RUSHB - Still Optimistic About U-Haul As We Move Into Earnings

2023-11-04 09:00:14 ET

Summary

- Things have not been going all that great for U-Haul, thanks to weakening demand for some of its services.

- Even so, the firm looks cheap enough to warrant optimism.

- Management is also doing well to continue to grow the company's self-storage operations, which will add value in the long run.

- While shares are cheap enough now, investors should be watchful over earnings that come out in the coming days.

In an ideal world, stocks that we buy would only ever go up in value. But that's not how the world works. Unfortunately, shares of companies can outperform the broader market for an extended period of time, only to then pull back significantly and erase some or all of those gains. A really good example of this of firms that I have been bullish of involves U-Haul Holding Company ( UHAL ) ( UHAL.B ), previously known as Amerco. Almost a year ago, in late November of 2022, I revisited the company , ultimately concluding that it still made for an attractive opportunity because of how cheap shares were and how robust financial performance had been. Since the publication of that article, however, shares have seen downside of 17% while the S&P 500 has jumped 5.3%.

This marks a stark turnaround from how things had been going. To put this in perspective, since first rating the company a 'buy' in February of that year, shares are down 5.7% while the S&P 500 is down almost as much at 5.2%. This means that, up until very recently, my bullish call on the company was performing as expected. So the big question is what went wrong. Digging into the numbers, we see that a modest decline in revenue has recently developed. But the bigger issue is that profits have pulled back rather materially. The good news for investors is that while this pain is real, shares still look cheap on both an absolute basis and relative to similar firms. In the near term, I wouldn't be surprised to see additional volatility be an issue. But for those focused truly on the long haul (pun intended), I would argue that U-Haul Holding Company should still end up being an attractive opportunity.

Assessing recent pain

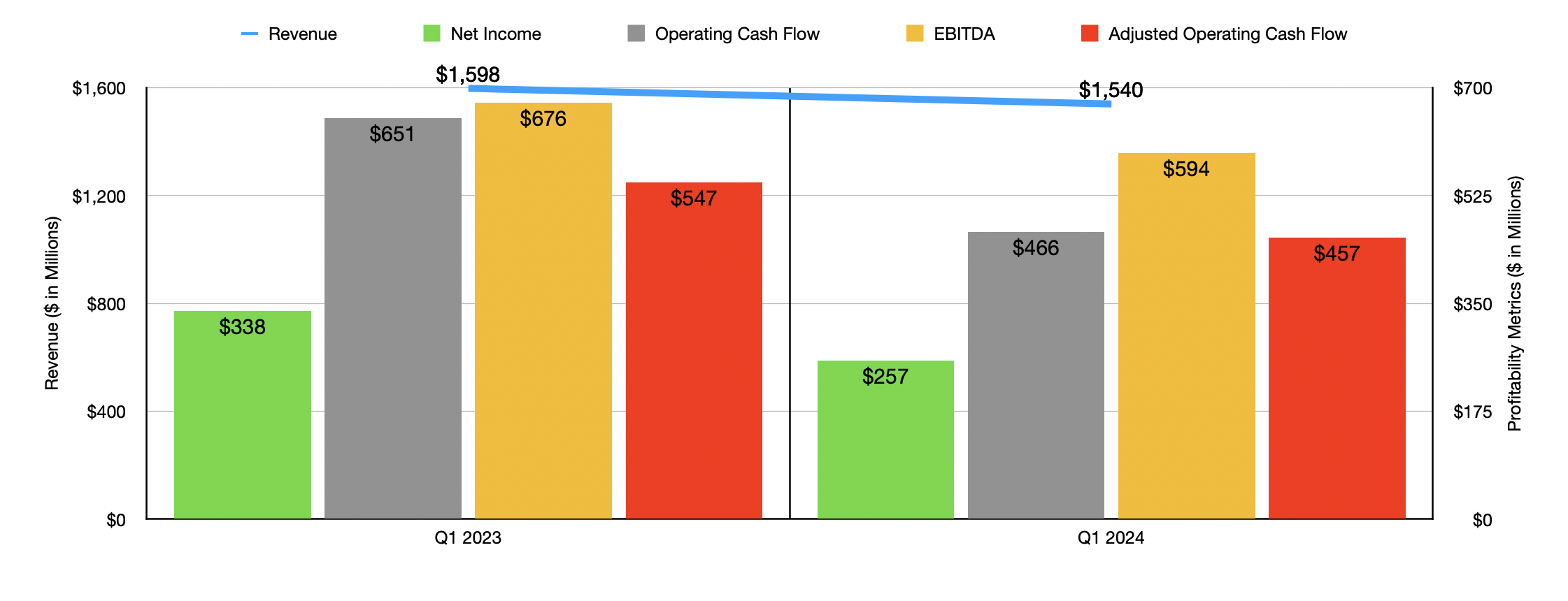

As I mentioned already, recent financial performance achieved by U-Haul Holding Company has not been great. Consider the performance of the company during the first quarter of its 2024 fiscal year . According to management, revenue came in at $1.54 billion. This represents a decline of 3.6% compared to the nearly $1.60 billion generated one year earlier. As you can see in the image below, almost every part of the company saw revenue worsen year over year. The biggest issue was the revenue associated with the self-moving equipment rentals that the company makes available. Revenue here fell from $1.09 billion to $999.2 million. That decrease, according to management, was really the result of a reduction in demand for this type of equipment, particularly in one-way markets.

{kind=link}

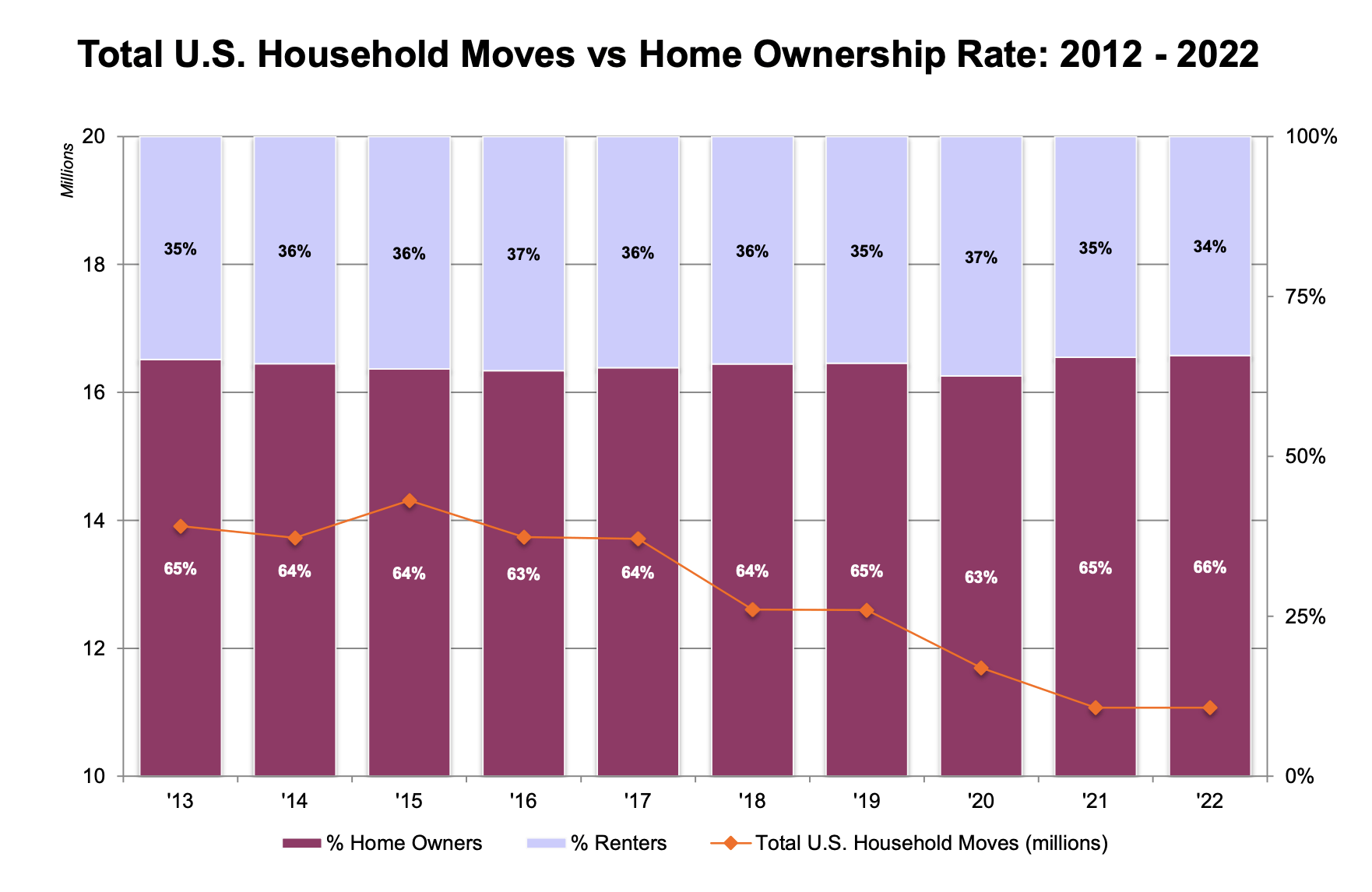

Management has not really provided much in the way of detail as to why this is. But I do know that a lot of the self-moving equipment can be used when people move from one home to another. In September of this year, it was estimated that nationwide existing home sales were down 15.4% compared to the same time last year. The 'one-way' statement made by management likely is referencing this space. Although management did not say anything specifically in their filings, they did, in an investor presentation, show a reduction in total US household moves but that really began in 2018 and continued through at least 2022. So I would argue that this interpretation is almost certainly accurate.

{kind=link}

This is not to say that there weren't any bright spots for the company. Self-storage revenue, for instance, came in at $199 million for the quarter. That's up significantly from the $173.2 million generated one year earlier. I know that management has been investing heavily in this market segment. In fact, the total unit count for the business grew from 620,000 at the end of the first quarter of 2023 to 683,000 by the end of the first quarter of 2022. The occupancy rate at these locations has dropped some. But the overall number of units occupied jumped from 518,000 to 563,000. Another growth spot for the company involved net interest and investment income. That nearly doubled from $33.6 million to $64.6 million. But at the end of the day, this is not really an operational thing period rather, it's because the company is benefiting from higher interest rates on short term deposits and from good investments being made by the company.

This decline in revenue brought with it a drop in profits as well. Net income fell from $338 million to $257 million. The drop in sales was part of the problem period but there were other issues as well. For instance, operating expenses for the company increased from $733.2 million to $763.2 million. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, fell from $651 million to $466 million. Even if we adjust for changes in working capital, we get a drop from $547 million to $457 million. And finally, EBITDA for the company dropped from $676 million to $594 million.

{kind=link}

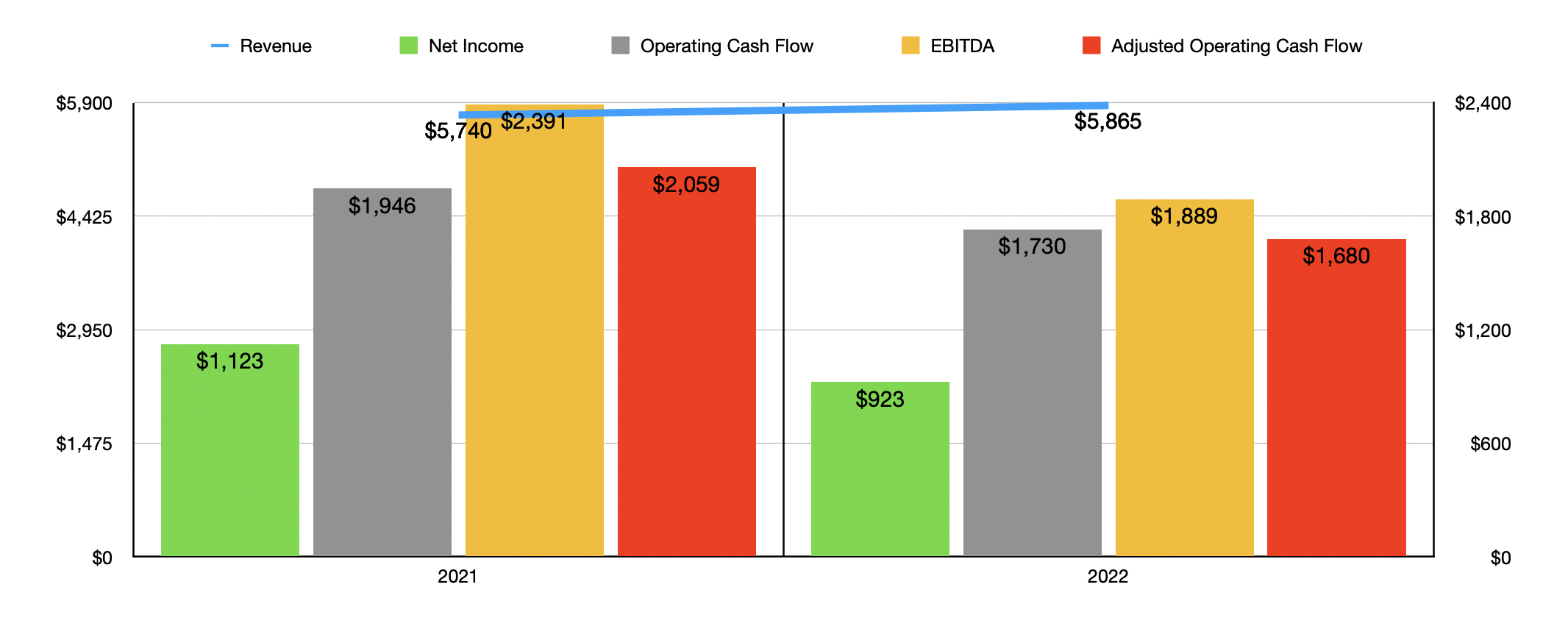

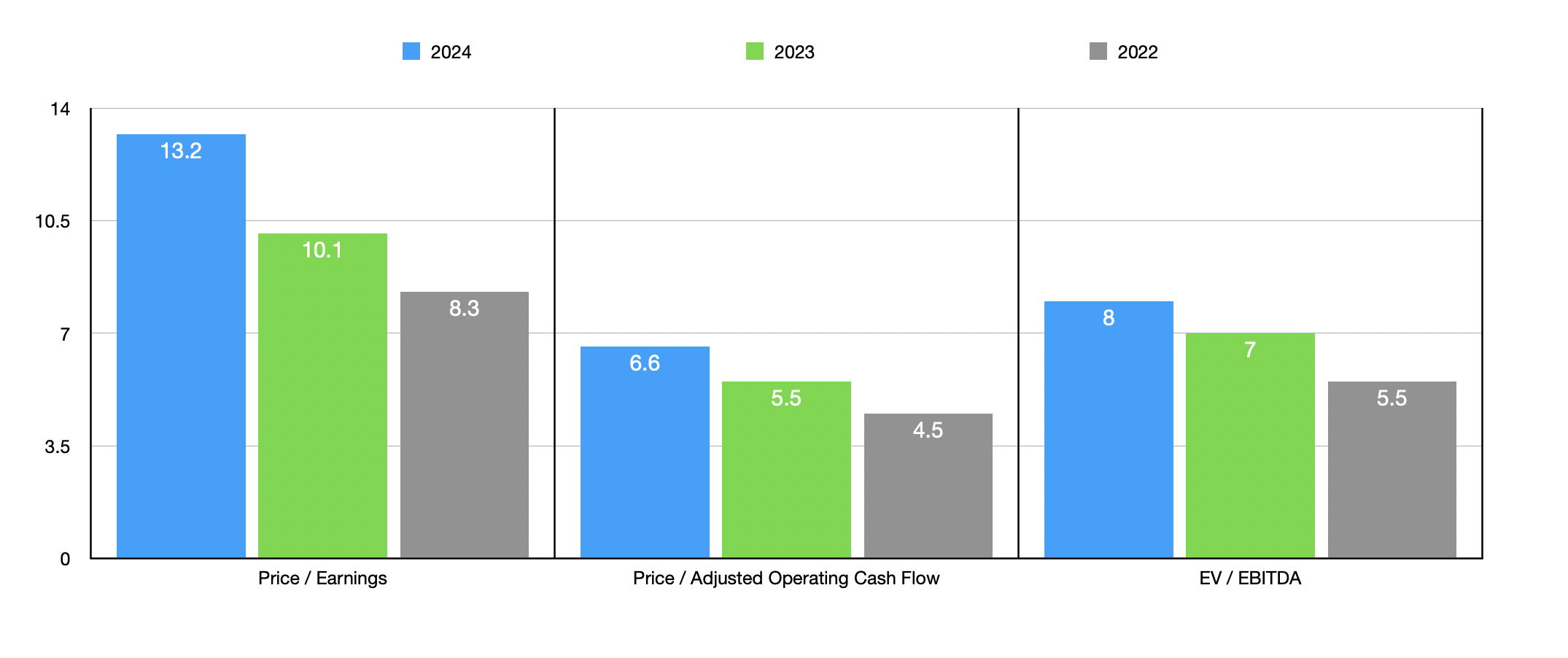

For context, you can see financial data covering both 2022 and 2023 shown in the chart above. It is still far too early to take terribly serious results seen so far when it comes to what impact they might have on this year as a whole. But if we were to annualize results from the first quarter, we would expect net income of $702 million, adjusted operating cash flow of $1.40 billion, and EBITDA of $1.66 billion. Using these figures, I then valued the company as shown in the chart below. Even though the stock does look a bit more expensive on a forward basis relative to both 2022 and 2023, I would argue that shares are still cheap on an absolute basis. In the table below that, you can see the company stacked up against three similar firms. While it is the most expensive when it comes to the price to earnings approach, I found out that only one of the three enterprises I looked at were cheaper than it when it comes to the other two profitability metrics.

{kind=link}

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| U-Haul Holding Company |

| 10.1 |

| 5.5 |

| 7.0 |

| Penske Automotive Group ( PAG ) |

| 8.5 |

| 7.6 |

| 10.7 |

| Hertz Global ( HTZ ) |

| 3.7 |

| 1.2 |

| 14.7 |

| Rush Enterprises ( RUSHA ) |

| 8.2 |

| 9.2 |

| 6.0 |

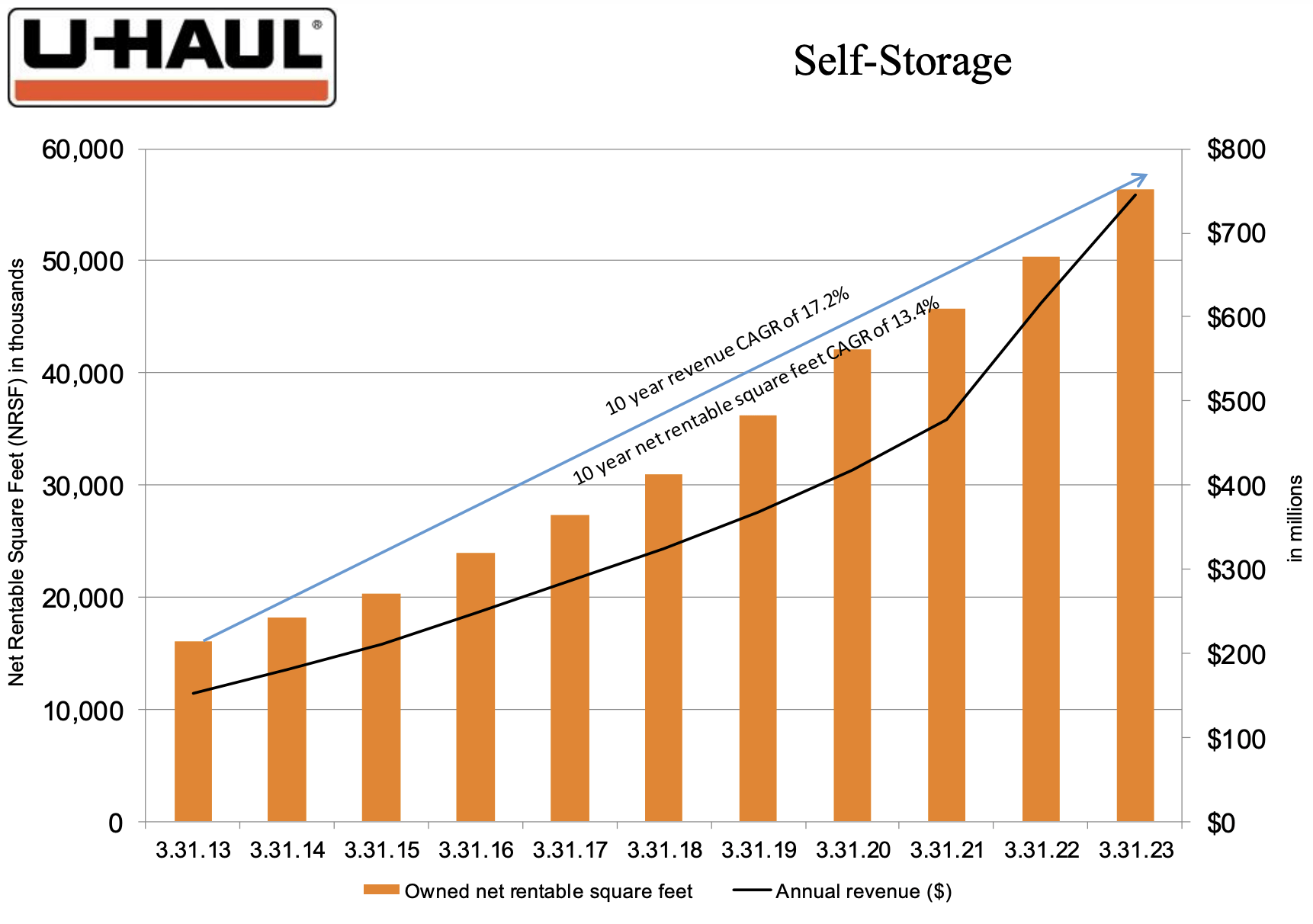

In the near term, we could see some additional pain. But it is important to focus more on the long run. Although the self-storage side of the business is still relatively small compared to the rest of the firm, management has made clear just how dedicated they are to continue building out these operations. As you can see in the image below, management has grown its owned net rentable square footage by 13.4% per annum over the last ten years while growing its revenue at a rate of 17.2% per annum during that same window of time. This increase in growth has been made possible by both acquisitions that the company has engaged in over the years and by organic growth.

{kind=link}

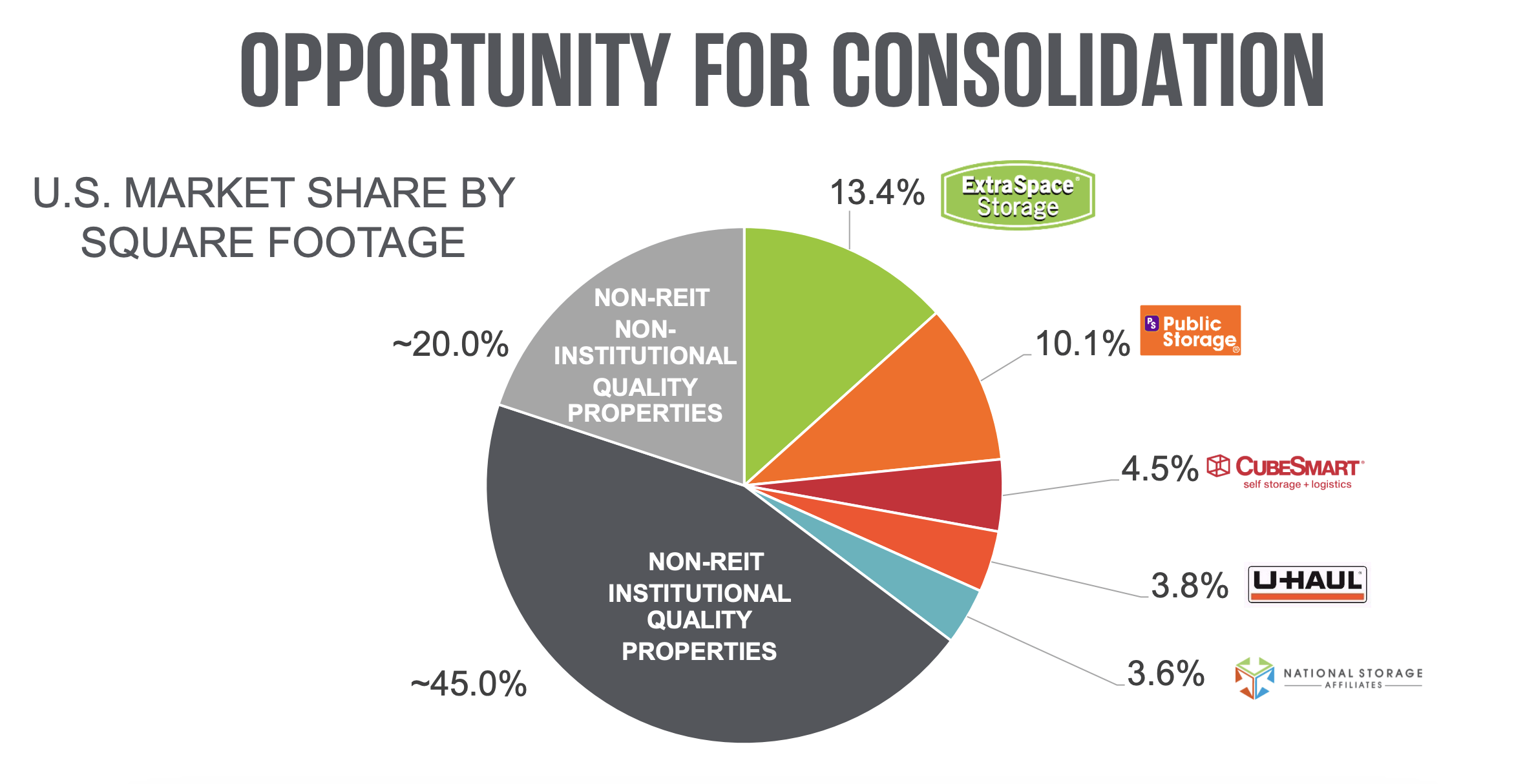

According to rival in this space, Extra Space Storage ( EXR ), this is a massive market in which U-Haul Holding Company only has a roughly 3.8% stake. And that is only focused on the US. It's also a market that is known for its stability and steady growth over time. This is particularly interesting because it should help to offset the more volatile equipment leasing operations and other activities that U-Haul Holding Company engages in.

{kind=link}

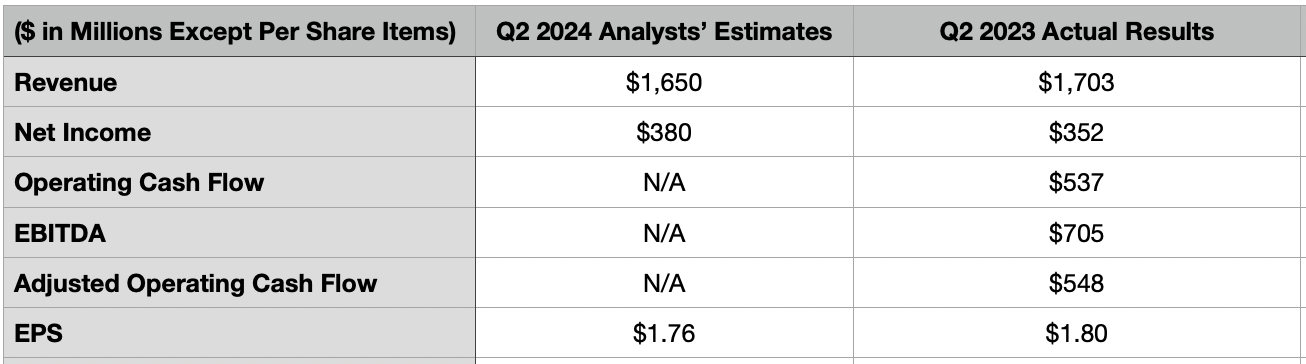

Investors should always be prepared for conditions changing. That is especially true in the current uncertain economic environment. That's why shareholders would be wise to pay attention to when management reports financial results later this month. That is expected to occur on November 8th, after the market closes. At present, analysts are forecasting revenue of $1.65 billion. That would represent a decline of 3.1% over the $1.70 billion generated the same time last year. The current expectation for earnings per share for the second quarter of the 2024 fiscal year is $1.76. That would be down slightly from the $1.80 per share reported the same time last year. But even so, given the change in share count of the company, it should result in net profits climbing from $352 million to $380 million. Analysts have not offered guidance when it comes to other profitability metrics. But in the chart below, you can see what some important ones are that should be the primary focus of investors once the data comes out.

{kind=link}

Takeaway

Based on the data provided, it seems to me as though U-Haul Holding Company is facing a bit of pain. But investors need to understand that this is likely short term in nature. At some point, we will see a recovery. It would be different if shares of the enterprise were expensive because investors were banking on attractive growth. But that couldn't be further from the truth. Shares are cheap on both an absolute basis and relative to similar enterprises. When you add on to this continued growth in the self-storage space, I see no reason to be anything other than optimistic. As such, I have decided to keep the company rated a 'buy' for now.

For further details see:

Still Optimistic About U-Haul As We Move Into Earnings