STEM - Stem: Despite An Expanding Industry Trend It Continues To Lose Money

2023-05-02 14:01:04 ET

Summary

- Stem recently increased its debt burden with a new bond issue.

- Part of the new debt will pay off a cheaper-to-finance old debt.

- The company has increased revenues since 2018, but has also continuously increased losses.

Stem (STEM) was incorporated in 2009; I say that because when I first saw its books, I thought it was a start-up. This company has been losing money consistently for the past five years. It's what you might expect from a company in its early stages.

What's worse, in my opinion, is that it has been consistently increasing revenue yet still manages to increase its losses also. And to add to that, in an industry that has seen a positive growth trend. Some alleviation may come from the fact that most forecasts for the industry see substantial growth through 2030.

However, I personally doubt the company would be able to make anything of it, given its track record over the past five years. This looks like the type of company an activist hedge fund would do handsomely with if they targeted it.

Let’s have a closer look at why I believe this company is a sell from a fundamental analysis.

New Debt Burden

There are several reasons a company may take on new debt . In any of those cases, it will almost always dilute shareholder value. The most consistent reasons I know of are:

- To refinance maturing debt.

- To take advantage of favorable market conditions to refinance debt.

- To raise funds needed for new capital expenditures.

- To raise capital for unforeseen operating expenses.

From what I see, the reason for this new round of debt has nothing to do with any of the above. First, I'll mention what I believe to be STEM's objective with this round of $200 million in debt. Then I’ll discuss why I believe they really issued this round.

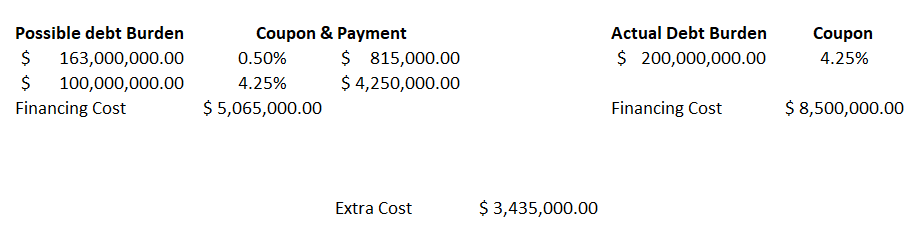

The reason I mention this new round of debt is two-fold: the new debt will pay off an old but much cheaper debt, and the rest will be used for operations, less $23 million for capped call transactions. The new debt of $200 million will mature in 2030 and cost the company 4.25% in coupons.

The company will use $100 million of the net proceeds to buy out $163 million of previously issued debt at 0.50%, which matures in 2028. I would guess their objective is to lower the debt burden, as they are using $100 million to reduce it by $163 million.

Under this scenario the company’s debt will be $200 million. If the company had kept the old debt and issued new debt for just $100 million they would have had a total debt of $263 million ($163 million old debt + $100 million new debt). That seems like an adequate move, reducing liabilities and improving the overall long-term debt burden.

However, it comes at a cost. The $163 million had a financing cost of 0.50%, while the new debt to pay that off costs 4.25% in coupons. If they had kept the old debt of $163 million maturing in 2028 and only issued $100 million, they would be paying much less in financing their debt.

Unless my math is wrong, the company now faces an extra $3.4 million in financing costs annually. The arithmetic is simple and hopefully clear from the image below.

STEM Debt Costa (SeekingAlpha)

{kind=link}

That’s an extra $3.4 million in costs for a company that has been in the red and going deeper for the past five years. This begs the question, why would the extra cost of financing a smaller debt burden be justified?

My only answer is that they believe they may not get financing later down the road if they are carrying too large an amount of debt, which may be prudent in this case because it looks to me like they are going to need it.

STEM Fundamentals

The outlook for this company using the metrics I analyze is nefarious, to say the least, except for the liabilities to assets ratio. I look at revenue, EBITDA, EPS, cash flow, and the debt ratio I just mentioned.

Growing revenue is a must; it's how a company can increase earnings. However, this company has seen increased revenue over the past five years with negative and decreasing earnings. In the table below, we can see how the company has managed to increase revenue consistently.

SeekingAlpha

In fact, 2022 shows a nearly 3 times increase in revenue over 2021, yet EBITDA still turned more negative. I'm not looking at EPS as it's negative, and from what I see in various sources, it doesn't make sense. Let’s consider how revenue has gone from $7 million in 2018 to $363 million in 2022, while EBITDA has plunged from a loss of $37.5 million to a loss of $76.3 million.

So, where is the money going? I thought it might be in CAPEX, but I see that CAPEX/sales TTM is only 1.13%. If STEM was investing a large portion of its earnings in capital expenditures, I have a feeling that number would be way higher.

The only positive metric I see is the liabilities to assets ratio, now at 0.61, and more importantly, it has been coming down since its high in 2020 at 1.4. That number just about sums up the value of STEM at the moment.

Industry Trend

The industry trend for both energy management software and renewable energy storage are both positive and have high growth forecasts. This seems to worsen the situation, as I wonder how a company in this industry can lose money so consistently.

As an afterthought, it does offer the hope that they can turn things around and profit from an expanding industry. But it’s a hope, and I don’t believe things will change unless there is a change in management.

MordorIntelligence

The energy storage industry, which includes batteries and other segments, is expected to have a CAGR of 19.9% from 2019 to 2027. The global market was worth $10.37 billion in 2020 and is expected to be worth $37.06 billion by 2027.

The global energy management software industry is expected to grow by 16.2% from 2017 to 2032. In 2020, the global market was valued at $36.2 billion and is expected to rise to $161.9 billion by 2030.

From what I have seen from these reports, the industry STEM is dedicated to seems healthy, has been growing over the past years, and is forecast to expand by double digits over the following years. This fact makes me even more skeptical about the ability of this company to produce profits.

If it hasn’t managed that for several years in a healthy environment, why would that habit change? And for what reason would there be a catalyst?

Conclusion

On May 4, we will get STEM's earnings report for Q1 , which will be interesting to see. I expect a sharper drop than the expected negative number. Other analysts are also downgrading STEM, such as Wolfe and BofA . I know you may have seen it; I'm just adding voices to my call.

To me, this company is worth its assets of $1.4 billion minus its liabilities of $869 million, which equals $531 million. Divided by the number of shares, 155,552,000 gives a value of $3.41 per share. Considering the progression of the previous five years, I believe that the market would price in further poor performance, making the market price of STEM even lower.

This may seem a very simple model to value a company, but as it has been generating negative earnings and is likely to continue doing so, I only see some value in this aspect.

For further details see:

Stem: Despite An Expanding Industry Trend, It Continues To Lose Money