PAGS - StoneCo: Heading In The Right Direction Amid Challenges

2023-09-21 11:03:49 ET

Summary

- StoneCo's stock value has plummeted by over 90% compared to its all-time high in February 2021.

- The decline in stock value is attributed to macroeconomic and microeconomic factors, including increasing interest rates in the US and suboptimal capital allocation.

- StoneCo's second-quarter results show significant cost improvements and improved profitability, positioning the company favorably for capturing additional market share.

- Trading at a forward P/E ratio 75% lower than its historical average, StoneCo seems to hold promising growth prospects, particularly as risk aversion diminishes.

In the financial sector, Brazilian company StoneCo ( STNE ) operates as a payment services provider, with services such as credit and debit card payment processing, software, banking, and other services to online and physical merchants.

A little over two years ago, in February 2021, StoneCo reached its all-time high in stock value. However, as of the first quarter of this year, specifically in March, the company's shares had plummeted by over 90% compared to that peak.

It's important to clarify that the decline in StoneCo's stock value wasn't solely attributable to worsening business fundamentals. Within a high-growth company context, the main factors contributing to this decline included macroeconomic elements, such as the increasing interest rates in the United States, and microeconomic factors, including suboptimal capital allocation and growth challenges.

In the present analysis, we are operating under the assumption of a "worst is over" scenario concerning the US interest rate hike cycle and an observed downward trend in interest rates in Brazil. Despite experiencing fluctuations throughout the year, the company's valuation trades at a 75% discount compared to its historical price-to-earnings (P/E) multiple. Considering the more favorable economic cyclical momentum, the company is believed to have significant potential for further appreciation in the near future.

StoneCo Is Going Through a Moment of Transition

Over the last two years, StoneCo has been undergoing a restructuring of its target system, key performance indicators (KPIs), and objectives and key results.

In addition, significant work has been done on customer segmentation, seeking a more targeted approach. In the meantime, there have also been several changes in the company's technology management. These measures aim to improve the company's trajectory and address the challenges faced previously, bringing in an experienced and skilled leadership perspective to drive its development.

{kind=link}

In addition, management was strengthened with the integration of experienced professionals, and the Board of Directors was reformulated last year. One of the highlights was Pedro Zinner, former CEO of Eneva (a Brazilian power generation company), officially became Stone's CEO.

As a result, StoneCo, under new management, is on the path to delivering a net profit of over R$1 billion this year, which would considerably increase from the loss of R$519.4 million in 2022. This upturn is objectively based on continuing to grow efficiently, maintaining operational discipline, and focusing on the growth of micro, small, and medium-sized companies.

StoneCo considers 2023 to be a period of investment in technology, which will bear more excellent fruit in 2024 and 2025. Improved profitability in the second half of 2022 and better-than-expected guidance for this year's first half have reduced concerns about financing costs. Thus, in theory, developing an increasingly better operating result will be possible due to lower costs and expenses.

The consequence of this trend should be expanding the customer base in the acquiring business. This expansion will enable the introduction of new solutions and the capture of higher take rates, ultimately improving the expenses through effective pricing execution and enhanced monetization of banking solutions.

StoneCo's Latest Results

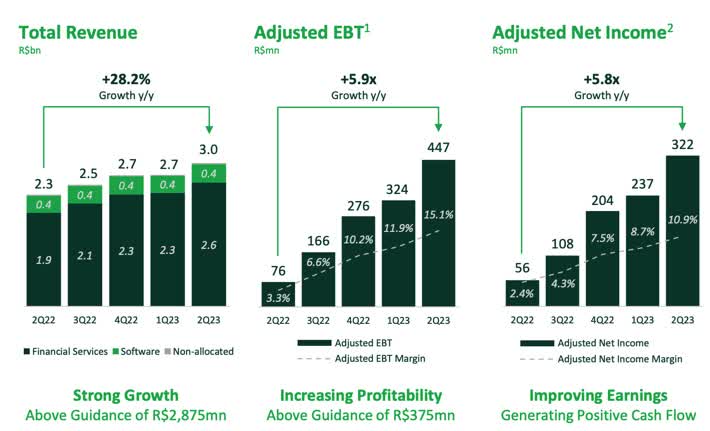

In mid-August, StoneCo released its second-quarter results, which were highly favorable. The company achieved significant cost improvements and an improved take-rate despite setbacks related to a low Total Payment Volume (TPV) on Key Accounts, dropping 32% from last year. Furthermore, the company exceeded its revenue, adjusted EBT (Earnings Before Taxes) guidance, and generated positive cash flow.

During the second quarter of this year, StoneCo reported an adjusted net profit of R$322 million, marking a 477% increase compared to the same period last year and a 36% increase compared to the first quarter.

The adjusted EBITDA stood at R$1.49 billion, reflecting a 46% year-over-year increase. This solid performance can be attributed to rising revenues and improved operational efficiency. These effects were partially offset by increased financial expenses as a percentage of revenues.

Adjusted EBT was R$447.0 million, up 489.3% year over year, with adjusted EBT margin increasing 3.2 percentage points sequentially to 15.1%, aided by operating leverage across all expense lines.

The company's net revenue, encompassing acquiring and software activities, reached R$2.954 billion, representing a notable 28.2% year-over-year growth. StoneCo attributed this impressive performance to its increased market share in micro, small, and medium-sized businesses.

{kind=link}

One of the key positive highlights was the increase in its Financial Services take rate (the commission charged to merchants on transactions), which rose by 38 basis points year-over-year for MSMEs (Micro, Small, and Medium-sized Enterprises) and by 28 basis points year-over-year for Key Accounts. A positive trend in market share and improved profitability was also driven by lower cost of services, decreasing from 27.2% in Q2 2022 to 23.2% in Q2 2023 as a percentage of revenues. Selling Expenses also showed a sequential decrease, dropping from 14.4% in Q1 2023 to 13.9% in Q2 2023 as a percentage of revenue.

Despite a 12.5% increase in financial expenses in Q2 compared to the same period the previous year, this was due to StoneCo's strategy of maintaining a larger average cash position during this period as a conservative measure. The company ended with R$4.3 billion in cash, an increase of R$1.6 billion from Q2 2022, partially offset by R$332.2 million of CAPEX and R$28.7 million from M&A expenses.

StoneCo's IR

The company also demonstrated an evolution in banking, with strong net additions of clients of 419,000 (compared to 560,000 in the first quarter). This growth was bolstered by the digital account solution for "Super Conta Ton" customers. However, the software business continued to disappoint in Q2, with revenues declining by 9% year-over-year, compared to a 10% decrease in Q1. This decline was primarily due to lower inflation and transactional revenues.

In summary, the second-quarter results yielded numerous positive aspects. Additionally, this quarter has reignited optimism regarding the competitive landscape in the MSMB segment. StoneCo's distinctive business model, user experience, and product offerings continue to position the company favorably for capturing additional market share.

Valuation Is Not a Major Concern

Despite trading at approximately 88% below its historical peak, StoneCo still trades at a 50% premium compared to the industry average. It is priced at a multiple of earnings 5 times higher than its primary domestic competitor, PagSeguro. However, it's important to note that StoneCo's forward P/E ratio is currently discounted by 75% relative to its historical average.

Above all, it's important to emphasize that StoneCo possesses certain competitive advantages that potentially justify its premium compared to its peers.

Despite facing stiff competition, with Cielo ( CIOXY ) and PagSeguro as prominent players in the Brazilian acquiring market, StoneCo has a comprehensive value proposition. This means it offers solutions that fully address customers' needs, a feat its competitors have not yet achieved by combining banking services with the acquiring function.

Brazil's small and medium-sized business segment lacks a more integrated banking offering. StoneCo views this as an opportunity for growth and profitability. The company is positioning itself as a "one-stop-shop" where customers can access all the required integrated solutions. This approach aims to provide customers with a unified experience and meet all their needs.

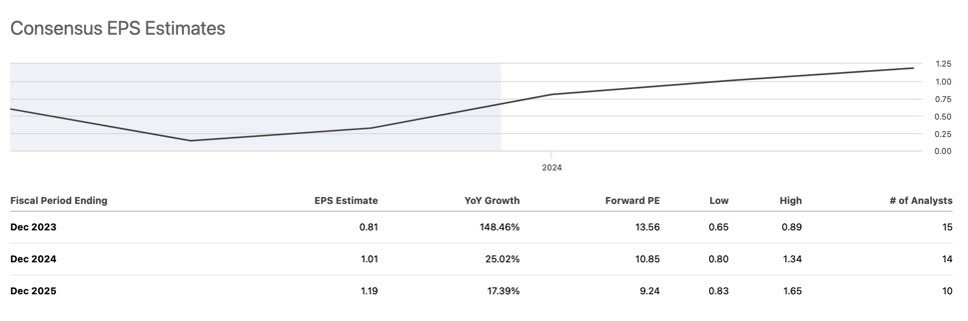

When we examine the estimates for StoneCo's EPS (Earnings Per Share) growth over the next two years, the multiple is expected to decline to 9x by 2025. This would align the company with the industry and make its multiple more appealing.

{kind=link}

Challenges Ahead, But Promising Prospects

For Stone to regain its competitive edge sustainably, it is crucial to continue timely repricing of the take rate, focus on micro, small, and medium-sized enterprises, and exercise prudent and controlled expense management.

On the credit front, where the company is expected to return to growth next year, maintaining extremely disciplined control of defaults will be vital. This is particularly critical in the current credit cycle, where Brazil's defaults remain elevated, considering the company's track record in this area.

As implied in the guidance, the outlook for revenue growth of 22% for Q3 suggests challenges related to the slowdown in TPV within the sector and the further expansion of EBT. This expansion seems to be reliant on greater cost efficiency, and that's the biggest risk of the thesis, in my view.

Lastly, I believe that the stock's performance has been hindered by overly cautious investor sentiment, which may gradually change as the second-quarter earnings seasons of Brazilian banks indicate that defaults have peaked. Furthermore, the trend of falling interest rates in Brazil (forecasted to reach 11.75% by the end of 2023) could be a tailwind for improving TPV results from 2024 onwards.

With its 2023 P/E ratio trading 75% below its historical average, I view StoneCo as having promising growth prospects, particularly as investors' risk aversion gains strength.

For further details see:

StoneCo: Heading In The Right Direction Amid Challenges