CLZNF - Stepan's Shares Are Reaching Even More Appealing Prices

2023-08-28 10:57:19 ET

Summary

- Volumes are declining as customers have high inventories.

- Profit margins are currently depressed due to current headwinds.

- The company's headwinds are likely of a temporary nature as they are directly linked to the current macroeconomic landscape.

- The dividend is safe as the cash payout ratio is low, and capital expenditures are declining.

- This represents a good opportunity to add shares to any long-term dividend growth portfolio.

Investment thesis

A year ago, I wrote an article on Stepan Company (SCL) as I considered that the 18.03% decline in the share price from all-time highs represented a good opportunity to start averaging down as inflationary pressures, labor shortages, and supply chain issues were likely headwinds of a temporary nature due to their direct link to the macroeconomic landscape. Since then, the share price has declined by a further 22.57% and currently accumulates a total decline of 37.80% from all-time highs.

Although inflationary pressures and supply chain issues have recently shown signs of improvement, declining volumes, high-cost inventory, and pricing pressures have caused another significant margin contraction, which has caused a significant increase in net debt due to strong investments in the construction of the company's upcoming Pasadena, Texas site and equipment upgrades to meet new regulatory limits on 1,4 Dioxane in the United States. Furthermore, increased interest expenses are beginning to put some pressure on the company's operations as the company is expected to pay over $15 million per year from now on.

Despite this, net debt declined by $33.2 million during the second quarter of 2023 as the company reported positive free cash flows thanks to some inventory destocking and a significant decline in capital expenditures as the 1,4 Dioxane and the Pasadena site projects are in advanced stages. Furthermore, the company currently holds $340 million in inventories. For these reasons, and considering that customer high inventories and weak demand are likely temporary headwinds, I strongly consider that Stepan Company is poised to deleverage its balance sheet so it shouldn't be a major issue to reduce its net debt from $618 million to significantly lower levels, and thus this represents, in my opinion, a good opportunity to continue adding shares to any dividend growth portfolio with a long-term focus.

A brief overview of the company

Stepan Company is a well-known global manufacturer of specialty and intermediate chemicals for third-party manufacturers. The company was founded in 1932 and its market cap currently stands at $1.94 billion, employing over 2,000 workers. The company operates under three business segments: Surfactants, Polymers, and Specialty Products.

Stepan Company industries (Stepan.com)

{kind=link}

The Surfactants segment manufactures chemical agents used in detergents for washing clothes, dishes, carpets, fine fabrics, floors, and walls. They are also used for shampoos and conditioners, fabric softeners, toothpastes, cosmetics, and other personal care products, as well as emulsifiers for agricultural products and as emulsion polymers for floor polishes and latex foams and coatings, wetting and foaming agents for wallboard manufacturing, and surfactants for enhanced oil recovery and biodiesel. The Polymers segment manufactures polyols and phthalic anhydride used in multiple types of specialty polymers, and the Specialty Products segment manufactures chemicals used in food, flavoring, and pharmaceutical applications.

Currently, shares are trading at $86.65, which represents a 37.80% decline from all-time highs of $139.30 reached on May 10, 2021. As can be seen in the chart, the share price has continued declining as a recent reduction in volumes has caused a drop in sales and a further contraction in profit margins due to unabsorbed labor, and interest expenses are increasing as a result of increased debt exposure as the company is making strong investments for long-term growth. The recent drop in sales is mainly due to weakening demand and unusually high customer inventory levels, which suggests that although new headwinds are adding to the current situation, these continue to be directly related to the current macroeconomic landscape and are not as related to the nature of the company.

The company keeps acquiring new businesses

After the acquisitions of Logos Technologies and Clariant's ( CLZNF ) ( CLZNY ) anionic surfactant business in Mexico in 2020, and the acquisitions of INVISTA's aromatic polyester polyol business and a fermentation plant located in Lake Providence, Louisiana, in 2021, the management continued with the M&A strategy and, in September 2022, it completed the acquisition of the surfactant business and associated assets of PerformanX Specialty Chemicals, including intellectual property, commercial relationships, and inventory, for $9.7 million. Although the impact will not be noticeable since it is a minor acquisition, this shows that the company remains open to continuing to expand its market reach for the long term.

Declining volumes caused a significant contraction in sales

Despite the global restrictions derived from the coronavirus pandemic in 2020, the company reported a slight increase in sales of 0.59% during that year, and this increase accelerated during 2021 and 2022 as sales increased by 25.47% and 18.21%, respectively, boosted by acquisitions and the reopening of the world economy after a year marked by aggressive self-imposed restrictions around the world derived from the coronavirus pandemic. Furthermore, the company has strong geographical diversification as 57% of the company's total net sales in 2022 took place within the United States, 8% in the United Kingdom, 8% in France, 7% in Poland, 6% in Brazil, 5% in Mexico, and 8% in the rest of the world.

Stepan Company TTM sales (Seeking Alpha)

{kind=link}

Despite the fact that net sales increased by 2.81% year over year during the fourth quarter of 2022, they actually declined by 12.79% sequentially, and net sales declined by 3.53% year over year during the first quarter of 2023, and by 22.84% (also year over year) during the second quarter as demand is weakening while customers remain with high inventories. Also, pricing pressure, especially from Latin America, is forcing the company to sell its products at lower prices. The management expects the second half of 2023 to deliver improved sales boosted by increased rigid polyol demand, and new contracted low 1,4-dioxane volumes are expected to start picking up in the second half of 2023 and drive growth in the future. Still, growth is poised to be relatively slow as some further destocking is expected. In this regard, sales are expected to decline by 11.19% in 2023 but should slowly start recovering in 2024 as they are expected to increase by 6.50%.

Despite this decline in sales, the recent decline in the share price has caused a significant decline in the P/S ratio to 0.773, which means the company currently generates $1.29 in sales for each dollar held in shares by investors, annually. Nevertheless, note that the recent decline in revenues is still not fully reflected in the ratio as it uses trailing twelve months' revenues for the calculation.

This ratio is 19.63% below the average of the past 10 years and represents a 53.15% decline from decade-highs of 1.650 reached in 2021, and this means that investors are placing less value on the company's sales due to four main reasons: weakening demand, reduced profit margins, increased debt exposure and interest rates, and growing recessionary concerns as a result of recent interest rate hikes.

Margins are currently impacted by declining volumes and high inventory cost material

Since the reopening of the global economy after the coronavirus pandemic crisis, the company's operations have been impacted by supply chain issues, inflationary pressures, and labor shortages. Now, declining volumes caused a further margin contraction as the trailing twelve months' gross profit margin declined to 12.65%, and the EBITDA margin to 7.64%.

During the second quarter of 2023, the company reported a gross profit margin of 11.45% and an EBITDA margin of 7.64% which, despite representing a slight improvement compared to the fourth quarter of 2022 when the company reported a gross profit margin of 10.80% and an EBITDA margin of 4.37%, are well below the profit margins investors were used to before the coronavirus pandemic when the company used to report gross profit margins of over 15% and EBITDA margins of over 10%. As a consequence of this drop in profit margins and a significant decline in sales volume, the company reported an EBITDA of $44.7 million for the quarter, which represents a 56.41% decline compared to the same quarter of 2022.

Now, the management expects improved margins during the second half of 2023 boosted by increasing volumes and lower raw material costs. Also, the company continues running down higher inventory cost material, so the production costs and the sale prices should eventually align. Regarding actions to help margins stabilize, the management applied headcount and discretionary expense controls at the beginning of 2023, and now plans to initiate a voluntary early retirement program for eligible employees at its corporate headquarters and Global Technology Center. Despite this, volumes will have to pick up in order to see a noticeable positive impact on profit margins as the decline is significant, so the company's turnaround will be, in my opinion, directly linked to the improvement of the current macroeconomic landscape.

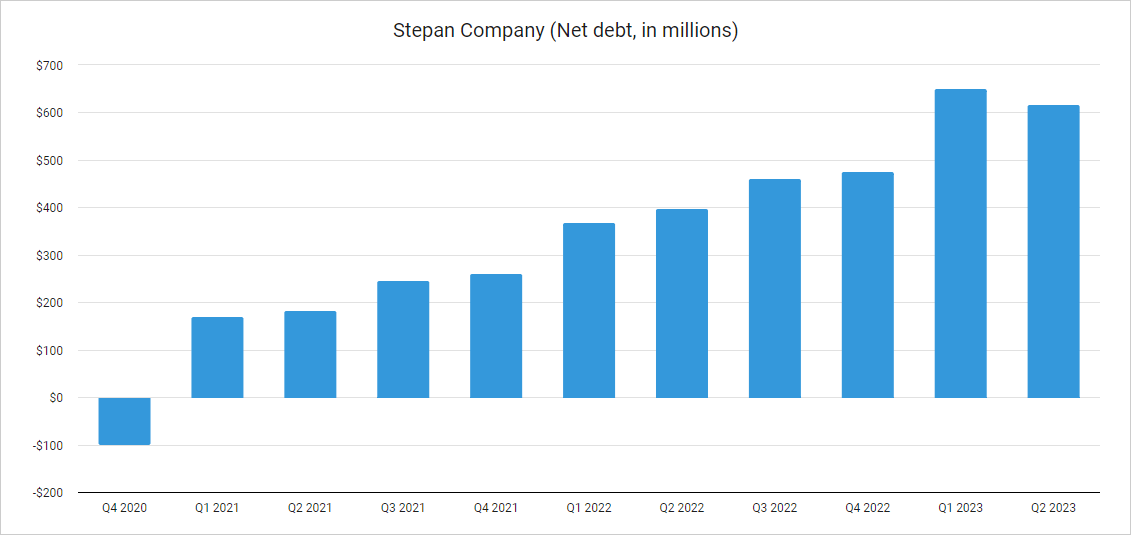

Net debt has increased significantly in recent quarters, but the deleveraging phase has begun

The company reported negative net debt in 2017, 2018, and 2019, but expenses of $184.5 million for acquisitions in 2021 and aggressive capital expenditures ($126.0 million in 2020, $198.0 million in 2021, and $301.6 million in 2022) have caused a significant increase in net debt to $651.2 million during the first quarter of 2023.

Stepan Company net debt (Seeking Alpha)

{kind=link}

Despite this, the company managed to reduce its net debt by $33.2 million to $618 million during the second quarter as it reduced its inventory levels by $34.1 million during the first quarter and by $28.4 million during the second quarter while capital expenditures declined by $4 million during the first quarter and by a further $24.5 million during the second quarter, and the company expects to reduce inventories by a further $40 million during the second half of 2023 in order to free up some cash, which should be enough to keep deleveraging the balance sheet as capital expenditures are also expected to continue declining.

In this regard, the company's inventories remain high and should allow for strong cash from operations in the coming quarters and, if capital expenditures continue declining as expected, this should allow for a significant deleveraging of the balance sheet in the short and medium term, which should reduce interest expenses and make the dividend safer in the long term while poising the company for future growth.

The dividend is safe

The company has increased its quarterly dividend for 55 consecutive years as it announced a 9% dividend raise from a quarterly dividend of $0.335 per share to $0.365 in the fourth quarter of 2022. This makes Stepan Company a shareholder-friendly company as investors can expect growing dividends as the cash payout ratio has historically been low, and the recent share price decline coupled with increased dividends caused an increase in the dividend yield to 1.68%, which I would consider as appealing due to the low cash payout ratio and the potential growth in the long term.

Despite the recent difficulties the company is going through regarding contracted margins, the trailing twelve months' cash payout ratio remained low quarter after quarter as the dividend is very low compared to current capital expenditures. In the following table, I have calculated the percentage of cash from operations allocated to the payment of dividends and interest expenses in order to assess its sustainability in the long term.

| Period |

| Q2 2021 |

| Q3 2021 |

| Q4 2021 |

| Q1 2022 |

| Q2 2022 |

| Q3 2022 |

| Q4 2022 |

| Q1 2023 |

| Q2 2023 |

| Cash from operations (TTM, in millions) |

| $201.4 |

| $114.9 |

| $72.1 |

| $62.9 |

| $85.6 |

| $125.7 |

| $160.8 |

| $109.6 |

| $158.4 |

| Dividends paid (TTM, in millions) |

| $26.8 |

| $27.4 |

| $28.1 |

| $28.7 |

| $29.3 |

| $30.0 |

| $30.6 |

| $31.2 |

| $31.9 |

| Net interest expenses (TTM, in millions) |

| $5.9 |

| $5.9 |

| $2.9 |

| $3.6 |

| $4.8 |

| $8.2 |

| $8.1 |

| $8.6 |

| $9.7 |

| Cash payout ratio |

| 16% |

| 29% |

| 43% |

| 51% |

| 40% |

| 30% |

| 24% |

| 36% |

| 26% |

As one can see, the cash payout ratio remained low in the past few quarters boosted by recent inventory reductions. Nevertheless, despite accounting for less than 10% of cash from operations, net interest expenses have increased significantly in recent quarters to $9.7 million. Furthermore, the company reported net interest expenses of $3.9 million during the second quarter of 2023, for which the company is expected to pay over $15 million annually due to the recent increase in debt exposure and interest rates. In this sense, it is not the cost of the dividend or interest expenses that put stress on the company's operations, but high capital expenditures.

In this regard, capital expenditures increased to $301.6 million in 2022 from $194.5 million in 2021 and $126.0 million in 2020 as the company is currently building a manufacturing plant in Pasadena, Texas while performing equipment upgrades to meet new regulatory limits on 1,4 Dioxane in the United States, and the company expects a decline to $240-$270 million in 2023 as capital expenditures of $ 67.7 million during the second quarter of 2023 represented a 26.57% decline compared to the first quarter of 2022. Furthermore, capital expenditures are expected to continue declining even further in the foreseeable future as a big part of the investments for products with lower 1,4 Dioxane and the Pasadena facility have already been made as the Pasadena plant is expected to be 90% complete by year-end and to start up in mid-2024 as it is currently 35% completed, and considering the company currently holds $133.9 million in cash and equivalents and inventories of $340 million (which should help to deliver strong cash from operations in the short and medium term), I believe interest expenses may have reached the highest point and should slowly start declining as the company deleverages its balance sheet.

Risks worth mentioning

Although I consider Stepan Company to be linked to relatively low risks thanks to acceptable margins (despite recent contraction) and the temporary nature of the current headwinds, there are certain risks that I would like to highlight, especially for the short and medium term.

- Recent interest rate hikes could trigger a (more or less profound) global recession, which could cause a further decline in volumes, sales, and profit margins.

- If inflationary pressures or supply chain issues intensify again, profit margins could remain depressed, which would translate into lower cash from operations and a potential further increase in net debt (and thus interest expenses).

- Profit margins could continue to be stressed if pricing pressures intensify, which would have a significant impact on the company's ability to generate cash from operations.

- The company could have issues in successfully emptying its inventories as the global demand for its products has dropped significantly in recent quarters. Although the management has demonstrated the ability to slightly reduce inventories over the past two quarters, a further reduction in demand could make it more difficult to continue converting inventories into actual cash.

- Due to the volatility that the markets are currently exposed to, the share price could continue to decline, so averaging down continues to be a strategy that I strongly recommend regarding Stepan Company.

Conclusion

Stepan has been operating for almost a century, and the company still has (at least) many decades ahead as the products it produces are essential for third-party manufacturers and is making significant investments to adapt its products to the (regulatory) demands of the future. Despite this, current headwinds are putting significant pressure on the company's operations and this, added to the growing fears of a potential recession due to recent interest rate hikes, has caused a 38% drop in the share price as investors remain on the sidelines. The recent decline in demand added to the pricing pressures (especially from Latin America) is putting more pressure on profit margins when it seemed that the inflationary pressures and supply chain issues were beginning to ease.

Net debt has increased significantly during the past quarters as the company is building a major manufacturing facility and is investing in the development of lower 1,4 Dioxane products while cash from operations is limited due to recent margin contraction, but capital expenditures started to decline in the past quarter and are expected to continue declining in the coming quarters, and the company is expected to continue converting its inventories into actual cash, which should allow for further reductions in net debt as it already achieved some reduction in the second quarter of 2023. In addition, the cash payout ratio is very low, so once capital expenditures reach even lower levels, the reduction in net debt should start accelerating, at least slightly. Furthermore, the current headwinds are most likely temporary as customer inventories should eventually reach more healthy levels, which should help in some volume recovery as expected for the second half of 2023 and 2024. For these reasons, I believe that the recent decline in the share price represents a good opportunity to add shares to any long-term dividend growth portfolio as the long-term dividend potential is high thanks to a very low cash payout ratio, but given current market volatility and the risks of a potential recession, I strongly recommend to average down from current prices as the market could present an even better opportunity in the foreseeable future.

For further details see:

Stepan's Shares Are Reaching Even More Appealing Prices