DJIA - Stocks Will Rally As Doom-And-Gloomers Overplay The Inflation Hand Again

Summary

- Stocks have pulled back from their highs following a round of mixed economic indicators.

- Concerns that inflation is re-accelerating may be unfounded, with the January data simply noise to the big picture.

- Stronger trends of economic activity are positive for corporate earnings as a catalyst for equities to rally higher.

As predictable as the sunrise, the latest round of market volatility has brought out the stock market bears calling for a pending big crash lower. This is from the same group that spent the second half of 2022 warning higher interest rates would cripple the economy resulting in surging unemployment, and that collapsing corporate earnings would definitely be here by now.

As those predictions haven't materialized, the next step is to naturally start moving the goalposts. The latest angle is the concern that inflation is accelerating, undermining the Fed messaging that the disinflationary process has started, forcing a walk back to the pace of slowing rate hikes.

We don't see it that way. The bigger story has been the stronger-than-expected economic data between labor market trends and even consumer spending. This is important as these factors play directly into supporting corporate earnings as a primary factor in stock prices.

We're nearly two-thirds through Q1 2023, and there's a case to be made that companies are having another solid quarter. Anyone expecting S&P 500 ( SPX ) companies to start reporting widening losses is going to have a hard time in the next few months.

The reality here is that the S&P has gained a solid 5% to start the new year, is around 12% higher from the October market bottom, and even up from levels last April. We're bullish and expect more upside.

Inflation Is Not Out of Control

The doom-and-gloomers have some fodder to work with, considering the January PCE came in hotter than expected climbing by 0.6% from December compared to a market estimate of 0.5%. That move was enough for the annual headline rate to tick higher to 5.4% from 5.3% last month, although still sharply lower from the cycle high of 7%. This follows a similar trend to the CPI data covering the same month.

Sure, investors would have rather seen those prints surprise in the other direction, but it's hardly a game changer in the big-picture. By all accounts, the annual inflation rate will resume its downside trend and we can look forward to the upcoming February CPI data as likely a more important data point providing a second chance to set the record straight.

Notably, the next inflation update set for March 14th will come ahead of the Fed's March 21st meeting. There's the potential that the February numbers work to pour cold water into the narrative that inflation is still out of control.

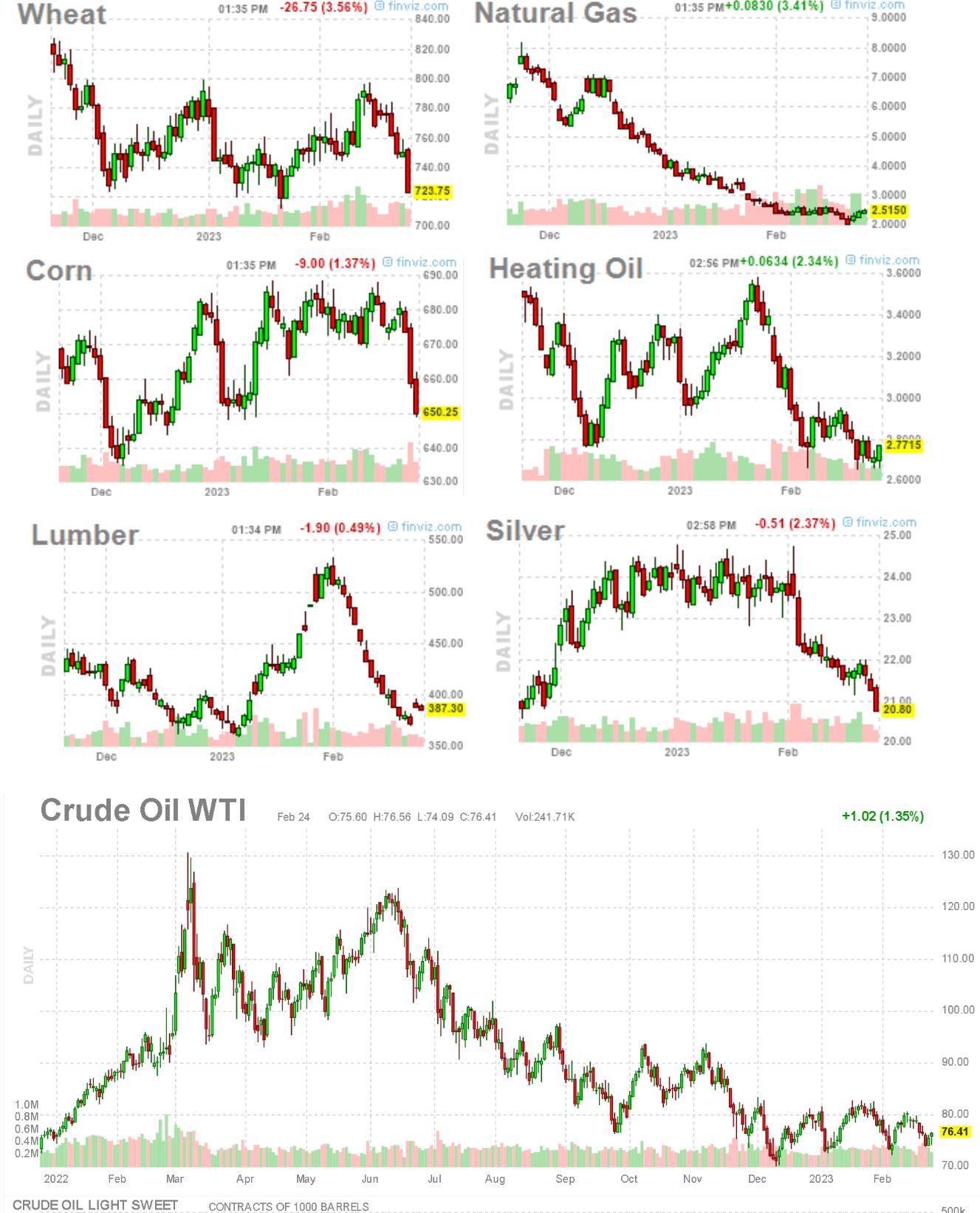

The good news is that commodities across energy, agriculture, and metals have been cooperating, with several markets down on a monthly basis and even lower compared to levels at the end of 2022.

The biggest factor here has been the normalization of skewed supply chain disruptions and trade bottlenecks that defined Q1 and Q2 last year. There will always be daily price volatility, but none of the charts below suggest supply-side factors as pushing inflation higher.

{kind=link}

source: finviz

For the January data, a bump higher in energy including gasoline was cited as a culprit to the monthly inflation rate staying elevated, but that also goes both ways. Indicators show the price of not only retail gas is down from January but also diesel which often plays a bigger role on the cost side of the economy.

There is also an understanding that "core" consumer prices beyond food and energy have a connection to non-core items. What we mean by this is that companies facing higher input costs, either in raw materials or through logistics, use those trends as reasons to increase prices. That was a big theme in 2022, but that is simply no longer in place at the same level.

We can also claim that the Fed rate hikes are still working through the system and slowing the underlying pricing pressures, even if there is a lag or monthly noise in the opposite direction. Housing is still correcting, and credit conditions are tightening. At least softer economic data should limit inflation compared to what we saw last year.

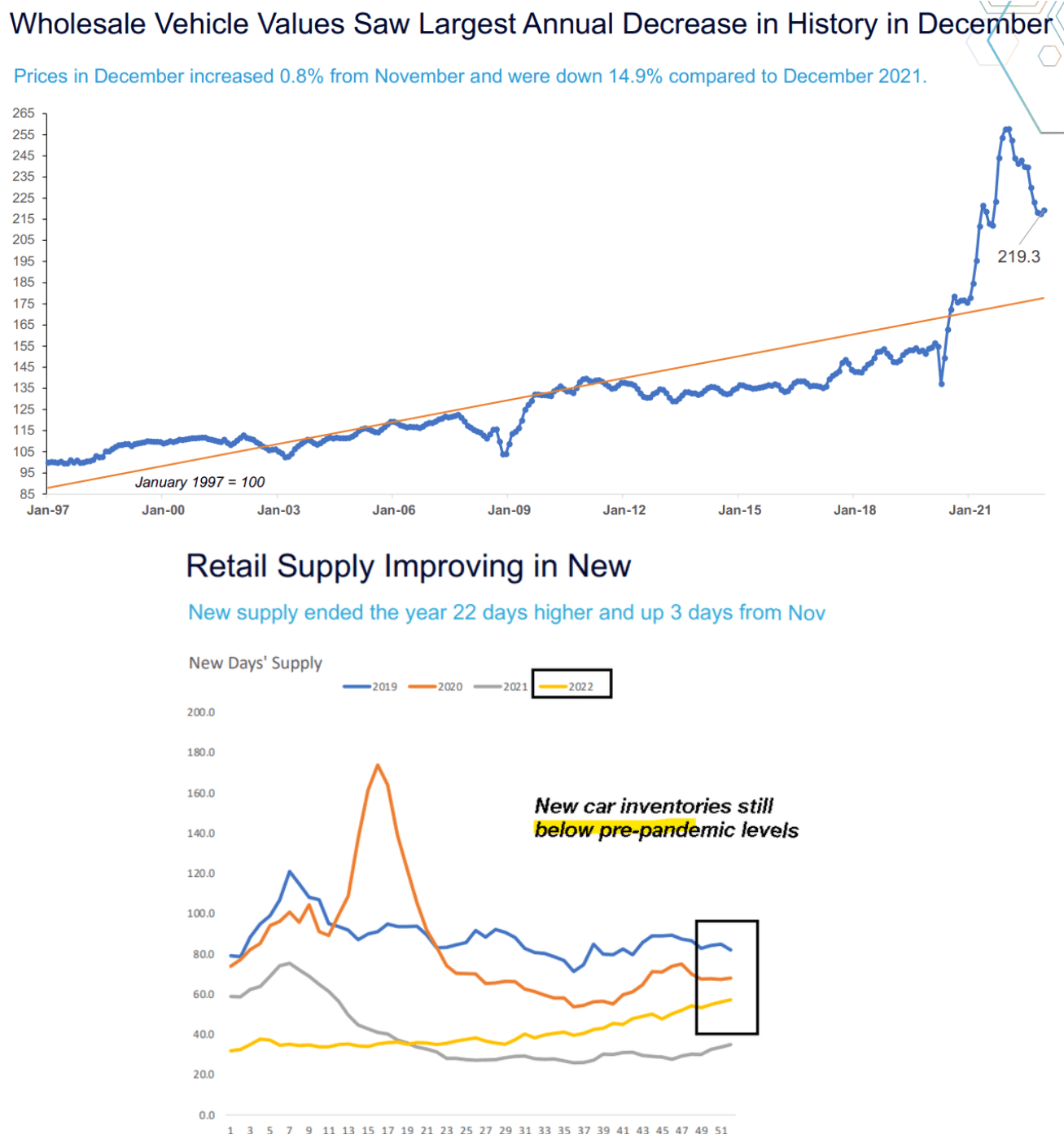

The other headline that has gotten bears out of their seats, is the data of a rebound in used-car prices to start the year. This dynamic goes back to exceptional pandemic-era circumstances when automobile production globally simply halted to a standstill. The lack of availability at a time when consumers were flush with cash based on global stimulus efforts drove a shortage of cars and fueled a record spike in used car prices.

We expect that this trend will normalize. The data we're looking at suggests "new car" inventory in retail dealerships remains below pre-pandemic levels . As automakers rush to expand output to take advantage of elevated pricing, there is simply no reason "used cars" would continue to trend higher. This is also the major headwind for the highest auto lending rates in over a decade.

Technically, the industry term is residual values . Historically, a used car was expected to lose more than 50% of its original price in three years. That ratio fell as low as 25% in early 2022, reflecting the "appreciation" of some vehicles. There simply isn't a fundamental reason a 3-year-old car should be nearly the same price as a new version, and that will revert to normal eventually.

The point here is to say that the January used-car component within the CPI was more noise than anything else in our opinion. Digging through the data, we found that dealers had cut back on wholesale purchases back in Q3 and Q4 forcing some stock rebuilds to start the year, part of the normal operating cycle. On a year-over-year basis, used car prices are down more than 10% from the peak 2021 level.

{kind=link}

source: Manheim

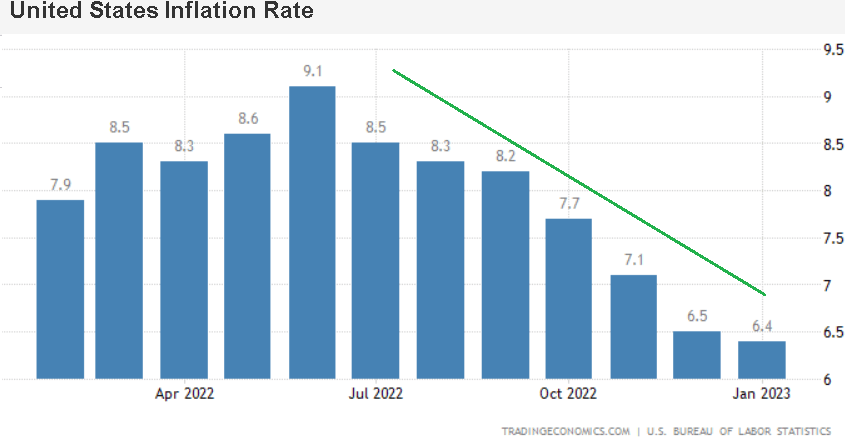

So when we start talking about inflation, there is some uncertainty as to when the annual CPI will approach the mythical 2% Fed target. At the same time, getting closer to 4% later this year would go a long way to help reset the narrative toward a sense of macro stability.

The other factor investors can look forward to is that as we get into March and April data, the year-over-year comparison will be up against a tough benchmark from 2022. The annual rate should continue to fall as a more favorable backdrop.

{kind=link}

source: tradingeconomics

Good News is Good News For Stocks

There is nothing wrong with maintaining a cautious approach towards equities or even expecting some downside. What is a problem is attempting to reconcile a bearish expectation for a looming "hard landing", which by definition would involve deflationary demand destruction, while at the same time calling for the CPI rate to keep running higher. The bears need to pick a side on that one.

The surprise over the past year, which largely explains the current stock market strength, is that the Fed taking rates from 0% in 2021 to the current level approaching 5% was not the end of the world.

If you go back to Q2 last year when the S&P was trading under $3,600, the setup we have today was simply not supposed to happen according to those that were convinced of even more downside. The latest data is impressive in this regard.

- Q4 GDP climbed by 2.7% y/y

- January payrolls climbed 517k compared to the 116k estimate

- January retail sales up 3.0% m/m compared to a 1.8% estimate

- February Michigan Consumer Sentiment at 67, from a low of 50 last June

So these data points inferring "good" news for the economy have been interpreted as "bad" with the connection that they will continue to push inflation higher as a sort of carrot for why stocks need to reprice lower. We believe this line of thinking is wrong, and don't see a reason to be concerned that an extra rate hike is going to crack the outlook at this stage in the cycle.

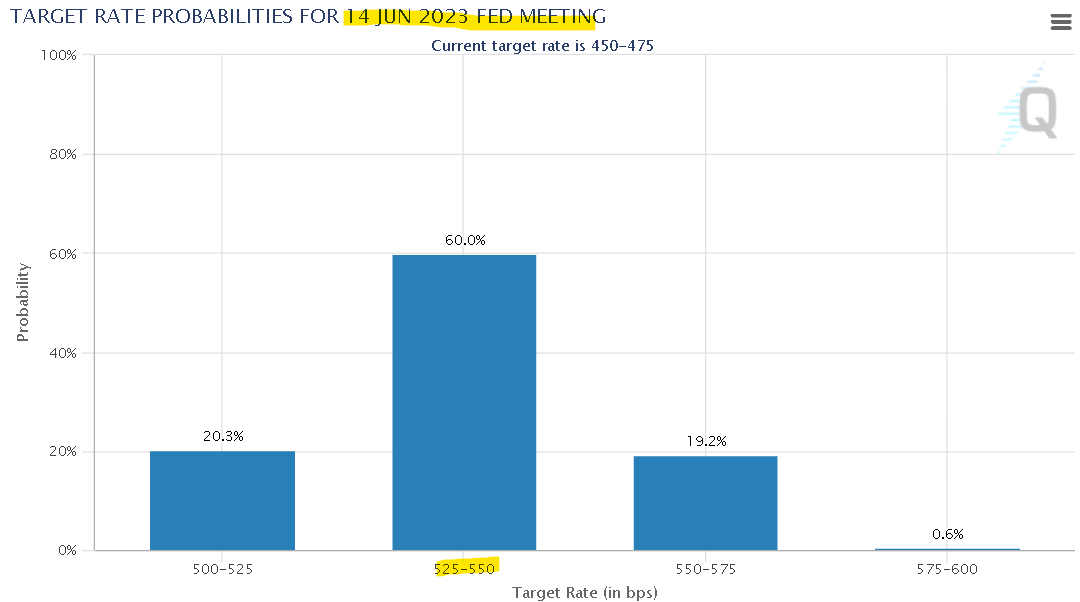

The current consensus is that the Fed will hike three more times this year, with a 25 basis point increase in March to 5%, May to 5.25%, and June to 5.5%. The change in the last few weeks is into the higher probability of that last move in June while noting the futures market still implies a 20% chance they "pause" at 5.25% from the May meeting. There is also a 19% chance the rate ends up at 5.75% at that meeting.

The group has said they are data dependent, and a surprise lower in the monthly CPI over the next four months is a possibility that would work to shift the expectation lower.

{kind=link}

So what investors need to be asking themselves now is which factor becomes the lesser of evils. Do you want economic conditions to start deteriorating rapidly, just so the CPI can make a faster move lower? Or are we content with the labor market and activity trends remaining resilient, despite higher interest rates?

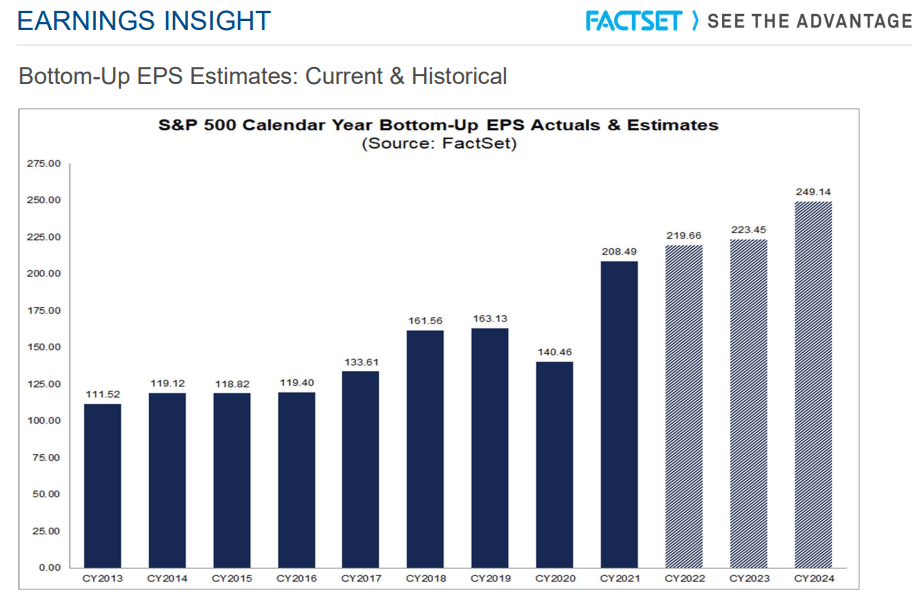

For stocks, every additional month that goes by with positive payrolls and further consumer spending strength ends up working more favorably as the backdrop for corporate operating and financial conditions. The market is currently eyeing a 2023 S&P 500 bottom-up EP S of $223.45, up 2% from the still pending final 2022 numbers.

The bullish case for stocks is that we get some revisions in earnings estimates higher as companies begin to benefit from stronger demand-side tailwinds into sales and earnings capture higher margins from the theme of cost-cutting and savings initiatives.

Into 2024, the setup looks more positive as earnings accelerate which would be under a backdrop of lower headline inflation, and stabilize interest rates. From the chart below, stock market bears will need a sharp reversal lower to earnings trends which we don't see happening.

{kind=link}

source: FactSet

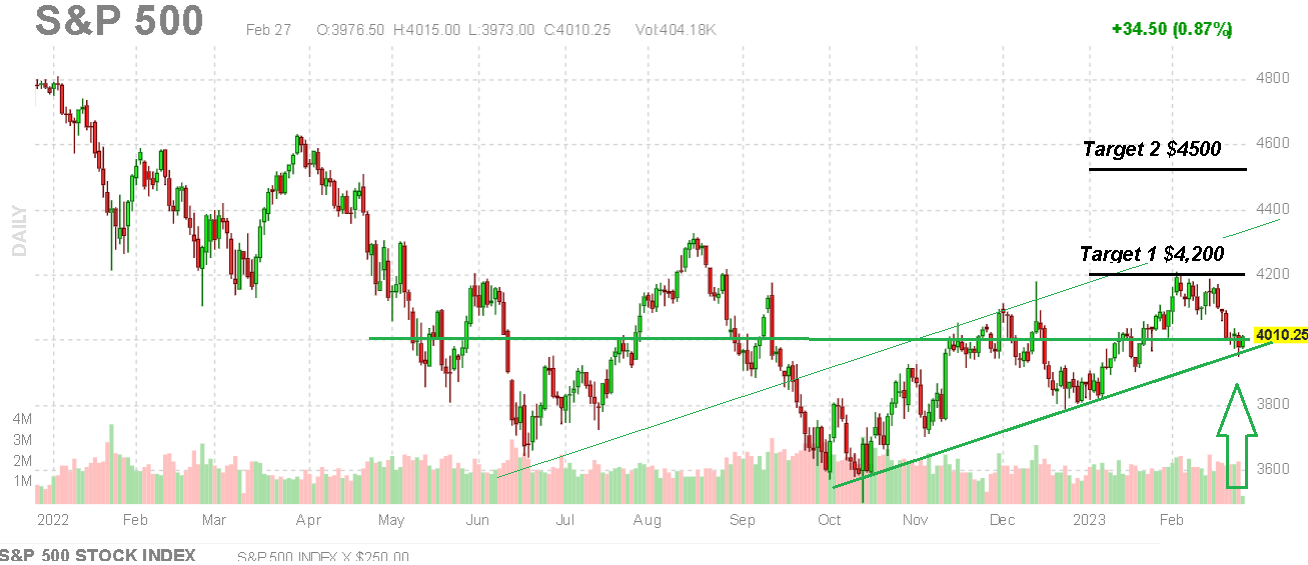

SPX Price Forecast

While the 2022 strategy of "sell the rips" worked into historically high volatility, we believe the setup now is to "buy the dip". From the rally to the start of 2023, the latest pullback may represent a new buying opportunity. The recent high of $4,200 becomes the next upside target while $4,500 into the second half of the year could be in play.

The way we see that target playing out is through a combination of stronger-than-expected macro trends while the inflation outlook resumes its trend of slowing going forward. A solid Q1 earnings season for S&P 500 companies can drive a string of revisions higher to full-year EPS estimates keeping the bulls in control.

On the downside, it will be important for the S&P 500 to remain above ~$3,800 as an important area of technical support. We would be concerned by sharply higher commodity prices or a significant jump to energy benchmarks like crude oil and natural gas which would signal a more concerning inflation pressure. The situation in Eastern Europe can also be highlighted as a potential tail risk for the market that will need to be monitored.

{kind=link}

source: finviz

For further details see:

Stocks Will Rally As Doom-And-Gloomers Overplay The Inflation Hand, Again