SCL - Stepan Company: An Unfortunate Development Resulting In An Upside

2023-12-03 04:04:51 ET

Summary

- Stepan Company's net income declined by more than half in 3Q23 due to lower sales volume and lower unit margins in core operational segments.

- The company is investing in new capacities for Nonionics and Dioxane products, which are expected to be ready by mid-2024 and 3Q23, respectively.

- Stepan's earnings have dropped significantly, but there is potential for a double-digit upside in the long term, although there are better investment options available in the basic materials sector.

Dear readers/followers,

I've been updating on Stepan Company ( SCL ) before, but the last article I wrote on this particular company is now over 8 months old. I like investing in the area of chemicals and basic materials, despite their overall volatility. I like "riding the waves" of the ups and the downs, enjoying being able to sell at very good short-term returns (or longer-term), even if that means holding the investments during times when people seem convinced that the overall appeal of the company in question is very low.

When it comes to Stepan, I haven't been positive on this one for years - but only for this year since March, when I first saw an upside to the business. Unfortunately, the company since that article has underperformed, making my stance one of loss - 15% compared to a positive 15% by the S&P500 in the same timeframe.

Not the greatest TSR - which is why I am glad despite my "BUY" stance, I did not get a position of any meaningful size in the company at the time, owing to other chemicals like Evonik ( OTCPK:EVKIY ) being more attractive. Still, Stepan is now 15% cheaper and that's even after recovering quite a bit. It's time to see what upside there is following 3Q23, and how 2024-2025E might look for this basic materials operator.

You can find my last article on this company here .

Stepan Company After 3Q23

If you recall my initial article on Stepan, you'll recall it is a surfactant and polymer sort of basic materials business. To simplify it even further, the company focuses over half of its annual sales revenues on chemicals having to do with detergents, wetting agents, emulsifiers, foamers, or dispersants - chemicals changing the surface tension of a liquid.

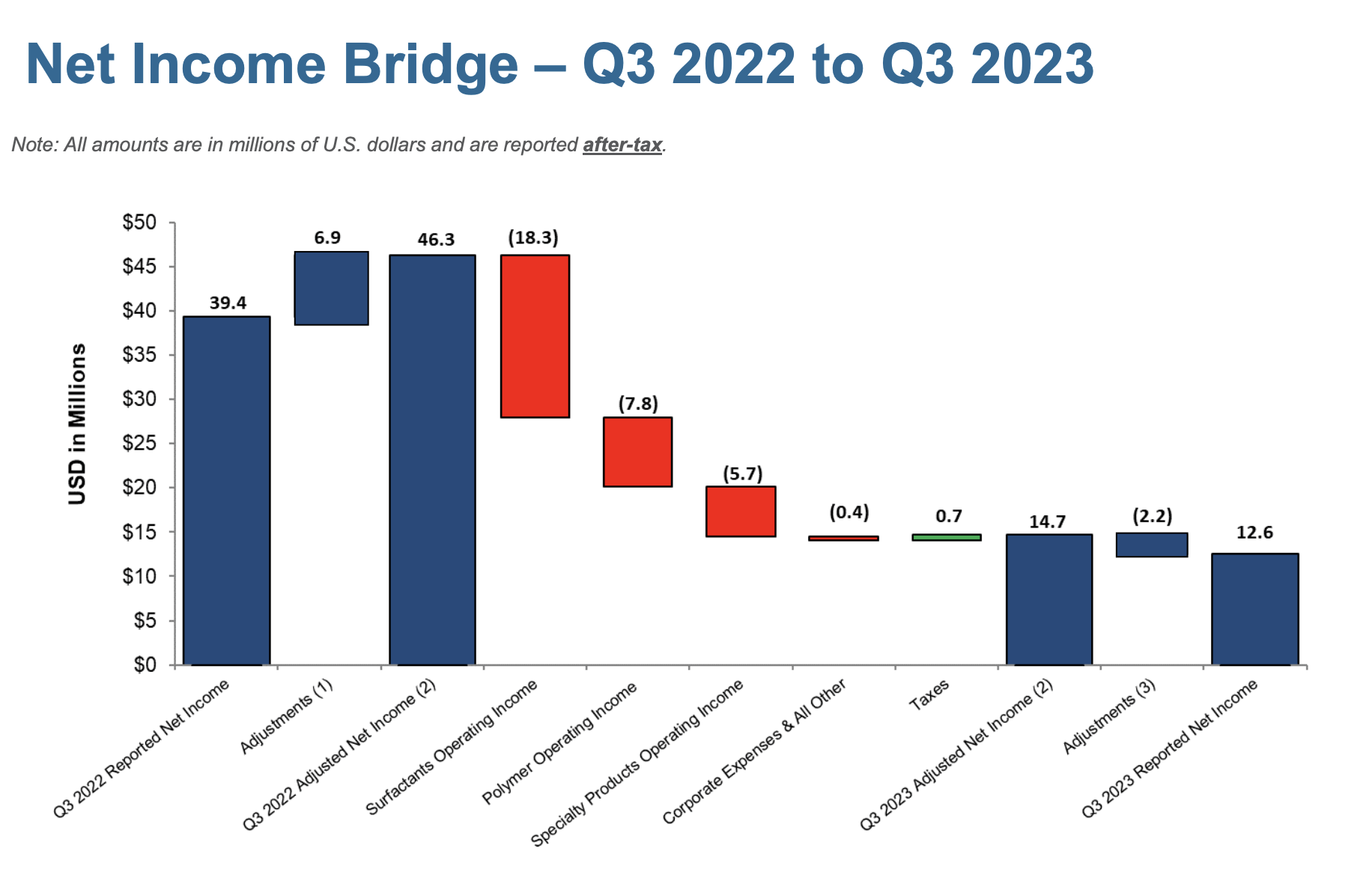

3Q23 was not a great quarter for the company's core, or other segments, as you might have expected by looking at the company's share price development. Net income was down to less than half on a YoY basis. Though this was an essential record-level result, it's still worth noting here.

This resulting income decline was primarily a result of a significant, near-double digit decline in sales volume, as well as lower unit margins in core operational segments, Surfactants. This margin decline, which is what we want to drill down on, was due to a mix of factors, but lower demand from agriculture coupled with significant customer destocking after record-level results a year ago was part of the core reason here.

Positives include new contracted volume for Dioxane products, but these positives were in the end, completely unable to weigh up the negative trends in net income here.

{kind=link}

More positives include overall lower CapEx and a slow inventory normalization. The company's 3x net debt/adjusted EBITDA on a TTM basis also isn't something to be worried about on a fundamental basis. The decline in CapEx is also, given the company's lower income, something I like to see - especially with the lower working capital and over $100M in reduction in inventories. Things are moving in the right direction.

And fundamentally speaking, Stepan does not have any material worries. In 2024, less than $60M worth of debt is coming due, and out of the total $650M worth of debt, most of it is after 2027. This gives the company plenty of time to handle what I view as a clear downcycle for the company's end market and verticals.

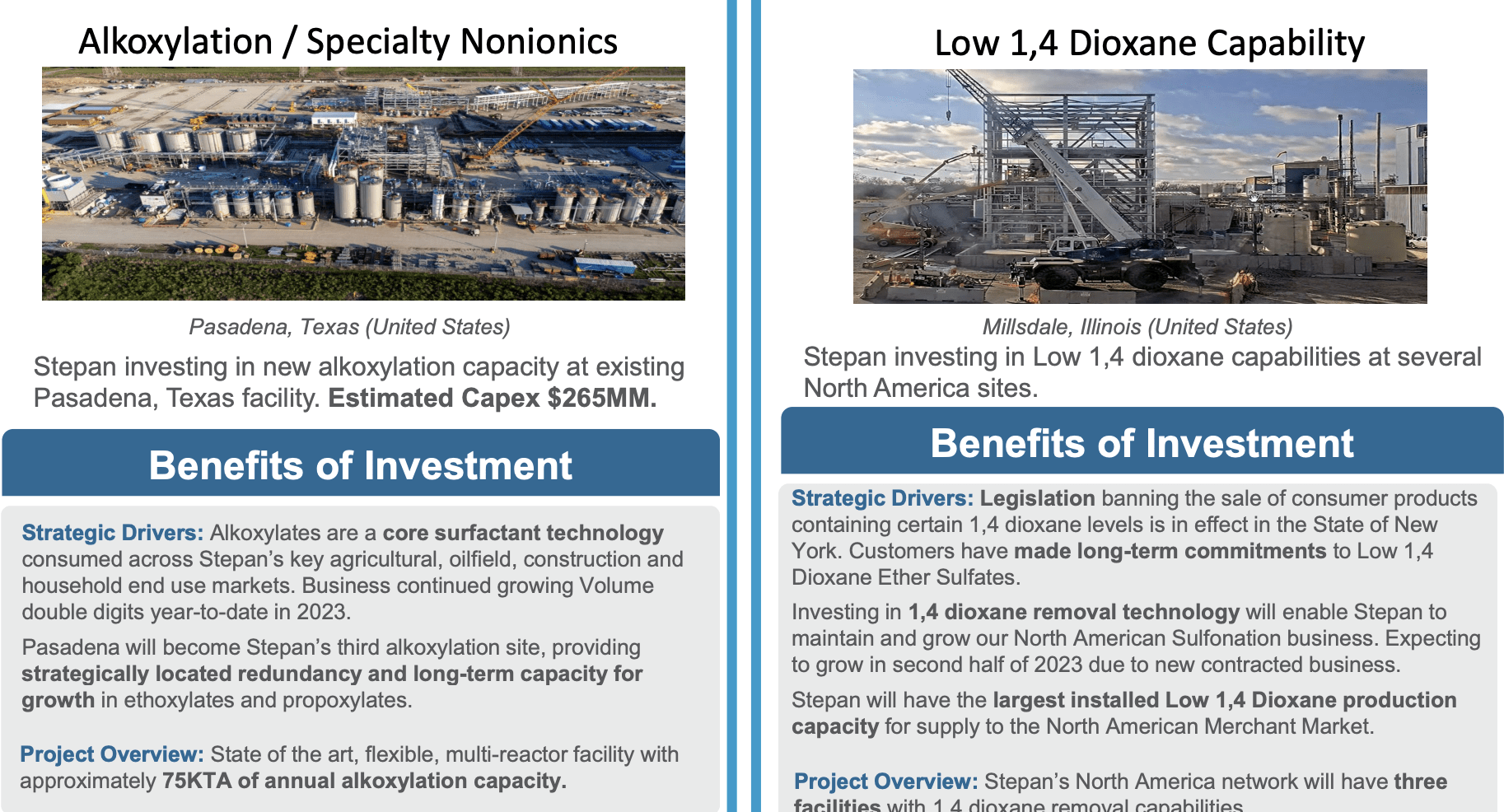

The company is taking the time to invest in new capacities - among the Nonionics and Dioxane, as mentioned.

{kind=link}

According to company information, we can expect the Nonionics to be ready for a start in mid-2024 and for the Dioxane capacity to see completed network construction in 3Q, with commissioning underway.

You might ask, just what is 1,4-dioxane? It's a solvent used for a multitude of practical applications, but also as a stabilizer for the transport of chlorinated hydrocarbons when transporting in aluminum containers. Applications of chlorinated hydrocarbons include pesticides, insulators, and vinyl chloride, a key production for PVC, or Polyvinylchloride. As such, 1,4-dioxane is a key chemical to these and many other industries, and Stepan's focus here is, if you believe in a more efficient and EV-focused world, logical, as this requires more focus on these sorts of lighter materials.

The company is also still the aforementioned global producer of a set of patented nutritional oils used in food and pharma, and this is obviously a segment they're trying to grow.

Stepan, despite my lack of interest until 2023, has been a good performer over time. Long-term shareholders of Stepan have been able to enjoy significant market outperformance, and this is not significantly impacted even by the last set of negative results that have seen the company's earnings drop quite a bit.

It's also important to not overstate the specialty segment for the company, which is really still far too small to make any sort of meaningful positive impact.

While Stepan chemicals are used pretty much in every segment that you can imagine, Stepan is also in no way unique in providing these chemicals, as there are plenty of other companies that do this sort of business - if not with the same sort of operational specialization as Stepan. I do favor specializes over masters of none in terms of company investments, but the company also needs to offer a compelling valuation weighing up for a lack of quality, or above-average quality with good value.

The company is now expecting a significant EPS drop, far above what I myself was able to forecast 8 months back. The cycle has gone down deeper than I expected, resulting in earnings moving from around $6.65 last year on an adjusted EPS basis, to less than $2.5 this year, which would mark more than a 60% overall earnings decline. Even with recovery clearly in the books once things cycle back up again, the question that becomes key to me is the following.

How much should we be willing to pay for a "decent" performer without a credit rating, less than $2B market capitalization, and less than 2% yield, in an environment where quality is found on every street corner and you can find 4-5% yields by moving to bonds and treasuries?

The answer to me, at least, is "not much".

Risk & Upsides

I already made it clear in my last article that I do not see Stepan as cheap here. Despite what has happened since the last article, the company is only cheap at this time if you normalize the EPS over a very long period of time - because if you look on the basis of 2023 or expected 2024-2025E there are investment-graded chemical companies available with far better upsides and yields. The main risk that I see here is that you end up overpaying for the company, even if you buy it at $80-$90. I don't see any operational weakness - the company's headwinds are a product of macro, and they are certainly not unique in this environment - but the risks in terms of valuation and quality are here, and they certainly do muddle things.

The upside to Stepan Company comes in the form of eventual reversal. If you're a seasoned investor with a long-term investment timeframe, then you can easily see a double-digit upside inclusive of yield here. However, that will take, if current estimates are to be believed, and these estimates hold around 2-3 years.

Valuation

I went back and forth on whether to change my target for Stepan here, and in the end, I'm sticking with my stance, but I'm cautioning investors to go in here unless you really know what you're getting into.

In this case, you're getting into a very long-term play. With the new capacities online, the company's earnings and the underlying macro reverting in 12-24 months, I do see a good potential for return here in a Stepan investment. My problem is that, like before, there are simply far better investments available at similar or far better valuations - and those also happen to come with far better yields.

Stepan will be experiencing a reversal equal in force and trajectory to the decline that preceded it - perhaps more. This will in turn result in the company's share price likely increasing. TSRs of up to 50-70% are possible, based on where the company has traded before in terms of multiples.

But given how uncertain the timing of this 30%+ adjusted EPS growth rate is, and how many better alternatives in the basic materials sector exist, I would be very cautious about where to put my money and my time here.

You're investing in a cyclical chemical business going into a more or less confirmed downturn in EPS in a rising interest rate environment, and you are doing so at a premium because Stepan tends to be valued at closer to 18-20x P/E. The valuation we're currently at is a bit more muddled because of the earnings drop. The severity of the earnings drop can be compared to the one that was forecasted in my last article in early 2023. That was 13%. The actual earnings drop has come in closer to 50-60% depending on how Q4 turns out.

That's why you'll also find me significantly changing my PT for this company. I now expect Stepan to manage something close to a $90/share long-term, but that doesn't mean you necessarily should invest today unless you believe the outperformance for this company could be very significant over time.

I see the upside - I'm just cautious about the timing, and that's also why I'd rather push money to work in other sectors and companies at this particular time.

I give you my updated thesis for Stepan here and caution you to go deeply into this investment unless you're fine holding this one for at least 20-30 months - if so, there is an upside here.

Thesis

- Stepan is an average chemicals company with a good portfolio and good fundamentals - but it is not class-leading. Its inherent volatility means that the closer to below a 15x-P/E or equivalent cheap pricing you can buy, the better.

- At current pricing, I view Stepan as a "BUY" for the first time in some time, but I also want to point out that there are plenty of attractive alternatives across the chemicals sector that may offer you better rates of return.

- my PT for SCL is now $90, changed from my last article, and while I say "BUY" here, I would also caution you to.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company definitely isn't cheap, but I can see an upside here.

For further details see:

Stepan Company: An Unfortunate Development Resulting In An Upside