SHOO - Steven Madden: Gloomy Outlook

2023-04-15 02:42:47 ET

Summary

- Steven Madden's stock price might have seen an uptick this week, but its fundamentals do not indicate that this can continue.

- Not only did its performance suffer in Q4 2022, its 2023 outlook is weak and its guidance for the immediate future is cautious too.

- It is a good time to sell it while it is still at a relative high, considering that demand can drop more this year.

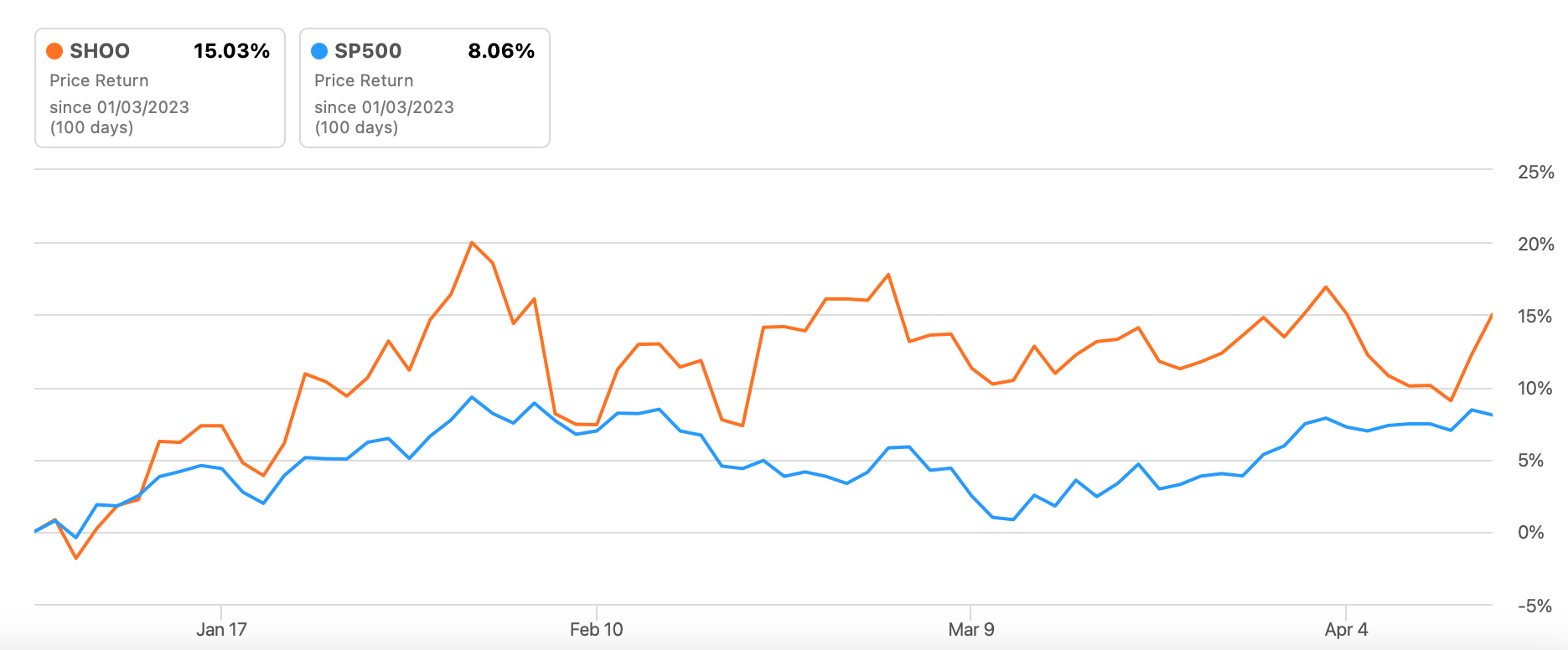

When I started writing about the Steven Madden ( SHOO ) stock in the middle of the week, its price performance was underwhelming, compared to when I last wrote about it in January. It was actually down by some 2% since.

But things are looking up for the shoe manufacturer since Citi’s positive outlook on the stock came through later this week. Enough to turn around its performance. It is actually up by 2.3% since my last piece on it now. It is also up by almost 15% year-to-date [YTD], though much of it is because of the bump up in consumer discretionary stocks in January this year.

{kind=link}

Weak performance

The big question now, as I see it, is can this upturn in performance continue? I am not convinced. Here is why. My article, which was titled “Steven Madden: 2023 Could Be Challenging” with a Hold rating on SHOO stock, was based on the weak demand outlook and lower profits likely in the year. The company’s own forecasts indicated as much.

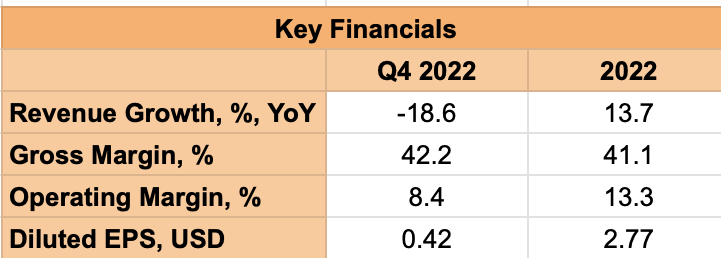

Its full-year outlook for 2022 was relatively muted compared to its performance for the first three quarters of the year, indicating a sharp worsening in the last quarter. This has played out, with an 18.6% year-on-year (YoY) decline in revenues in the final quarter of the year (Q4 2022). Diluted earnings per share [EPS] halved to USD 0.42 during the quarter from the same time last year.

{kind=link}

Gloomy outlook

At that time, however, I had still wanted to wait for the company’s outlook for the next year. When it released its full-year results in February this year, it became clear that 2023 is indeed expected to be a challenging year for Steven Madden. It expects its revenues to decline between 6.5-8%, down from a 13.7% rise in 2022, suggesting continued demand softening from Q4 2022. It also expects its full-year diluted EPS to range between USD 2.4-2.5 compared to USD 2.8 in 2022.

Forward P/E shows little upside

Considering the midpoint of the EPS forecast gives a forward GAAP price-to-earnings (P/E) ratio of 14.7x, which is a little over that for the consumer discretionary sector at 14.6x. This means, that based at least on this market multiple, there is little upside for Steven Madden. We can of course consider others, like its trailing twelve months [TTM] GAAP P/E, which is lower at 12.7x compared to the 15.3x for the sector, but it is probably not as relevant right now, considering the change in the company’s situation from last year to 2023.

The positives

There is of course the question now, why did Citi upgrade its rating for Steven Madden at this time, of all times? It so happens, that it expects the company’s tone to be more optimistic in its upcoming results, with a potential for demand upside as well as lower inventories. While this is in sharp contrast to the company’s own weak outlook, there are three points worth noting.

The first is that its inventory is indeed on the decline, reported at the lowest in five quarters in Q4 2022. And second, while there is little denying that the Q4 2022 figures have indeed dropped, they are a shade better than anticipated. My calculations had yielded a potential decline of 21% in the quarter.

The company could also benefit from a slowing down in cost increases as inflation comes off. In fact, it already has. In Q4, 2022, its cost of sales declined by 20.1% YoY, compared to a 13.6% increase for the whole year. Similarly, its operating cost were up by just 1.9% in the final quarter of the year, compared to a 13.9% rise in 2022.

Inflation figures have only improved since last year, with consumer price inflation in the US, its biggest market, down to 5% YoY in March 2022 , making it the slowest increase since May 2021. This could further reduce cost pressures, which in turn could stabilise its margins. Its gross margin is already quite strong, but this would certainly be helpful at a time when the company’s operating margin dropped to 8.4% in Q4 2022, the lowest in seven quarters.

The risks

Are the positives enough, though? I am not so sure. Consider the company’s immediate expectations. It says “We are cautious on the near-term outlook due to the challenging operating environment and conservative initial Spring orders from our wholesale customers as they prioritize inventory control.”

This indicates that at least for Q1 2023, the numbers might not be pretty. Also, the outlook for the US economy is still weak, with a recession possible in 2023. And finally, even if the inventories have declined, the inventory turnover ratio is still at 5.5x for the full year, which is higher than the 4.3x level seen in 2021.

What next?

It is of course likely as the overall scenario improves, Steven Madden will perform. We are already seeing a come-off in inflation, which could be good for its margins. But if there is indeed a recession this year in the US, its demand will suffer and impact its key financials. Its final quarter performance in 2022 and its outlook for 2023 suggest that much already. While it is true that its Q4 2022 performance was not quite as bad as expected, it was still quite poor.

At the same time, there could still be a case to buy it if the medium to long-term returns on it were strong. They are not. In fact, an investment in the stock over the last five years would have resulted in a 23% decline in the capital right now. And over the last 10 years, it has given just 20% returns. There is a dividend yield of 2.4% to consider, but it is not big enough to justify an investment in the company.

If anything, I think it is a good time to sell Steven Madden. Right now, its price is still high, but it could drop over the year or show indifferent performance at the very least. As and when its performance or outlook shows signs of improvement, it might be a good idea to reconsider it.

For further details see:

Steven Madden: Gloomy Outlook