STRA - Strategic Education: Turning Bullish On Higher Enrollments

2023-12-26 05:07:25 ET

Summary

- Strategic Education Inc. released a 113-slide presentation outlining its strategic planning, segment results, and future outlook.

- The company's main challenge has been sustaining and growing student enrollments, but recent data shows enrollments are starting to increase again.

- Strategic Education provided 2024 guidance and outlined its 5-year plan to achieve transformational operating performance.

Strategic Education Inc. (STRA) released its Investor and Analyst Day 2023 presentation on November 7, 2023. It's 113 slides long and outlines the business regarding its strategic planning, segment results, and future outlook. This presentation is actually the most information-rich source I've come across since I started coverage on the company more than a decade ago when shares were trading below $40. Overall, I've been bullish on the company, as I've thought that management was among the best in the for-profit education industry. Strategic Education's main challenge has been sustaining and growing its student enrollments. It's made business changes to achieve that goal including making tuition more affordable and providing better post-graduation employment outcomes. Over the years, Strategic Education has driven revenue growth in two primary ways: organically developing its corporate-affiliated accounts and acquiring other education companies. Collectively, Strategic Education operates three segments:

- U.S. Higher Education "USHE" (Strayer University & Jack Welch Management Institute, Devmountain, Hackbright Academy, and Capella University)

- Education Technology Services "ETS" (Enterprise Partnerships, Sophia Learning, and Workforce Edge)

- Australia/New Zealand "ANZ" (Torrens University, Think Education, and Media Design School)

For those who are new to the company, its operations are located in the U.S. and Australia/New Zealand and management's goal is to deliver better outcomes for students and employers, as shown on slide 13 of its investor presentation:

Strategic Education Slide 13 (STRA's Investor Presentation)

{kind=link}

Strategic Education experienced a difficult period of shrinking enrollments between 2020 through 2022. However, during 2023, student enrollments began to increase again. For context, the U.S. Higher Education segment represents the bulk of revenue at 70+%, Education Technology Services at 20+%, and Australia New Zealand at ~6%. Importantly, Strayer University is expected to show 6% growth from 35K students to 37K in 2023.

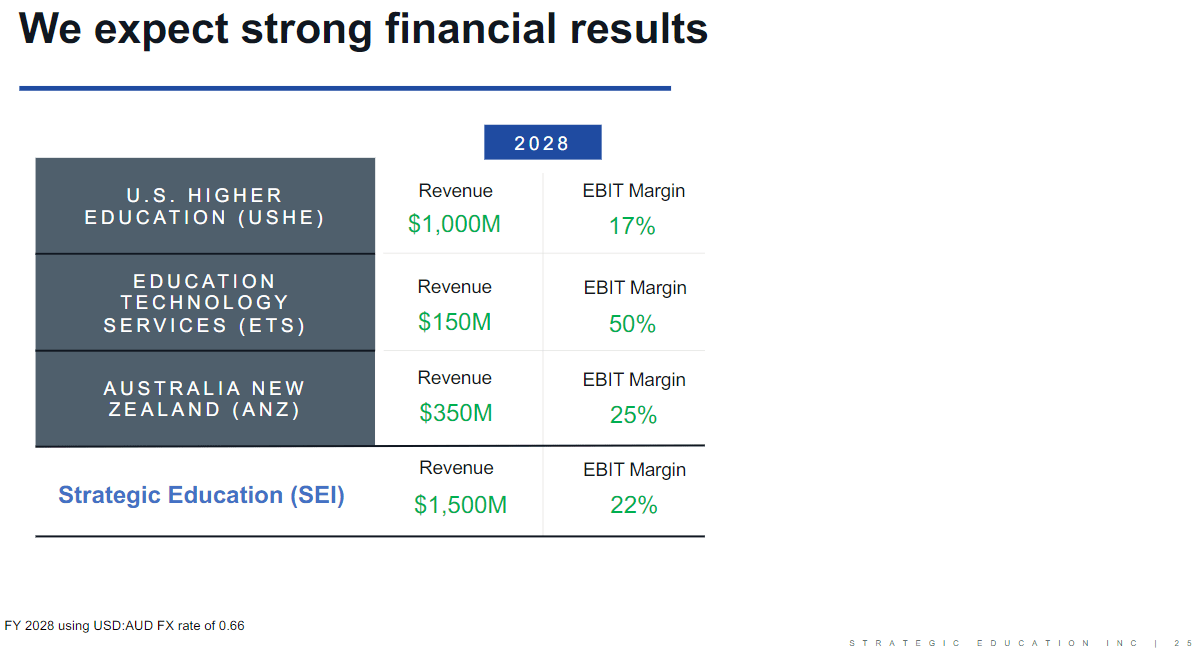

Strategic Education provided 2024 guidance that shows consolidated revenue growth will be between 4-6%. USHE enrollment growth will be around 4-6%, ANZ will be 3-4%, and Sophia subscription growth will be 15-20%. Management's 5-year plan for USHE, ANZ, and Sophia is to have growth of 4-6%, 6-8%, and 16-18%, respectively. So what does that look like long-term? Management was kind enough to provide an idea of what they hope to achieve regarding sales and operating margins by 2028:

Strategic Education Slide 25 (STRA's Investor Presentation)

{kind=link}

How does that compare against today? Consolidated revenue is currently trending around $1.1 billion and EBIT margins are depressed at 7.4%, primarily given poor enrollment trends in the last few years (i.e. a lack of operating leverage) and other investments made up until now. For example, disclosures stated instructional and support costs (salary increases, technology costs) as well as G&A expenses (branding initiatives and brand ambassadors partnerships) have increased. That said, Q3 2023 was the first quarter in over three years where both revenue and EBIT margins sequentially improved.

Strategic Education in currently generating TTM operating profit of about $81 million. There's potential that Q3 was the first period of stabilization and where we could see incremental improvement. Looking to 2028, $1.5 billion in revenue with consolidated EBIT margins of 22% would generate about $330 million. Effectively, management's goal is to increase operating profits by 3x over the next 5 years. That would make the business incredibly cheap today given its enterprise value of $2.15 billion, or 6.5x 2028 EBIT.

Obviously the challenge is whether Strategic Education can meet its guided targets. Granted 2023 is a clear turning point for the company, I don't see how or why all three segments would steadily grow enrollments year after year over the next five years. Remember that Strayer Education's total enrollments trended down from 51K to 37K, or a decline of 27.5%, between FY19 and FY23. That wasn't a linear downtrend either, but my point is that enrollment trends experience hiccups and I'm willing to bet that it will be a bumpy road leading up to 2028, and investors should adjust their expectations accordingly.

What's good for USHE enrollments is that employer affiliated enrollments are proportionally increasing up from <20% in FY20 to 28% in FY23. In general, these enrollments drive higher enrollment performance. In the Q3 2023 conference call , management outlined this trend:

Overall demand in the US remains very strong, and both Strayer and Capella universities continue to have healthy new student growth, driven predominantly by increases in our employer affiliated enrollments, which, I believe, our owners know is one of our key strategies. Total employer affiliated enrollment grew 21%, which was more than twice the overall growth rate. Employer affiliated enrollment is now 28% of all US Higher Education enrollments, which is up 250 basis points from last year and nearly double what it was four years ago. Finally, student retention remained stable with our trailing one-year persistent rate at 87.3%. "

At this proportionally increases, USHE's existing and new enrollment trends should improve. If we run out this trend linearly, employer affiliated enrollments should represent approximately 45% of all USHE enrollments by FY28, which would be excellent outcome.

The final point I'll make on the business itself is that management has finally had time to get past the COVID pandemic and integrate all of its acquisitions (which involved a lot of time, effort, and restructuring costs). Now management can focus more so on driving enrollments and cost discipline.

Addressing Valuation

I'm directionally bullish on the stock given that Strategic Education is certainly executing on its enrollments and management anticipates that they will continue doing so over the long term. Whether they can achieve their FY28 targets is another story. I think the for-profit education industry is not easy and there are forces outside management's control that can adversely affect enrollment trends. Both should be considered.

Currently, the company sells for ~27x TTM EBIT and management's 2028 targets would put the stock at 6.5x EBIT. That's a very wide range. But I think there's a floor in the stock since that multiple will be steadily decreasing.

Compared to the Street, analysts expect that EPS will stairstep up from $2 today toward $5 over the next few years. If you work out the math regarding the company's net interest expenses of $8 million and effective tax rate of 30%, that's broadly in-line with management's guidance.

I strongly believe the company will keep executing, but guiding for such a linear improvement of enrollments and earnings will be interesting to watch. It makes for an easy setup to miss analysts' consensus estimates.

Bottom Line

Count me back in the bull camp, especially with Strategic Education providing so much detail on their long-term plans to achieve sustained growth and tremendously higher operating margins. The Q3 2023 quarter was certainly an improvement, quite possibly a P&L turning point, and so I'll be watching with a closer eye heading into 2024. That said, investors should remain watchful for a slowdown in enrollments in any of the three segments, especially in USHE. Thanks for reading and please comment below.

For further details see:

Strategic Education: Turning Bullish On Higher Enrollments