EVC - Still Avoiding Entravision

2023-03-20 18:06:17 ET

Summary

- The company has just released financials, and they're not great in my view. Though revenue has risen, net income is down. That's never a good combination in my view.

- 97% of the company's debt is coming due next year, and there's a significant probability that the "high" interest expense will become "very high."

- Buying these shares doesn't make sense in my view in light of the fact that you can earn 200 basis points more on a risk-free Treasury.

It's been a little over four months since I walked away from Entravision Communications Corporation ( EVC ), and in that time the shares have returned about 1.5% against a loss of about 1% for the S&P 500. I thought I'd check on the company again, because I've obviously owned it previously, and did well on both the stock and on short puts. Since the company has just reported earnings, I'll review those, and I'll compare them to the valuation.

When I worked on Bay Street many years ago (Bay Street is Canada's deeply insecure baby brother to Wall Street), I asked one of my "greybeard" colleagues the following question: "at what stage in your life should you start to think about capital preservation?" The auld fella shrugged his shoulders as he frequently did, turned to me and said, "that's a good question, Irish, and here's my answer: you should start worrying about capital preservation when you start to breathe." I forget the man's name (Hersh? Shlomo?) but I remember the wisdom he imparted, and I'm reminded of it when I consider Entravision. I think investors would be wise to continue to eschew these shares for a few reasons. First, I don't like the disconnect between revenue and net income. If you increase sales, net income should be taken along for the ride, and that's not happening here. Second, the company will be rolling 97% of its debt next year, and, as you may have noticed, interest rates are relatively elevated at the moment. Interest expenses currently represent 43% of net income, and so an uptick in this expense would be troublesome in my view. Finally, the dividend yield is currently about 200 basis points lower than the rate an investor could earn on a risk-free Treasury Bill. Given all of the above, I would recommend avoiding these shares.

Financial Snapshot

The company has increased revenue fairly massively over the past year. Specifically, revenue is up by $196 million, or 26% from the year-ago period. Unfortunately, that's where the good news ends on that front. Net income cratered while revenue was rising. Specifically, net income is down about $11.1 million, or 38% from the year-ago period. The primary culprits are not "one-offs" unfortunately. For example, the cost of revenue, SG&A, and corporate expenses increased by 33.75%, 32.8%, and 50%, respectively. Collectively, these three increased by $192.3 million, which nearly matches the uptick in revenue. This adds to my concern that this company is not "scalable."

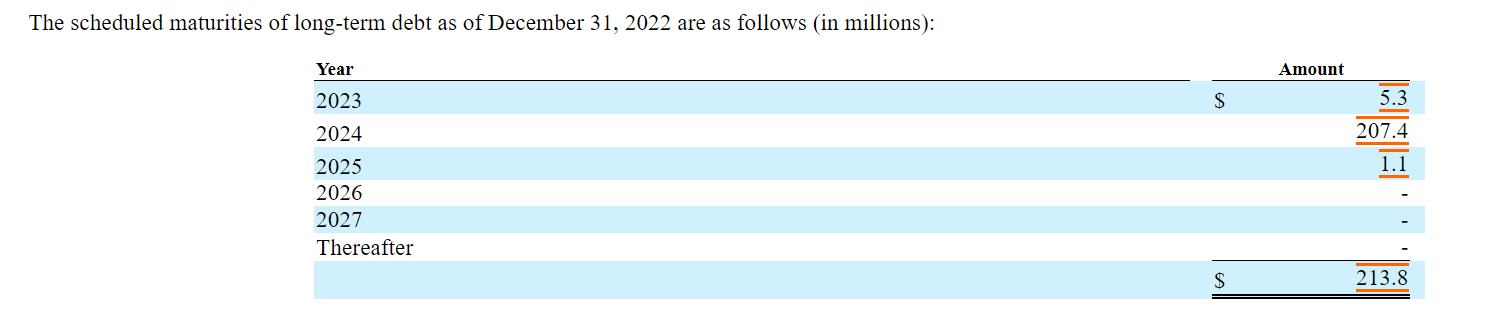

Additionally, I have some concerns about the capital structure. While the level of indebtedness has only picked up by about $230k, or 0.11%, I'm concerned about the timing here. According to the following table, plucked from page F-36 of the latest 10-K for your enjoyment and edification, the company will be rolling the vast majority of its debt next year. You may have noticed that interest rates have risen dramatically recently, and 97% of the company's debt is coming due next year. It's highly likely that the firm will end up paying higher rates unless interest rates drop massively from current levels. That may happen, but the risk that rates remain elevated adds to the risk in this stock.

Entravision Debt Repayment Schedule (Entravision 2022 10-K)

{kind=link}

I feel a need to drive this point home further, so I'm going to drive this point home further. In 2017 the company entered into a credit facility agreement at a rate of 7.13%. That was in 2017 when rates were far lower. If the company rolls next year, I don't think it's a stretch to imagine a new rate between 11%-13% on this debt. We saw that interest expenses rose by $1.237 million, or 18.26% to $8 million. Given where rates are now, and given the repayment schedule above, it's conceivable that interest expenses could jump to $12 to $14 million. This would obviously impact earnings, and not in a good way. Given all of this, I'd be willing to buy back in, but only at a very reasonable discount.

Entravision Financials (Entravision investor relations)

The Stock

I understand that words like "reasonable discount" can be troublesome, because they may cost you future profits. After all, I've talked myself out of some profitable trades with words like "if the price is reasonable", or "at the right price", and so on. The thing is that I'm of the view that it's better to miss out on some gains than lose capital. My regulars also know that I consider the "business" and the "stock" to be quite different things. Every business buys a number of inputs and turns them into a final product or service, like "advertising solutions." The stock, on the other hand, is an ownership stake in the business that gets traded around in a market that aggregates the crowd's rapidly changing views about the future health of the business, future demand for Entravision's media services, future margins, and so on. The stock also moves around because it gets taken along for the ride when the crowd changes its views about "the market" in general. Most strange of all to me is that the market seems to be affected by the subtle pronouncements of a government-appointed bureaucrat at the Federal Reserve. Anyway, my view is that the stock is affected by a host of variables that may be only peripherally related to the health of the business, and that can be frustrating.

This stock price volatility driven by all these factors is troublesome, but it's a potential source of profit because these price movements have the potential to create a disconnect between market expectations and subsequent reality. I don't want to be too repetitive, but in my view, this is the only way to generate profits trading stocks: By determining the crowd's expectations about a given company's performance, spotting discrepancies between those assumptions and stock price, and placing a trade accordingly. I've also found it's the case that investors do better/less badly when they buy shares that are relatively cheap, because cheap shares correlate with low expectations. Cheap shares are insulated from the buffeting that more expensive shares are hit by, and this is why I try to buy shares when I believe they are cheap.

As my regulars know, I measure the relative cheapness of a stock in a few ways, ranging from the simple to the more complex. For example, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. I like to see a company trading at a discount to both the overall market, and to its own history. In case you forgot, when I last reviewed the shares, they were trading at a price to free cash flow of 4.714 times, the market was paying about $0.55 cents for $1 of sales, and the dividend yield was about 1.78%. Fast-forward and the shares are about 50% more expensive on a price to free cash basis, though the market is paying about 9.5% less for $1 of sales. Additionally, the dividend yield has spiked higher by 29% to 2.3% per the following:

Given that everything in the world of investing is relative, I think it's worth noting that the current dividend yield is about 200 basis points below the risk-free rate . So, an investor would be taking on (substantial) business risk here, and receiving just over ½ the return they could generate risk-free.

As my regulars also know, in order to validate (or refute) the idea that the shares aren't objectively cheap, I want to try to understand what the crowd is currently "assuming" about the future of a given company. If the crowd is assuming great things from the company, that's a sign that the shares are generally expensive. If you read my articles regularly, you know that I rely on the work of Professor Stephen Penman and his book "Accounting for Value" for this. In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is "thinking" about a given company's future growth. This involves isolating the "g" (growth) variable in this formula. In case you find Penman's writing a bit dense, you might want to try "Expectations Investing" by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently "expecting" about the future.

Anyway, applying this approach to Entravision at the moment suggests the market is assuming that this company will not grow profits from current levels. While I consider this to be a nicely pessimistic forecast, I can't get past the reality that investors are receiving less cash on their capital than they would on a risk-free investment. Since I'm at a stage in life where capital preservation is far more important, I'm going to continue to eschew these shares, and recommend others do the same.

For further details see:

Still Avoiding Entravision