SNEX - StoneX Group: Industry Tailwinds And Strong Results Should Fuel Growth

2023-12-12 23:51:36 ET

Summary

- StoneX has reported strong financial results for Q4 and the full year, driven by favorable market conditions and increased product offerings.

- The company is expanding its product portfolio to target additional clients and increase profitability.

- The company is undervalued and has the potential for significant growth, with a 48%-52% upside from the current price levels.

Investment Thesis

StoneX Group ( SNEX ) deals in providing clearing and execution services, advanced digital platforms, and global market expertise. I wrote an article on SNEX last year , where my main thesis was the acquisition of cotton distributors. In a recent conference call , the management confirmed that this acquisition has already surpassed first-year financial expectations. I also mentioned in last year's article that the company has experienced significant growth in its customer base. It has recently reported strong financial results for Q4 and FY2023, and I believe it can sustain this performance as a result of favorable market conditions and its increased product offerings.

About SNEX

SNEX is a global financial service that offers end-to-end clearing and execution services, advanced digital platforms, and global market expertise to its clients worldwide. The company has 54,000 institutional, commercial, and global payment clients and a presence in over 180 countries with about 400,000 retail accounts. Its capabilities mainly include Execution, Clearing, Advisory Services, OTC/Market Making, Physical Trading, Market Intelligence, and Global Payments. It conducts its business in four operating segments: Commercial, Institutional, Retail, and Global Payments. The Commercial segment consists of activities linked to the management, identification, monitoring, and hedging of different commodities and financial risks experienced by commercial businesses, including risks related to foreign exchange, interest rates, precious metals, agricultural commodities, industrial metals, energy and renewable fuels, and other physical commodities. This segment contributed approximately 95.70% to the company’s total revenue. The Institutional segment offers its clients a comprehensive suite of equity trading services. It also places, originates, and structures debt instruments in the international and domestic markets. This segment accounted for 2.48% of the company’s total revenues. The Retail segment offers its clients access to 18000 financial markets globally, including CFDs and spot foreign exchange. It also deals in retail precious metals and wealth management services. This segment contributed approximately 1.45% to the company’s total revenues. The Global Payments segment provides technology, treasury, and customized payment services to banks and commercial entities as well as NGOs, charities, and government organizations. This segment represented approximately 0.34% of the company’s total annual revenues in FY2023.

Financials

The company has seen robust growth over the years as it has been consistently evolving and adding more clients to its portfolio by introducing a diverse range of products and services. Recently, the market volatility and rising interest rates have acted as great industry tailwinds that have increased the company’s profitability. In addition, the long-term perspective is also highly positive as globalization boosts international investing and accelerates transaction levels. The volume of securities transactions rose by 57% which reflects the impacts of volatility. Identifying these market dynamics, the company has various expansion plans in its growth pipeline, which are at progressive levels. Discussing the international side, it is working on the final tests of launching cash trading in international equities in the upcoming quarters. I believe this expansion of the product portfolio can accelerate the company’s growth as it can potentially target additional clients and increase its profitability. In addition, it is also working on adding more capabilities and products apart from CFDs such as precious metals, coin payments, crypto, futures, and foreign exchange. As per my analysis, this can help the company to expand its addressable market significantly and increase its market share by acquiring more clients. The competitive environment also seems to be favorable as the company expects that banks might have a huge capital charge as a result of the recent FIA conference which can create increased opportunities for the business. I think it can sustain this upside for a longer time as the regulatory environment is highly strict, which acts as an entry barrier and helps the firm to maintain its competitive position.

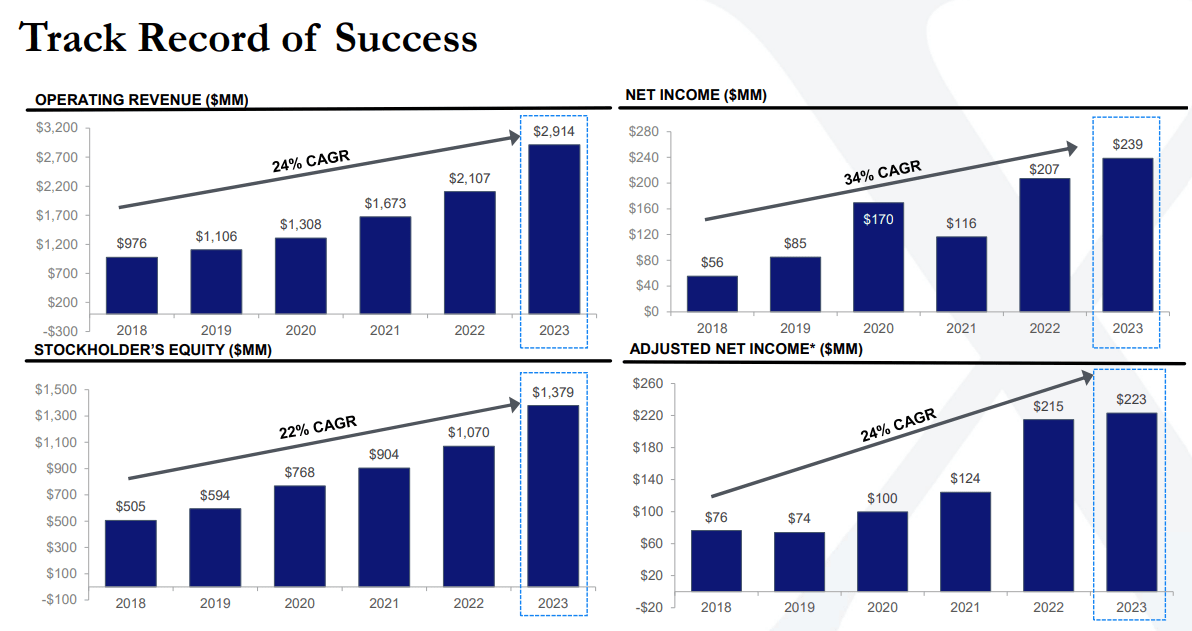

Growth of Various Financial Metrics of SNEX (Investor Presentation: Slide No: 13)

{kind=link}

The company has reported its quarterly results. It reported operating revenue of $778.00 million, up 33.35% compared to $583.40 million in Q422. This growth was mainly fueled by increased interest rates and volatility. Net income declined by 3.05% YoY from $52.30 million to $50.70 million due to high income tax expenses. It reported a diluted EPS of $1.57 (with the effect of stock split). The Commercial, Institutional, Retail, and Global Payment segment revenues were $207.50 million, $426.50 million, $92.4 million, and $54.2.40 million respectively. The company’s ROE stood at 15%

It has also recently reported its FY2023 results. It has reported operating revenue of $2.91 billion, which is a 38.27% YoY increase compared to $2.10 billion in the prior year. It was mainly fueled due to increased volatility in the market. Net income jumped by 15.16% YoY from $207.10 million to $238.50 million. It reported a diluted EPS of $7.45 ( with the effect of stock split). The company ended its quarter and year with $1.10 billion in liquidity.

The company has performed well in the last quarter and the annual performance also appears to be impressive. I believe the current market conditions and the company’s growth in the addressable market are key factors that are to be considered in analyzing its future growth. It is exponentially increasing its addressable market by introducing new product categories which I believe can attract a large customer base and can expand its profit margins.

What is the Main Risk Faced by SNEX?

The company highly depends on vendors and other third parties to obtain services that are required to offer clients its products and services. These services include core infrastructure such as communications, utilities, and web hosting services to systems that facilitate the company to process and execute transactions. If the parties fail to offer these services due to operational issues and cyber-attacks, it can negatively impact the company’s operations and can further contract its profit margins.

Valuation

The company is highly benefiting from the recent market volatility and interest rate fluctuations and to cater to these opportunities, it has increased its capabilities significantly and working on more product expansions which can potentially increase its profitability in the coming times by adding more clients to its portfolios. After considering all these factors, I am estimating an EPS of $7.20 for FY2024 which gives the forward P/E ratio of 9.13x. After comparing the forward P/E ratio of 9.13x with the sector median of 10.26x , we can conclude that the company is undervalued. I think the firm can potentially grow in the next year as a result of positive market conditions and its increasing expansion of service offerings which can help it to trade above its sector median. I estimate that the company might trade at a P/E ratio of 13.90x in FY2024, giving the target price of $100.8, which is a 52.12% upside compared to the current share price of $65.79. However, in the scenario of rising inflation, the company's outsourced services such as communications, utilities, and web hosting services to systems can become costly. Expensive third-party services can put negative pressure on the company's profit margins. Therefore, in a bear-case scenario of lower margins as an outcome of expensive third-party services, I project that SNEX's EPS might be $7.08 and trade at P/E ratio of 13.75x which gives target price of $97.35, with potential returns of 47.97% compared to present share price.

Conclusion

SNEX has reported solid quarterly and full-year results. Its growth is primarily fueled by market volatility and rising interest rates have increased the volume of securities transactions. To cater to these opportunities SNEX has increased its product offerings & enhanced its platform. It is also working on adding more capabilities and products such as coin payments, future, and crypto which can expand its TAM (total addressable market) & boost its growth by attracting additional customers. However, it is exposed to the risk of high dependency on third-party vendors which might affect its profitability in case of disruptions. SNEX is currently undervalued and due to its expansionary operations, investors can look forward to solid 48%-52% rise from present share price levels. After taking into account all the above-mentioned factors, I assign a buy rating to SNEX.

For further details see:

StoneX Group: Industry Tailwinds And Strong Results Should Fuel Growth