STRL - Sterling Infrastructure: Moving To Sidelines Post The Recent Stock Price Run-Up (Rating Downgrade)

2023-08-21 14:40:43 ET

Summary

- Sterling Infrastructure, Inc. has seen significant price appreciation since my previous coverage.

- The company's revenue and margin growth prospects still look good.

- However, the company's valuation multiple has already been re-rated and is much higher than the historical average.

Investment Thesis

I last covered Sterling Infrastructure, Inc ( STRL ) with a bullish rating in May this year and the stock has seen a massive ~80% price appreciation since then. In fact, the stock is up over 200% since I initiated coverage on it with a buy rating a year ago. Looking forward, STRL is well-positioned to deliver good revenue growth in the near term as well as the medium term. The revenue growth should benefit from a healthy backlog level of $2.39 billion exiting Q2 2023 and good end-market demand across all segments. This demand is driven by secular trends from the growing need for data centers and reshoring manufacturing in the U.S. This healthy demand is further supported by federal infrastructure funding, which is acting as a multiyear tailwind in the company's end markets. On the margin front, the company should benefit from easing supply chain challenges, volume leverage, price increases, and improving project mix through increasing margins in the backlog.

However, these revenue and margin growth prospects already seem to be reflected in the company's current valuation which is trading at a significant premium to historical averages. In my previous article, I argued that the stock deserves a re-rating given its good execution and improving growth prospects. I believe after the recent run-up, the stock has already re-rated appropriately to reflect its growth prospects in the coming years. Hence, I am moving to the sidelines and downgrading my rating to neutral despite good growth prospects.

Q2 2023 Earnings

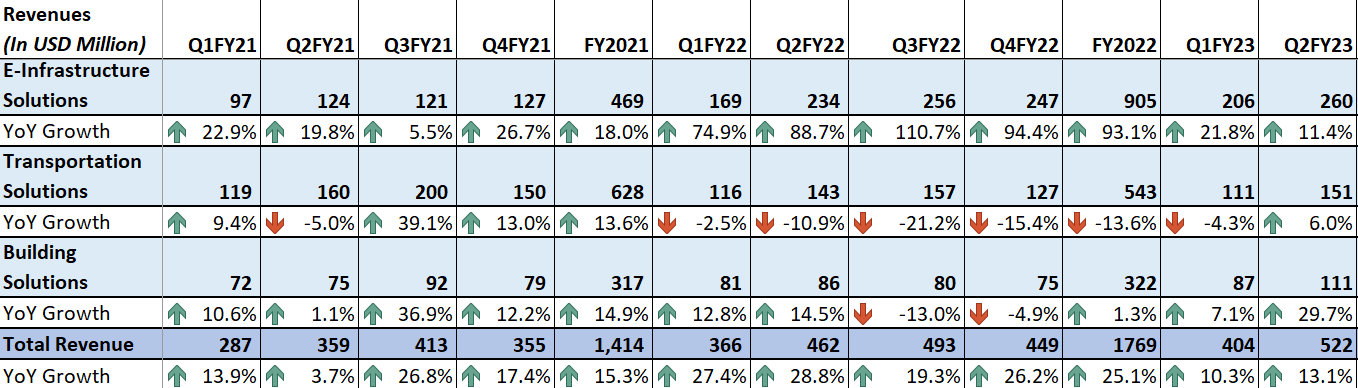

Recently, Sterling Infrastructure Inc reported better-than-expected results for the second quarter of 2023. The company's revenue increased by 13.1% YoY to $522 million and exceeded the consensus estimate by $27.3 million. Adjusted EPS grew by 37% YoY to $1.27 and was higher than the consensus EPS estimate by $0.34. The gross margin increased by 230 bps YoY to 17.7% and the operating margin increased by 200 bps YoY to 11.5%. The revenue growth was driven by good end-market demand and a healthy backlog. Adjusted EPS and margin increased due to high margins in backlog and volume leverage.

Revenue Analysis and Outlook

In my previous article in May, I discussed Sterling's future growth prospects benefiting from a healthy backlog and favorable end-market demand driven by increased federal infrastructure funding. STRL reported earnings for its second quarter of 2023 recently and similar dynamics were seen there as well.

In the second quarter of 2023, revenue growth continued to benefit from healthy end-market demand in the infrastructure space. In addition, a good backlog execution across all the segments also contributed to sales growth. As a result, revenue increased by 13.1% YoY to $522 million.

On a segment basis, the E-infrastructure segment which accounts for approximately half of total revenue, saw strong end-market demand for building data centers, and large manufacturing projects for EV battery facilities. Additionally, the transportation segment also saw revenue recovery in the quarter driven by a number of federal, state, and local infrastructure investment programs, all fueling the end-market demand. Lastly, the Building segment also saw good growth due to increased commercial market activities and some recovery in the residential market for both multifamily and single-family households.

STRL's Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I believe the company should be able to continue delivering good revenue growth benefiting from a healthy backlog level, good demand for infrastructure projects in the E-infrastructure segment and increasing the bidding pipeline in the transportation segment.

The backlog of a company serves as a good indicator of the future revenue growth of the company. STRL's backlog has seen good backlog growth over the past few quarters, thanks to the increased level of federal investments in the E-infrastructure and Transportation segment. In the second quarter, the backlog continued to increase both year-over-year as well as sequentially. Compared to the previous year's quarter, the awarded backlog increased by 13% YoY to $1.74 billion with a book-to-burn ratio of 1.2x, and the unsigned low-bid awards increased by 257.1% to $657 million due to strong bidding activity in the transportation segment in order to capture increasing opportunities from Infrastructure Investment and Job Act (IIJA). This resulted in combined backlog growth of 38.2% YoY to $2.39 billion with a book-to-burn ratio of 2.4x.

STRL's Order Backlog (Company Data, GS Analytics Research)

This strong level of backlog should continue to support the company's sales growth moving forward. In the Q2 2023 earnings call , CFO Ronald Ballschmiede commented regarding the visibility of backlog contributing to revenue growth ahead:

The reality is in our big -- in our project [indiscernible] businesses, specifically the Transportation group and the large projects within E-Infrastructure, the second half is pretty much locked in, frankly. What we're selling today and what's in our combined backlog, that's really 2024 and beyond, which is great. We have -- it's been probably two years or three years since we've had that many large in excess of $50 million and up to [indiscernible] million projects. And as you saw in the huge growth in the Unsigned, we expect that to really help us in 2024 and forward."

So, the current backlog should help the company in delivering revenue growth in the second half of 2023 as well as in the coming year. I expect backlog levels to further increase over the coming quarters as the end markets across the segments remain favorable. In the E-infrastructure Solutions segment, STRL is experiencing multi-year tailwinds from secular demand trends in building data centers and the reshoring of U.S. manufacturing to improve supply chain resiliency in the country. The U.S. government funding under the CHIPS and Science Act to encourage reshoring is helping demand in this segment which should accelerate over the coming years. Similarly, in the Transportation Solution segment, the company should benefit from good end-market demand driven by the Infrastructure Investments and Jobs Act (IIJA). So, I am optimistic about the company's growth prospects.

Margin Analysis and Outlook

In the second quarter of 2023, STRL's margins benefited from easing supply chain challenges and volume leverage. In addition, price increases and high margin backlog also helped the company in delivering margin expansion. This resulted in a 230 bps YoY increase in gross margin to 17.7% and a 200 bps YoY increase in operating margin to 11.5%. The margin growth was contributed by all the segments due to the improved project mix in the quarter.

STRL's Historical Gross Margin and Operating Margin (Company data, GS Analytics Research)

Looking forward, I believe the company should be able to deliver margin growth. Post-pandemic, the company saw headwinds from supply chain challenges which resulted in poor backlog execution and impacted margins. However, over the last couple of quarters, these supply chain challenges have meaningfully eased as material and resource availability has improved. So, moving forward, the incremental costs associated with supply chain inefficiencies should abate, supporting margin growth. Additionally, the price increases in the Building segment should also support the margin growth. Moreover, increasing volume leverage with good revenue growth should also support the margin expansion ahead. Further, the company continues to increase margins in the backlog by being highly selective in the bidding process.

STRL's Historical Margin in Combined Backlog (Company data, GS Analytics Research)

So, the overall margin outlook remains positive.

Valuation and Conclusion

Sterling is currently trading at a ~18.82x FY23 consensus EPS estimate of $4.09 and ~16.38x FY24 consensus EPS estimate of $4.70. This is a significant premium to its 5-year historical average FWD P/E of 11.10x.

While I understand that the stock deserves a re-rating given good growth drivers and excellent execution and frankly, that was my thesis when I previously covered the stock, I find after the recent run-up the company's growth prospects are appropriately getting reflected in the current valuations. The company's peer Granite Construction ( GVA ) which has exposure to some of the similar end markets and government spending is available at just 9.76x FY24 consensus EPS estimates. So, the chances of P/E multiple re-rating further from here are limited and the margin of safety isn't much. Hence, I am downgrading my rating to neutral and will wait on the sidelines for a better entry point.

For further details see:

Sterling Infrastructure: Moving To Sidelines Post The Recent Stock Price Run-Up (Rating Downgrade)