STEM - Stem: Energizing Growth Yet Draining Cash

2023-11-07 11:26:11 ET

Summary

- Stem, Inc. is a cheap stock in the growing smart energy storage industry, with a projected market size of $31.20 billion by 2029.

- The company has a strong customer base and has shown revenue growth, but faces challenges with cash flow and increasing debt.

- While Stem has potential in the market, there are less risky alternatives, and it is recommended to wait and see financial improvements before investing.

Stem, Inc. ( STEM ) is a small-cap company specialising in smart energy storage through its hardware and software offerings. The company is known for its prolific customer base and award-winning products targeting a multi-billion dollar growth industry . However, over the last year, it has faced a considerable drop of 70.80% in value. The most recent Q3 2023 earnings report showed a shortfall, missing both EPS and revenue expectations and lowered its guidance for FY 2023. Additionally, in just the last day, the stock experienced a further 8.3% decline in its value.

{kind=link}

Although the recent downward trend appears concerning, it seems the market may have overreacted. In Q3 2023, the company saw a significant YoY increase in its top line by $134 million and achieved a record in bookings at $676 million. With potential benefits from the long-term Inflation Reduction Act tailwinds and consistent growth in recurring annual revenue, there's a promising spot for Stem in this vast yet increasingly competitive market. However, the company grapples with mounting cash burn, increasing debt, and a delay in its expected profitability date. Considering this, some other companies in the industry might offer less risk at the moment. Therefore, I recommend a wait-and-see-hold approach.

Company overview

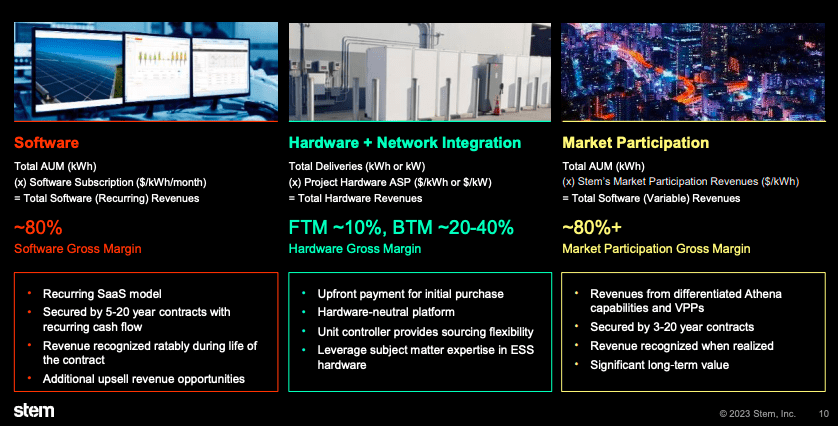

Stem has pioneered hardware and AI-driven software to optimise lithium-ion batteries, enhancing their efficiency and enabling more affordable and resilient connections with electricity grids. What truly validates Stem's prowess is not just its cutting-edge technology but also the strong backing from top-tier customers, investors, and a proficient management team, further substantiated by its rapid revenue growth.

{kind=link}

Key investors, including General Electric ( GE ) and Blackstone ( BX ), signal strong support for Stem's trajectory. The company is strategically shifting focus towards high-margin software and services from hardware-dominated sales. This move is already evident in the notable 43% year-over-year increase in Contracted Annual Recurring Revenue in Q3 2023.

While competition is intensifying, the market potential remains vast, accommodating players like Fluence ( FLNC ), Wartsila ( WRTBF ), and Tesla ( TSLA ). Stem's differentiating focus is small energy generation and storage, as opposed to the utility-scale energy storage of it peers. Notably, the explosive 400% growth in the Chinese market could influence the global landscape if international competition intensifies. While Chinese peers may compete on pricing, US-based companies stand to gain from clean energy legislation, acting as a positive force.

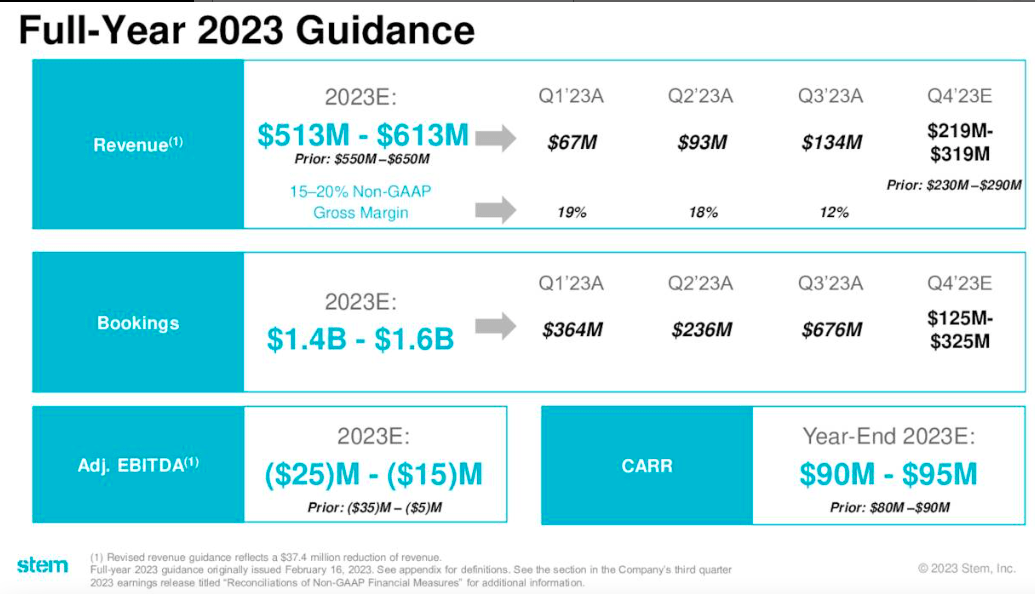

Looking forward, Stem has revenue potential from a recent $1 billion booking contract from entering municipal and cooperative markets. For the next quarter and full year 2023, the company has decreased its forecast with a revenue projection ranging from $513 million to $613 million, and it has delayed its profitability projection into FY2024.

{kind=link}

Financial highlights

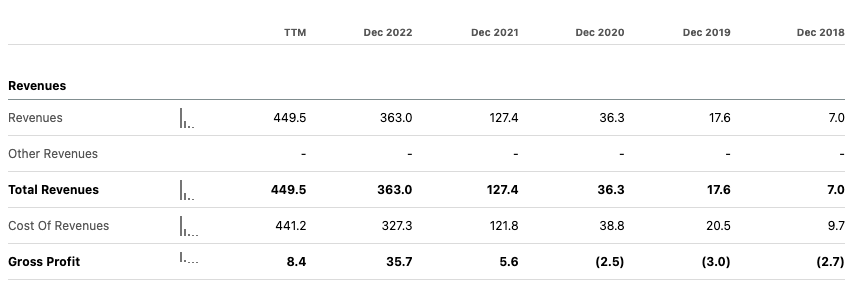

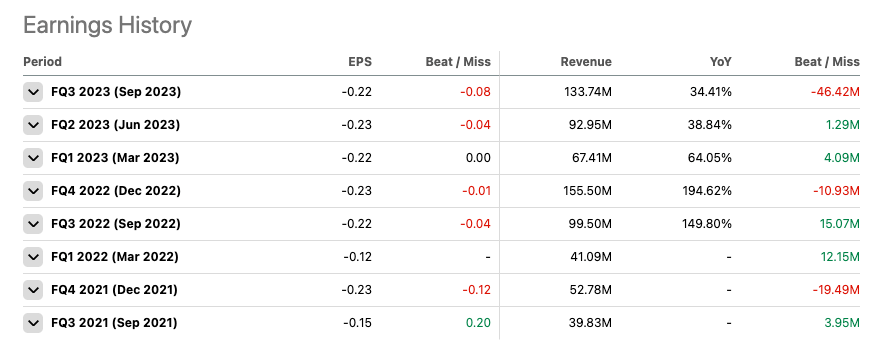

Stem missed EPS and revenue expectations in its most recent quarterly report. It reported a 2023 Q3 GAAP EPS of -$0.49, misses by $0.30, and although revenue increased YoY by 34.4% to reach $133.7 million, it missed expectations by $46.46 million. However, if we look at the progress YoY since going public, we see impressive top-line growth, at $449.5 million TTM and expected revenue for the FY of around $513 million. The gross profit margin has been less consistent and declined to TTM $8.4 million, which is a concern. However, the company is increasing its SaaS contracts, which should improve future margins.

{kind=link}

In terms of Adjusted EBITDA, there's been a notable improvement, nearly reaching breakeven at around negative $900,000 compared to a negative $13 million in the same quarter last year. However, examining the company's quarterly earnings per share reveals that it's yet to achieve positive results, having missed expectations in two out of the last four quarters.

{kind=link}

Balance sheet and Liquidity

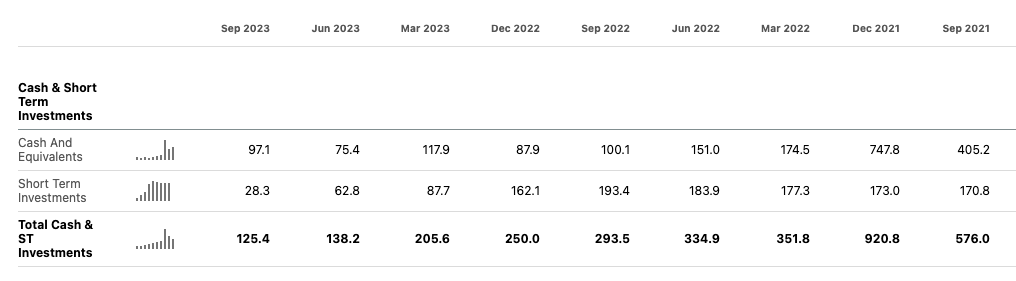

Assessing the financial stability of a growing company involves critically evaluating available cash for reinvestment. We can see that Stem has been burning through its cash and taking on more debt, which is a risk for the business if it does not manage to increase its operating income.

{kind=link}

In Q3 2023, the company held $97.1 million in cash, $28.3 million in short-term investments, and a net working capital of $241.3 million. The company has a credit agreement of $2.7 million. Furthermore, it has senior notes due in 2028 of $163.0 million and another senior note worth $232.4 million due in 2030. If we compare the company to larger-scale energy storage-providing companies, it has a high debt-to-equity ratio of 133.65%, making it look more risky than alternatives.

Balance sheet versus peers (seekingalpha.com)

Valuation

Stem's stock hasn't surged past the $10 mark since January 2023 and has faced a significant 70.80% decrease in value over the past year. While the stock might seem appealing due to its lower price compared to other energy storage peers and its promising growth potential, there are a few red flags worth considering. It's essential to approach with caution, given Stem's challenges with cash burn, mounting debt, and the persistent absence of positive earnings, repeatedly postponed during earnings calls. If we compare Stem's price to sales ratio of 1.27 to that of Fluence, there's an interesting observation. Fluence, like Stem, hasn't generated profits yet, but it appears relatively more undervalued. Furthermore, Fluence shows improving earnings , a more appealing gross profit margin, and stronger growth in its top line, boasting a healthier balance sheet in comparison.

Relative peer valuation (seekingalpha.com)

Profit versus peers (seekingalpha.com)

{kind=link}

Risks

Stem is encountering challenges in delivering positive earnings, has negative cash flow and has increased its debt intake which is a concern for potential investors. Despite being in a growth phase, the company has yet to demonstrate significant EPS improvements over the last seven quarters. This trend raises concerns about its ability to convert rising revenues into profits. The energy storage sector has rapidly evolved, witnessing a transition from few to numerous competitors, particularly from the expanding Chinese market, which experienced a remarkable 400% growth in 2021. This shift in the landscape and increased competition could lead to pricing pressures, potentially affecting Stem's market share and its profit-generating capacity.

Final thoughts

Stem is known for its solid customer base and award-winning products. It has been growing its top line and increasing its recurring revenue service contracts, which have more attractive margins than its pure hardware sales. Furthermore, the company has reported record-breaking bookings, which should benefit the company in the future. Yet, despite these strengths, the stock hasn't yielded the desired returns for early investors. The company's track record lacks positive earnings or cash flow. Although there's an anticipated positive turn in earnings for FY 2024, a similar projection for FY 2023 didn't materialise. I believe there are less volatile and more promising growth opportunities within this industry. Therefore, I recommend adopting a wait-and-see approach, holding off for now.

For further details see:

Stem: Energizing Growth, Yet Draining Cash