STPZ - STPZ: TIPS Close To A Buy Zone At Much Higher Yields Than Before

2023-04-28 10:39:35 ET

Summary

- If inflation remains high and bonds rally, STPZ could win both ways.

- I feel strongly that continued high inflation is inevitable, and short-term bonds are the most attractive part of the yield curve now. That makes STPZ one to track.

- I rate STPZ a Hold, but this is a prime upgrade candidate once the current market obsession with the Fed fades.

Elevated inflation and an uncertain market outlook have led me to consider The PIMCO 1-5 Year U.S. TIPS Index ETF (STPZ). STPZ offers some inflation hedging benefits, with lower interest rate risk and lower volatility than a longer-duration TIPS ETF. However, I think the worst of rate hikes is behind us and if bonds rally and inflation remains high I would prefer to invest in a longer-duration option. I rate STPZ a Hold.

TIPS: A quick introduction or re-introduction

Low inflation has rendered TIPS largely irrelevant to investors for a while, and there is limited coverage of this space on research platforms, so here's a quick overview of this off-beat but useful asset class, now returning to investors' radars.

TIPS are well known for their inflation protection. After all, it is in the name. TIPS pay a semi-annual coupon that is a fixed percentage of the principal value of the bond. The principal value is pegged to the Consumer Price Index (the full version, not the "core" subset of CPI), and is adjusted up and down with inflation and deflation.

When the principal value is adjusted upwards, it is considered income but not distributed until maturity. This creates "phantom income" as it generates taxable income but investors don't receive any cash. With deflation, the principal value is adjusted downward, but losses are capped if held to maturity as the investor never receives less than the original principal amount.

TIPS ETFs are not the same as owning TIPS bonds directly!

Now TIPS ETFs, such as STPZ, are a different story. A TIPS ETF has no time to maturity. STPZ invests in 1-5 years US inflation-linked treasuries, but the ETF will not mature like the underlying holdings will. So, the downside protection provided by an individual TIPS is lost, since there is no guarantee to see a full return of the principal in a TIPS ETF. However, STPZ's very short maturity range gives it a decided advantage over longer-maturity TIPS funds on this issue.

Countering the lack of a firm maturity date is the ease of trading and tax efficiency of TIPS ETFs like STPZ. It pays a monthly distribution, instead of a semiannual distribution like its underlying securities. STPZ's monthly distribution accounts for accrued income and any inflation adjustments. This eliminates so called "phantom income," or the taxable investment gain that has not yet been realized, as the inflation adjustments are actually paid out. This may make holding a TIPS ETF more tax efficient than a TIPS in taxable accounts (but as I am not a tax advisor, any TIPS investor should check with their accountant about their own tax situation).

However, it is important to note that what goes up can also come down. Deflation causes the principal value to be adjusted downward resulting in a reduced or no monthly dividend. This is essentially a "floating" return feature of TIPS that factors into the evaluation of STPZ.

Blackrock

Strategy Analysis

The PIMCO 1-5 Year U.S. TIPS Index ETF invests in short-term US TIPS and is indexed to the ICE BofAML 1-5 Year US Inflation-Linked Treasury Index.

STPZ invests in US TIPS with maturities between 1 and 5 years and currently has an effective duration of 2.8 years. STPZ currently holds 21 holdings and weightings are based on a representative sampling strategy. This means STPZ may not track its index as accurately as ETFs that replicate the composite and weighting of their indices. However, STPZ's indexing method aims to lower portfolio turnover costs relative to actively managed ETFs.

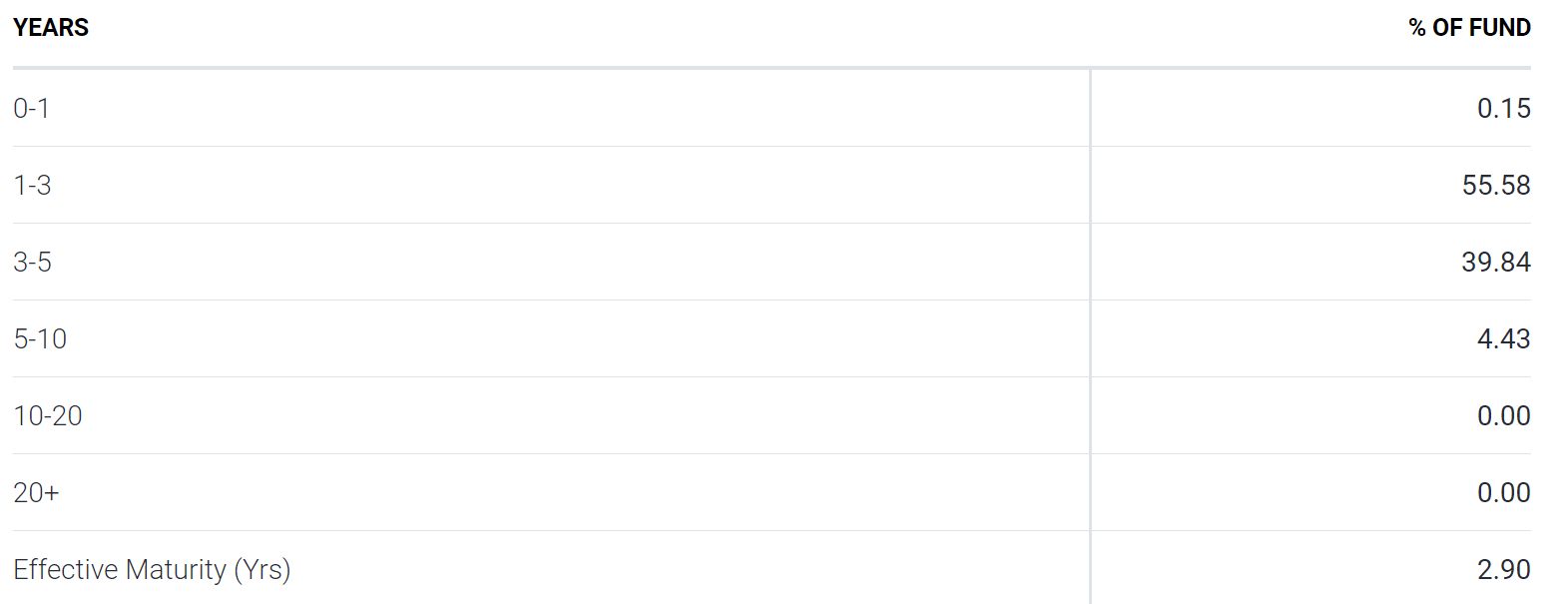

STPZ's Maturity Distribution

{kind=link}

2022 was a poor year for STPZ; here's why

Intuitively, a year of sharply rising inflation would seem to benefit TIPS. However, despite 2022's high inflation, STPZ had a negative return of -4.5%. This was due to the increased interest rates having a greater impact on STPZ's underlying securities than the adjustment for inflation.

Credit market conditions have been challenged over the last year. The Fed began its rate hiking spree in March 2022 and financial market indicators worsened. However, the banking crisis may cause the Federal Reserve to stop hiking rates sooner than previously expected, potentially benefiting STPZ. I see 2022 as a historical "perfect storm" for STPZ, and as such, it essentially took a year for this ETF to get into position to finally be useful again. But now it's there, or at least very close to being there, which prompted my first report on the TIPS space. STPZ's 2.6% return through the first ? of 2023 is evidence that the adjustment period of 2022 is in this ETF's rear-view mirror.

Current bull case

A goldilocks scenario for TIPS is for inflation to remain elevated but with enough recessionary concerns to keep the Fed from hiking rates. The Fed's preferred inflation gauge, the personal consumption expenditures (PCE) price index, remains at 5.0% as of the latest release in February. Well above the Fed's target of 2%. Inflation seems to be here to stay. Furthermore, the risk of a US recession is up to close to 60%.

Breakeven inflation rate: a key determinant of STPZ's attractiveness

TIPS will perform better than Treasury bonds if inflation is higher than what the market anticipates. If inflation is below market expectations, TIPS will perform worse than Treasury bonds. The breakeven inflation rate, or difference between the yield of a nominal Treasury and the yield of a TIPS with similar maturity, is essentially the hurdle rate for investing in TIPS instead of a Treasury. TIPS outperform their nominal Treasury counterparts when the breakeven rate averages (or exceeds) inflation over the life of the TIPS.

Currently, the breakeven inflation rate for a 5-year TIPS is at 2.3%. This means CPI inflation only needs to average greater than 2.3% over the next five years for the TIPS to outperform a five-year Treasury. On the other hand, if CPI inflation averaged less than 2.3% TIPS would underperform. For better or for worse, I don't see inflation coming down to 2.3% within the next few years. The Fed talks tough about getting inflation to their "2% target," but that may go the way of "transitory" inflation talk from last year. In other words, I believe it is just Fed speak, and is unlikely to happen any time soon.

STPZ has an effective duration of 2.8 years. This shorter maturity has historically had less interest rate risk, a higher correlation to inflation, and lower volatility than a longer-duration alternative. The spread between STPZ's total return and price is near an all-time high. The difference between the two is STPZ's interest rate. While STPZ's yield has pulled back a bit this year off its all-time high, it remains elevated.

Current bear case

As was the case in 2022, if interest rates rise enough where a TIPS's price declines offset the CPI inflation adjustment, total returns can be negative. Furthermore, if inflation doesn't rise as high as expected, STPZ will likely underperform.

STPZ's estimated yield to maturity is 4.16%. This is not competitive in the current environment where many savings accounts yield upwards of 4%. But these savings accounts obviously do not adjust with inflation and their rates can be cut at any time. That makes STPZ a very competitive alternative, provided the risks and quirks are understood by the buyer.

STPZ is a low-risk / low-reward defensive investment. If the market were to rally, STPZ would underperform.

Current investment opinion

While I believe TIPS ETFs can provide meaningful diversification and inflation protection, I would like to be further out on the yield curve than STPZ. My rationale for this preference is my apprehension about a possible recession coupled with inflation that is moving lower fairly slowly. That limits my rating to a Hold for now.

For further details see:

STPZ: TIPS Close To A Buy Zone, At Much Higher Yields Than Before