PSA - Storage Wars: May The Force Be With You

Summary

- I’ve always liked the self-storage business due to its low capex requirement and the somewhat sticky customer mindset.

- Perhaps I’m biased because as my wife tells me “I’m a pack rat” and I tend to keep everything.

- The larger REIT brands should be able to navigate the tempered cycle due to their strong balance sheets and technology enhancements.

- Let's take a closer look at four self-storage REITs and one bonus pick.

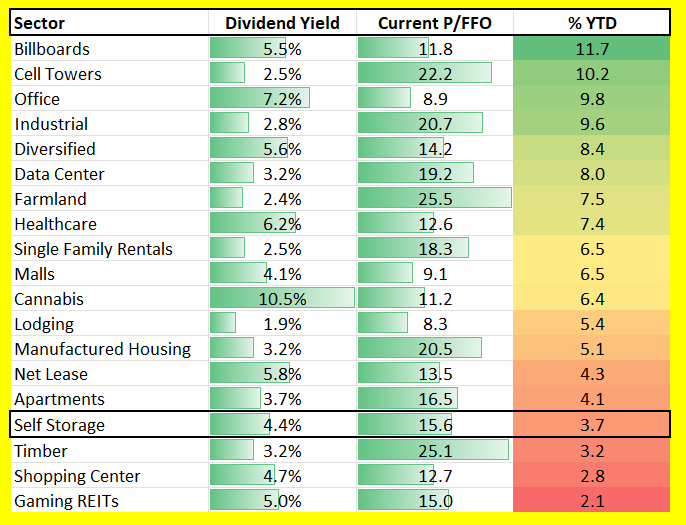

One of the great things about owning REITs is that the investor can gain access to many forms of commercial real estate. This way, he or she can design a REIT portfolio using a variety of sector allocations based on their unique risk profile.

Some sectors, like office, have become extremely cheap, but many investors aren't willing to place their hard-earned capital on hopes that the office market will eventually recover. Other sectors, like self-storage, have become attractive, although cyclical headwinds linger.

{kind=link}

Personally, I've always liked the self-storage business due to its low capex requirement and the somewhat sticky customer mindset.

Perhaps I'm biased because as my wife tells me "I'm a pack rat" and I tend to keep everything, although in her words, "most of the stuff belongs in the junk yard."

Although storage does have defensive demand characteristics, it's still a pro-cyclical, short lease duration business that could have further downside during what I believe will be a mild recession. This could make for a more challenged pricing environment over the next few quarters.

Not surprisingly, REIT acquisition activity has slowed after a solid start to the year with the market going through the price discovery phase as rates increased dramatically and credit has become scarce.

{kind=link}

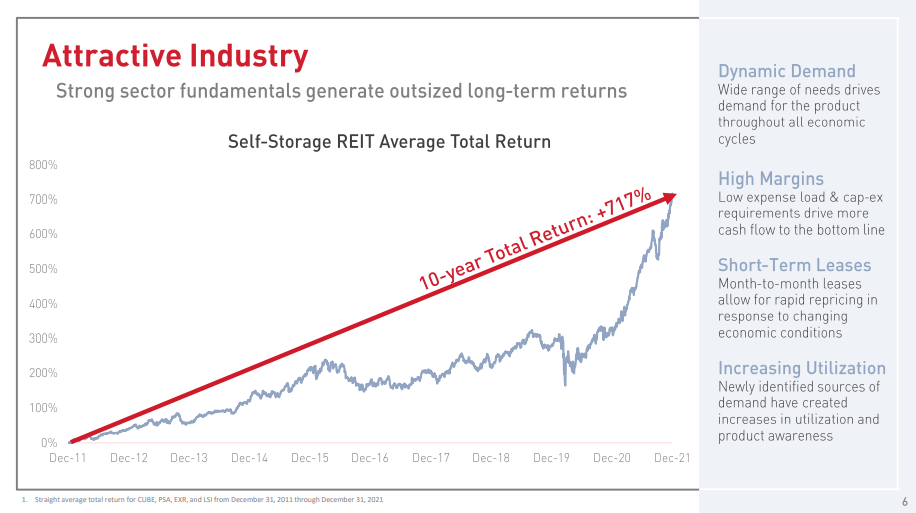

The self-storage industry has been in growth mode for quite some time, and the trend is not slowing down. A few years ago, the average self-storage space per capita was around six-square feet, but now it has risen to between 10 and 13 square feet. Basically, people are demanding more and more storage space.

The moving patterns during and after the pandemic also contributed to this upward trend. In the past 10 years, the average total return of a self-storage REIT has been a staggering 717%.

Currently, there's more than 1.6 billion square feet of self-storage space in the U.S., and more than 50 million square feet of space was added in 2022. About a third of Americans use self-storage space, and more than 2.4 million website searches are performed every month.

The fastest-growing markets by storage rate are Shelby, NC, Covington, GA, Clayton, NC, and Detroit, MI.

The four companies in this article (CubeSmart, Extra Space Storage, Public Storage, and National Storage) are the leaders in the industry, and they're all in a great position to take advantage of this upward swing in demand.

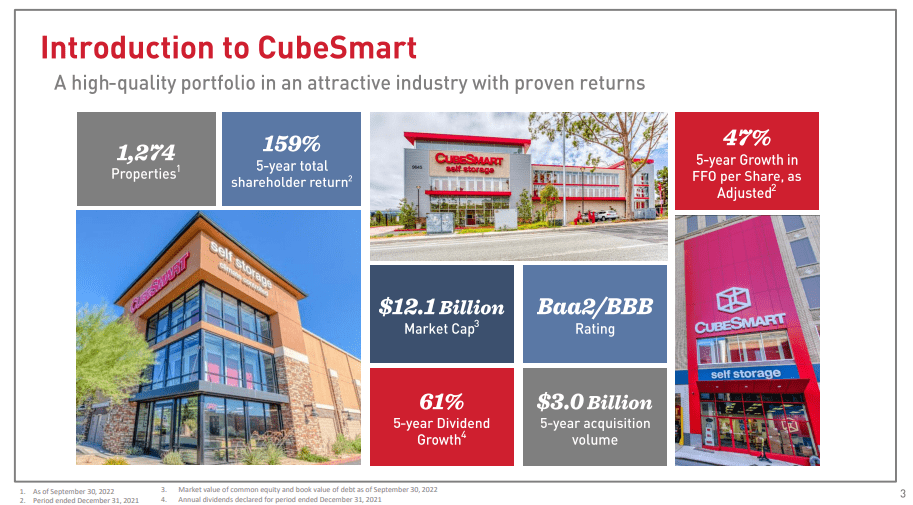

CubeSmart ( CUBE )

CubeSmart owns more than 1,200 properties, and they provide affordable and easily accessible storage space for residential and commercial customers.

Through their high-quality investment and strong operation, their footprint has been growing, and shareholder return has been strong in the past several years. CubeSmart acquired properties worth of $3.1 B since 2017, and they're located in areas with strong demographics.

{kind=link}

CubeSmart has very strong financials. The net debt to EBITDA is at 4.4x, and debt to gross asset ratio is at 37.7%. The EBITDA coverage ratio is at 7.0x.

Also, they have plenty of liquidity available and good access to capital. The remaining capacity on their revolving credit facility is $664 M, and they have shown their access to capital by raising more than $6 B since 2010.

The debt maturity schedule shows that CubeSmart is doing a good job at managing the debt.

CubeSmart's dividend is safe at this point. The cash dividend payout ratio of 65.05% and FAD payout ratio of 61.04%, both demonstrating the safety of the dividend payment. Given their AFFO growth rate in the past five years is at 9.67% per year (five-year CAGR), I expect they will have no problem in raising their dividend in the future.

Extra Space Storage ( EXR )

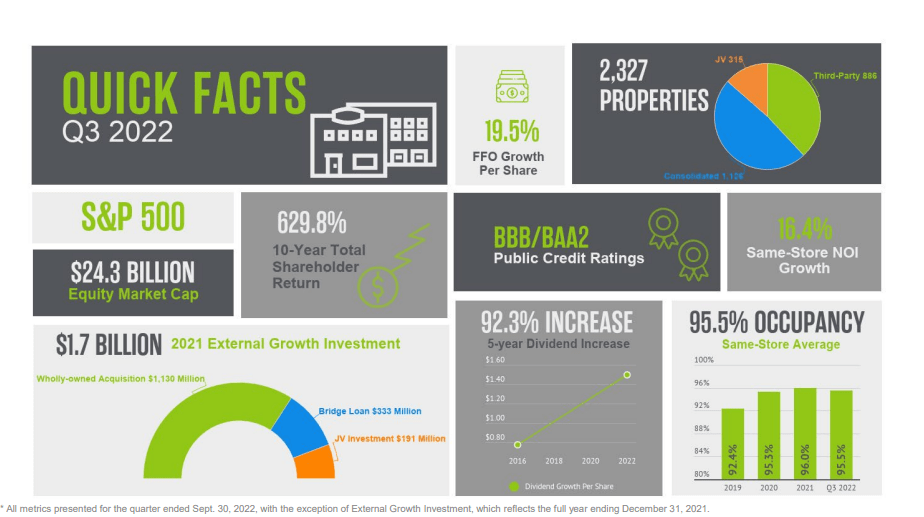

Extra Space Storage is a self-administered and self-managed REIT that owns and operates more than 2,300 self-storage properties.

They have been growing at a fast pace in the past several years, and their properties are in high demand. The average occupancy rate of their units are 95.5%.

{kind=link}

Diversification and scale are definite strengths for Extra Space Storage. They have more than 175 million net rentable square feet and 1.6 million units in their portfolio. They operate in 41 different states, and they have more than 4,000 employees.

Extra Space Storage has a strong balance sheet to support growth plans. They have $1.4 B revolving capacity, and the net debt to EBITDA is at 4.6x. The interest coverage ratio is 6.7x, and fixed charge ratio is at 6.2x. The weighted average interest rate is at 3.6%.

The dividend growth of Extra Space Storage has been very strong. The dividend increased by 650% in the past 10 years, and 92.3% in the past five years. The safety of dividend payment is still solid at this point. The cash dividend payout ratio of 67.05% and FAD payout ratio of 61.71% shows that there is a substantial cushion between cash flow and dividend payout.

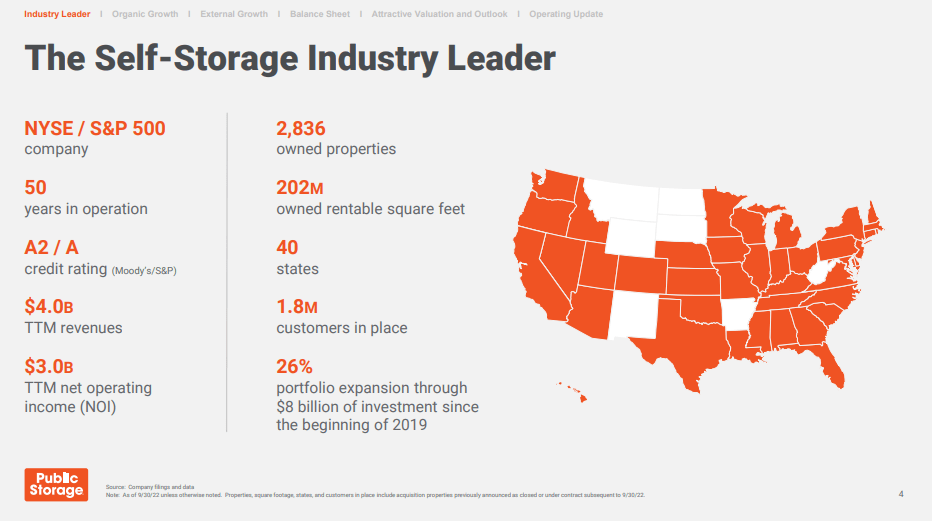

Public Storage ( PSA )

Public Storage acquires, develops, owns, and operates self-storage facilities. They offer storage spaces for lease on a month-to-month basis for personal and business use. Public Storage has a strong portfolio with over 2,800 properties and 202 million square feet of rentable space. They have a presence in 40 different states.

{kind=link}

Public Storage has a strong balance sheet. The net debt plus preferred equity to EBITDA ratio is at 3.3x. About $6 B of preferred equity has been refinanced since 2015, and $7.4 B of debt was issued at a very low 1.7% blended rate. This strong balance sheet and favorable capital structure will bring strong growth to Public Storage's portfolio, and dividend growth will naturally follow. It's not surprising to see the strong credit rating of A2 (Moody's) and A (S&P).

The dividend payout is very safe at this point. The cash dividend payout ratio is at 50.91%, and FAD payout ratio is at 59.78%.

With a strong portfolio and solid operating capacity, I have little doubt that Public Storage will keep on growing and shareholders will be rewarded in the future.

National Storage ( NSA )

NSA has grown its platform substantially since it was formed (in 2013) and currently boasts a portfolio of over 1,100 properties (915 wholly owned and 185 JVs) and over 71.5 million square feet (around the same size portfolio as UHAL).

NSA has a unique structure called PRO that essentially serves as regional property managers for NSA's contributed properties and directly contributes to the potential upside of those properties, while simultaneously diversifying their upside in the broader portfolio of self-storage properties.

This structure provides NSA with a competitive growth advantage over self-storage companies that do not offer property owners the ability to participate in the performance and potential future growth of their contributed portfolios.

NSA Investor Deck

NSA also has a strong balance sheet, rated BBB+ by Kroll with solid credit metrics:

NSA Investor Deck

During Q3-22 NSA closed on a $200 million 10-year unsecured debt private placement with a fixed rate of 5.06%. At quarter end, the leverage was 6.0x net debt to EBITDA, right in the middle of the targeted range of 5.0x and 6.5x.

In Q3-22 , NSA delivered a solid quarter, with growth in core funds from operations ("FFO") per share of 26.3% and same-store NOI growth of 12.1%. Like other peers, results continue to moderate as operators face tougher year-over-year comps and a return to more normal seasonality.

So, in Q3-22, NSA reported core FFO per share of $0.72, which represents an increase of 26% over the prior year period. As the CFO explains:

"This continued robust year-over-year growth was driven by a combination of double-digit same-store growth and our healthy acquisition volume over the past four quarters."

NSA Investor Deck

NSA's Q3-22 same-store NOI increased 12.1% over last year, driven by a 10.7% increase in revenue combined with a 6.9% increase in property operating expenses. The contract rates were up 15% in Q3-22 from the prior year, while street rates were up 10% year-over-year.

Same-store occupancy averaged 94.1% for Q3, down 240 basis points compared to 2021. NSA ended Q3 with a same-store occupancy of 92.6%, down 350 basis points compared to the prior year.

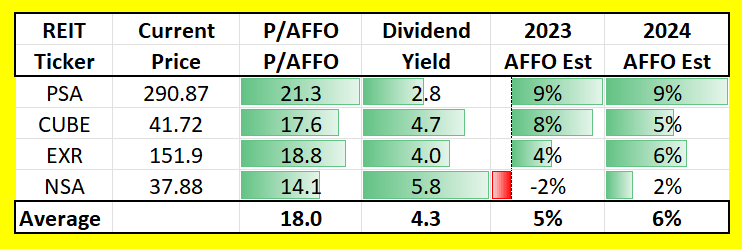

NSA is trading at the lowest P/AFFO multiple (14.1x) and the highest dividend yield (5.8%) in the peer group. NSA has the widest margin of safety in our self storage coverage spectrum, and we maintain a Spec Buy rating.

In Closing

As viewed below, Self-Storage total returns have outperformed all other equity REIT sectors for 28 years while experiencing the least volatility:

NSA Investor Deck

This chart below provides another snapshot illustrating the fact that the self-storage sector has optimal risk-adjusted returns:

NSA Investor Deck

One of the main growth drivers for self-storage facilities in the past couple of years was the nomadic lifestyle induced by the pandemic.

As more people were moving away from metropolitan areas, the demand for self-storage facilities sharply increased. Also, increased interest and preference for working from remote areas positively contributed to the need of self-storage facilities.

But as people return to the office, and more employers are requiring people to work physically from office, the growth rate that we've been seeing in the past couple of years in the sector may not continue in the future.

As the Federal Reserve maintains a high interest rate, the mortgage rate has also become much higher and the real estate market has been struggling.

During times like this, the gaps between buyers' bids and sellers' asks tend to get larger, and the transaction volumes go down. This might make it harder for the companies to execute their growth plan in the short term.

During the financial crisis REITs lost -210bps in average occupancy (4Q07-4Q09) and we suspect that the sector will lose some occupancy (around 150 bps) during the likely 2023 mild recession.

Yet, the larger REIT brands should be able to navigate the tempered cycle due to their strong balance sheets and technology enhancements.

{kind=link}

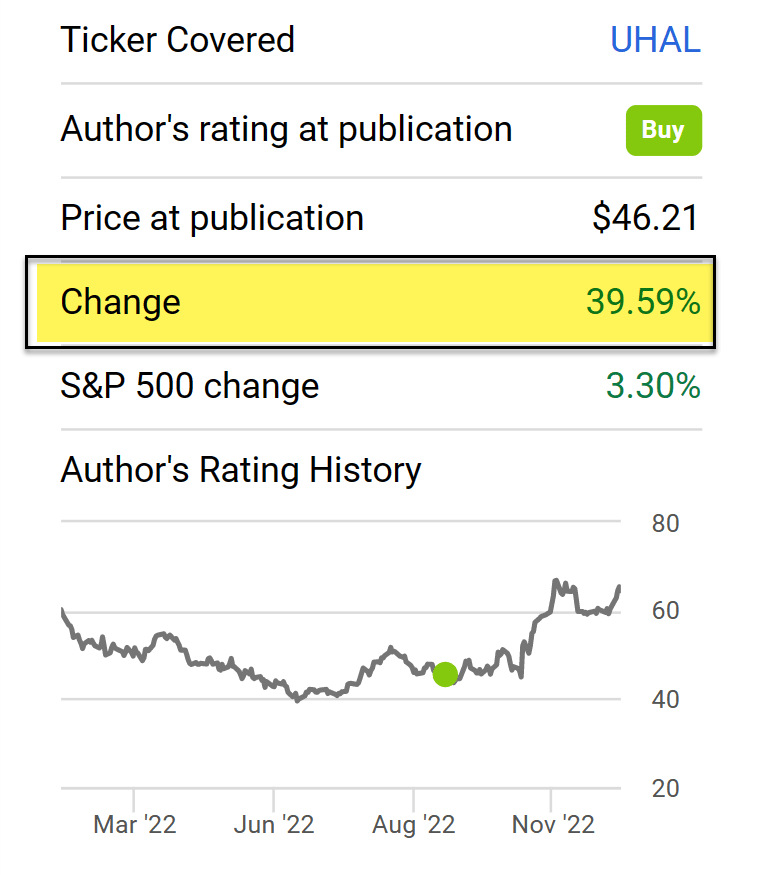

On Sept. 19, 2022, we published an article on U-Haul ( UHAL ) in which we explained

UHAL generates around $700 million in annual revenue from its self-storage business, compared to these REIT comps:

- Public Storage: $3.9 Billion

- Extra Space: $1.8 Billion

- CubeSmart: $920 million

- National Storage: $700 million

Although UHAL is structured as a C-Corp. (not a REIT) we initiated a Strong Buy and I personally added shares to my portfolio ( shares +39.6% since my article ).

{kind=link}

For further details see:

Storage Wars: May The Force Be With You