SSLY - Stocks Will Keep Rising As Inflation Keeps Falling

2023-04-14 10:54:39 ET

Summary

- Yesterday's Producer Price Index was well below expectations, reinforcing the disinflationary trend that started last June.

- Stocks soared on the news, as producer prices are a precursor to consumer prices.

- This should end the debate about future rate hikes, and increase the likelihood of a soft landing.

- Corporate earnings may outperform as cost cuts and dollar weakness serve as a double tailwind for Q1 results.

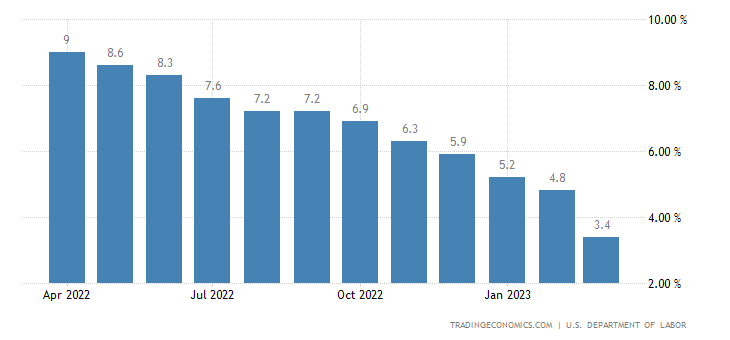

What a difference a day makes. Producer prices plunged in yesterday’s Producer Price Index report - PPI, as the headline number fell 0.5% for March, which was the largest drop in three years, compared to expectations for no change. This resulted in the annualized rate falling to 2.7%, which was below expectations for 3%. The core rate, which excludes the volatile food and energy components, fell 0.1% for the month and plunged from 4.8% to 3.4% on an annualized basis. The expectation was for a decline 4.4%. Since producer prices are a precursor to consumer prices, this confirms that the disinflationary trend is still on track.

{kind=link}

Stocks soared on the news, reversing the prior day’s losses, which were the result of meeting minutes that indicated Fed officials see a mild recession later this year. Those losses were compounded by Fed President Tom Barkin stating that more rate increases were likely needed to contain inflation. I disagree. I think this PPI report is the evidence Chairman Powell has been looking for to bring an end to the Fed’s rate-hike cycle. We're starting to see the first signs of deflation in the pipeline.

{kind=link}

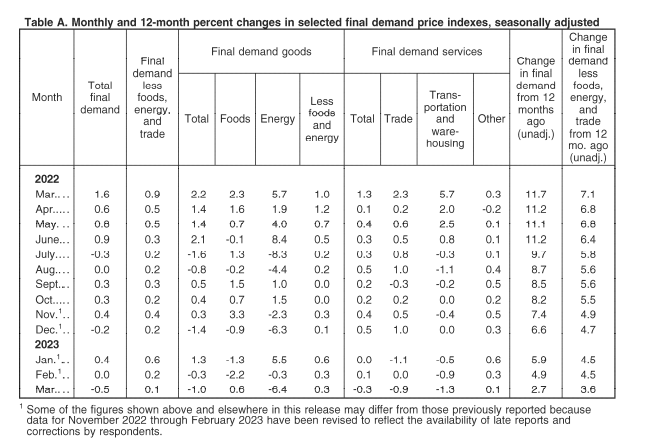

Inflation hawks have been obsessed with the sticky price increases in services for some time. Note in the details of the PPI report below that final demand services fell for the first time in months. The 0.3% decline was the largest since April 2020.

{kind=link}

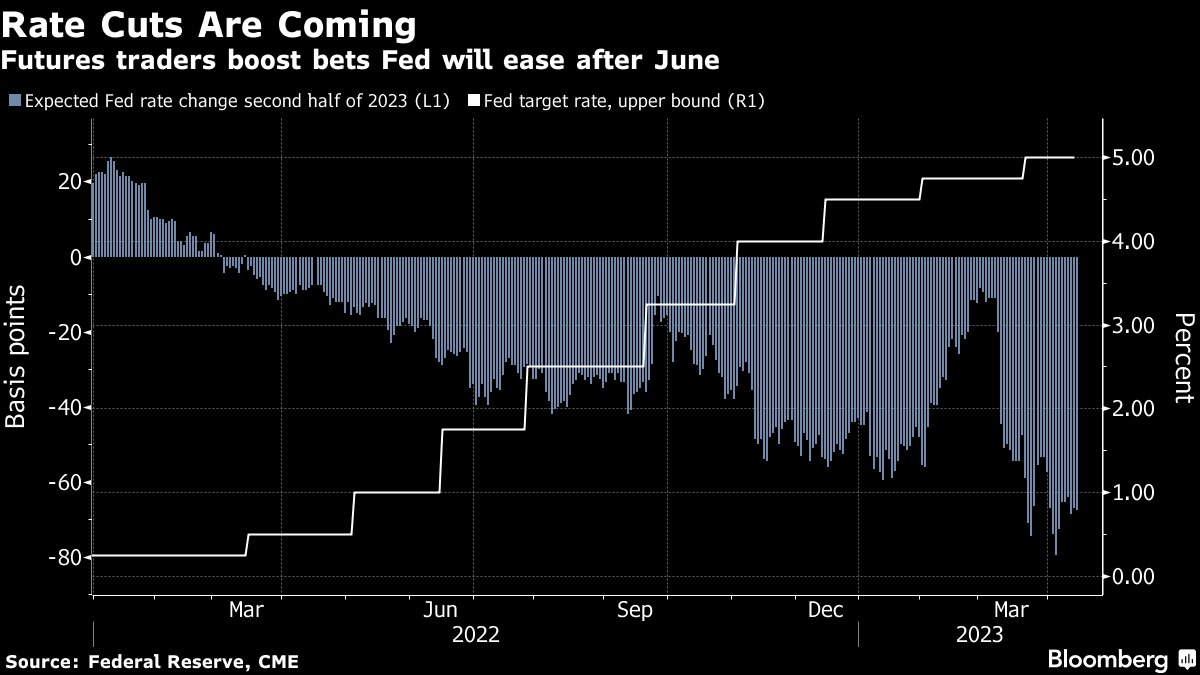

This is why markets are expecting the Fed to cut rates later this year by as much as 75 basis points. The bears will assert that this is because a recession is imminent, but I think it will have more to do with a rapidly-slowing rate of economic growth that compliments the equally rapid decline in the rate of inflation.

{kind=link}

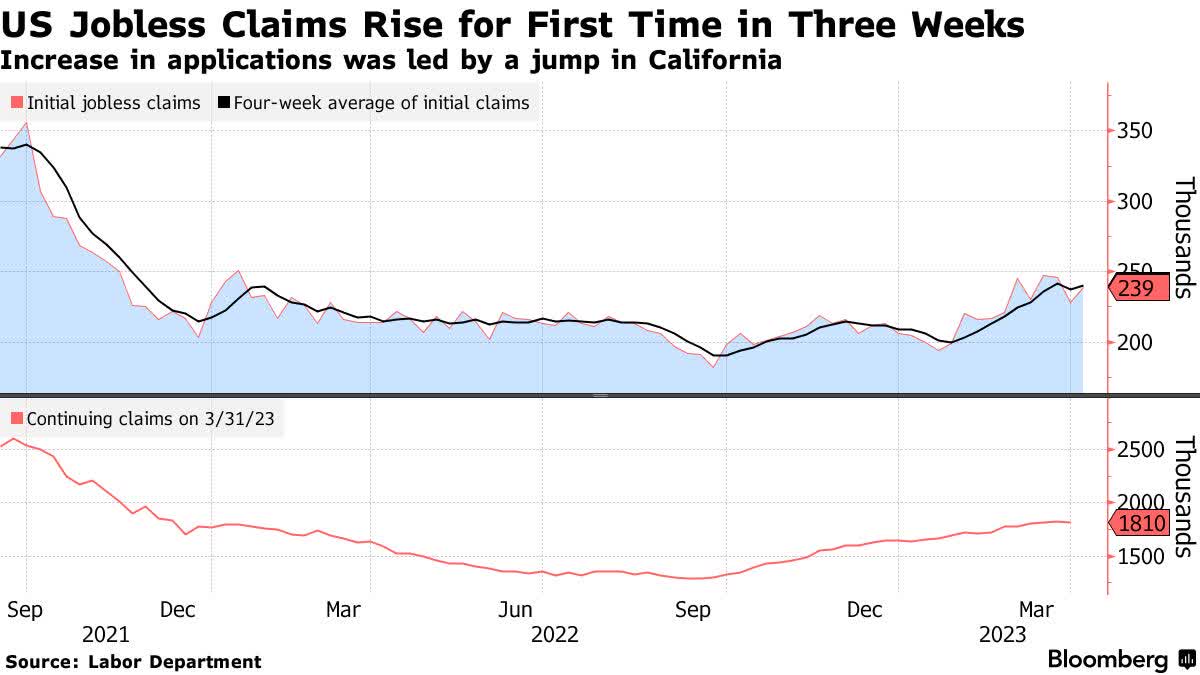

The strength of the labor market is what should keep this economy growing, as reflecting is the very modest increase in weekly unemployment claims yesterday to 239,000. That level is still below what we saw in January 2022. Labor market strength has been sustained despite the rapid decline in prices for goods and soon to be services. The is what soft landings look like.

{kind=link}

As we begin the official earnings season today, the importance of the decline in the PPI will come into play because it measures corporate costs. Most companies took measures to reduce costs and become more efficient last year to head off the increase in prices. Now those prices are coming down, while the cost cutting benefits remain in place. That should help sustain profit margins. Additionally, the US dollar has weakened measurably since the start of the year, which will be another tailwind for corporate profits, especially for the S&P 500 companies. This combination of a weaker dollar and cost cutting efforts should result in bottom-line results outperforming the consensus estimate for earnings to decline 6.8% in the first quarter of this year.

For further details see:

Stocks Will Keep Rising As Inflation Keeps Falling