SGFY - Stop Playing Short Term With CVS

Summary

- CVS is becoming engrained in U.S. medical care.

- Recent acquisitions are not added in great forward guidance.

- Don’t stare at debt numbers so much that you miss the income!

I have written a decent amount about CVS Health ( CVS ) back in 2020 both here and here , before its great run, as well as about a year ago . Anyone who put money to work with me easily gained over 80% if it was held. Admittedly, I have always held a partial position in the name but did trade in and out, gaining some funds to be used elsewhere as the name got pricier.

However, it is becoming clearer that this is not a good strategy with CVS. Don't get me wrong, I have not lost any money in the name, however, I purchased because I believed CVS was a sleep-well-at-night stock that I wanted to own long term. Trading around the position has taken time, and even though I have gained some advantages/funds, I submit that CVS is a name that should be held for the long term in order to power your portfolio without trading in and out. I also have fewer shares in CVS than I used too, as I put that money to use on things that should grow faster.

I am now seeing the wisdom in keeping core positions closer to untouchable… positions I do not trade in and out of. Some would say this is being foolish, some would say it is growing wiser - no matter which camp you fall into, let's look at CVS and see why it's worth a longer hold.

2022 Numbers In Review...

CVS just reported earnings for the 2022 year and, as expected, total revenue grew notching up 10.4% to $322 Billion . This worked out to $8.69 EPS, or if you prefer GAAP numbers, a GAAP EPS of $3.14. Cash flow was down 11.4% in 2022 but was still a nice $16.2B for the year. Q4 results show a 9.5% increase from 2021, rising to $83.8B in revenue and a quarterly GAAP EPS of $1.75.

This allowed CVS to pay $2.9B in dividends for the year - previously announcing a 10% increase going forward - and $3.5B in stock repurchases for the year. (A $2B accelerated repurchase plan started on January 3, 2023 and will affect future numbers.)

Healthcare brought in $23B in revenue for the quarter - a gain of 11.3% over 2021. The total medical memberships increased to 24.4 Million. As usual, Pharmacy brought in the lion's share of revenue by rising 11.2% YOY to $43.7B. Retail sales brought in $28.1B, for a gain of 4% over 2021.

Forward Guidance...

CVS also announced an expected guidance for the next few years, bucking the trend of most companies today, which tend to give less guidance. CVS execs issued an expected $7.73-$7.93 in GAAP EPS for 2023 (Adjusted EPS of $8.70-$8.90 vs. analyst consensus of $8.86) with a cash flow of $12.5-$13.5B. This assumes a roughly 3-5% increase in revenues, without factoring in the recent Oak Street ( OSH ) news. If Signify and Oak Street were included, things are highly likely to have better income - though, more expenses as well.

Giving more great forward guidance, CVS gave an adjusted EPS of roughly $9 in 2024, growing to $10 in 2025 - regardless of if the deals officially go through. Even if some consider this low, it is still an upward trajectory of over 10% per year.

The two billion dollar accelerated share reduction plan started on January 3rd this year. This means the roughly 1.31B share count will be reduced by 20 million shares, or 1.5% of outstanding shares. (This assumes roughly $100 per share, roughly 10% above current pricing.) This is part of a $10B in authorized repurchases, or over 7% share reduction. Of note, this reduces the dividend payout by $48.4 million with every two billion in share buybacks, as well as increases EPS going forward.

Recent Transactions...

The Signify Health ( SGFY ) transaction is approximately $8B and gains them access to 10,000 clinicians in 50 states, plus an analytics software/tech platform. Signify is instantly accretive to earnings and is expected to go through this year. Signify adds to their focused "Value-based care" plan.

Other writers have mentioned the virtues of this deal, including here (where the author points out that Signify was expecting to quadruple its revenue in the next decade alone) and here (where the author points out its greater growth potential vs. CVS alone and the reasonable price tag).

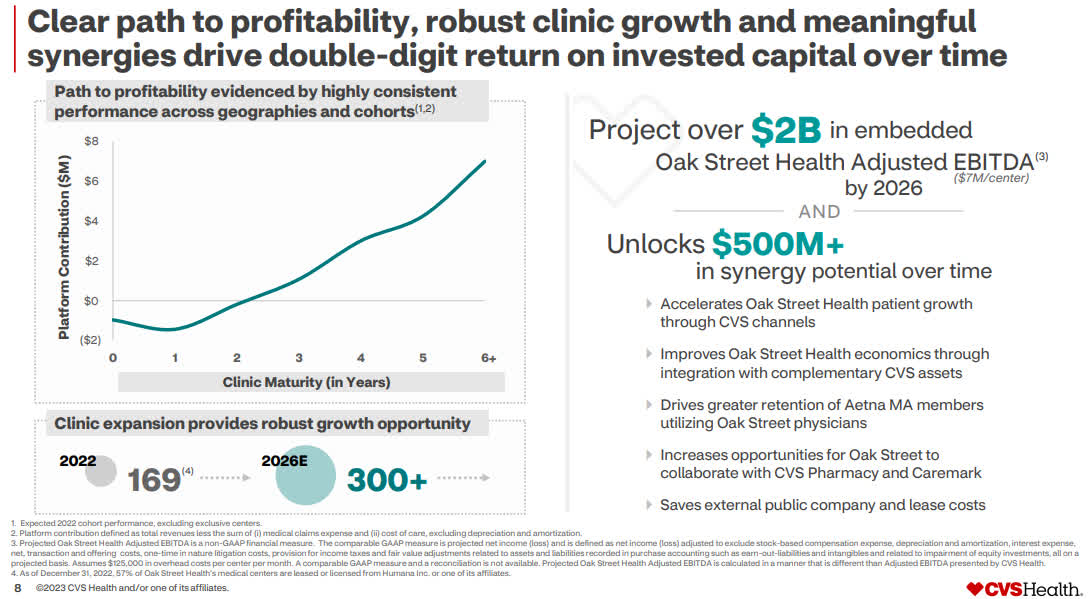

Also making news is the more recent announcement that CVS is planning to acquire Oak Street Health ( OSH ). Oak Street brings more primary care that can integrate vertically with CVS/Aetna health insurance and PBM. It is a drag on current earnings, however, has a great deal of growth expected from it. Oak Street states their platform is nationally scalable and provides predictable income, something CVS Health is very interested in. Also, Oak Street data suggests the platform reduces costs by around 17%, another benefit for any acquirer. OSH numbers also show they have had compound growth of over 50% for the past 5 years, even through Covid. Oak Street also would give CVS access to a planned 300 centers by 2026, plus it's assumed $2 Billion in EBITDA. (See slide below)

CVS slide from recent presentation (Source: CVS Presentation)

{kind=link}

And Growth...

With Medicare spending growing at 7% annually, this increases the CVS portion of income as well as gains a larger piece of the pie. This is exactly what a good business does, increases market share and/or wisely purchases the increase in growing markets. Medicare currently covers about 15% of the population, increasing 12% in 2022 alone. (This is expected to increase quickly as costs keep rising.) On top of this, the Inflation Reduction Act gives incentives for purchasing healthcare plans on ACA Marketplaces, so Medicare gaining a larger portion of healthcare is highly likely - This should result in giving CVS access to a larger slice of the Medicare pie as well.

In addition to Medicare's steady growth, the Oak Street acquisition will assist in gaining the Medicare bonus back for CVS/Aetna. The Aetna National PPO had a lowered star rating from the Centers for Medicare & Medicaid ((CMS)). The drop from 4.5 to 3.5 reduced the "quality bonus payout" for Medicare in 2024. Estimates suggest this calculates to a loss of roughly $2B in 2024. Current guidance assumes this information and is still above expected 2023 numbers.

Oak Street's excellent ratings will now favor into future decisions - and of course, CVS will do everything it can to get the plan back into 4+ range - which allows for a nice bump in revenue when/if they get back the bonus. This bonus is not included in forward guidance. This is confirmed with an answer from the earnings call transcripts, as Shawn Guertin (CVS Executive Vice President and Chief Financial Officer) answered if the 2024 and 2025 numbers would be affected by the Oak Street deal…

"…specifically to your question about the timing of close, the answer is no, it would not change those. And arguably, it actually adds a little bit of lift because , if you remember, there is an operating loss that's going on for a little bit of time and you are picking that up a little bit deeper into the cycle of moving from kind of loss to breakeven to gain. So, it actually would not kind of change the $9 to $10 at all, certainly not in a negative way." ( Source . Emphasis added to reiterate, CVS expects the guidance numbers to be accurate without Oak Street.)

Finally, Oak Street will assist in focusing on giving great care upfront, which reduces costs down the road. This can assist in avoiding ER visits and expensive hospitalizations - something anyone with an interest in the funding for Medicare should be interested in. This gain is all from what is less than one year of CVS's Free Cash Flow.

Valuation...

Valuation can be given in many forms, but a company with a Forward PE Ratio of 10 is considered low, especially for a company expecting growth. Numerous authors will break down its value, but I follow growth and love paying value prices for it. Market comparisons can be an important deciding factor, and some comparisons are listed here.

Below is a quick list with Walgreens ( WBA ) and numerous other companies that CVS sometimes compares to. It is easy to see that CVS has great revenue, a strong and growing dividend and a relatively low stock price in comparison to peers. What becomes increasingly noticeable is that CVS's revenue is much stronger than other companies its size.

Author given list of financial data from Seeking Alpha (Source: Author compilation from Seeking Alpha)

{kind=link}

Another important note is that once each person's financial investment is considered, it is easy to see how CVS works out to a better deal per dollar spent. (By multiplying shares to reach a roughly equivalent dollar amount, things are easier to see.) CVS and Walgreens give the best dividend for roughly equal dollar amounts invested. However, the strong CVS revenue makes this a safe, sleep-well company to hold for the long term.

Author list of companies and financial data from Seeking Alpha (Source: Author compilation from Seeking Alpha)

{kind=link}

Going Forward...

- $25.2B has been repaid from the Aetna purchase and debt has been greatly reduced to a more reasonable level, especially when you consider Free Cash Flow.

- The $10B share repurchase program assists in gaining back half the $2 Billion loss expected in 2024. Signify is also expected to get that last one Billion back, any other increases are a bonus to the great forecast provided.

- Current EPS and RSI (43) numbers all fall into undervalued territory, especially in regards to the market as a whole.

- Most Signify and Oak Street growth is not listed in the forward guidance.

- The overall healthcare market is growing fast, as is Medicare's percentage of that market.

Even if the bullet points don't convince, CVS has clearly transformed itself into a strong overall healthcare company, as predicted years ago, with its acquisition of Aetna. At its most basic, Pharmacy drives income and Health drives people to the Pharmacy. Retail is mostly what folks will pick up while they are on-site or add to shippable orders. Finding attractive companies to add consumers CVS can access gives a great chance for increasing cash flow and growth… especially for a company that typically is very conservative in forecasting.

If you are looking for a safe stock for the future, a solid and growing dividend, in an industry that is nearly immune to recessions and benefits from inflation - CVS seems a great bet under $100.

For further details see:

Stop Playing Short Term With CVS