STEW - STEW: An Attractive Equity CEF With Low Fixed Leverage Cost

2023-09-11 12:15:53 ET

Summary

- The SRH Total Return Fund is an equity-oriented closed-end fund with a large cap value tilt and a significant holding in Berkshire Hathaway.

- STEW has access to low-cost fixed leverage below 3%, giving it an advantage over other closed-end funds that pay higher variable cost leverage.

- The fund's net asset value (NAV) may be understated due to the way closed-end funds compute NAV when there are senior notes or preferred stock in the capital structure.

The SRH Total Return Fund (STEW) is an equity-oriented closed-end fund with a large cap value tilt and a big holding in Berkshire Hathaway (BRK.A) (BRK.B). It is quite attractive now because it has access to very low-cost fixed leverage, which gives it an advantage over other closed-end fund peers that are paying for much higher variable cost leverage.

This article is a follow-up to my last article on this fund back in November 2021. In April 2022, there was a name change from Boulder Growth and Income to SRH Total Return Fund, and the fund ticker also changed from BIF to STEW. I believe the fund is even more attractive now for two reasons:

1) The rise in interest rates have made their locked-in fixed cost senior note leverage much more valuable.

2) The fund discount is now above 19%.

Fund Background and History

After graduating from college with a business major, Stuart Horejsi inherited a family welding supply with shrinking margins. He was impressed with Benjamin Graham's book "The Intelligent Investor" and began investing profits from his family business in Berkshire Hathaway stock in 1980 when it was only $265 a share. Berkshire closed today at $550,000 a share, and Horejsi is now a billionaire.

Horejsi's net worth from the Berkshire Hathaway investments grew tremendously. He sold the family business in 1999, started a charitable foundation and formed several family trusts. He also entered the investment management business and assumed control of four closed-end funds where his family trusts were large shareholders.

The four Horejsi-controlled funds were later merged into one survivor fund, BIF, which was recently re-named the SRH Total Return Fund and the ticker was changed to STEW. Note that SRH stands for Stuart R. Horejsi. His family trusts now own 46.6% of the STEW shares.

Low-Cost Fixed Leverage

One of the main reasons I like STEW now is because the portfolio managers made a very savvy investment move a few years ago, and locked in a lot of low-cost fixed leverage. On November 5, 2020, the Fund issued senior unsecured notes in an aggregate amount of $225,000,000 in three fixed?rate series with maturities ranging from 2030 to 2035. The "locked-in" interest rates are all below 3%.

Senior Notes Table (STEW website)

Most of the leveraged equity closed-end peers of STEW pay much higher interest costs now for their leverage. Many funds use variable rate interest vehicles. For example, PDT is currently paying OBFR plus 70 basis points which is now around 6% and they were recently forced to reduce their distribution. Some other equity CEFs use preferred stock or repo rates for leverage which is also around 6%.

Understated NAV Value

There is an odd "quirk" in the way that closed-end funds compute NAV when there are senior notes or preferred stock in the capital structure.

From an economic viewpoint, a senior notes position issued for leverage purposes is similar to a short position in the senior notes in the portfolio. You would think the market value of the senior notes would be subtracted from total assets when computing NAV.

But that is not how it works. The rules require the principal value of the notes minus a deferred charge related to the note issuance costs to be subtracted when computing the NAV.

For example, this is how the NAV for STEW was computed in the Statement of Investments from the semi-annual report dated May 31, 2023:

Total Investments= 1,713,125,238.

Senior Notes = (223,263,615).

(net of deferred offering cost of $1,736,385).

Other Assets and Liabilities, Net (1,146,121).

==========

Net Assets Applicable to Common Shareholders= $1,488,715,502.

The $223,263,615 amount subtracted for the senior notes was computed by subtracting the deferred offering costs of $1,736,385 from the total principal outstanding of the notes which is $225,000,000.

But in the chart above, you can see that the estimated fair market value of the three senior notes on May 31, 2023 was only $183,814,562. If this reduced value is used for the negative NAV adjustment, the NAV would be higher by around $40 million.

Interest rates are even higher now than on May 31, so the fair market value of the senior notes is lower now, which means that the NAV of STEW is even more understated.

The senior notes were a private placement and are not publicly traded. There is no easy way to repurchase them at a discount in the secondary market. But STEW can easily hedge the exposure by just going long US Treasury or Agency bonds if they ever want to reduce their leverage which would lock in a nice positive interest rate spread.

Share Repurchases

For the 6 month period ended May 31, 2023, STEW did not repurchase any shares. But in the year ended November 30, 2022, they repurchased 469,255 shares of Common Stock at a total purchase amount of $6,259,136 at an average discount of 17.13% of net asset value.

Going forward, management said they will continue to consider making additional share repurchases based on their relative attractiveness compared to other available market opportunities. Now that the discount is approaching 20%, I would not be surprised if the fund managers have done some more share repurchases the past few months.

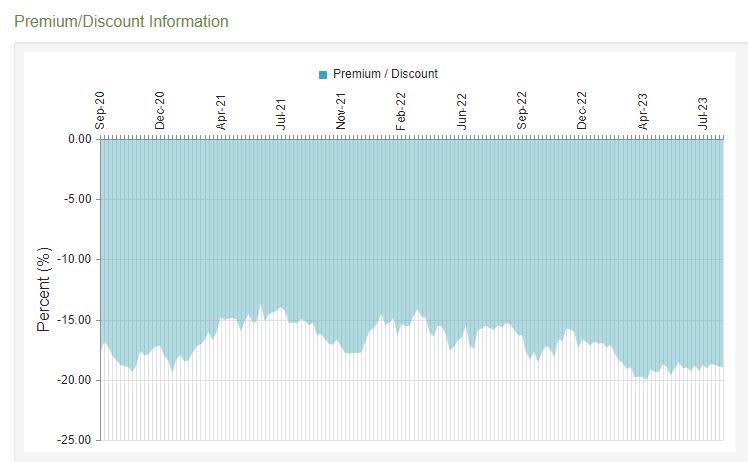

STEW- Three Year Discount History

STEW Discount History (CEFConnect)

{kind=link}

The NAV ticker for STEW is XSTEX and is reported to Yahoo Finance daily. As of September 1, 2023, the discount to NAV is -19.20%.

The fund had only 23 holdings as of the end July 2023, and the assets were highly concentrated with about 70% of the portfolio in the top ten holdings.

Here are the top ten STEW portfolio equity holdings as of July 31, 2023 taken from the fund website.

Top 10 STEW Holdings (as of 07/31/2023)

| ( BRK.A ) |

| Berkshire Hathaway-Class A |

| 29.56% |

| ( JPM ) |

| JP Morgan Chase & Co. |

| 8.72% |

| ( BRK.B ) |

| Berkshire Hathaway-Class B |

| 6.52% |

| ( YUM ) |

| Yum! Brands |

| 6.34% |

| ( EPD ) |

| Enterprise Products Partners LP |

| 5.20% |

| ( SWK ) |

| Stanley Black & Decker, Inc. |

| 3.63% |

| ( MSFT ) |

| Microsoft Corp. |

| 3.61% |

| --------- |

| State Street US Govt. Money Market |

| 3.52% |

| ( CSCO ) |

| Cisco Systems, Inc. |

| 3.47% |

| ( UTF ) |

| Cohen & Steers Infrastructure |

| 3.45% |

Aside from the large Berkshire Hathaway holding, STEW also owns several publicly traded holdings that are also owned by Berkshire Hathaway:

Stocks in STEW portfolio also owned by Berkshire Hathaway

| WMT |

| Wal-Mart Stores, Inc. |

| 1.85% |

| JNJ |

| Johnson & Johnson |

| 1.61% |

| AXP |

| American Express |

| 0.95% |

Total= 4.41%.

If you add the 36.08% Berkshire Hathaway holdings to the 4.41% holdings in stocks that are also held in Berkshire's portfolio, you get 40.5% of the STEW portfolio. This partially explains why the stock price tends to be highly correlated with Berkshire Hathaway. The rolling 24-month correlation coefficient is over 90% over the past few years.

Insider Ownership

As of May 31, 2023, trusts and other entities affiliated with Stewart Horejsi and his family owned 45.4 million shares or about 46.6% of the fund. The market value of these shares is around $620 Million, so Mr. Horejsi certainly has "skin in the game".

Valuation

A good rule of thumb to use for equity closed-end funds is to look for funds where the discount is at least 10 times more than the expense ratio. In general, very few closed-end funds meet this criteria. Based on this rule of thumb, STEW would be a decent buy when the discount is 12% or higher, since the baseline expense ratio is 1.20%.

One reason the discount for STEW tends to remain fairly high is because fund activism is not a possibility due to the large Horejsi fund holdings.

Another reason could be the $954 Million in unrealized capital gains which could become a tax issue at some point in the future if the fund ever decided to realize some of its very large gains in Berkshire Hathaway stock.

I mainly own STEW in tax deferred retirement accounts, so I am not concerned about the large amount of unrealized capital gains. But even if you own STEW in a taxable account, I think it is highly unlikely that Mr. Horejsi would want to realize large capital gains in the near future. It is more likely he will try to defer the gains and get a step-up in cost basis for his family trusts.

Low Expense Ratio Due to Discount Capture

A useful metric to look at is the adjusted expense ratio which takes into account how much alpha you earn from recovering net asset value from the annual managed distributions.

Let's compute the dividend yield enhancement and adjusted expense ratio for STEW.

Management has been using a managed distribution policy of $0.125 per quarter. At the current price level, the distribution yield is 3.70%.

Baseline expense ratio = 1.21% (Source: last S/A annual report).

Distribution yield (market) = 3.70%.

When you recover NAV from a fund selling at a 19.2% discount, the percentage return is 1.00/ 0.808 or about 23.7%.

Dividend yield enhancement alpha = 3.70% * 23.7%= +0.88%.

Adjusted Expense Ratio = 1.21% - 0.88%= 0.33%.

The adjusted expense ratio is reasonable compared to most of its peers. If you use an adjusted discount of about 21% to reflect the fair market value of the senior notes, the dividend yield alpha would be even higher.

Trading Liquidity

Since the 4-way fund merger some years ago, there has been reasonably good trading liquidity. The average 3-month daily trading volume has been 60,768 shares (Source: Yahoo Finance). This is equivalent to $830,000 a day. One reason why the trading volume is not higher is because a good portion of the float is owned by the Horejsi family trusts.

Institutional Ownership

Based on recent 13F SEC filings, some sophisticated institutional investors are invested in STEW. But activism is pretty much off the table because of Horejsi management's large fund holding.

Here are the current STEW shareholdings for some institutions that specialize in closed-end funds:

| Bulldog Investors L.P. |

| 1,097,043 |

| Shaker Financial Services LLC |

| 593,426 |

| Thomas J. Herzfeld Advisors, Inc. |

| 471,096 |

| 1607 Capital Partners, LLC |

| 135,503 |

Ticker: ((STEW)) SRH Total Return Fund

- Total Investment Exposure = $1,846 million.

- Total Common assets = $1,623 million.

- Current Quarterly Distribution = $0.125 ($0.50 per year).

- Annual Distribution Rate = 3.70%.

- Fund Baseline Expense ratio = 1.21%.

- Discount to NAV = -19.16%.

- Portfolio Turnover rate = 10%.

- Number of Holdings = 23.

- Average 3-Month Daily Trading Volume: 60,780 shares (Source: Yahoo).

- Average $ Volume: $830,000.

- Largest Holding: Berkshire Hathaway (about 36%).

Summary

STEW is a good core holdings for investors who want to stay invested in the stock market, but may be concerned about market valuation levels. It is a very solid fund that lets you sleep well at night. It has more of a value orientation with very limited exposure to the "Magnificent Seven" stocks that have driven most of the S&P 500 gains this year.

I would look to purchase STEW at a 17% discount or higher. It can be a good stock for swing traders, but is also an excellent holding for long-term buy and hold investors looking for a lower risk way to participate in the equity market.

STEW's expense ratio is a little on the high side, but its high discount and very low-cost fixed leverage below 3% easily compensates you for the management fee costs.

For further details see:

STEW: An Attractive Equity CEF With Low Fixed Leverage Cost