NTST - STORE Capital: Netstreit Could Be A Great Replacement

Summary

- Understandably many investors were disappointed with the acquisition of STORE Capital, which was a very popular REIT.

- While much smaller, NETSTREIT shares many characteristics with STORE Capital, making it a replacement option worth considering.

- The three things that they have in common are a focus on uni-level profitability and real estate merits, defensive portfolios with high-occupancy and e-commerce resistant tenants, and reasonable valuations.

A lot of investors were disappointment by the acquisition of STORE Capital ( STOR ) despite it being at a premium to the price at which it was trading when the acquisition was announced. This is understandable given that despite the premium the acquisition was done below what many investors considered fair value, and the solid dividend provided by STORE was much appreciated. In any case the acquisition is going to be completed soon, and investors have to decide where to reinvest the proceeds.

We believe an excellent candidate for a replacement REIT to consider is NETSTREIT ( NTST ). This is a small REIT that had its IPO in 2020, and despite being at a much earlier phase of its corporate life, it shares many important characteristics with STORE. In addition to both being focused on net-leased properties, they share similar underwriting strategies. If one thing separated STORE from many other similar REITs, it was their singular focus on unit-level profitability. This allowed the REIT to acquire properties at relatively high cap rates and still experience good operating performance. Similarly NETSTREIT puts a lot of attention on the unit-level economics and aims to have its properties rank in the top half of its tenant’s store portfolio in terms of profitability. Another similarity: they both focus on e-commerce resistant tenants with high economic resiliency. This has resulted in very high occupancy levels. The third similarity is that both are trading at similar valuations, although STORE's dividend was higher. Understandable, given that NETSTREIT is currently focused on building its portfolio.

Underwriting Strategy

STORE Capital used to say that most REITs focused on corporate credit quality and real estate value, but a third element that few others focused on was unit-level profitability. STORE's focused approach on acquiring profitable locations gave it its name: single tenant operational real estate (STORE). STORE firmly believed that profitability at the property level improved the credit profile of its portfolio and had 99% of locations subject to unit-level financial reporting. It boasted a 4-wall 4.7x weighted average fixed-charge coverage ratio (FCCR).

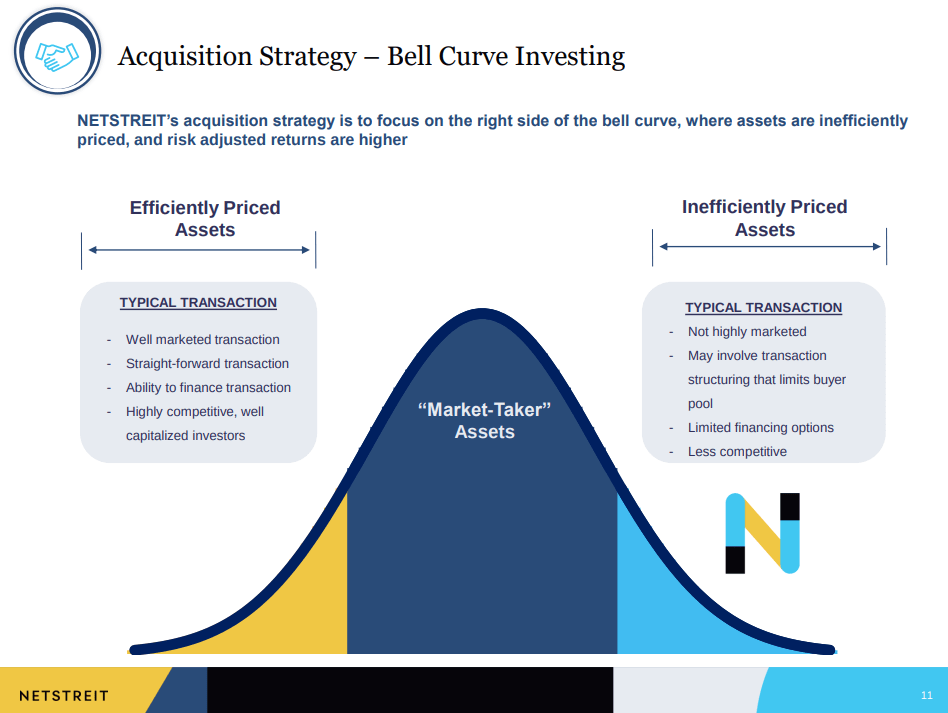

Similarly NETSTREIT seeks a rent coverage of minimum 2x, and assesses a property relative to both corporate stability but also the real estate merits. It takes into consideration the fungibility of the building for alternative uses, its replacement cost, and performs a location analysis. This type of analysis includes traffic counts, nearby uses and traffic drivers, accessibility, parking capacity, etc. It also aims to have properties that rank in the top half of a tenant's store portfolio. Given that properties with high-quality tenants are expensive, NETSTREIT focuses on smaller less marketed transactions to be able to still obtain attractive cap rates. They call this "Bell Curve Investing": they focus on transactions that are not highly marketed and may involve structuring that limits the buyer pool.

NETSTREIT Investor Presentation

{kind=link}

Property Types

Thanks to its high-quality, diversified, and defensive net lease retail portfolio STORE boasted of occupancy levels above 99%. A lot of its properties were focused on restaurants, education, manufacturing, and other e-commerce resistant purposes.

STORE Capital Investor Presentation

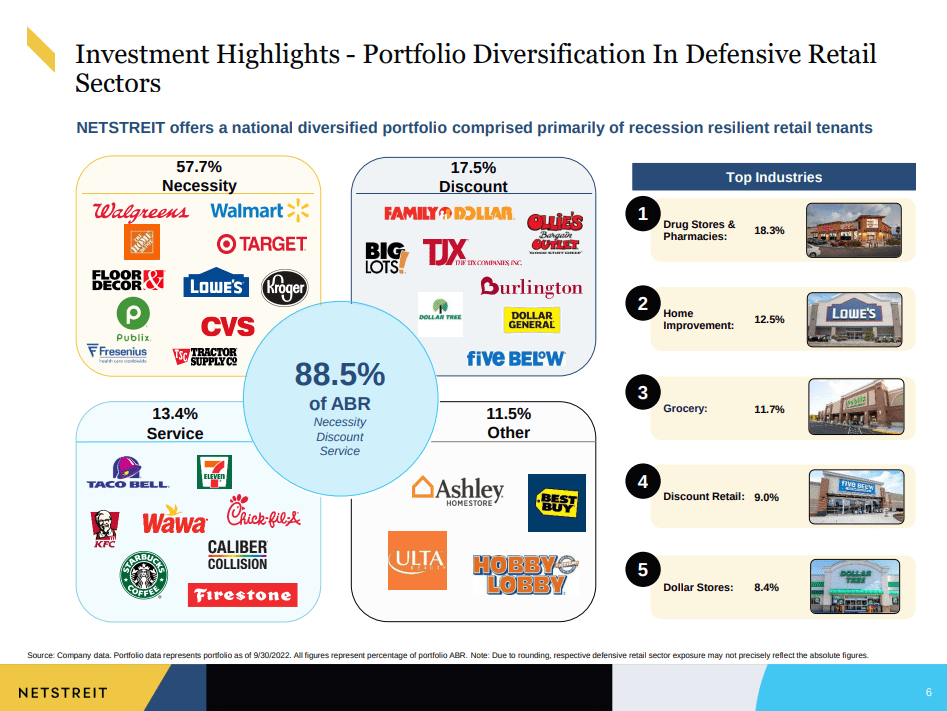

NETSTREIT also has an impressive occupancy level, having maintained 100% occupancy since its IPO. It likes to boast that its high-quality tenants create bond-like leases with high rent collections during times of disruption. One difference between STORE and NETSTREIT is that the latter gives more importance to the investment credit rating of its tenants, with 78% of its portfolio consisting of investment grade tenants, or tenants with an investment grade profile. Importantly, 88.5% of its annual base rent comes from tenants focused on necessity products, discounted products, or services. The top industry for NETSTREIT is drug stores & pharmacies, reflecting this focus on e-commerce and recession resistant tenants. Management has shared that their investment criteria since they formed the company back in 2019 was that they wanted to focus on tenancy that does very well in any economic cycle.

NETSTREIT Investor Presentation

{kind=link}

Growth

Given its smaller size, and that it is still in the process of leveraging up, we believe NETSTREIT can offer superior growth to what STORE was delivering. In its last few years STORE delivered adjusted FFO growth of ~5.9%. This was far from spectacular, but combining AFFO growth and the high dividend provided investors with a very decent return.

STORE Capital Investor Presentation

{kind=link}

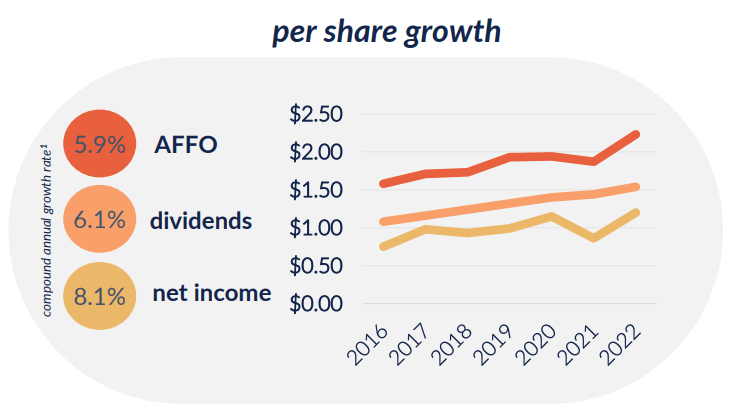

In the last year, NETSTREIT's FFO per share has gone from ~$0.90 to ~$1.13, which translates to higher than 20% growth. This is very high and will likely decelerate going forward, but we believe will remain stronger than what STORE was delivering.

Balance Sheet

NETSTREIT is still in the process of leveraging up its balance sheet, but it is getting closer to being fully leveraged. Its financial debt to EBITDA is still meaningfully lower than that of STORE, and at what we consider still a healthy level.

Valuation

The last dividend STORE paid was a quarterly dividend of $0.41, which at the current share price represents a ~5.1% annual dividend yield. NETSTREIT pays a quarterly dividend of $0.20, which at current prices represents a ~4.2% dividend yield. While a bit lower, we believe NETSTREIT will probably start increasing its dividend once it believes its initial portfolio building is complete. In terms of price to funds from operations both companies trade at similar valuations.

Risks

The main risk we see with NETSTREIT as a replacement option for STORE Capital is that STORE had a more significant trading history, while NETSTREIT is relatively new and still has to prove itself to the market. Still, we believe both companies have solid defensive strategies that make them less risky compared to other REITs. For investors interested in REITs with a much longer history, other potential replacements worth considering include Realty Income ( O ) and W. P. Carey ( WPC ).

Conclusion

We understand the disappointment that many investors experienced when STORE was acquired. A beloved high-dividend yield investment has been taken away from the market. Still, there are good potential replacement options. One that we believe is particularly attractive is NETSTREIT, which shares many characteristics with STORE Capital. The three things that they have in common are a focus on unit-level profitability and real estate merits, defensive portfolios with high-occupancy and e-commerce resistant tenants, and reasonable valuations.

For further details see:

STORE Capital: Netstreit Could Be A Great Replacement