STIP - STIP: Real Yields Can Only Grow

2023-10-15 05:55:39 ET

Summary

- CPI figures are high, meaning the desperate need for real yields to grow continues.

- STIP provides a hedged exposure to inflation risk as coupons scale with inflation. However, the downside is to growth in real yields, where the nominal rate-inflation gap grows.

- The Fed will continue to raise rates to lower inflation, or at the very least allow real yields to rise by keeping nominal rates high, to tackle inflation.

- STIP duration isn't too long, so the downside isn't that extreme, but the direction isn't terribly positive.

CPI figures are stubbornly high, and that means that per the Fed mandate, real yields will have to grow in order to achieve the objective of lower inflation rate. TIPS instruments see their face value grow according to inflation, and therefore are hedged to inflation effects. What effects their price are changes in real yields, i.e. the difference between nominal rates and inflation rates. The iShares 0-5 Year TIPS Bond ETF ( STIP ) has been performing worse in the last 12 months on account of that - while high inflation initially raised face values, the consequent rate hikes started driving up real yields and devaluing the inflation hedged coupons provided by STIP. We believe that real yields will continue to rise and STIP will suffer on account of that.

STIP Breakdown

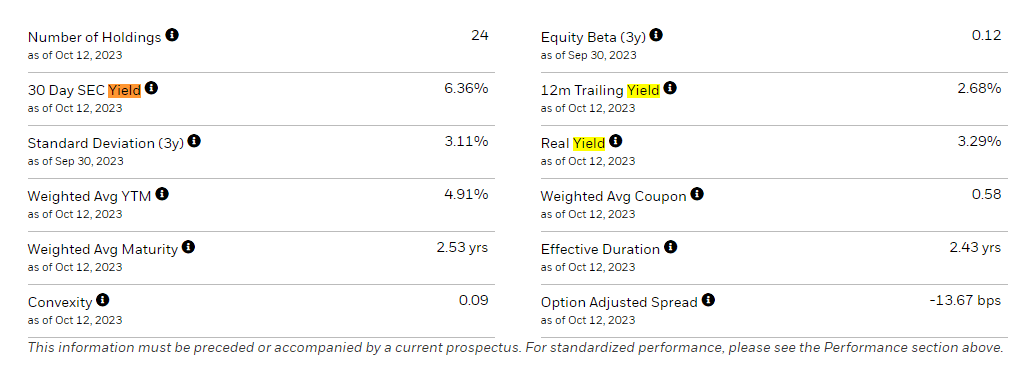

Expense ratios are low at 0.03% , and STIP gives a neat exposure that is hedged against the technical inflation risk, providing to maturity a constant and unerodable real yield from coupon rates applied on an inflation adjusted face value. Effective duration is 2.46 years, which is not high.

There is no credit risk (depending on who you ask), as this is the Treasury we are talking about.

{kind=link}

Comments

CPI comes in at pretty high rates. Oil keeps the headline rates quite high, and core rates are remaining at pretty high levels around 4.1% . The CPI report is a big of a lagging indicator, and markets are more concerned with employment data since that leads inflation outcome from the labour market , which is an important mechanism that persists inflation in the economy. The labour force continued growing, the opposite of what markets wanted to see as it means that inflation won't come down naturally, could persist dangerously, and that interest rate hikes so far haven't had their hoped-for effects which may mean there needs to be more. Equity markets have had to revise down on the basis of the new data.

Some things in particular are the advances that are coming in still from shelter prices. Declines in housing prices were hoped to trigger a shift from rent to own, which might have released pressure on rents. Instead, they are continuing to create inflation pressure, likely reflected by overall limits of supply in housing in the US.

For STIP the implications are clear. Inflation is not on the rise, but the worst case scenario for the economy, and the best case scenario for STIP, is that inflation will persist at the current levels. However, the Fed cannot allow that, and will continue to either keep nominal rates high or raise them further until higher real rates start impacting consumption such that inflation comes down. That will also impact the PV of future cash flows, where the effects of nominal discount rate increases are hedged in the numerator by coupon growth, but where the real component can levy value from TIPS.

Assuming consumers are quite sophisticated, a necessary condition for lower consumption, to the extent that consumption is really affected by rates, requires that the rate effect be real and not just nominal. That is also the condition for lower TIPS prices.

While STIP is a great TIPS ETF, with very low expense rates, we feel that for TIPS upside one would need to believe that the Fed won't deliver on its promises. Meanwhile, it seems obsessed with being credible, as it should be since its ability to affect expectations is so important to being able to carry out its mandate, and therefore it is necessary and inevitable for real yields to come up.

While STIP was an excellent pick when inflation figures were exceptionally high and rates were still coming up, we believe the direction is down for a while longer since the inflection point was reached.

For further details see:

STIP: Real Yields Can Only Grow