QVMS - Stock Market And Economic Outlook For 2023

Summary

- More interest rate increases are likely to slow the economy in 2023 as the Federal Reserve works to lower inflation.

- Earnings are likely to take a hit in 2023 as economic activity slows down.

- I am forecasting a recession for next year.

- I will also forecast where I think the S&P 500 will end up at the end of the year based on valuation and earnings.

There are many dynamics in the current economic and stock market environment. Inflation, interest rate increases, corporate sales/earnings, and geopolitical events are all factors shaping the outlook for 2023. The Federal Reserve has been focused on driving down inflation with a series of interest rate increases. The most recent increase of 0.50 percentage points brought the primary credit rate to 4.5%.

It is my opinion that these interest rate increases haven't been fully reflected in the economy yet. Sure, we have seen mortgage rates increase from record low levels of 2.65% for a 30-year mortgage in January 2021 to the current level of about 6.5% . There have also been mass layoff announcements from Amazon ( AMZN ), Meta Platforms ( META ), Twitter ( TWTR ), Netflix ( NFLX ), Carvana ( CVNA ), Peloton ( PTON ), Goldman Sacs ( GS ), Micron ( MU ), and others. It is likely that higher rates and layoffs will have a snowball effect in the broader economy as demand for goods/services declines as consumers and companies cut back on spending due to higher borrowing costs and with more people out of work.

Interest Rate Outlook for 2023

The Federal Reserve typically has a goal of 2% for the inflation rate over the long-term. The latest inflation rate was 7.1% for November 2022 . While this was lower than the 7.7% rate from October, the level still remains stubbornly high. So, there is still work for the Fed to do to drive down inflation.

The Fed hinted that it will increase its target interest rate to 5.1% in 2023. This implies more increases that amount to 0.75 percentage points. So, the borrowing costs for homes, vehicles, and businesses to expand are likely to become more expensive in 2023. This is likely to reduce demand for large-ticket items and for business expansion. Therefore, corporate sales/earnings are likely to decline and more layoffs are likely to occur in 2023 as a result.

As borrowing becomes more expensive, potential home buyers are more likely to postpone purchasing homes, consumers may hold off on purchasing new vehicles and other big-ticket items, existing home owners probably won't refinance and may postpone large home improvement projects, businesses may halt investments for expansion, etc.

Higher interest rates typically lead to recessions as a part of the normal business cycles. We witnessed that in the financial crisis of 2008, the dot com bubble burst in 2000, and in other recessions. Previous recessions occurred after a series of interest rate increases. It is likely to happen again as economic activity slows down.

Yield Curve Inversion

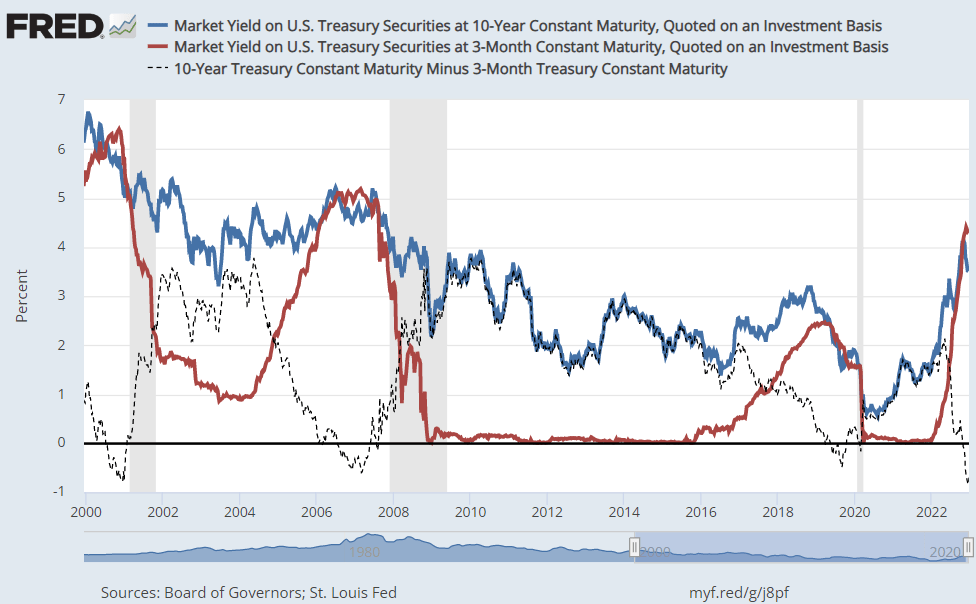

One reliable recession indicator is the relationship between the 3 month and 10-month treasury yields. When the 3-month treasury yield becomes higher than the 10-year treasury yield, the yield curve is said to be inverted. This occurrence predicted the last 10 recessions . The 3-month treasury is currently yielding 4.28% while the 10-year treasury yields 3.75%. Normally, the longer-term treasuries will have higher yields. So, when the opposite occurs, it indicates that economic conditions are changing due to short-term interest rate increases.

{kind=link}

We can see in the chart above that the 3-month treasury yield (red line) rose higher than the 10-year yield (blue line) prior to the last three recessions. It occurred before the COVID-related recession in 2020, prior to the 2008 financial crisis, and during the dot com bubble burst and recession that followed. While there is no guarantee that the current inversion will result in a recession, this indicator has been reliable since the 1980s. So, I do think it does increase the chance of a recession occurring in 2023 significantly.

Corporate Earnings Declines

Analysts have been lowering EPS estimates for the S&P 500 ( SP500 ) ( SPY ) companies for Q4 2022 by a larger margin than average. The EPS estimates were lowered by 5.6% for Q4. The average decline for estimates over the past 5 years has been 2.1%.

These larger estimate declines are likely to continue in 2023 in my opinion. The reason for that is inflation is still high and interest rates are still rising. The cost of most items including food and energy are still high which can reduce demand for other discretionary goods/services in the economy. Many consumers may have to put most of their money into food, shelter, and commuting costs and limit spending on travel, entertainment, dining out, and other discretionary goods/services.

Higher borrowing costs are likely to reduce demand for mortgages and home purchases. This can lead to less demand for other large-ticket items such as appliances, furniture, and large home improvement projects. Higher borrowing costs can also reduce demand for new vehicles.

With all of this in mind, many companies are likely to see reduced demand leading to lower revenue and earnings as compared to when the economy was healthier. When demand decreases, then companies begin laying off employees. That is likely to lead to an uptick in unemployment as many companies and businesses are shedding employees.

Declining Economic Indicators

One economic indicator that means a lot for the health of the economy is the housing market. The reason why housing is so important is because it comprises about 15% to 18% of GDP. We are experiencing significant declines in real estate sales due to higher mortgage rates.

Housing starts declined 16.4% in November 2022 over November 2021. Building permits declined 22.4% year-over-year with an 11.2% decline from October to November. While new home sales increased 5.3% from October 2022 to November 2022, they dropped 15.3% year-over-year in November 2022. Existing home sales fell for 10 consecutive months . November existing home sales declined 7.7% from October with a large 35.4% decline year-over-year.

Higher mortgage rates are having a negative effect on home sales. This is only likely to get worse as the Fed continues to increase rates in 2023. Many potential buyers are likely to wait for lower rates and/or lower prices as they might be priced out of the market for the type of house that they want to purchase.

Another indicator that looks troublesome is the ISM Manufacturing report. Economic activity in the manufacturing sector declined in November which marked the first decline since May 2020 . The November Manufacturing PMI came in at 49%. Percentages below 50% show contraction in manufacturing activity. The Backlog of Orders Index came in at 40% and was 5.3% lower than the October reading. This could be the start of a new downward trend in manufacturing especially with the backlog of orders declining.

One bright spot in the economy has been the services sector. The ISM Services PMI came in at 56.5% in November. This marked the 30th consecutive month of growth for services. However, I think it is likely that some parts of the services sector are likely to decline in 2023. That includes real estate which is likely to decline as higher mortgage rates reduce demand. Declines in 2023 could also occur in construction, retail, wholesaling, transportation, and warehousing if slower economic activity spreads due to less consumer and business investment demand. Services that are likely to hold up well include Agriculture, Healthcare, Utilities, and Food Services which can be considered non-discretionary spending.

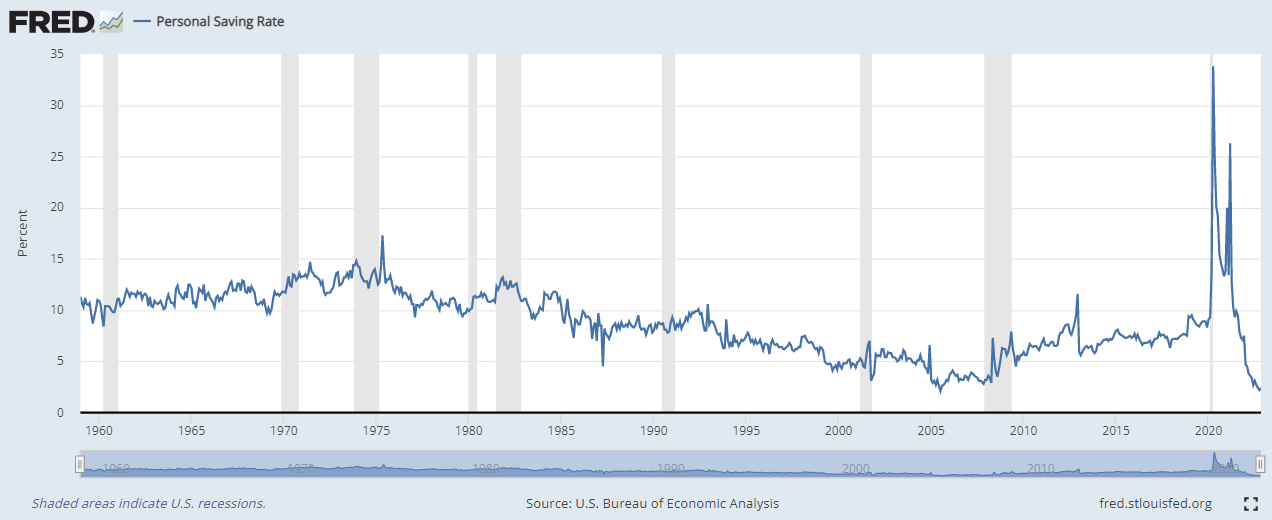

Another important point for the 2023 outlook is that the personal savings rate declined to a low level.

{kind=link}

The chart above shows that the personal savings rate dropped below where it was at the beginning of 2008. The high savings rate in 2020 led to strong growth as the economy opened back up from the COVID lockdowns. However, consumers are now beginning 2023 with much less saved up. This is likely to suppress demand as money is more likely to be spent on necessities such as food and energy and less on major discretionary purchases such as new homes, vehicles, travel, and entertainment.

Technical Perspective

{kind=link}

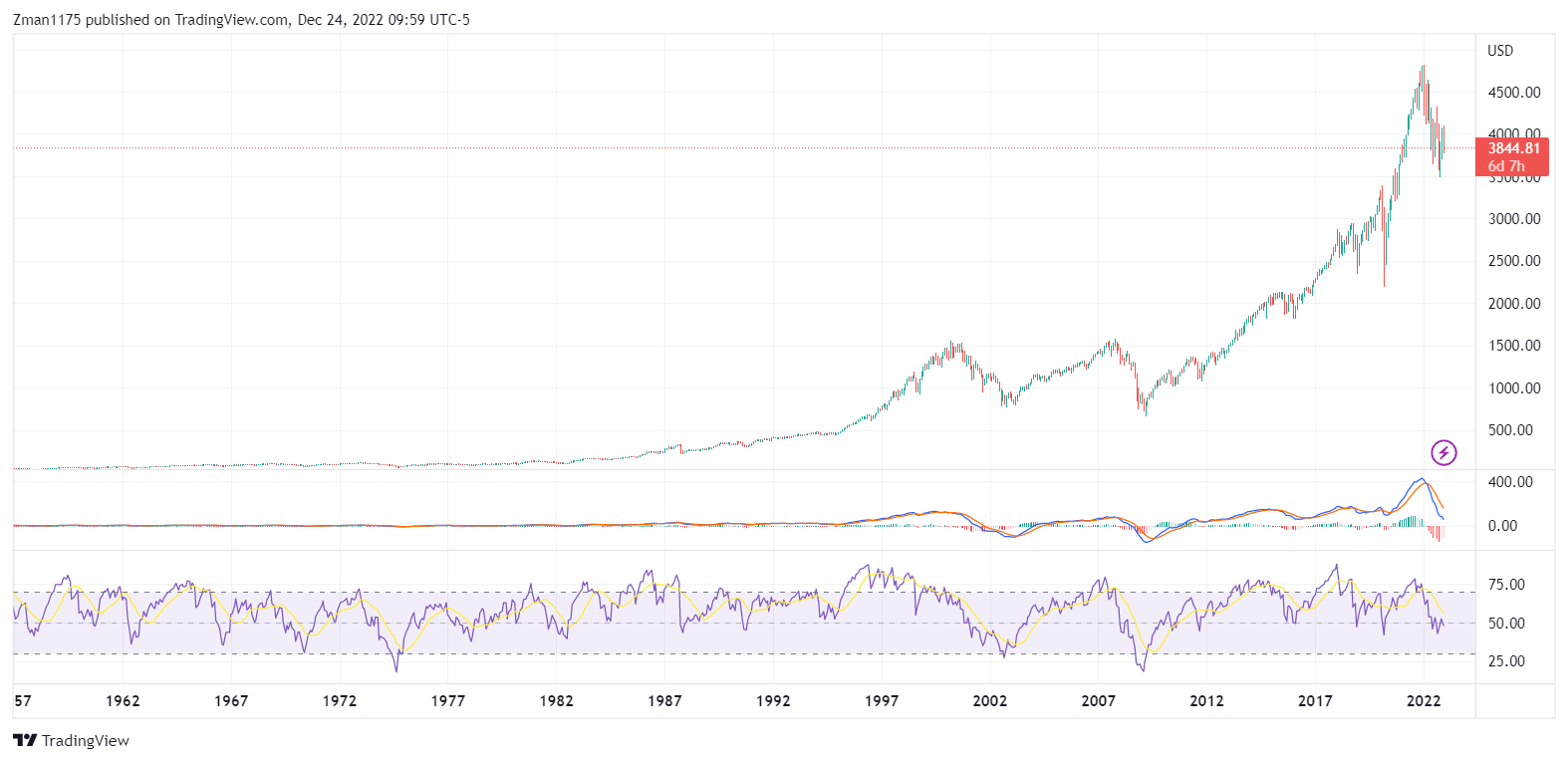

The monthly chart above provides a long-term perspective on how the S&P 500 traded in terms of overbought and oversold conditions. The RSI (purple line at the bottom of the chart) has been declining and is showing weakness below 50, and could be headed for an oversold condition below 30. Note that the last two major bear markets in 2008 and 2002 drove the RSI below 30. I didn't count the COVID recession because that was an anomaly and not a part of the longer-term natural business cycle. If this bear market behaves similarly to the 2002 and 2008 markets, then there is much more downside to go.

The MACD indicator above the RSI has been in decline and looks bearish as it has been dropping towards the zero line. Note that the MACD did drop below the zero line in 2002 and 2008. So, this could also indicate that we could see much lower prices in 2023 for the S&P 500.

Price-wise, the S&P 500 lost about 50% in the dot com bubble bear market and about 58% in the 2008 financial crisis bear market. We could see losses similar to the 2000-2002 bear market as valuations may need to come down further before the bottom is in. If we get a 50% drop in this bear market from the market highs, we could see the S&P 500 drop to $2400. However, the market may not fall that much in this bear market.

2023 Forecast for S&P 500

It can be difficult to forecast exactly where the S&P 500 will be at the end of 2023, but I will make an educated calculation for entertainment purposes. I will do this based on expected profits and the valuation for the S&P 500.

I think the interest rate increases will take a little longer to have a significant negative impact on the economy to the point of 2 consecutive quarters of negative growth. So, I am projecting that we see a recession in Q3 & Q4 of 2023.

I think that analysts are overestimating the S&P 500 earnings for 2023. Goldman Sachs Group is projecting S&P 500 EPS of $224, while JPMorgan Chase & Co ( JPM ) projects $205. The consensus estimate is $231 . I am projecting a lower EPS of $180. The reason why I am going lower is because I think the energy sector will take a hit in the 2nd half of 2023. Energy will probably remain strong in the 1st half of 2023 as the economy remains weak but not in deep recession territory. The energy sector (oil prices in particular) tends to drop significantly during full-blown recessions. I believe that will happen in the 2nd half of 2023. Therefore, earnings for oil and energy-related companies are likely to decline significantly in Q3 and Q4 2023 in my opinion.

The S&P 500's valuation in terms of trailing P/E ratio is currently about 19 . I am projecting that the S&P 500's PE ratio drops to 16 by the end of the year as the market continues to sell-off during an end of year recession. Therefore, my projection for the S&P 500 price at the end of 2023 is $2880 (PE of 16 x EPS of $180). This would be about a 40% drop from the all-time high of $4818 and 25% lower than the current price.

There are many factors/risks to consider that would make my projections incorrect. An actual end of the Russian-Ukraine war would be positive for the market and would likely lead to a rally. The actions of China opening up its economy could be more positive for the global economy than expected and help us to avoid a recession.

On the other hand, if China backtracks and implements full blown lockdowns sometime during the year, it could lead to economic conditions to be worse than expected. If the Ukraine war escalates and other countries become more involved, it could lead to a much more bearish market and lower than what I am projecting.

I am normally positive and optimistic about the stock market and the economy. However, the current developments have me realistically bearish when looking at 2023.

Editor's Note : This article was submitted as part of Seeking Alpha’s 2023 Market Prediction contest. Do you have a conviction view for the S&P 500 next year? If so, click here to find out more and submit your article today!

For further details see:

Stock Market And Economic Outlook For 2023