SFIX - Stitch Fix Continues To Lose Customers But Profitability Is Hanging On

2024-01-15 23:31:02 ET

Summary

- Stitch Fix has seen a decline in customers and revenue over the past two years, leading to a sharp loss in value.

- The company has made improvements to profitability, with gross margins rising and operating expenses declining.

- Cash represents a large portion of its market value, and SFIX's valuation on an adjusted EBITDA basis looks cheap.

- The Company still needs to stabilize its top line and faces competition from fast-casual brands. I'd watch and wait here.

We are now well past the pandemic era, which blessed a number of companies with a temporary recovery that we are now finding was unable to be sustained for long. Stitch Fix ( SFIX ) is one such example: the fashion e-commerce company has seen sharp bleeding of customers and revenue over the past two years as its once-innovative business model has largely been deemed irrelevant.

Over the past year, Stitch Fix has lost nearly 30% of its value; since the start of January alone, it has lost ~9%. The question for investors now is: is there more downside, or does Stitch Fix have room to rise?

I last wrote a neutral opinion on Stitch Fix in October when the stock was trading in the slightly lower $3 range. Though I acknowledged the company's poor fundamentals, I also noted that Stitch Fix traded at an incredibly low valuation not too far off from its book value: as the majority of Stitch Fix's market cap actually sits in cash, indicating the market's consensus view that Stitch Fix will eventually burn through these resources.

To be clear: I am quite far from becoming bullish on Stitch Fix. I remain neutral on this stock, but I am encouraged by several positive signals in the company's latest Q1 earnings print (released last month). In particular, we've continued to see Stitch Fix make improvements to profitability: with gross margins rising after the company's decision to exit its unprofitable UK arm, and opex continuing to decline as a percentage of revenue as Stitch Fix makes necessary cuts to its headcount. Overall, the company has paved a path to profitability as a much smaller company than it was in the past.

Still, it's too soon to proclaim a victory for Stitch Fix until it can stabilize its top line. Each quarter it continues to lose customers, and the customers it has aren't spending more either (net revenue per active customer is also waning). I also continue to worry about Stitch Fix now colliding with fast-casual brands such as H&M and Zara - now that it is predominantly a direct-buy model for simple closet staples, without the innovative twist of a stylist-curated "Fix," I'm not sure what defensive moat Stitch Fix has against these much larger brands.

All in all, this is still a "watch and wait" play: but the company's improvements in profitability, plus its high cash balances relative to its market cap, bear watching.

Q1 download

Let's now go through some of the key themes that resonated throughout Stitch Fix's first fiscal quarter. The top-line results are shown in the summary below:

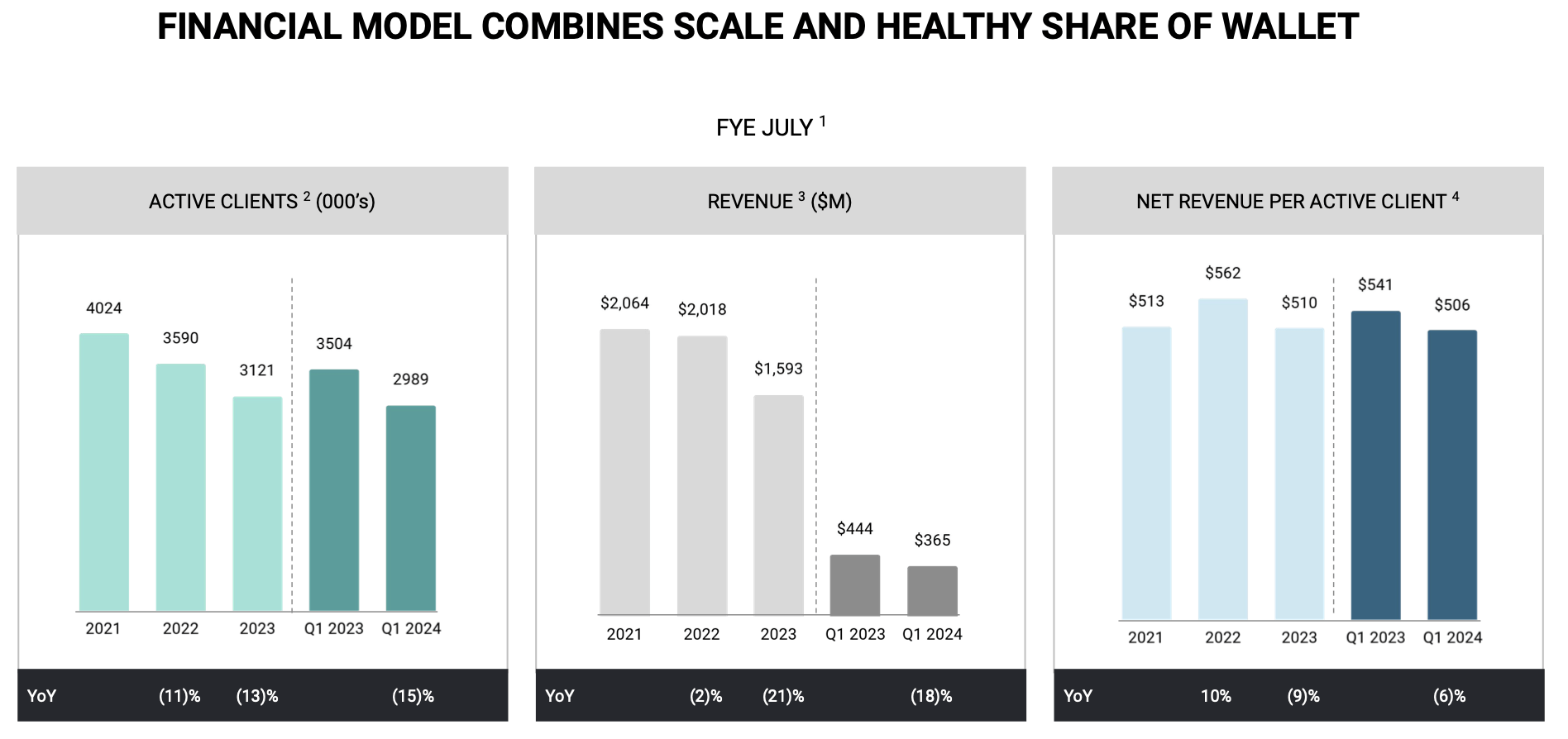

Stitch Fix Q1 revenue and client stats (Stitch Fix Q1 earnings deck)

{kind=link}

Stitch Fix's revenue continued its downward glide path, down -18% y/y to $365 million - though ahead of the company's guidance range, and beating Wall Street's expectations of $363 million (-19% y/y) by a one-point margin.

Continued client defections are the core red flag to focus on. Active clients (which the company defines as a customer who made any purchase in the trailing twelve months) fell to 2.99 million, which represented a 132k sequential decline from Q4. The company is having a difficult time encouraging repeat buys, especially with its focus on the direct-buy (standard retail) format.

Here is useful anecdotal commentary from CEO Matt Baer's remarks on the Q1 earnings call, detailing the company's plan to re-stimulate customer growth:

First, we are strengthening our foundation in embedding retail best practices throughout the organization. Second, we are building a healthier client base by more precisely targeting high lifetime value clients that we expect will help us expand our client base over time. And third, we are developing a long-term strategy to better serve the clients we have today and those we intend to attract in the future [...]

We saw encouraging results in Q1 as we continue to strengthen our foundation and apply those retail best practices across a number of functions. Let me share a few examples. In merchandising, we began to establish best-in-class buying, assortment planning, and inventory allocation strategies, and we increased our focus on private brands. We expect it to improve operational efficiencies, grow margin, and ensure we have the right product in the right location at the right time to best serve our clients.

Our private brands play an outsized role in improving both client outcomes and profitability. Over the last few years, we have increased our private brands from approximately one-third to nearly 50% of total sales. Because these brands perform well, generating higher keep rates and margins, we plan to emphasize them in our assortments moving forward.

We also continue to refine our brand portfolio in order to better serve our clients, unlock greater operational efficiencies, and build deeper relationships with national brand partners. Over the last two quarters, we've reduced the number of brands, and we will continue to assess brands and optimize categories to deliver newness and trend while also driving growth."

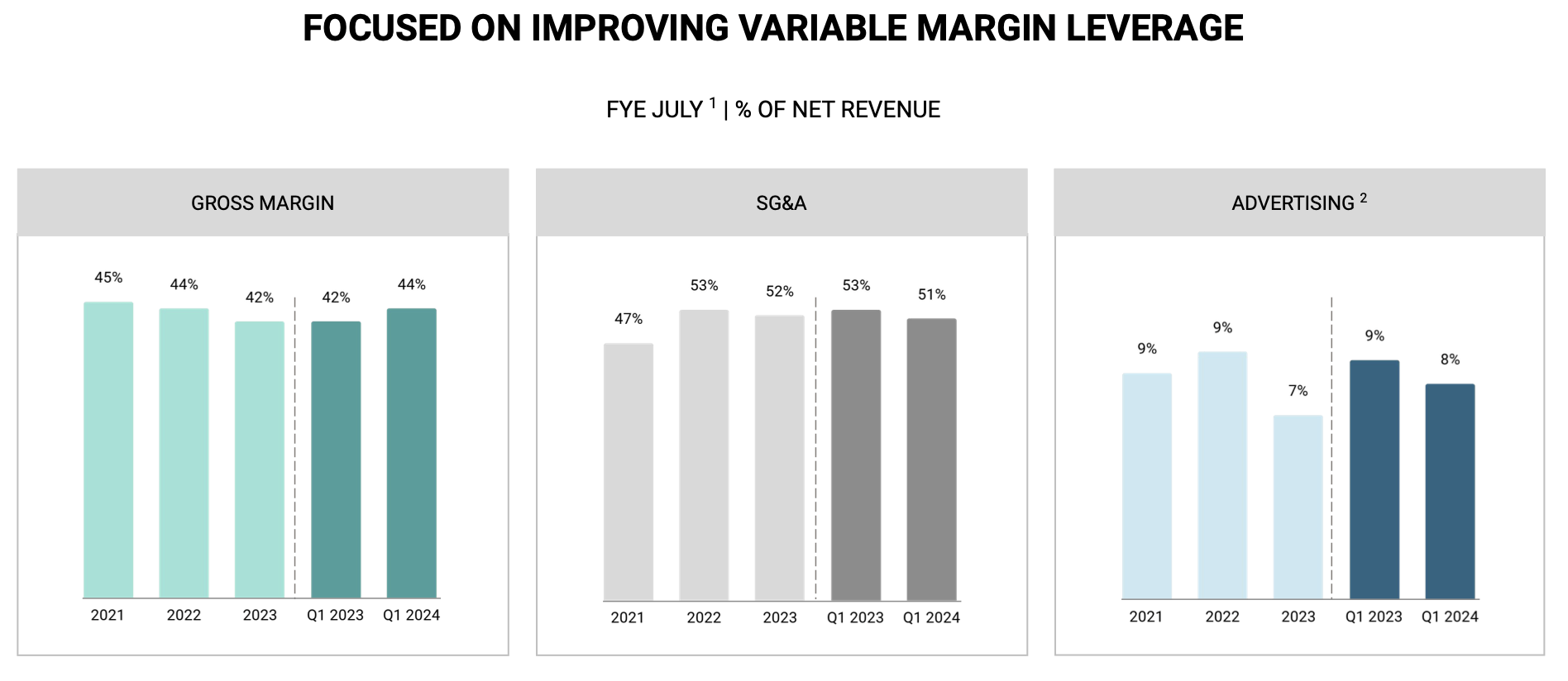

As mentioned above, slimming down the company's brand assortment and winding down obsolete inventory, plus the company's exit from the UK, have thankfully driven a two-point y/y improvement in gross margins to 44%. The company's CFO noted that it expects inventory to sequentially decline from Q1 (which represents the peak holiday period) and to remain at lower y/y levels throughout the remainder of the year.

{kind=link}

In addition to improved gross margins, cost controls have also slimmed down SG&A and advertising costs as a percentage of revenue by two points and one point, respectively. All in all, Stitch Fix has managed to boost adjusted EBITDA margins to 2.4%, a 280bps y/y improvement:

{kind=link}

Valuation and key takeaways

At current share prices of just over $3, Stitch Fix trades at a market cap of $384.3 million. After we net off the $262.3 million of cash and short-term investments on Stitch Fix's most recent balance sheet, the company's resulting enterprise value is $122.0 million.

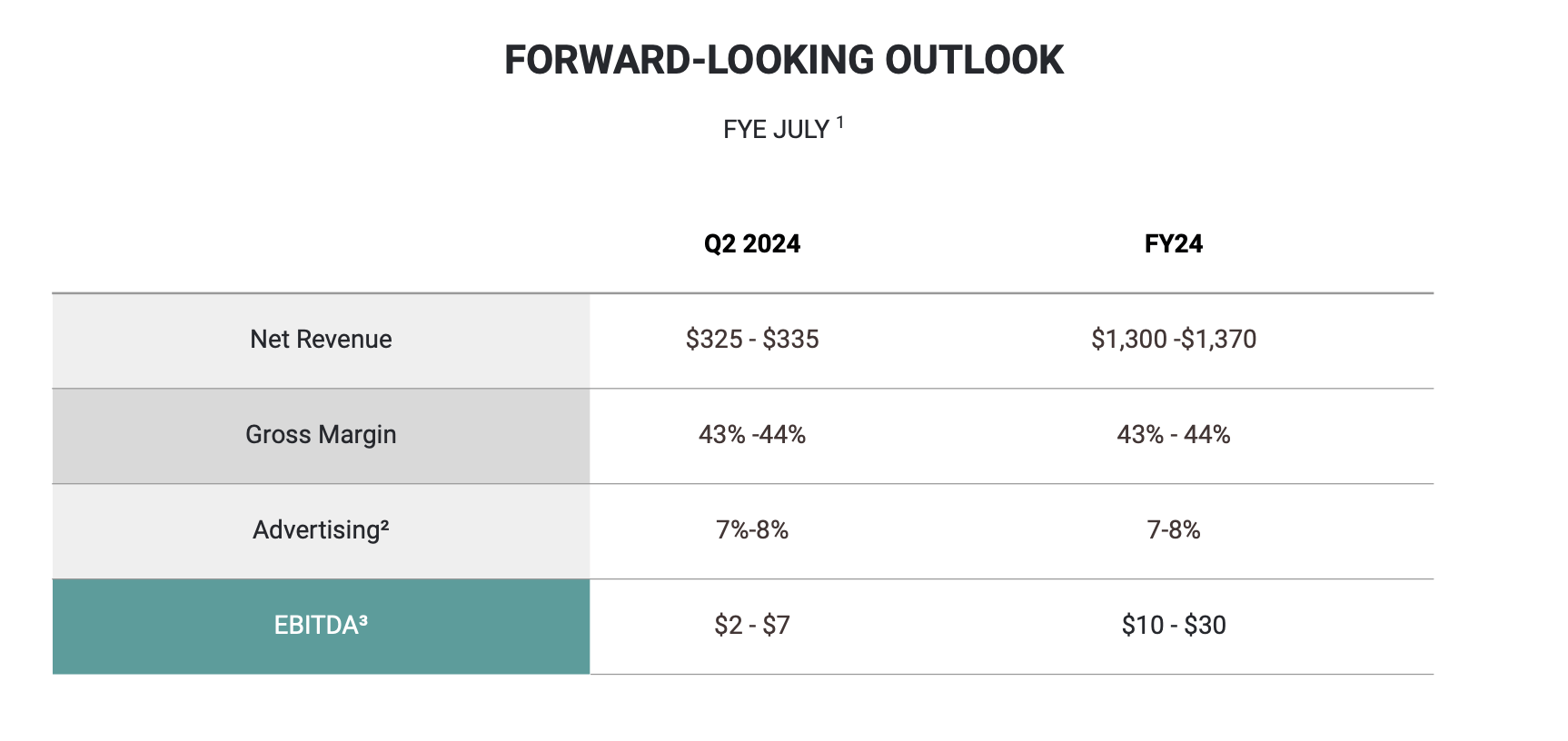

For the current fiscal year, meanwhile, Stitch Fix has guided to $10-$30 million in adjusted EBITDA on a range of $1.30-$1.37 billion in revenue, representing a ~1.5% adjusted EBITDA margin at the midpoint on a ~17% y/y revenue decline.

{kind=link}

Taking the midpoint of this range at face value, Stitch Fix trades at 6.1x EV/FY24 adjusted EBITDA. There's a lot of volatility in the EBITDA figure, needless to say. Faster-than-expected revenue deterioration (i.e., more than a -20% y/y decline) could entirely wipe out Stitch Fix's profits, while top-line stabilization, better-than-expected improvement in logistics and transportation costs, and a higher mix of private-label sales could push Stitch Fix's adjusted EBITDA to the high end or even higher than that.

This isn't a risk I'm inclined to take yet: but I'll continue to monitor this stock.

For further details see:

Stitch Fix Continues To Lose Customers, But Profitability Is Hanging On