GOOD - Stick The Soft Landing

2023-07-16 09:00:00 ET

Summary

- U.S. equity markets advanced to their highest levels of the year on an "inflation week" rally after the closely-watched CPI and PPI reports showed a continued sharp cooldown in price pressures.

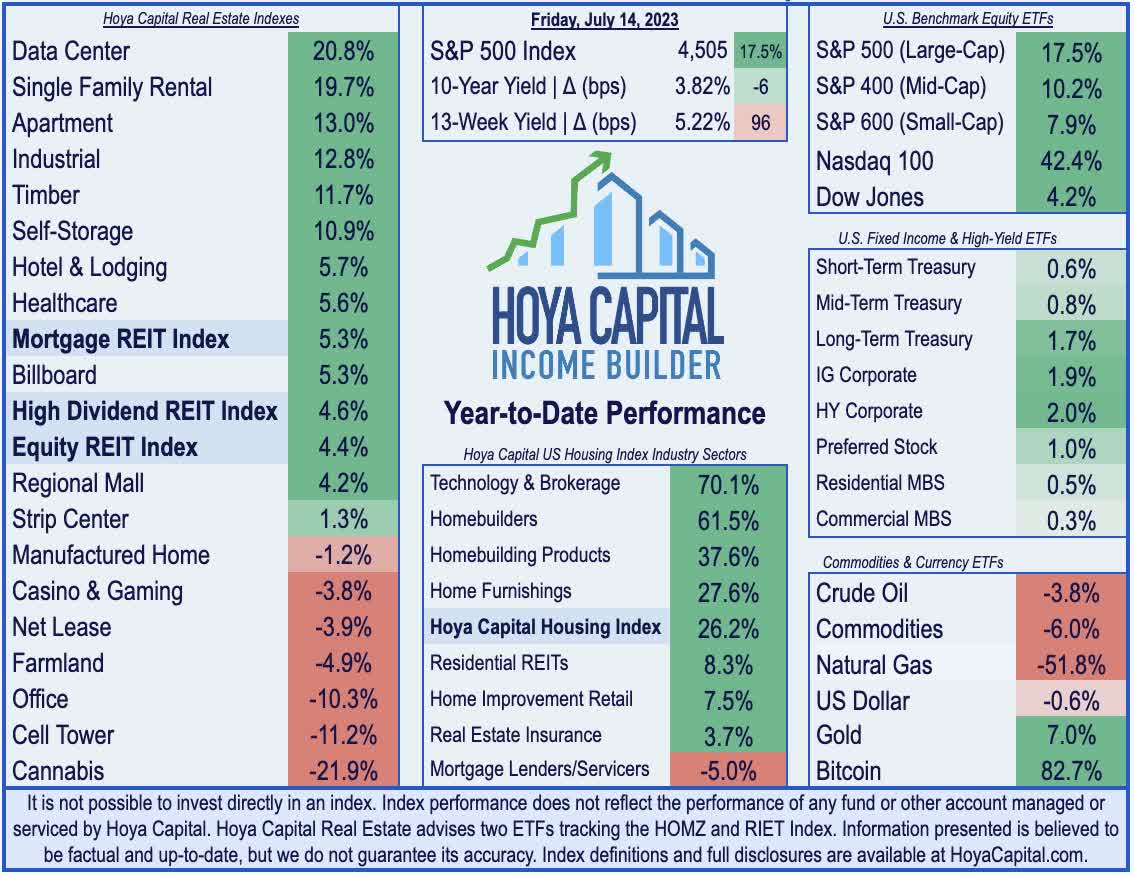

- Closing at the highest levels since April 2022, the S&P 500 advanced 2.4% this week, while the other major equity benchmarks - the Mid-Cap 400 and Small-Cap 600 - gained 3%.

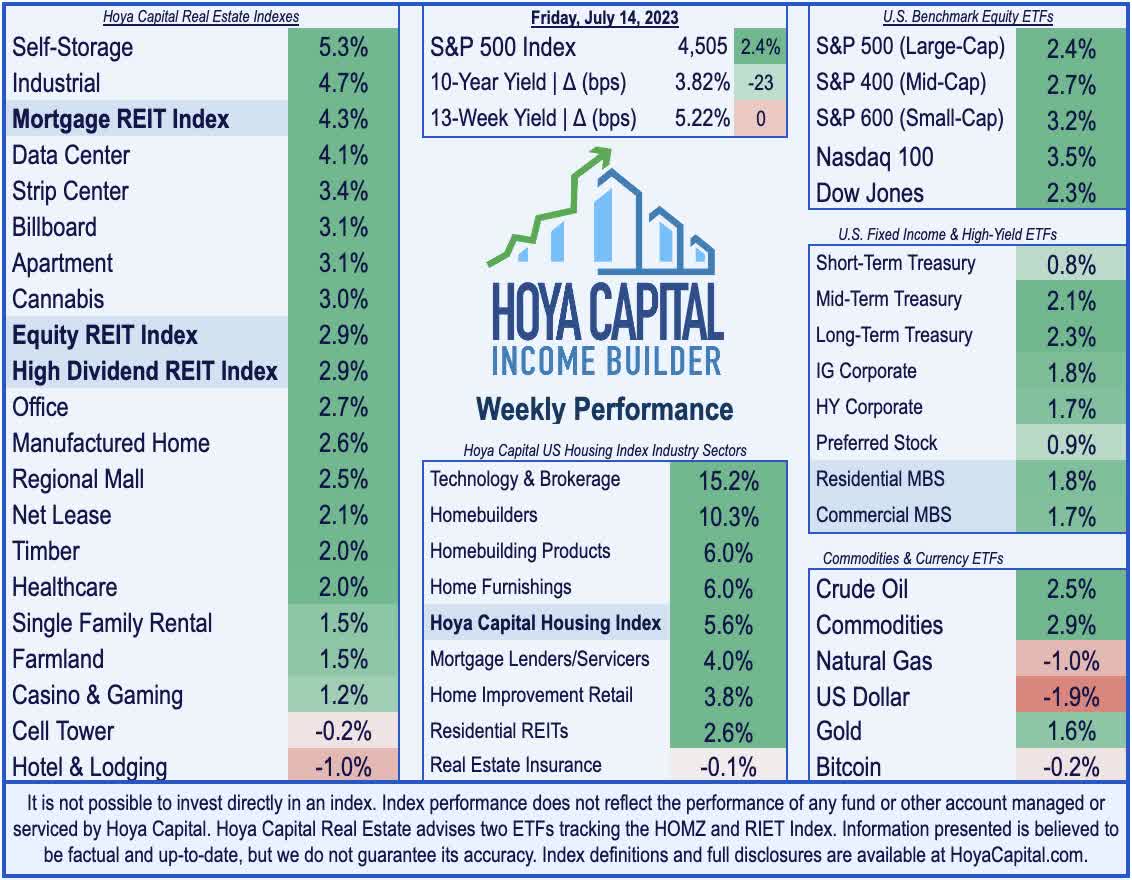

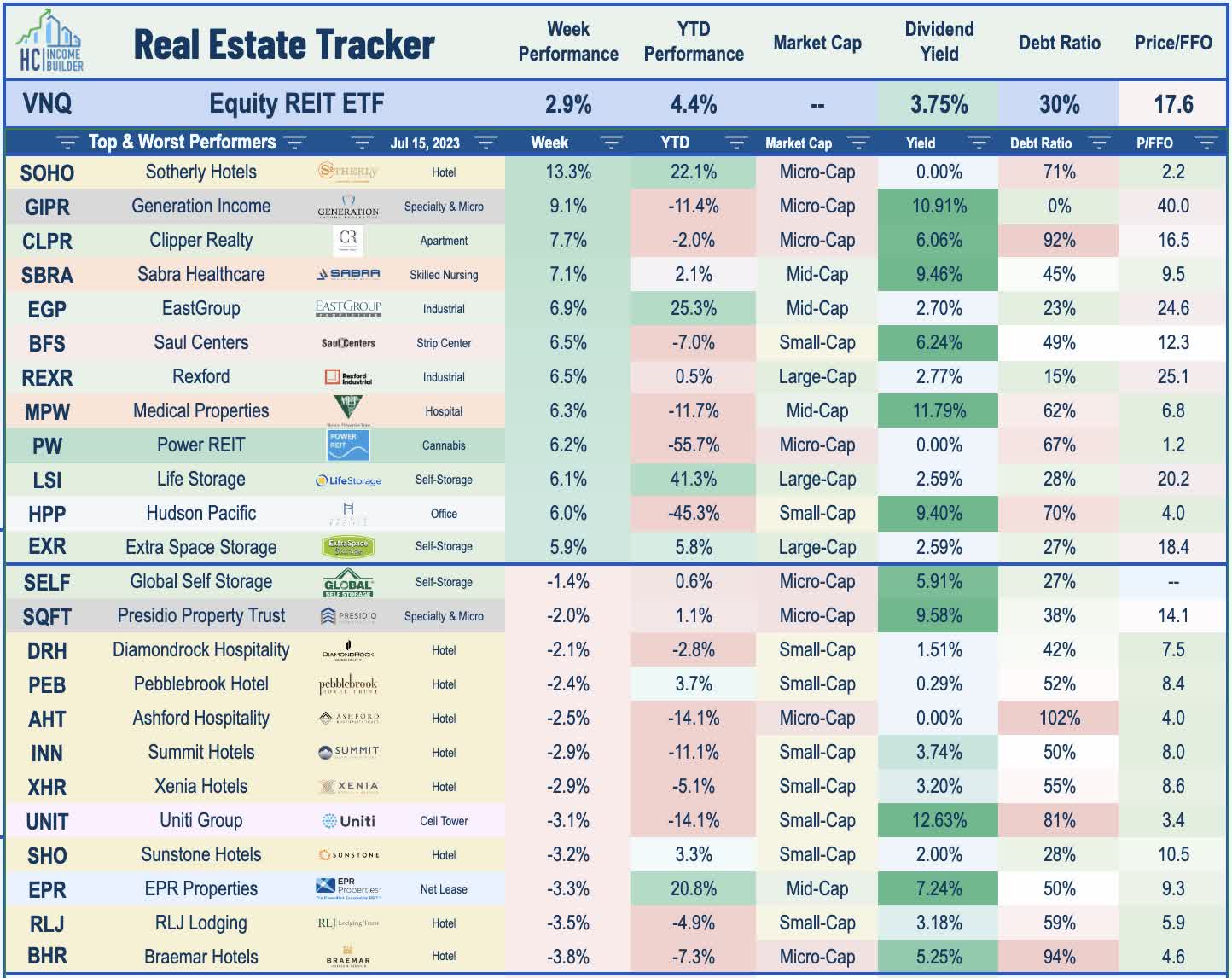

- Real estate equities- the sector with perhaps the most potential upside from a "soft landing" scenario- were among the leaders for a third straight week. The Equity REIT Index gained 2.9%.

- The "2-handle" on the headline CPI print and the "0-handle" on headline PPI clash with recent commentary from Federal Reserve officials speaking of "sticky inflation" that requires further demand softening.

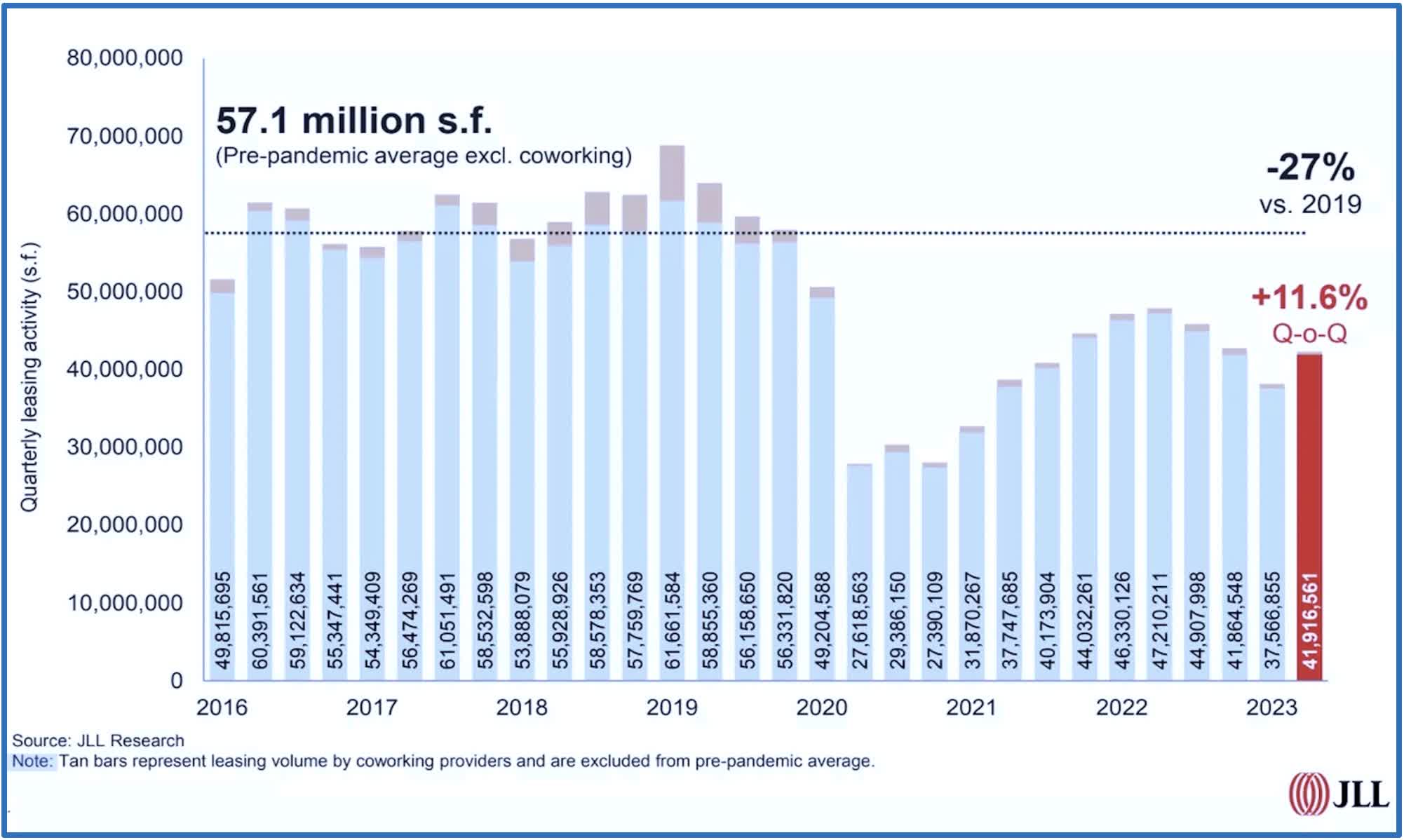

- Ahead of the start to real estate earnings season next week, brokerage firm JLL reported this week that office leasing activity rebounded 7.7% in Q2 compared to Q1, an encouraging sign that office demand may be showing early signs of stabilization.

Real Estate Weekly Outlook

U.S. equity markets advanced to their highest levels of the year on an "inflation week" rally after the closely-watched CPI and PPI reports showed a continued sharp cooldown in price pressures. The "2-handle" on the headline CPI print and the historically sharp decline in the year-over-year rate clashes with recent commentary from Federal Reserve officials, including from Richmond Fed President Barkin, who said this week "inflation has proven stubbornly persistent" and advocated for "weakening demand to control inflation" - perplexing commentary that appears to discount or outright ignore the last six-to-nine months of economic data in which inflation has cooled without a corresponding uptick in the unemployment rate.

{kind=link}

Hoya Capital

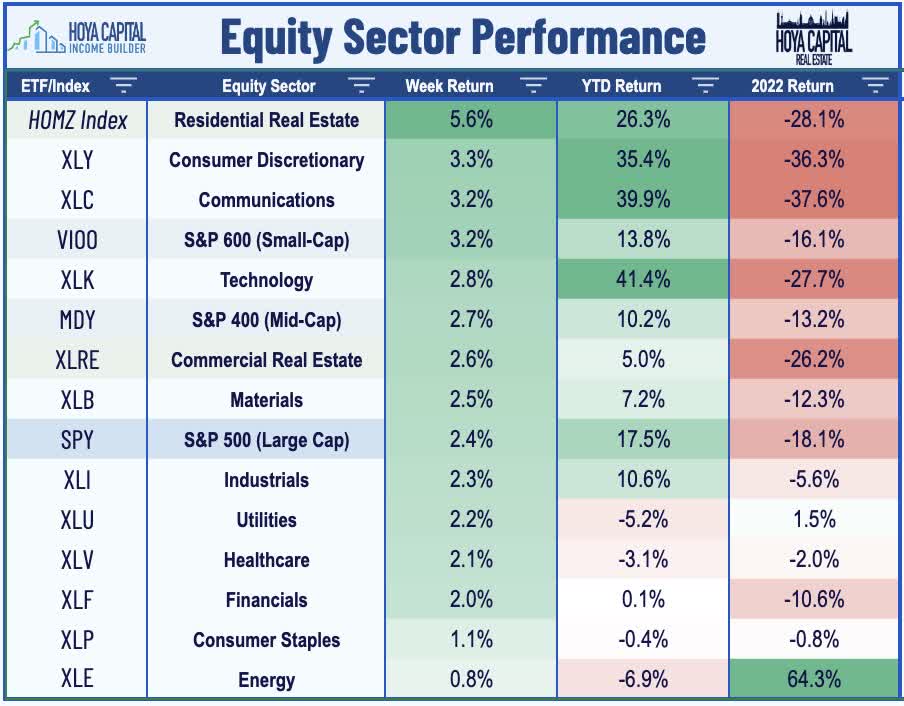

Closing at the highest levels since April 2022, the S&P 500 advanced 2.4% on the week, while the other major equity benchmarks - the Mid-Cap 400 and Small-Cap 600 posted gains of around 3%, as did the tech-heavy Nasdaq 100 . Real estate equities - the sector with perhaps the most potential upside from a "soft landing" scenario - were among the leaders for a third-straight week. The Equity REIT Index advanced 2.9% on the week, with 16-of-18 property sectors in positive territory, while the Mortgage REIT Index rallied more than 4%. Homebuilders and the broader Housing Index were leaders once again this week following another wave of encouraging housing market data - including a nearly quarter-percentage-point plunge in mortgage rates - which prompted another wave of upward analyst earnings revisions.

{kind=link}

Hoya Capital

Encouraging inflation data, combined with soft Chinese economic data, and the unexpected resignation of Fed Bank of St. Louis President James Bullard - who has been among the most "hawkish" Fed members in recent quarters - fueled the strongest week of the year for several of the major bond benchmarks. The 10-Year Treasury Yield plunged 23 basis points on the week to close at 3.82%, while the policy-sensitive 2-Year Yield dipped 21 basis points to 4.75% today. Even with monetary policy as restrictive as it has been since the period immediately before the Great Financial Crisis, and even with several major inflation benchmarks now below the Fed's 2% policy objective, swap markets still imply a nearly 95% probability of a 25 basis point Fed rate hike later this month, but rate markets see the July increase as the final increase in the Fed's most aggressive rate hiking cycle in history. Expectations of a pending pivot - and the fact that the U.S. inflation rate is now among the lowest among major economies - sent the US Dollar Index to its lowest levels in over a year.

{kind=link}

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

Hoya Capital

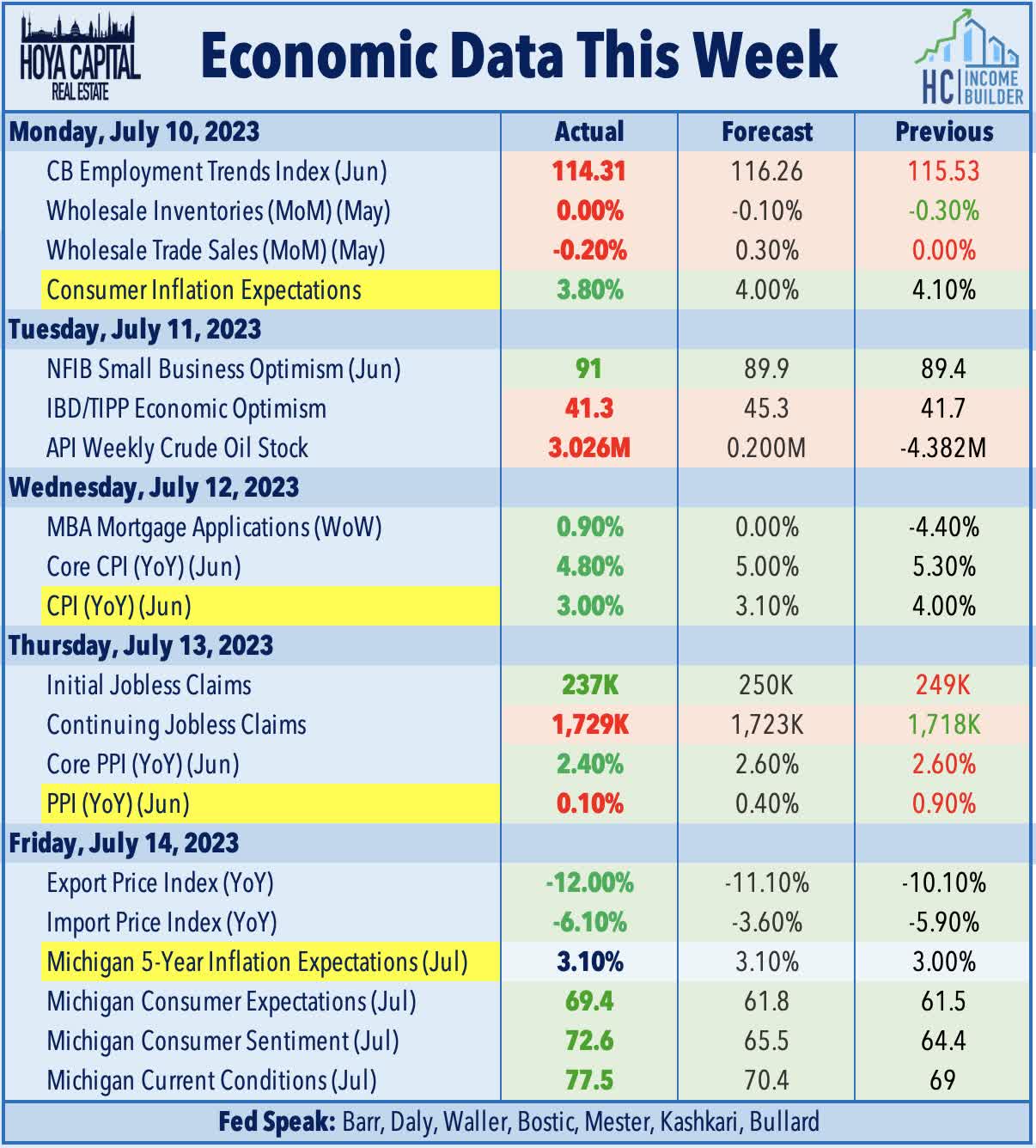

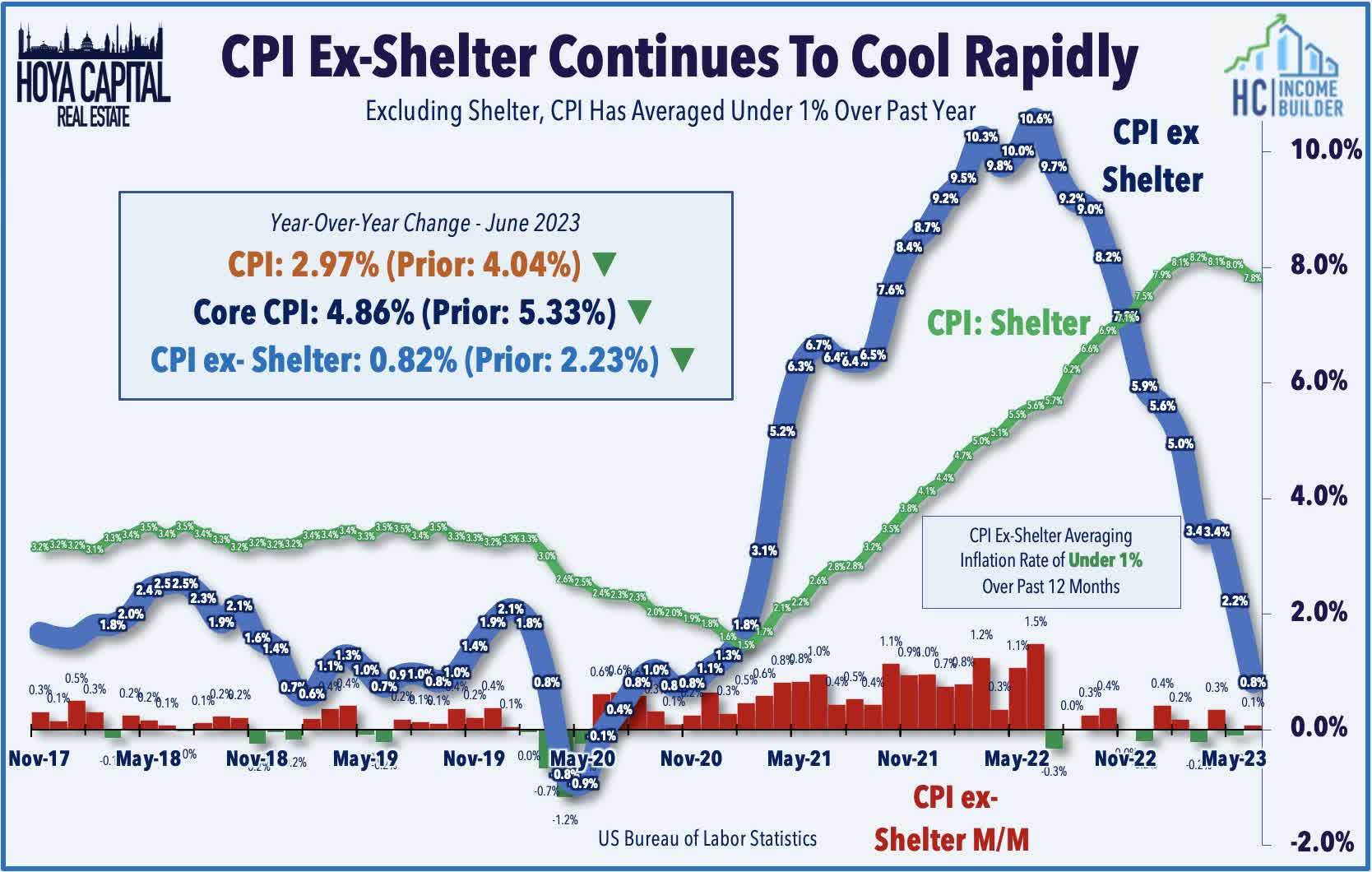

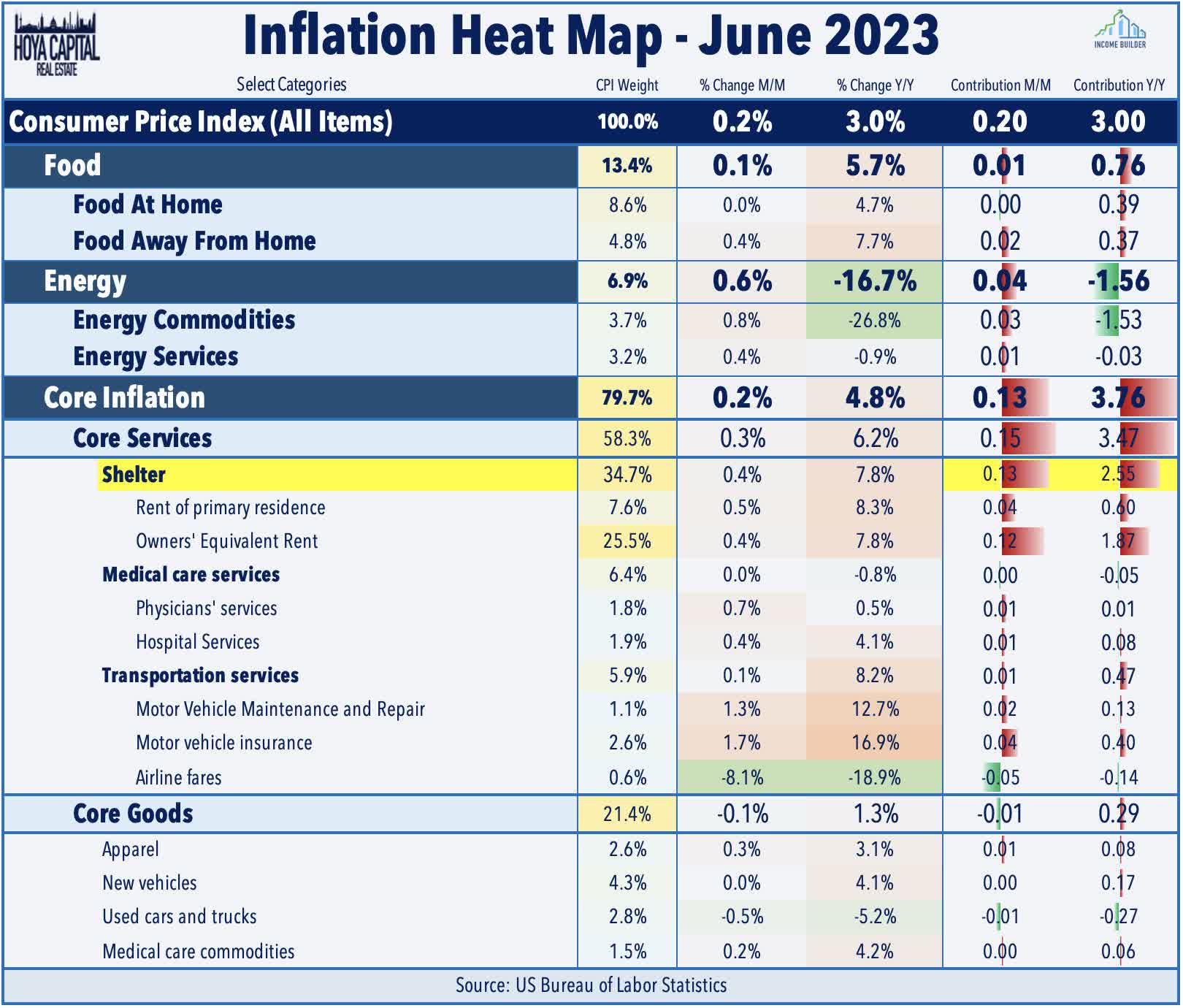

All eyes were on the Consumer Price Index report this week, which showed a sharp cooldown in inflationary pressures from the four-decade-high levels seen last summer. Headline CPI inflation moderated to a 2.97% year-over-year rate in June - down sharply from the 4.04% rate last month and below the 3.1% consensus estimate. As we've discussed since early in the pandemic, the delayed recognition of shelter inflation continues to heavily distort the headline and core metrics, resulting in an incorrect illusion of "sticky" inflation that has not existed in the corrected metrics (replacing the BLS rent series with an average of private market metrics from Zillow and others). Core CPI - which is dominated by the shelter component at a 60% weighting - has consequently been even more distorted. Core CPI remained relatively elevated at 4.9%, resulting from the 7.9% year-over-year increase in the Shelter index.

{kind=link}

Hoya Capital

Real-time shelter inflation data via Zillow, Case Shiller, and Apartment List show annual increases in rent and home prices ranging from -0.5% to 2.0%. The metric that we watch most closely - CPI-ex-Shelter Index - cooled to just a 0.82% year-over-year increase in June, as shelter inflation accounted for 85% of the overall increase in the year-over-year headline CPI figure and 65% of the month-over-month increase. Energy was a major downside contributor to the year-over-year rate as consumer gasoline prices are currently 25% lower year-over-year, while natural gas prices are over 60% lower from a year ago. Freight costs - another driver of consumer goods prices - are now lower by 80% from last year and 89% from the 2021 peak.

{kind=link}

Hoya Capital

Following the cooler-than-expected Consumer Price Index report, the Producer Price Index data the following day showed an even sharper moderation of price pressures. The headline PPI rose 0.1% in June - below the 0.2% increase expected - which, combined with downward revisions to prior months, dragged the annual increase to just 0.1%, its lowest reading since August 2020. Goods costs fell 4.4% from a year ago, the biggest decline in more than three years. Food prices at the producer-level dropped for a third month, suggesting future downward pressure on the closely-watched CPI food index. Excluding the volatile food and energy components, Core PPI also barely rose from May and was up 2.4% from a year ago, which was the smallest annual gain since January 2021. Forward-looking indices in the PPI report showed even more significant deflation coming through the supply chains. The PPI Index for Unprocessed Goods for Intermediate Demand is lower by 32.2% in June, the most significant deflationary one-year period on record for that index.

{kind=link}

Hoya Capital

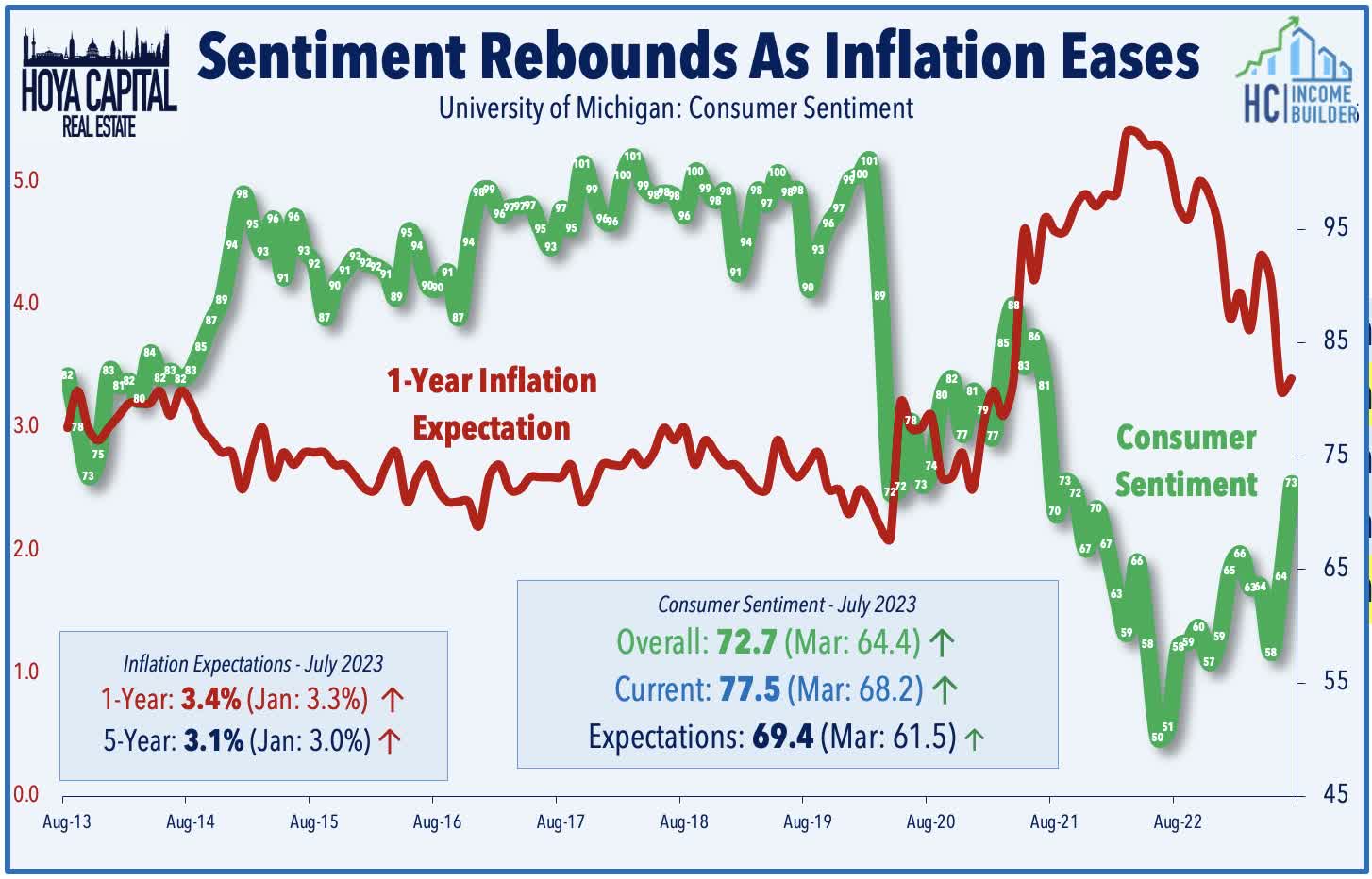

The week of encouraging news on the inflation front concluded on a mildly sour note via the Michigan Survey of Consumers data on Friday, which showed a slight uptick in consumer inflation expectations alongside a surprisingly sharp rebound in consumer confidence in early July. Inflation hawks harped on the modest uptick in 1-year and 5-year inflation expectations, which followed a historically sharp decline in inflation expectations during the prior month. Earlier in the week, the New York Fed reported that its Survey of Consumer Expectations showed that inflation expectations declined for the third consecutive month to reach 3.8% at the short-term horizon, its lowest reading since April 2021. Expectations were unchanged and slightly up to 3.0% at the medium- and long-term horizons. Home price growth expectations rose to its highest level in almost a year. Households’ perceptions and expectations for credit conditions and their own financial situations improved slightly.

{kind=link}

Hoya Capital

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hoya Capital

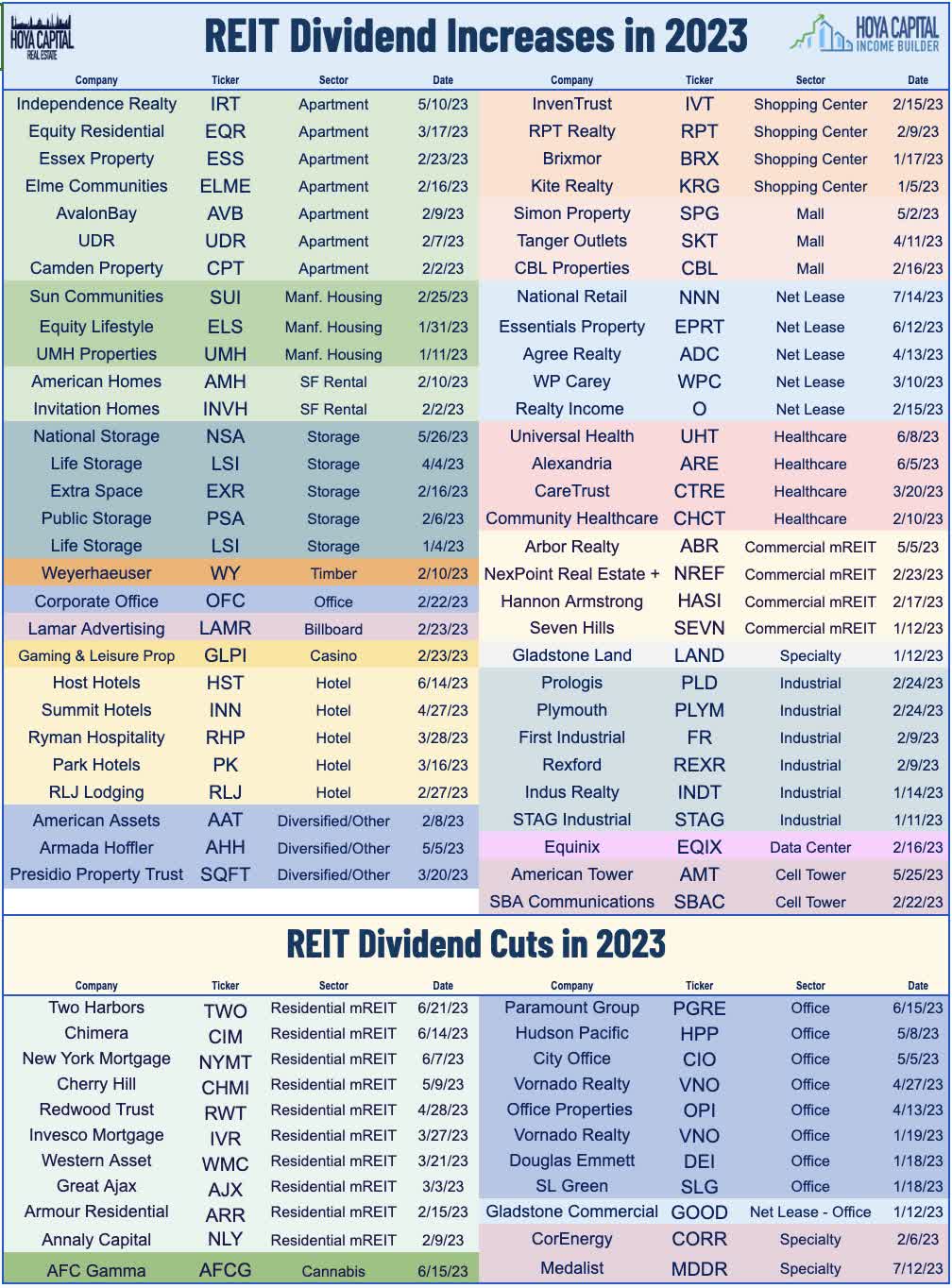

Real estate earnings season kicks off next week with reports from a half-dozen REITs. On Monday, we'll hear results from manufactured housing REIT Equity LifeStyle ( ELS ). Industrial REITs Rexford ( REXR ) and First Industrial ( FR ) report on Wednesday, as does cell tower REIT Crown Castle ( CCI ) and office REIT SL Green ( SLG ). We'll see results on Thursday from net lease REIT Alpine Income ( PINE ). Speaking of net lease REITs, National Retail Properties ( NNN ) gained 2% this week after it raised its quarterly dividend by 3% to $0.565/share (5.23% dividend yield), becoming the 5th net lease REIT and 59th REIT across all sectors to raise its dividend this year, a wave of dividend hikes that has been partially offset by 22 dividend reductions this year, primarily seen in the office and residential mortgage REIT sectors. Micro-cap Medalist Diversified ( MDRR ) added its name to the "cut list" this week after announcing that it would suspend its dividends on its common and preferred stock for at least the next six months after it decided to sell its interests in four properties after concluding a review of strategic alternatives.

{kind=link}

Hoya Capital

Office : Brokerage firm JLL ( JLL ) reported this week that office leasing activity rebounded 7.7% in Q2 compared to Q1, an encouraging sign that office demand may be showing early signs of stabilization. The 40.4 million square feet of space leased in the second quarter was still roughly 14% below the same period a year ago and still about 25% below the pre-pandemic average from 2016-2019. In our latest Office REIT report, we noted that there is more nuance to the story than what the prevailing narrative would suggest. Debt service expenses have been the primary culprit behind the wave of recent loan defaults on coastal office properties from private equity firms Brookfield, Blackstone, and Pimco, and the eight dividend cuts from office REITs. Nationally, property-level cash flows and occupancy rates remain within 5% of pre-pandemic levels, but actual utilization rates continue to exhibit a wide regional variance. Coastal tech-heavy markets remain at sub-50% daily utilization rates compared to pre-pandemic levels, but Sunbelt and secondary markets - most with less costly commutes - have recovered to over 75%.

{kind=link}

Hoya Capital

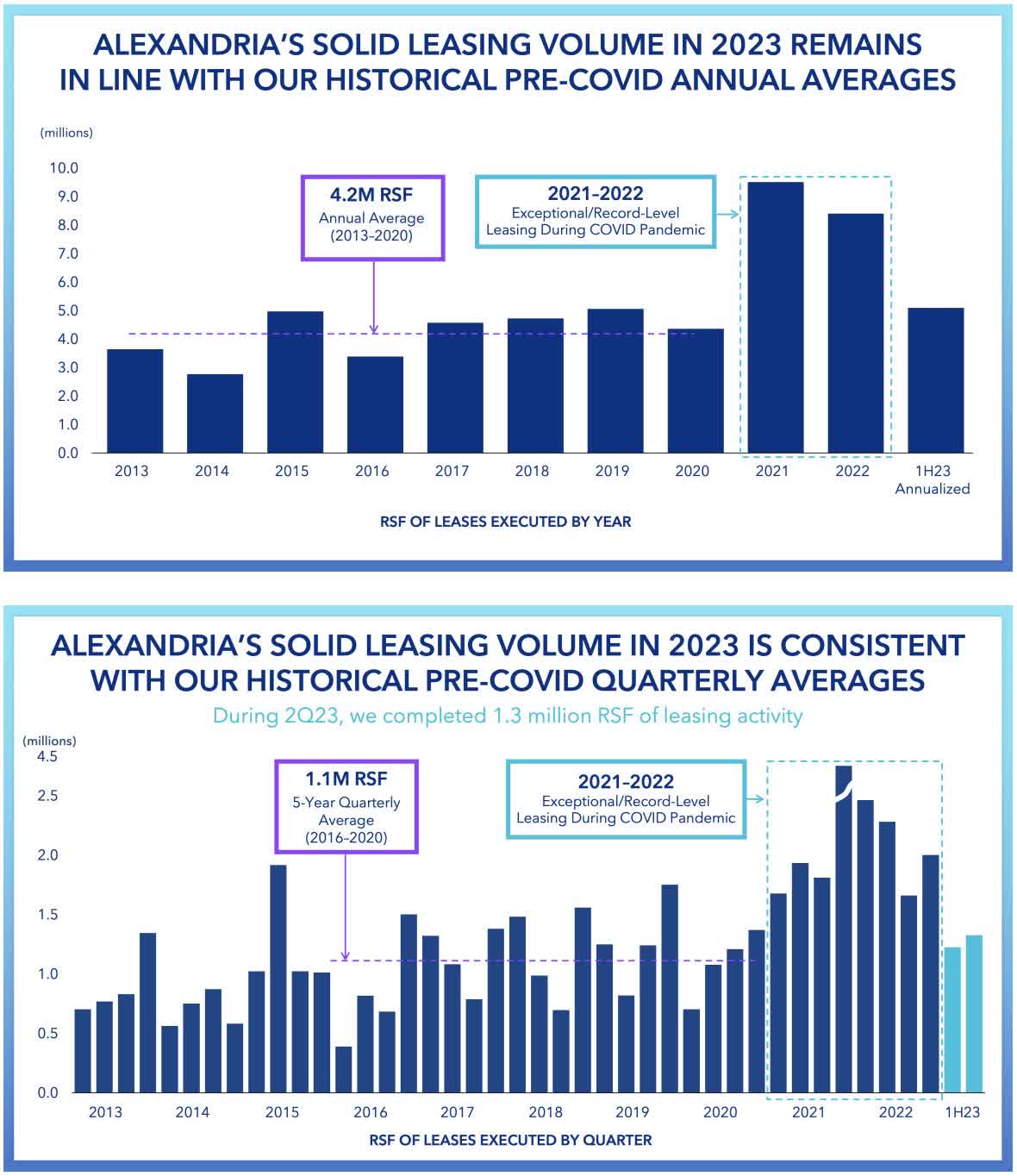

Healthcare : Lab space operator Alexandria Real Estate ( ARE ) - which has come into the cross-hairs of short-sellers in recent months - gained about 2% this week after it released preliminary second-quarter operating metrics and updated full-year guidance in a 10-K filing. ARE recorded total leasing volume of 1.1M square feet in Q2 - down slightly from the 1.2M SF signed in Q1 - and on these leases, it achieved cash rent increases of 16.6% GAAP/ 8.3% cash compared to the prior rent, a rate of increase that was down from its record-high spreads in Q1 of 48.3% GAAP / 24.2% cash. Notably, ARE downwardly revised its full-year FFO guidance to reflect several recent asset sales and the previously-announced impairment related to a Boston property - 275 Grove Street - where it dropped plans to convert the office space into lab space. ARE, however, maintained the midpoint of its outlook for full-year adjusted FFO at $8.96 - representing a 6.5% increase from 2022 - and maintained the midpoint of its outlook for full-year average occupancy at 95.1% and for cash rental rate spreads at 14.5%.

{kind=link}

Hoya Capital

Net Lease : Gladstone Commercial ( GOOD ) - a net lease REIT focused primarily on office properties - rallied nearly 5% on the week after it provided preliminary second quarter metrics. GOOD noted that it collected 100% of Q2 rents and that its portfolio occupancy stood at 96.0% at the end of Q2, up 10 basis points from Q1. GOOD signed 859k square feet of new and renewed leases - which was more than double the volume in Q1 - covering eight tenants with a weighted average remaining lease term of 8.9 years. Global Net Lease ( GNL ) also advanced more than 5% this week after it announced that it signed a definitive purchase and sale agreement to sell an office property it owns in San Jose, CA for a contract sale price of $50 million noting that the Company had originally acquired the property in 2014 for $52.5 million. In our recent Net Lease report, we noted that private market values for net lease assets have remained far "stickier" than comparable public market assets. Despite the tighter investment spreads, the pace of acquisition activity for some REITs slowed only modestly in late 2022, a strategy that could prove costly if rates remain persistently elevated.

{kind=link}

Hoya Capital

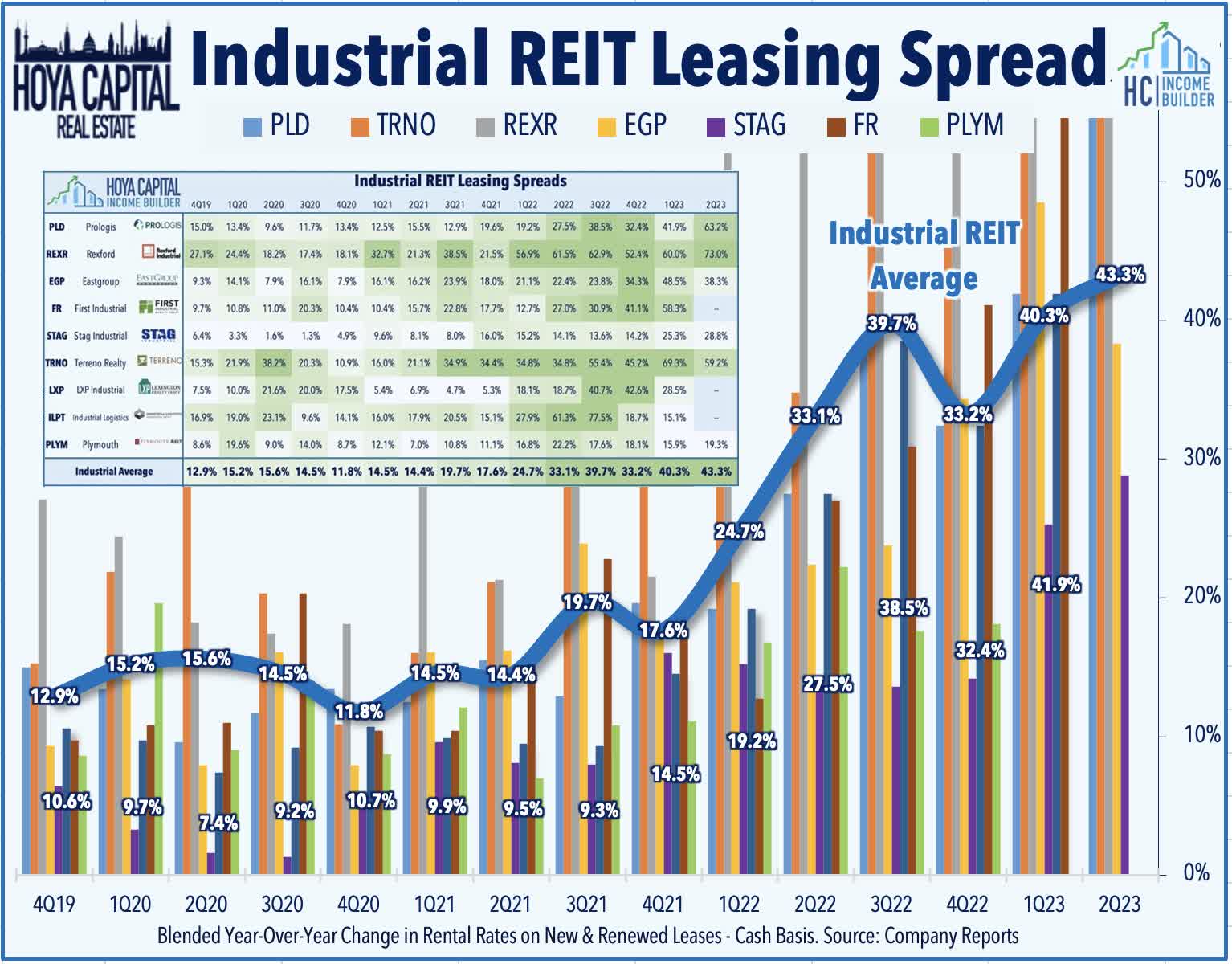

Industrial : Terreno ( TRNO ) advanced 2% on the week after it announced preliminary second-quarter metrics. TRNO noted that its same-store portfolio was 97.8% leased in Q2 - down slightly from the 98.1% rate in Q1. TRNO achieved blended cash rent spreads of 59.2% on 800k square feet of leases - down from the record-high rate of 69.3% in Q1, while its tenant retention ratio stood at 51.7%, also down slightly from its Q1 retention ratio of 54.4%. TRNO's acquisition pace also slowed rather considerably in Q2, noting that it acquired $13M of properties in Q2 following a haul of nearly $400M in Q1. In our latest Industrial REIT report, we noted that strengthening logistics rent growth last quarter came despite substantial downward pricing power across other areas of the supply chain. Four of the six industrial REITs that have provided Q2 leasing spreads have reported an acceleration from Q1.

{kind=link}

Hoya Capital

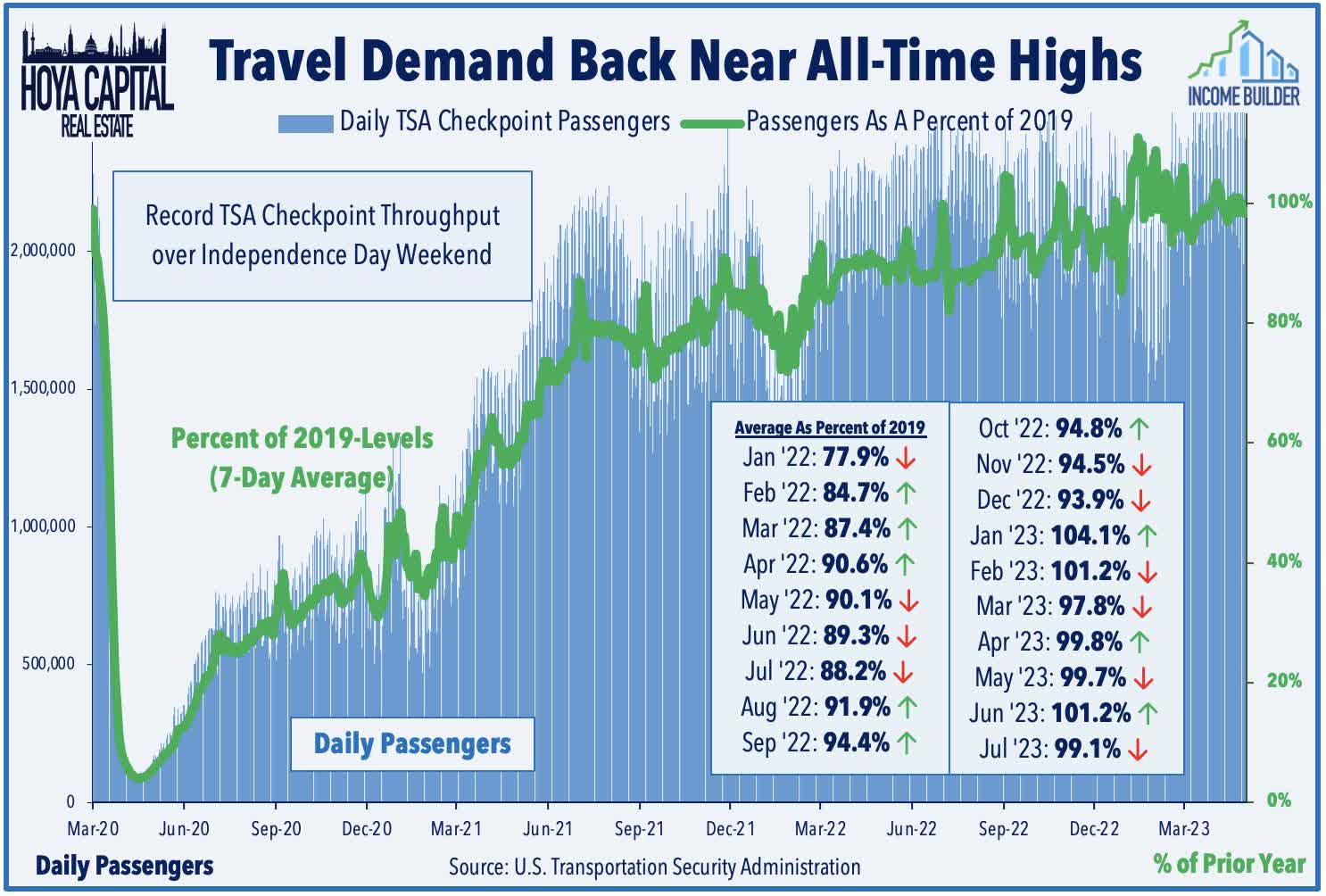

Hotel : Ashford Hospitality ( AHT ) - a small-cap externally-managed hotel REIT that owns 100 hotels across 26 states - slumped 3% on the week after it announced a "strategic decision" to hand back the keys to lenders for 19 of its hotels. The hotels were financed across three pools of commercial mortgage-backed securities loans that matured in June, and AHT commented the required $255 million in paydowns to extend loan terms would represent "negative equity value" after the company unsuccessfully marketed several of the hotels but did not receive any bids above the amount owed on the properties. The most highly-levered hotel REIT heading into the pandemic - and one of the few public REITs that made heavy use of variable-rate debt - Ashford barely managed to survive the pandemic, but has taken a fresh leg lower over the past year amid the sharp rise in benchmark interest rates. AHT commented that the decision will lower its net debt to gross assets ratio by three percentage points, and improve its revenue per available room ("RevPAR") by roughly 3%. AHT's struggles come despite robust travel demand, as the TSA reported last week that it processed record-high throughput at its checkpoints during the Independence Day week, peaking at nearly 3 million travelers for the first time ever.

{kind=link}

Hoya Capital

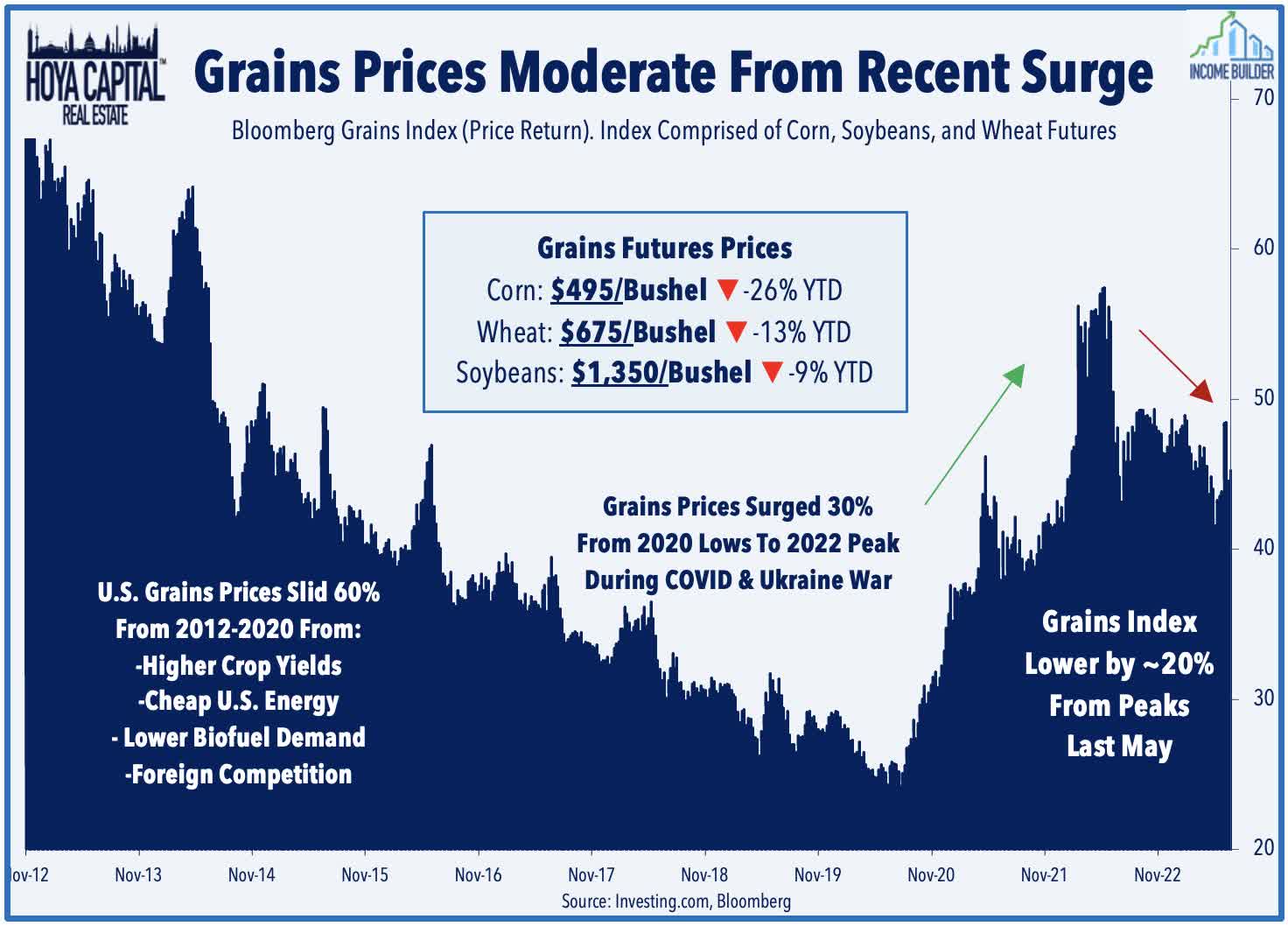

Timber & Farmland : This week, we published Land REIT: Disinflation Headwinds . One of the hottest "inflation hedges" during the pandemic, land REITs have fallen out of favor of late as rising rates and normalizing supply chains have created disinflationary - and even deflationary - headwinds for commodities. While services sector inflation remains sticky, goods-related inflation has fallen dramatically over the past nine months, with some inflation reports now showing levels of deflation that compare only to the Great Financial Crisis. Grains prices have declined 25% from their 2022 peak despite the ongoing Russia/Ukraine War, while lumber prices are lower by more than 50% from their pandemic-era highs. Timber REITs have benefited from a rebound in home construction activity this year and while long-term fundamentals remain attractive given pent-up housing-related demand, near-term upside now appears limited given the sector's elevated valuations. Farmland REITs, however, have stumbled amid a "triple whammy" of headwinds, but the selloff has brought valuations to reasonable levels.

{kind=link}

Hoya Capital

Mortgage REIT Week In Review

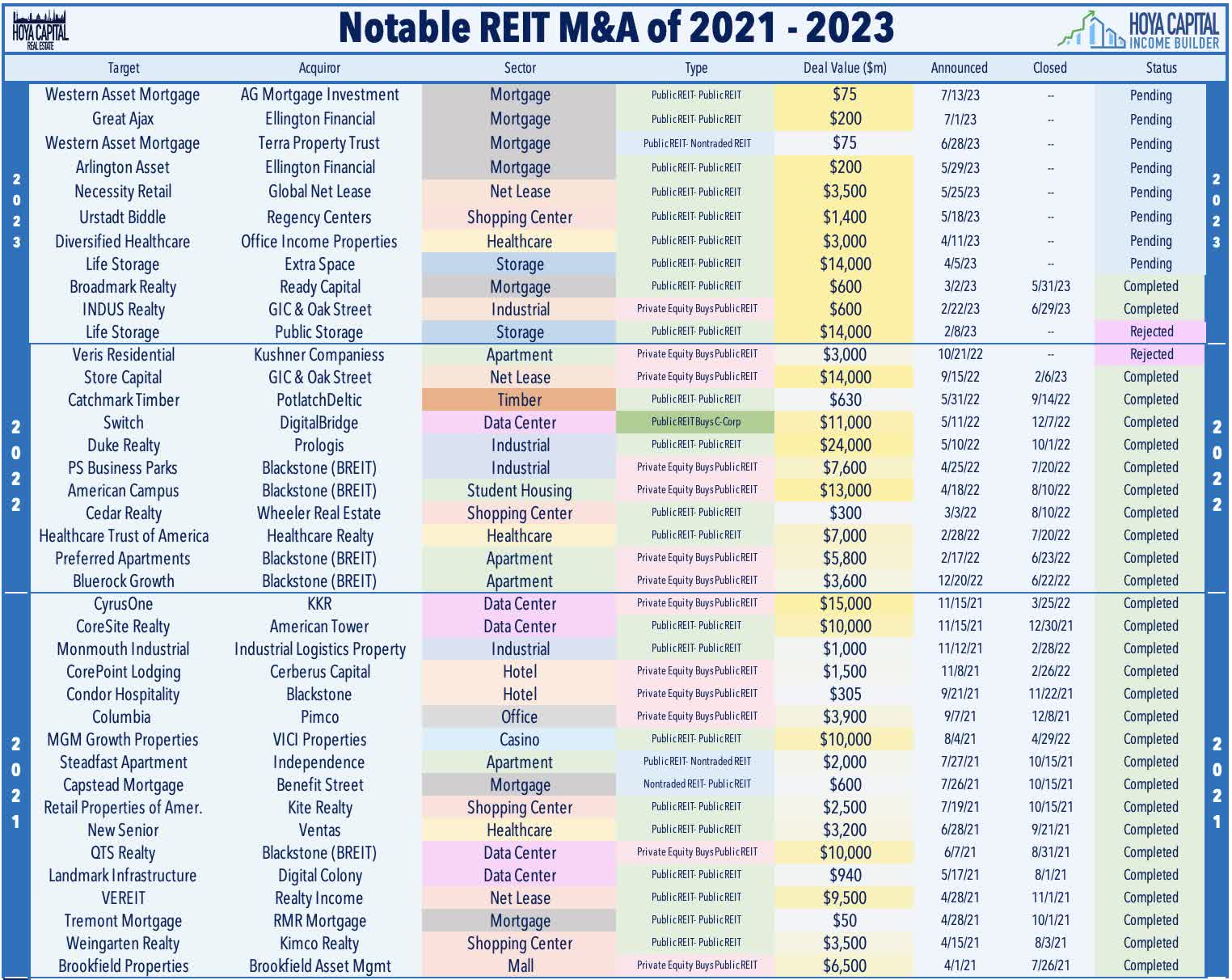

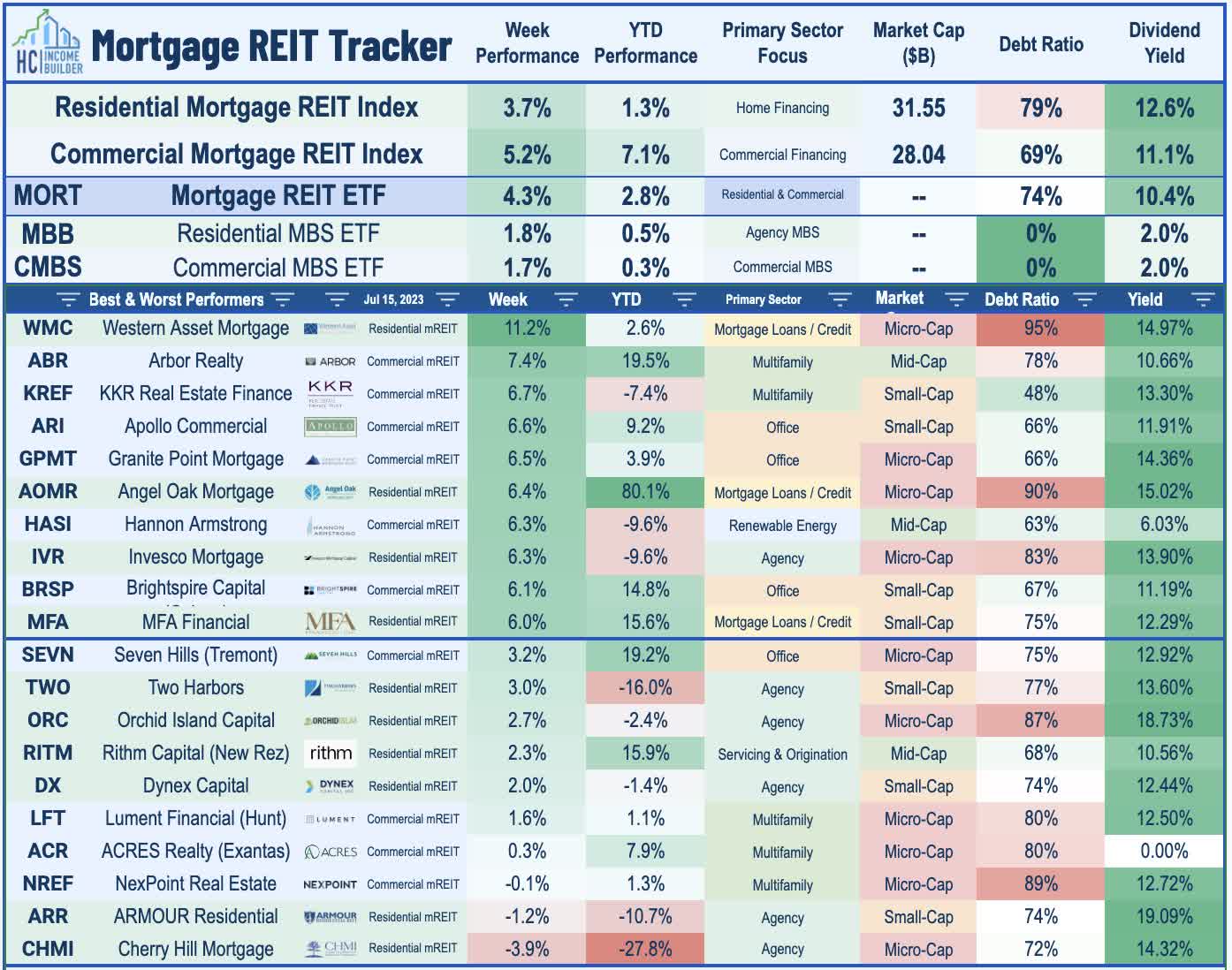

Another week, another mortgage REIT merger. Western Asset Mortgage ( WMC ) rallied 11% on the week after it received a competing merger bid from fellow mREIT AG Mortgage ( MITT ), which followed an announcement from WMC last month that it had agreed to merge with non-traded REIT Terra Property Trust . The bid from MITT - which also gained about 6% on the week - calls for a stock-and-cash deal at an implied price of $9.88 per share, consisting of a stock consideration of $8.90 per share and cash consideration of $0.98 per share. WMC - which has a market cap of just $50M - reported that its GAAP book value per share was $16.46 at the end of Q1. Terra issued a press release the following day that reaffirmed its intention to merge with WMC and outlined its case explaining why its merger plan is superior to the competing bid. The deal is the fifth mREIT-to-mREIT mergers proposed over the past quarter, and follows Ellington Financial's ( EFC ) proposed acquisitions of Great Ajax ( AJX ) and Arlington Asset ( AAIC ), and Ready Capital's ( RC ) acquisition of Broadmark Realty.

{kind=link}

Hoya Capital

More broadly, mortgage REITs posted broad-based gains for the week, with the iShares Mortgage REIT ETF ( REM ) advancing 4.3% to climb back into positive-territory for the year on a price-return basis. Orchid Island ( ORC ) was among the laggards this week - but still gained nearly 3% - after it provided preliminary Q2 results, noting that its GAAP EPS rose to $0.25/share - covering its $0.16/share dividend - but noted that its Book Value Per Share declined about 3% during the quarter. Elsewhere, the four REITs that declared dividends this week held their payouts steady at current levels: AGNC Investment ( AGNC ) held its monthly dividend at $0.12/share (14.1% dividend yield), Dynex Capital ( DX ) held its monthly dividend at $0.13/share (12.5% dividend yield), Ellington Residential ( EARN ) held its monthly dividend at $0.08/share (13.4% dividend yield), while Ellington Financial ( EFC ) held its monthly dividend at $0.15/share (13.0% dividend yield). The majority of mortgage REITs will report earnings in the final week of July and first week of August.

{kind=link}

Hoya Capital

REIT Capital Raising & REIT Preferreds

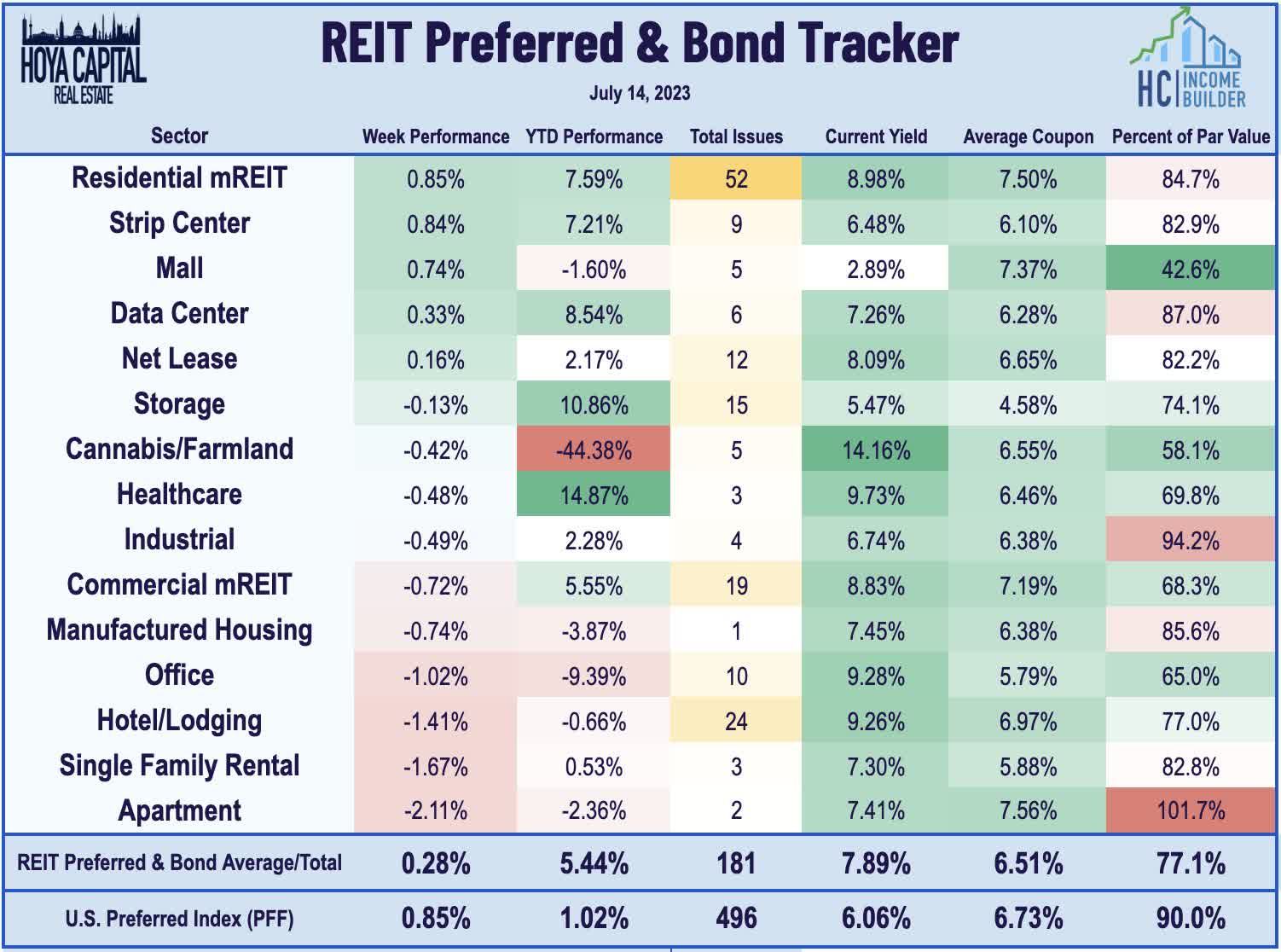

REITs were quiet on the capital-raising front this week following a busy two months of activity. San Francisco-focused office REIT Hudson Pacific ( HPP ) saw its credit ratings downgraded by Moody's this week, which lowered its unsecured debt rating to “Ba1” from “Baa3” with a negative outlook. Fitch Ratings, however, affirmed HPP 's ratings, including its Issuer Default Rating at “BBB-“ and its preferred stock rating at ‘BB” but revised its outlook to Negative from Stable. Fitch Ratings also affirmed the credit ratings of Getty Realty ( GTY ) including its “BBB-“ Long-Term Issuer Default Rating with a stable outlook. Led by strength from residential mREIT preferreds, the REIT Preferred & Bond Index finished higher by 0.3% on the week, slightly lagging the 0.9% gain from the iShares Preferred and Income Securities ETF ( PFF ).

{kind=link}

Hoya Capital

2023 Performance Recap & 2022 Review

Through the first half plus two weeks of 2023, the Equity REIT Index is now higher by 4.4% on a price return basis for the year (+8.8% on a total return basis), while the Mortgage REIT Index is higher by 5.3% (+11.0% on a total return basis). This compares with the 17.5% gain on the S&P 500 and the 10.2% advance for the S&P Mid-Cap 400 . Within the real estate sector, 11-of-18 property sectors are in positive territory on the year, led by Data Center, Single-Family Rental, Apartment, Industrial, and Timber REITs, while Office and Cell Tower REITs have lagged on the downside. At 3.82%, the 10-Year Treasury Yield has declined by 6 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% - but still below its late-2022 closing highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 2.29% this year. Crude Oil - perhaps the most important inflation input - is lower by 4% on the year and roughly 35% below its 2022 peak.

{kind=link}

Hoya Capital

Economic Calendar In The Week Ahead

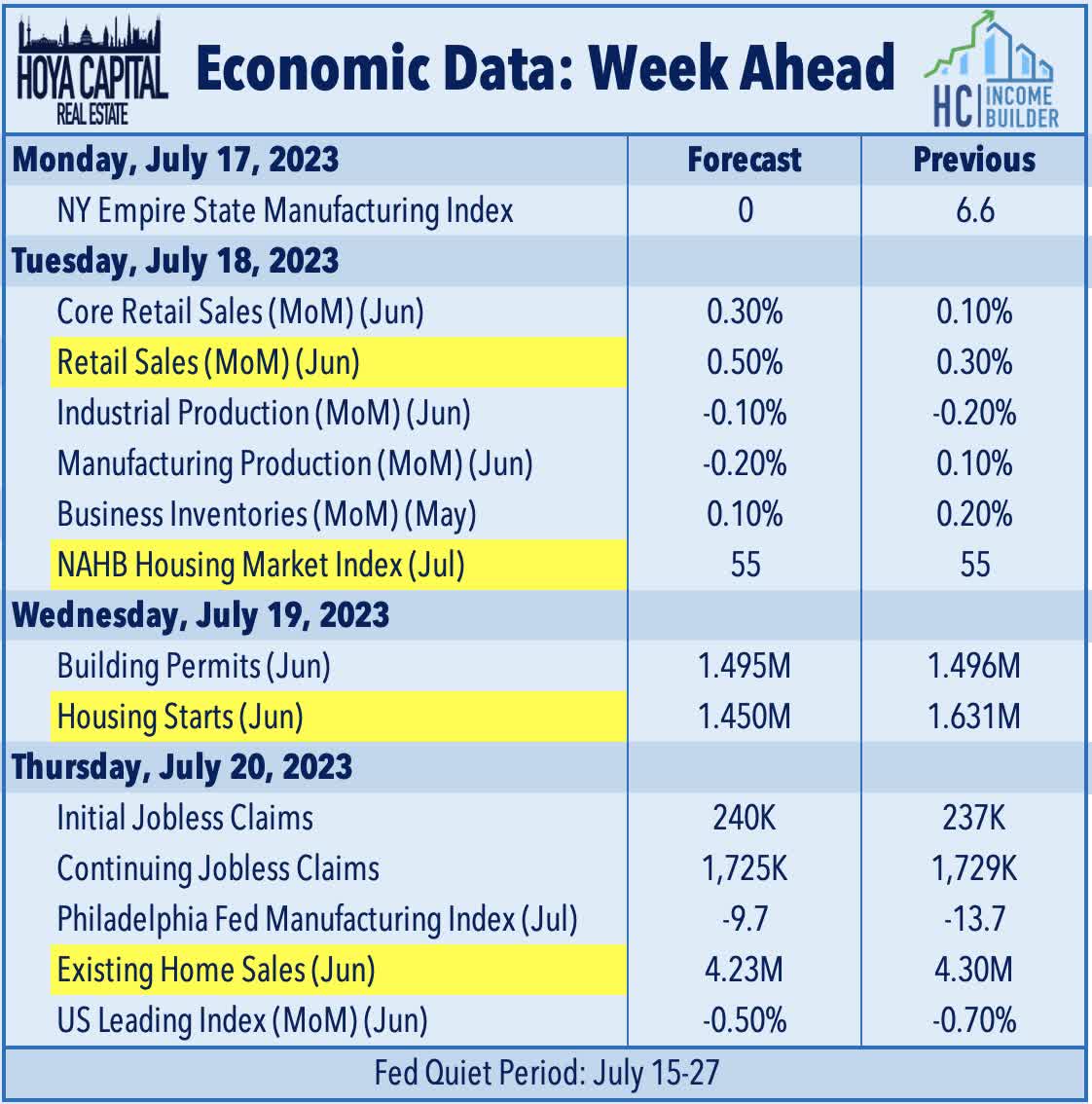

The state of the U.S. housing market will be in focus in the week ahead. The busy week starts on Tuesday with the NAHB Homebuilder Sentiment data for July, which looks to extend its streak of six-straight monthly increases after dipping to near-15-year lows late last year. On Wednesday, we'll see Housing Starts and Building Permits data for June, which are expected to moderate after a stronger-than-expected May. We'll see Existing Home Sales data on Thursday which is expected to decline slightly in May to a 4.23 million seasonally-adjusted annualized rate - up from the lows in January of 4.0 million but well below the 2021 highs of over 6.5 million. We'll also see Retail Sales on Tuesday, which is expected to post modest gains for a third-straight month, which follows a stretch of four-of-five monthly declines. We'll also be watching weekly Jobless Claims data on Thursday.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

Stick The Soft Landing