FSI - Stepan Company: A Downward Revision Is Warranted

2023-06-09 07:35:27 ET

Summary

- Stepan Company has been downgraded from 'buy' to 'hold' due to recent financial weakness and decline in sales volumes.

- Despite higher pricing, profits and cash flows have tumbled for the company.

- This increases the risk for shareholders and has caused me to re-evaluate the business in a way that incorporates new developments.

In an ideal world, every investment that you choose to buy would turn out to be profitable. But we unfortunately don't live in such a world. I suppose the good side to this is that it keeps things interesting. But interesting does not pay the bills. One firm that I did not buy shares of, but did previously rate a 'buy' that has not turned out exactly as planned is Stepan Company (SCL), a producer and seller of surfactants, polymers, and other specialty products such as those that are found in food and flavoring products. Despite having a rather stellar 2022 fiscal year, the company has shown weakness as of late. This weakness occurred on both the top and bottom lines. In the event that financial performance does revert back to what it was in prior years, shares would have a bit of upside from here. But given the change in fundamental condition for the firm, I believe that a downgrade to a 'hold' rating is appropriate at this time.

Assessing recent weakness

So far, Stepan Company is not off to a particularly good start this year. But earlier in the year, I thought that things were looking up. In an article that I published on the company in January, I discussed how sales and profits were doing quite well leading up to that point. This, combined with how cheap shares looked, led me to rate the enterprise a 'buy', a rating that reflected my view at the time that shares should outperform the broader market for the foreseeable future. Sadly, that did not come to pass. Even though only a few months have gone by since then, shares have seen downside of 5.4% at a time when the S&P 500 is up 10.7%.

{kind=link}

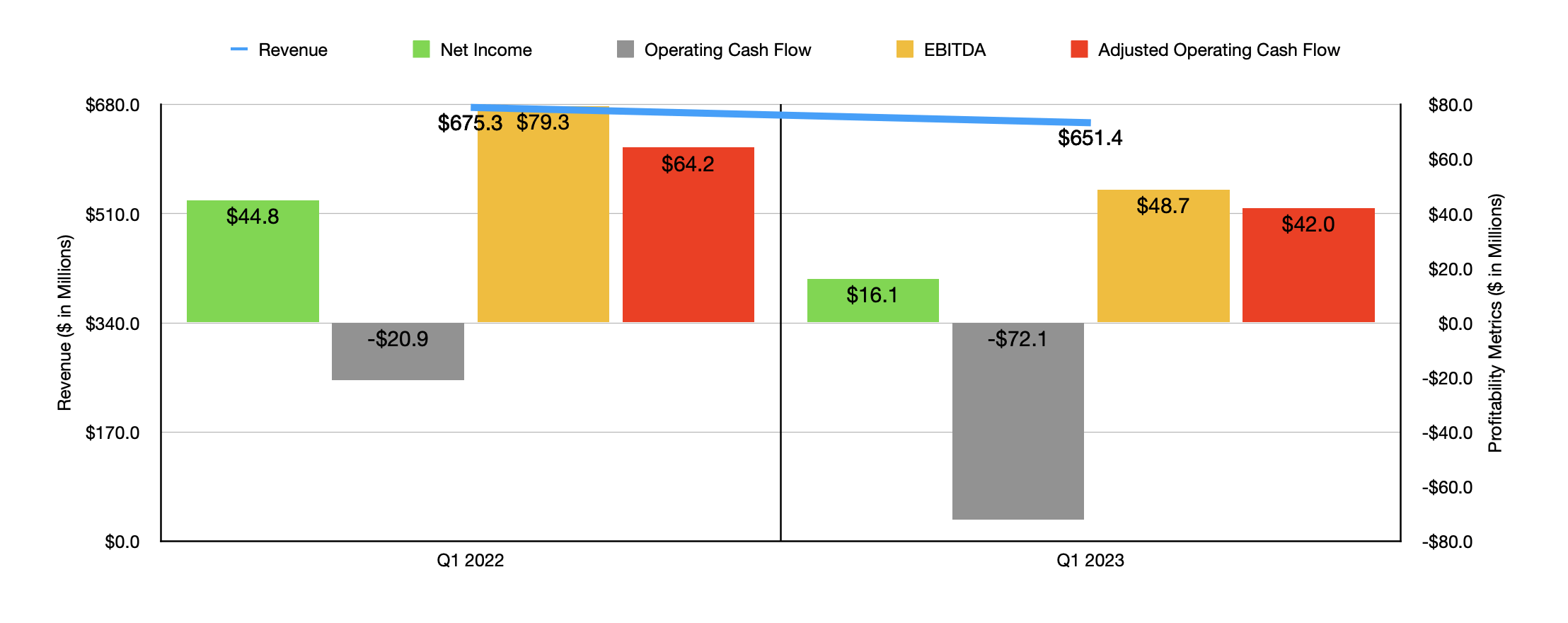

I am seasoned enough in the markets to know that, even when fundamentals are going right, market sentiment can cause share prices to move in the opposite direction of what you think they should for a time. But that is not what is occurring here. The fact of the matter is that the most recent financial data provided by management casts the company in a slightly less bullish light than what I saw when I analyzed it last. For the first quarter of the 2023 fiscal year, for instance, revenue came in at $651.4 million. That's a decline of 3.5% over the $675.3 million the company reported one year earlier. A little over half of the $23.9 million decline, $12.5 million in all, was caused by foreign currency fluctuations. But there were other contributors as well.

Overall product sales volumes, for instance, plunged 14%, negatively affecting revenue to the tune of $97.6 million. Polymers were especially problematic, with revenue in the Polymer segment plunging 18% year over year. Management attributed this decline to lower market demand and customer and channel inventory destocking activities. The picture would have been worse had it not been for the fact that higher pricing positively affected sales by $86.3 million.

In my mind, I don't have a problem with sales volume dropping. But to see sales volume drop enough that, even after ratcheting up pricing, you end up with profits and cash flows worsening, that becomes an issue. And that is exactly what we saw during the most recent quarter. Net profits fell from $44.8 million in the first quarter of 2022 to only $16.1 million in the first quarter of this year. Operating cash flow went from negative $20.9 million to negative $72.1 million. Even if we adjust for changes in working capital, it would have gone from $64.2 million to $42 million. Meanwhile, EBITDA for the company declined from $79.3 million to $48.7 million.

{kind=link}

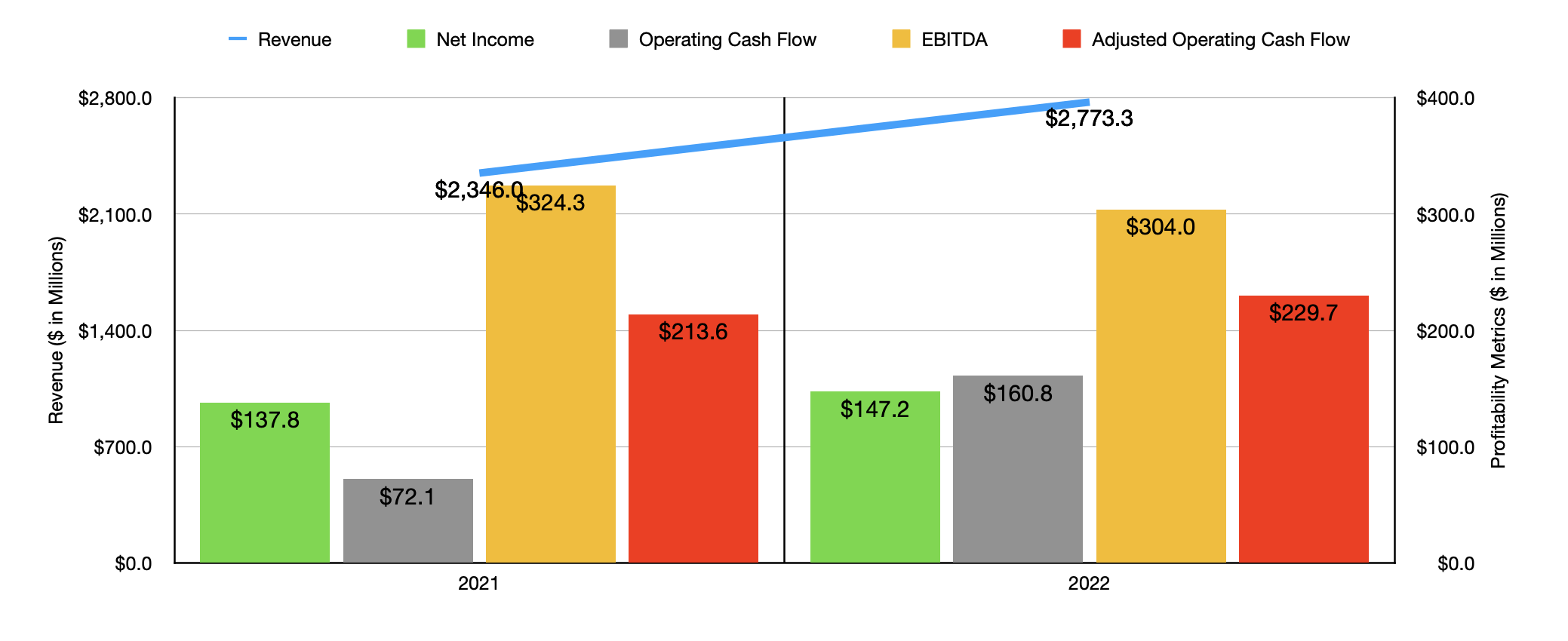

As you can see in the chart above, these results mark a significant departure from what the company experienced in 2022 relative to 2023. In addition to the decline in sales proving to be problematic, the company also faced downward pressure from a variety of other areas. The firms gross profit margin, for instance, managed to drop from 16.2% in the first quarter of last year to only 11.3% the same time this year. Administrative costs, meanwhile, grew from 3.2% of revenue to 3.5%. The largest chunk of the decline in gross profit margin for the company was related to the surfactants operations of the firm. Overall gross profit plunged $29.2 million year over year, driven mostly by a reduction in sales volume and lower unit margins. Higher costs associated with inflationary pressures, as well as higher pre commissioning expenses associated with the company's alkoxylation production facility in Texas, not to mention startup expenses associated with its 1,4 dioxane capacity here at home, really hurt the company's bottom line.

Management has not provided any real guidance for the current fiscal year. It is still early in the year, so forecasting out what results might look like for the rest of the year is definitely risky. But if we do this, we end up with net income for 2023 of $52.9 million. Adjusted operating cash flow would be $150.3 million. And EBITDA for the company would total $186.7 million. By comparison, these numbers last year were $147.2 million, $229.7 million, and $304 million, respectively.

{kind=link}

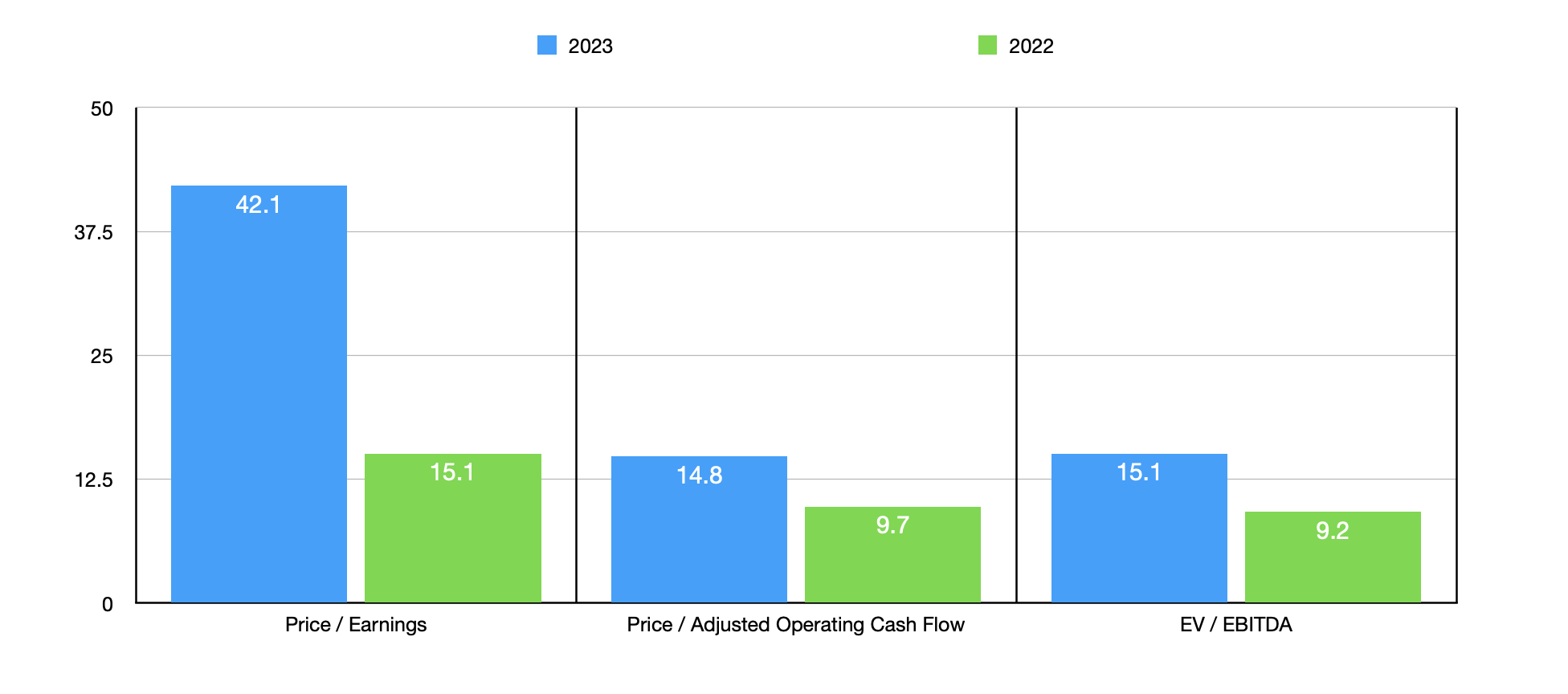

Using these figures, you can see how shares are priced in the chart above. The company goes from looking quite affordable using data from 2022 to looking fairly valued or perhaps even a bit pricey using data from 2023. Even if we are generous and assume that financial performance will revert back to what it was last year, shares of the company are only fairly valued compared to similar firms at this point. In the table below, for instance, you can see that, on a price to earnings basis, three of the five firms that I compared it to are cheaper than it. When it comes to the price to operating cash flow approach, only one of the companies was cheaper. However, when it comes to the EV to EBITDA approach, two firms ended up being cheaper, while another was tied with it.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Stepan Company |

| 15.1 |

| 9.7 |

| 9.2 |

| Celanese Corporation ( CE ) |

| 8.7 |

| 9.1 |

| 13.1 |

| Flexible Solutions International ( FSI ) |

| 5.8 |

| 10.0 |

| 4.9 |

| Minerals Technologies ( MTX ) |

| 16.4 |

| 13.6 |

| 9.2 |

| Albemarle Corp ( ALB ) |

| 7.0 |

| 10.6 |

| 7.2 |

| Innospec ( IOSP ) |

| 19.8 |

| 19.4 |

| 10.7 |

Takeaway

Based on the data provided, I would say that the current conditions are not looking particularly pleasant for Stepan Company at this time. A meaningful decline in sales volumes developed because of weaker demand and higher pricing. If that pricing had been enough to preserve profit margins or grow them, I would definitely be more bullish. But even ratcheting up the price of its products did not stop the company from seeing profits and cash flows tumble. For now, I expect this kind of weakness to continue. And because of that, I do believe that a modest downgrade from a 'buy' to a 'hold' is appropriate at this time.

For further details see:

Stepan Company: A Downward Revision Is Warranted