SHOO - Steven Madden: 2023 Could Be Challenging

Summary

- In line with consumer discretionary stocks, trends shoe maker Steven Madden has also seen an uptick in price. Can it continue to rise?

- There's a lot to like about its recent growth, margins, balance sheet and cash flow. Its full-year 2022 projections are also encouraging.

- But the projections also indicate a sharp sales contraction in Q4 2022 and a weakening in EPS to the lowest in six quarters.

- With macros expected to be weak in 2023, performance could falter further. It's not certain if SHOO can continue to rise even with an attractive current P/E.

Trendy footwear stock Steven Madden ( SHOO ) has risen by 13% in January 2023 so far. This isn't terribly surprising, considering that consumer discretionary stocks have seen an uptick as a whole. SHOO's performance is just shy of the S&P 500 Consumer Discretionary index, which is up by 14.5% . This is a decent start. The question now is, do its fundamentals justify the price rise or is it just based on improving market sentiment? And based on this, what could be next for the SHOO share price?

Slow but consistent growth

Steven Madden has a small market share at 1.9% compared to other publicly listed peers, where the market size is the sum of all their revenues. Nike for instance dominates the market with a massive 42% share of the revenues. Even Crocs is bigger, with a 2.7% share.

But it's a popular shoe brand, but the company has more under its belt like Dolce Vita, Betsey Johnson and Blondo among others. It's also a licensee to brands that include Anne Klein. Also, it's a growing company, albeit at a moderate pace. In the last 10 years, it has seen a CAGR in revenues of 4.3%. It did grow much faster in 2021 by 55.3% year-on-year (YoY), but this was largely a base effect. Compared to 2019 it grew by 4.4%, which is closer to its long-term average.

Positive outlook for 2022

This year looks like a bit of an exception. In its updated guidance published with the latest third quarter (Q3 2022) results , it now expects revenue to grow between 12.5% to 13.5%. This is almost 3x its average long-term growth. And this is after, it has reduced its guidance. It had earlier expected a revenue increase of 13% to 16% .

Similarly for its earnings expectations. It had earlier expected diluted earnings per share [EPS] to come in between $2.87 to $2.97. It now expects the number to be between $2.77 to $2.79. Despite this reduced guidance, it's interesting to note that at no time in the last 10 years has the company achieved this level of EPS.

Sustained margins

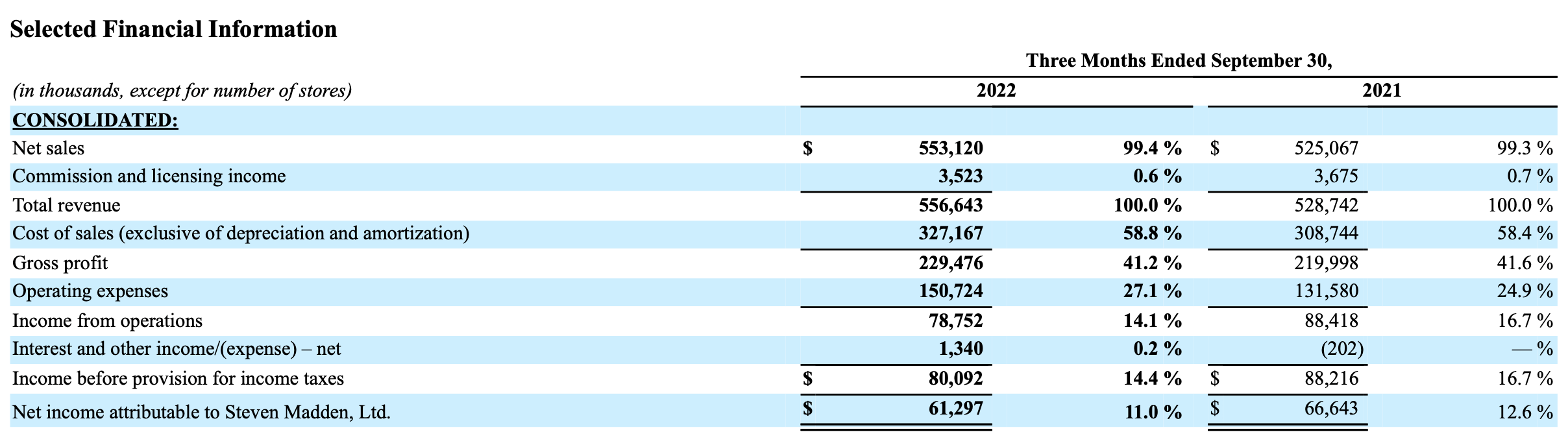

It would appear, that this is because of robust revenue growth of 55% and 34.5% in Q1 2022 and Q2 2022 respectively, which came off sharply to 5.3% in Q3 2022. But that's not true. First, the first quarter's growth had a huge positive base effect, as we were still in lockdown during the period in 2021. Second, at £229.5 million, the gross profit for Q3 is the highest in four quarters, and by extension in the year so far as the cost of revenue growth subsided sharply too.

In fact, it has also sustained gross margins at 40%+ levels in 2022 so far, a figure that was achieved in 2021 and continues to stay. Its latest operating margin at 14.1% isn't bad either, though it is a decline from the 16.7% level seen in Q3 2021. The margins are a standout feature for me considering how much high inflation has plagued consumer companies in a weak economy over the past year. It clearly speaks of the company's pricing power as also its ability to keep costs in check, which isn't all that common. In Q3 2022, its cost of revenues grew at under 6% and operating expenses by 14.5%.

{kind=link}

Note that both its operating income and net income in Q3 2022 have declined during the latest quarter compared to the same time last year. However, the overall picture for the year still looks healthy and going by the company's outlook will continue to do so for the final quarter as well.

The passive income advantage

Steven Madden's liquidity and debt position look healthy too. And it pays a dividend. Now, its dividend yield isn't the juiciest at 2.5% for the last trailing twelve months [TTM]. Especially not in the current inflationary environment. But it is a notch above that for the consumer discretionary sector at 2.3%. Further, since 2018 it has consistently paid dividends, save the pandemic period. Moreover, its TTM dividend payout ratio also looks good at 24.7%, indicating the potential for sustainability.

What the market multiples say

Despite these positives, the company's trading at a price-to-earnings (P/E) ratio of 11.2x, compared to the consumer discretionary sector average of 15.1x. However, its price-to-sales (P/S) is at 1.2x compared to 0.94x for the sector. In a nutshell, the market multiples imply different price directions for SHOO. Which way will it head now? To decide that, let's first consider the risks.

The devil in the details

So far so good. But when investing, we have to consider the company's future performance. If we just consider its full-year performance projections and even its revenue numbers up to Q3 2022, all looks well. But when considering what they mean for Q4 2022 figures, the picture looks more difficult. With around a 13% growth in revenue as forecast, the Q4 2022 projected revenue figure comes to around £457 million. This is a huge 21% YoY decline.

Some of this can be explained as a base effect. In Q3 2021, the company grew by a massive 76.1% YoY. But it is not entirely digestible. And here's why. In Q2 2021, the company had seen even bigger growth of 204.3%. But it still showed 28.1% growth despite this base effect in Q2 2022. So why does it expect a contraction in Q4 2022? My guess is declining demand.

I am even more cautious because double-digit growth is relatively recent for the company. This means that it doesn't have a history of growing rapidly, and could well fall back to low growth in the near future if demand conditions aren't conducive.

Shrinking earnings

Further, even though the company has sustained robust margins, SHOO's operating income and net income have shrunk from Q3 2021 in the latest quarter. Also, consider the earnings forecast. With a $2.8 diluted EPS expected in 2022, the forecast figure for Q4 2022 comes at $0.43, which would be the lowest seen in six quarters. That's also a 47% YoY decline. Its dividend payout ratio isn't bad at 40% right now, but it could rise, potentially putting future dividends at risk.

Macro risks to consider

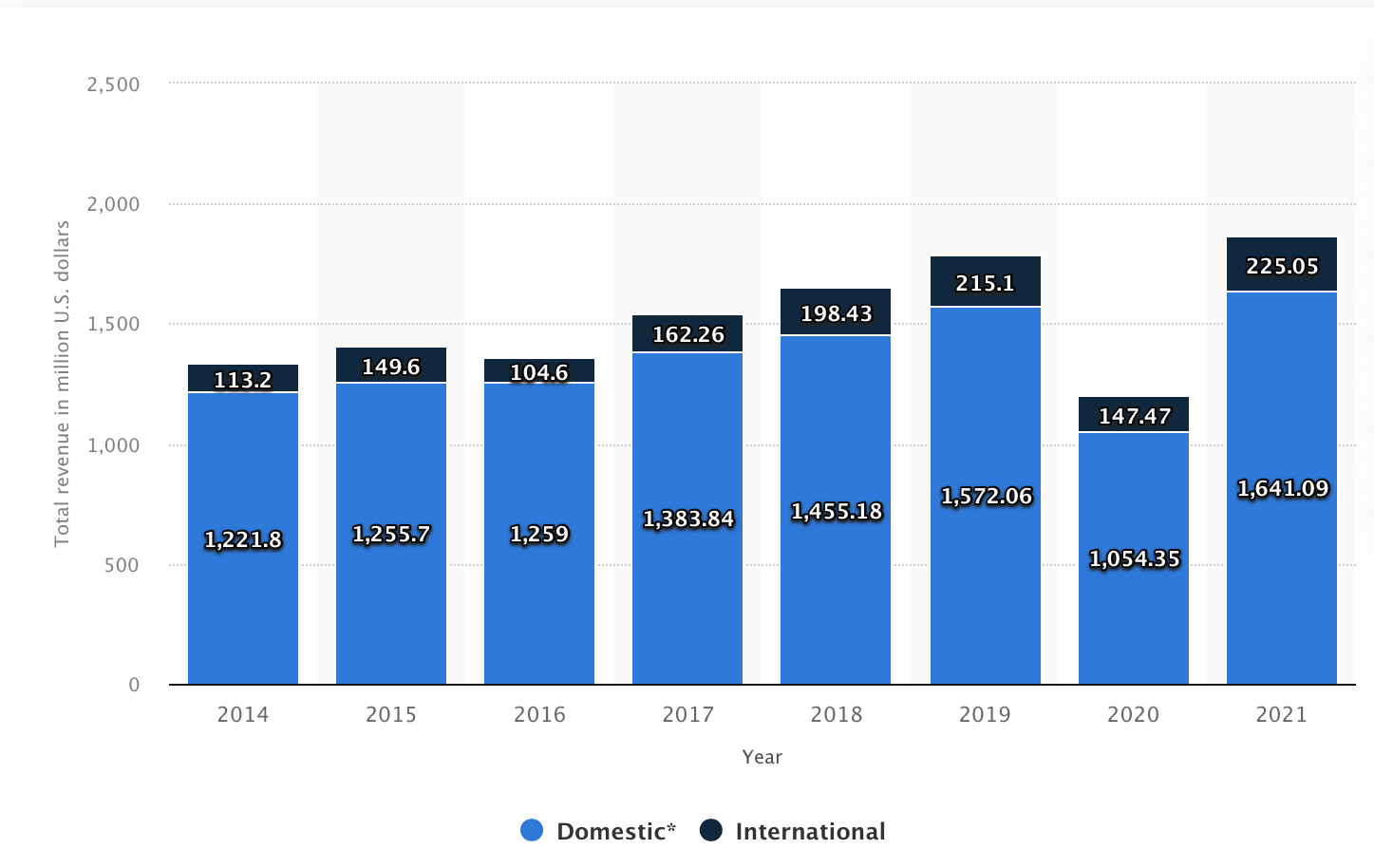

Importantly, the slowing down in Q4 2022 indicates that 2023 might not be as good for Steven Madden as the past year. We know that cyclical stocks like Steven Madden are particularly vulnerable to weak macro conditions. It's true that inflation has shown a sharp come-off in recent months in the US, its main market (see chart below), but forecasters don't expect it to decline to the Fed's target rate anytime soon. Further, while not everyone forecasts a recession in the US in 2023, these projections are very much around. This means, that it could be a worse year for consumer demand than the last.

Revenue by market (Source: Statista.com)

{kind=link}

What next?

In sum, we have a scenario where the company looks good right now but the outlook moving forward is weak. In terms of its positives, it's trading at a price much lower than where it was during the highs of early 2020 even though both its growth and earnings look better now. The company's margins are notable in the current climate of potentially high costs, indicating pricing power. Its balance sheet is robust, with little debt and its cash position looks good too. It doesn't hurt that it pays a dividend, and has been consistent with it over the past few years except during the slump caused by the coronavirus.

However, the risks have some serious weight to them. Both the expected numbers for revenue growth and earnings don't bode well. In Q4 2022, it actually expects an over 20% decline in revenues. Also, it will show the lowest EPS in 2022 in Q4 based on its projections. This may even tell on its dividends.

With the macroeconomic situation still looking shaky, this could be an indication of what comes in 2023. The company acknowledges the challenges it faces in its Q3 2022 update as well. Based on an uncertain future, which is already expected to show up in its upcoming numbers and still weak macros, it's best to be cautious. I'd Hold until it releases its next results, with guidance for 2023.

For further details see:

Steven Madden: 2023 Could Be Challenging