STE - Steris: Remains On Track For Strong Fiscal '24 Added Upsides From Operating Leverage

2023-09-01 08:00:00 ET

Summary

- STERIS plc continues to present attractive fundamentals and accretive market value.

- The company's latest numbers showed double-digit growth and strong cash flows across all portfolio segments.

- The stock remains in a long-term uptrend and has technical upside targets to $270, as shown in this analysis.

- Net-net, reiterate buy.

Investment summary

The data continues to suggest STERIS plc (STE) is a buy on long-term value in my informed opinion. STE staged a strong rally off lows in early '23, where I'd advocated buying the company at $214, following the removal of its Sotera overhang. The company's latest numbers exhibited double-digit upsides throughout the P&L, whilst cash flows remain strong, rolling off $214mm during Q1 fiscal '24 (note: the company reported its first quarter in its fiscal 2024, corresponding to Q1 CY'23. For consistency and simplicity, I'll talk in terms of Q1 from here).

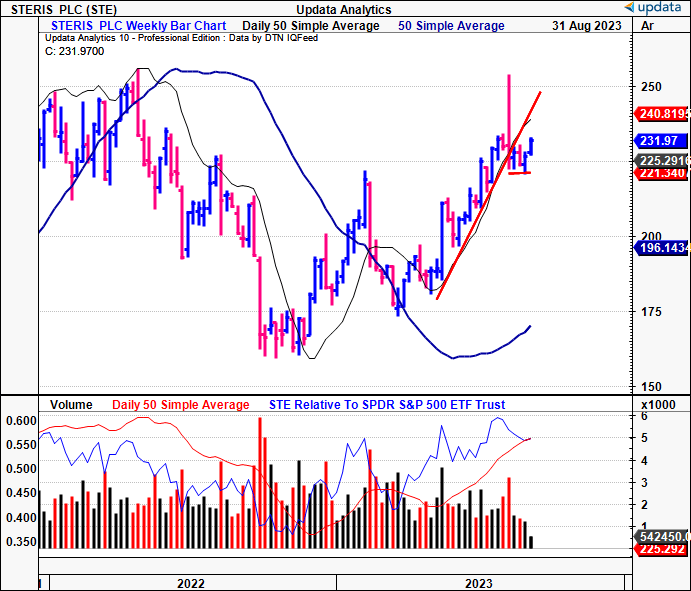

Further, a barebones look at price structure and technical drivers indicates a strong formation after curling up from a 4-week base as I write [Figure 1, with more technicals discussed later]. This report will unpack the company's latest numbers and link back to the overall buy thesis. Net-net, I continue to rate STE a buy, eyeing $249-$270 as the next performance band.

Figure 1.

{kind=link}

Critical updates to buy thesis

Brief overview of operations

The core business of STE is providing sterilization and infection control products to healthcare companies. The business sells its inventory to such customers and requires around 89% of revenues in working capital and employs ~$9.8n of fixed capital to maintain its current level of operations ($5.9Bn less goodwill).

The company operates in four business segments: Healthcare, AST, Life Sciences ("LS") and Dental. The Healthcare segment sells products that are critical to sterile processing departments and procedural centers, such as operating rooms and endoscopy suites. They include infection prevention consumables, capital equipment (and ancillary services to maintain the equipment), and outsourced instrument reprocessing services.

The AST segment is a 3rd-party provider for contract sterilization and testing services. These are essential to providers in order to validate their sterilization of medical devices and pharmaceutical manufacturing. Essentially, it helps them with all compliance and regulatory overhang in the sterilization domain. Meanwhile, its LS segment provides a comprehensive suite of products and services that support pharmaceutical manufacturing-primarily for vaccine and other biopharma customers that focus on aseptic manufacturing.

Q1 FY'23 insights

STE put up $1.28Bn in quarterly revenues , growing 11% YoY. Critically, the bulk of business growth was organic, underscored by volume growth (demand) and 290bps of aggregate pricing increase. I would point out that it pulled this to gross of 44.8%, down 30bps due to input inflation (material and labour costs) and a snip in productivity. Hence, whilst volumes were up, they weren't up to internal expectations, despite the favourable pricing.

The divisional breakdown is as follows:

- Its healthcare markets were up 17% YoY to $818mm and were the main revenue growth driver, as shown in Figure 2. Growth was observed across capital equipment, consumables, and service categories, and was driven by a combination of factors such as 1) procedural volume for U.S. medical procedures, 2) the price increases mentioned earlier, and 3) a gain in market share. To illustrate, estimates put the global sterilization market at a 7.9% CAGR into FY'27; hence, STE's growth of 17% illustrates it outpaced the average competitor and stole market share from these players in my view. Essentially, it shipped more capital equipment out the door and at a faster pace than last year.

- The AST segment did $233.1mm of business and grew 5% YoY. But I'd point out STE faced 2 temporary issues in Q2 that are plaguing global healthcare equipment suppliers-1) destocking of inventory in select categories, and 2) a drop in customer demand for bioprocessing as compared to the last 2 years (thanks to Covid-19 diminishing). Subsequently, operating profit in its AST arm grew just 30bps YoY.

- The destocking/demand issue hurt the LS division, with sales down 60bps and operating income down ~10% YoY.

Thankfully, many global healthcare equipment/devices players are reporting a wind-down in the destocking issue. Further, any impact from Covid-related revenues is likely to normalize and be non-meaningful going beyond 2023 (hopefully, anyway-fingers crossed). Still, any growth in STE's bioprocessing is likely to be negligible for its fiscal '24.

BIG Insights

Overall operating margin declined by 50bps and ended up at 22.4% of revenue as, thanks to the lower gross and destocking etc. mentioned earlier. Despite the margin contraction, operating leverage almost doubled YoY and was 0.8x compared to 0.4x in Q1 FY'23. This is important considering the destocking and demand headwinds outlined earlier.

That is, even with this in place, the company produced $0.8 in operating income off every extra $1 in revenues, 80% higher leverage than last year. Alas, it has leverage over variable costs, which could prove as a tailwind into the remainder of the year. This led to it producing $214mm in quarterly free cash to the firm. STE also left the quarter at 2.1x gross leverage (debt: EBITDA) and $2.9Bn in long-term debt on the balance sheet. It also diverted $66mm in CapEx-$22mm above the maintenance capital charge-and thus, I'd consider it spending the $22mm towards financing its growth operations.

Speaking to factors of CapEx and uses of cash, consider the following from Q1:

- STE reports capital expenditures in its core healthcare markets it still strong. Its backlog of orders posted ~$500mm by the end of the quarter, reflecting the level of capital spending by its hospital customers.

- Notably, c.40% of the orders in the Q1 were attributed to large-scale projects.

- It also finalized its agreement with Becton, Dickinson and Co. ( BDX ) to acquire a suite of surgical and laparoscopic instrumentation, as well as sterilization container assets. It will fold these assets into its healthcare segment. The transaction was completed in August, for a total cost of $540mm, and financed through new debt issued.

Hence, the quarter was still reasonably strong in my view, and the numbers corroborate this posture. The points on operating leverage are noteworthy and indicate a company adapting to its rate on cost pressures well. This backlog/demand issue is likely to settle by yearend in my view as well, and it would appear the majority of players in the space support this view.

Valuation and conclusion

The stock sells at 16x forward EBITDA, and this is a 28% premium to the sector. Critically, this number expenses R&D on the balance sheet, a total of $102mm in the TTM. This has been flat since Q2 fiscal 2023 for STE, and I'm carrying c.$100mm in R&D forward in my '24 assumptions for the company. Stripping this out of the calculus (by capitalizing its R&D as an intangible asset and amortizing it over a straight line for a 7-year useful life) you get to STE selling at ~14x forward, more in line with the sector. Hence, there is value in the name in my view.

Still, the market values it at 16x forward, and assigning this to my FY'24 EBITDA assumptions gets us to ~$249 per share, and in my upside case, calling for $1.65Bn in FY'24 EBITDA, this derives a value of $267/share at 16x forward.

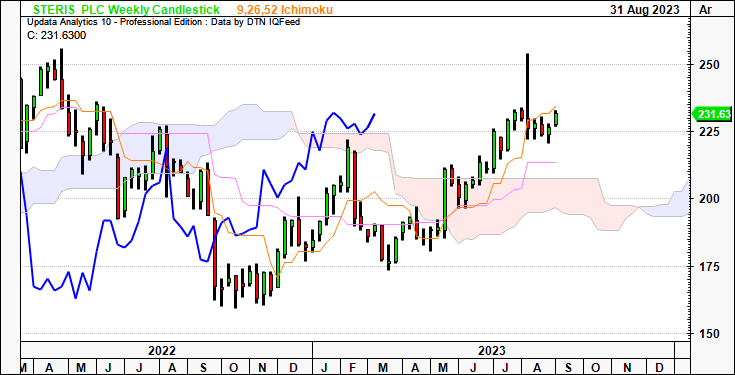

I'd also point out the stock still remains in a long-term uptrend and recently tested a key psychological level in August with a swift turn off this mark. This is shown in Figure 3, in the weekly cloud chart. Both price and lagging line are above the cloud, supporting a bullish view for a long-term horizon.

Figure 3.

{kind=link}

We therefore have technical upside targets to $270 after the stock took out the $231 mark at the time of writing. Hence, I'm eyeing $270 as the next technical target. This certainly supports a bullish view, and long-term fundamentals of the company are behind this price structure as well, given the multiples discussed just above.

Figure 4.

Data: Updata

In short, STE continues to present with long-term economic growth levers in its arsenal. You're looking at a differentiated offering in STE that is growing at above-market rates in its healthcare segment, the company's major breadwinner. The company is also off to a good start in its fiscal '24, tackling industry-wide pressures well, and still spinning off attractive operating leverage in doing so. Sales were up 11% YoY, and each turn in revenue produced an additional $0.8 in operating income in Q1, nearly double that of last year. Technicals are also supportive in my eyes. The major risk to the investment thesis is if industry pressures persist (I'm thinking the inventory destocking here) and the potential impact this could have on the firm's backlog, that currently rests at ~$500mm. The company's asset purchases off BDX are yet to be quantified as well, so I'll be paying close attention to this moving forward as well. Net-net, reiterate buy, eyeing $249-$270/share as the next target band.

For further details see:

Steris: Remains On Track For Strong Fiscal '24, Added Upsides From Operating Leverage