11.2% yield.

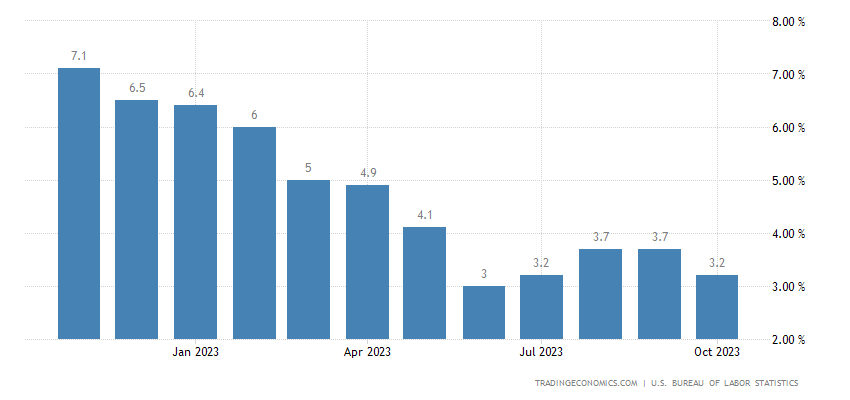

Taking into account that inflation in the United States fell from 3.7% in September to 3.2% in October, the central bank is probably set to bring the present rate-hiking cycle to an end very soon.

Thus, net interest income upside, from this point onwards, might only be driven by new investments rather than floating-rate loan interest resets.

Floating-Rate Exposure May Now Be A Risk

One reason I cited to buy Stellus Capital Investment, in addition to the others named above, was that the BDC had a First Lien investment portfolio that provided downside protection in a recession. This did not substantially change in the last two quarters that have passed since I covered Stellus Capital Investment and the portfolio structure itself would continue to support this argument.

In 3Q-23, Stellus Capital Investment was predominantly invested in Senior Secured First Liens which accounted for 90% of all investments on a fair value basis. Including the Second Liens in the BDC’s total Senior Secured investments yields a percentage representation of 92%.

Senior Secured First Liens (Stellus Capital Investment Corp.)

{kind=link}

However, what is driving my rating change here is that Stellus Capital Investment had 98% of its assets invested in floating-rate loans which are not great assets to hold on the balance sheet in a low-rate environment.

Inflation has cooled down substantially in recent months, at least compared against the year-ago period, which creates earnings and dividend risks for Stellus Capital Investment that passive income investors must include in their investment calculus.

{kind=link}

Why I Think Stellus Capital Investment’s Margin Of Dividend Safety Is Set To Diminish

Stellus Capital Investment is a floating-rate-focused BDC, a feature that strongly works in favor of the company’s net investment income during a rate-hiking period.

Stellus Capital Investment earned $0.49 per share in net investment income in 3Q-23, reflecting a huge 40% YoY growth rate (SCM earned $0.35 per share in core net investment income in last year’s third quarter). This growth in net investment income is primarily due to Stellus Capital Investment’s floating-rate exposure.

With that being said, though, the company raised its dividend by ~43% in the last year so this growth in net investment income has been passed through to investors.

As a consequence, Stellus Capital Investment’s dividend payout ratio has remained fairly stable at ~80%. Though Stellus Capital Investment has a decent margin of safety embedded in its pay-out ratio, a contraction of the BDC’s net investment income in a low-rate environment might pressure its dividend in 2024.

Dividend (Author Created Table Using BDC Information)

Peer Valuation And Discount To NAV, Investment Plan & Recommendation

BDCs are valued primarily based on net asset value. Stellus Capital Investment reported a net asset value of $13.19 per share for the third quarter which implies, taking into account a present stock price of $12.83, a NAV discount of 3%.

Though a discount to net asset value implies a potential undervaluation, I think that the market is just at the brink of pricing in weaker net investment income prospects into Stellus Capital Investment’s stock.

My recommendation for passive income investors would be to underweight those BDCs that have a large percentage of their assets invested in floating-rate loans, such as Stellus Capital Investment.

Since most BDCs have a significant floating-rate investment allocation, I think the best BDCs to invest in are those that have a history of producing strong returns even in low-rate environments, like Ares Capital ( ARCC ) and Oaktree Specialty Lending Corp. ( OCSL ) .

My personal investment plan with respect to Stellus Capital Investment includes down-ranking SCM from Buy to Hold. Secondly, I would only consider SCM as a Buy at a 15% discount to NAV which leads us to an implied buy point of $11.21 (13% downside).

Taking into account that the end of the rate-hiking period would probably also lead to higher NAV discounts (reflecting higher NII risks), I think that passive income investors will soon start to demand higher margins of safety in order to buy BDCs.

Why I Might Be Wrong About Stellus Capital Investment

Should inflationary see a resurgence again in the next couple of months, then the central bank might decide to keep interest rates at the current rate range of 5.25-5.50% for longer. This would invalidate some of the points I made in this article.

With that being said, though, I think the underlying premise of a growing probability of a cyclical net investment income contraction remains valid.

My Conclusion

Stellus Capital Investment is a First Lien-focused BDC with rather good dividend coverage. The focus on high-quality First Lien debt is particularly valuable during recessions when loan problems tend to rise, but the very large floating-rate exposure of Stellus Capital Investment’s portfolio is a potential problem.

With inflation moderating quite substantially in the last year, I think that the floating-rate exposure of 98% strongly tilts the odds in favor of cyclical net investment income declines next year. Thus, the discount to NAV may expand and dividend risks may grow moving forward. Hold.

For further details see:

Stellus Capital's 13% Yield Might Not Be As Safe As It Looks (Downgrade)