STEM - Stem: Revenue Surge Fatter Margins And War

Summary

- Stem just reported fiscal 2022 fourth quarter earnings that saw revenue grow by nearly 200% over its year-ago quarter.

- Profitability improved markedly with gross margin coming in at 8%, up by 1100 basis points.

- Subsidies, the energy crisis, and Russia's war in Ukraine will continue to see the uptake of solar energy ramp up.

Stem's ( STEM ) earnings continue to impress with hyper-growth on the back of the green transition now inherent in the operational momentum of the smart energy storage firm. The figures for its recently reported fiscal 2022 fourth quarter were strong with revenue surging by nearly 200% over its year-ago comp and gross profit margins recording a positive 1100 basis points move. The ramping figures have been set against the backdrop of commons that whilst up 15% year-to-date are down 46% from their 52-week high.

I'm bullish on STEM stock and believe the green transition presents a strong opportunity to invest in the reconstruction of the global energy architecture around an electrified lower carbon and ultimately more sustainable footing. Critically, Stem now stands to be boosted by adjacent multi-decade themes that have turbocharged the green transition and have essentially knocked years off the timeline for the adoption of solar energy.

Revenue Growth Comes In Strong As Profitability Expands

Stem reported revenue of $156 million for its fiscal 2022 fourth quarter, a growth of 196% over the year-ago period but a miss on consensus estimates for revenue of $166.43 million. Bookings grew by 111% year-over-year to reach $458 million with contracted backlog growing by 116% to reach $969 million from the year-ago figure.

{kind=link}

Stem

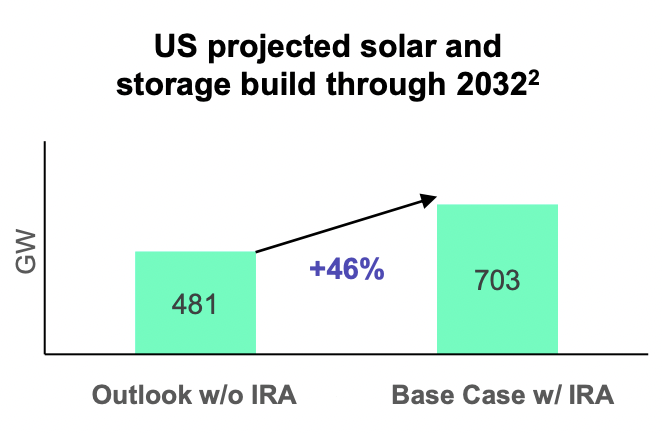

At the core of this growth is the rapid buildout of solar and storage as the production tax credit provided by the Inflation Reduction Act ((IRA)) gears up to work its way to disperse and derisk planned investment capital in the green energy source. Stem now expects the IRA to increase solar plus storage by 46% through 2032, a move that would underlie the growth of the company's Athena software business.

The company faced some supply chain issues during the quarter with interconnections and permitting remaining slow just as labour availability issues for its partners also came into the dynamic. GAAP gross profit margin came in at 8%, up from negative 2% in the year-ago period as higher margin service revenues moved to constitute a larger share of total revenue. Contracted annual recurring revenue grew to $65 million, sequential growth of 7% over the third quarter on the back of software and services revenue of $16 million during the fourth quarter. This represented around 10% of total revenue and is set to move higher in the coming earnings.

{kind=link}

Stem

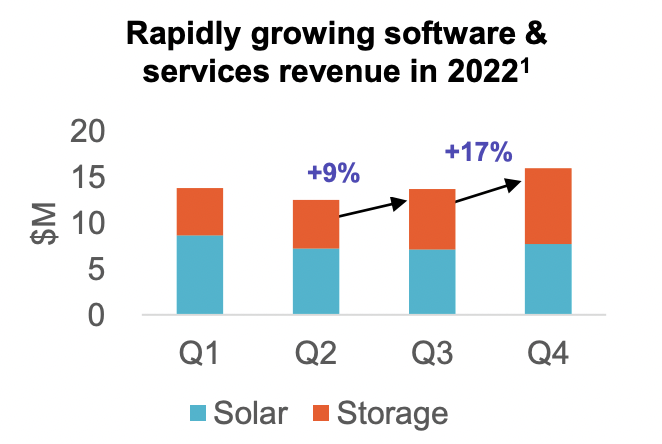

Athena, Stem's AI-driven battery optimization software platform, lays at the heart of the company's long-term bull case. This segment will do most of the heavy lifting for gross profit expansion and eventual positive cash flows. Hence, its quarter-on-quarter growth rate will be the key driver of Stem's ability to build future shareholder value. Growth sped up sequentially, growing by 17% over the third quarter from a growth of 9% over the second quarter. The company also completed its first FTM software-only project in ISO New England and stated it intends to chase more of these types of deals in the future.

The Green Energy Adoption Has Been Brought Forward

Stem's net loss fell by around $1 million from its year-ago figure to reach $35 million with adjusted EBITDA negative at $10 million. This was down from a negative adjusted EBITDA of $12 million in the year-ago period. The results were healthy with enhanced operating gearing allowing for a lower net loss even against higher revenue. However, the commons are currently down around 7% in pre-market trading as investors react negatively to the revenue miss. This is understandable as underperformance of expectations by a high growth ticker is almost always met with a reset of initial expectations. This will continue to form a key risk for Stem. However, I think this misses the larger picture around the changes the company is making to its business to embed greater profitability whilst riding the larger and fast-expanding TAM for smart energy storage.

The company ended the quarter with cash and equivalents at $250 million, around 16% of its current $1.58 billion market cap. This came as management in their earnings call for the quarter guided for fiscal 2023 revenue to come in at around $650 million at the top end to place their forward 1-year price-to-sales multiple ((PS)) at 2.43x. This is against a PS ratio of 4.35x against the full-year fiscal 2022 revenue of $363 million.

Critically, the shift to renewable energy is now codified in US legislation through the Inflation Reduction Act with demand further brought forward by Russia's war in Ukraine. The conflict and subsequent energy war have highlighted the need to shift from a mine-and-burn hydrocarbon economy to a more sustainable low-carbon green energy economy. I remain bullish on Stem and think exposure to the growing market for energy storage forms an important and overlooked component of the green transition. The company fits within my climate economy portfolio well and will form a long-term hold as the transition takes root.

For further details see:

Stem: Revenue Surge, Fatter Margins And War