SAUHF - Straumann: Expect Double-Digit EBITDA Growth In 2024 And 2025

2023-12-26 23:11:38 ET

Summary

- Straumann Holding has reported a robust financial performance in 2023, with organic growth rate of 7.5% and a gross margin of over 900M CHF.

- The company's net profit was 206M CHF, with an underlying EPS of 1.43 CHF per share.

- Straumann remains on track to meet its guidance of high single-digit organic revenue growth and an EBIT margin of 25%. However, the stock is trading at a premium valuation.

Introduction

Straumann Holding (SAUHF) (SAUHY) is a leading company in the orthodontics and tooth replacement 'sector'. The company has a worldwide presence and thanks to this presence and its sought-after products, the stock has been trading at a premium valuation for as long as I can remember . That being said, I do like the sector it is operating in and its leadership, so I am keeping an eye on its financial performance.

{kind=link}

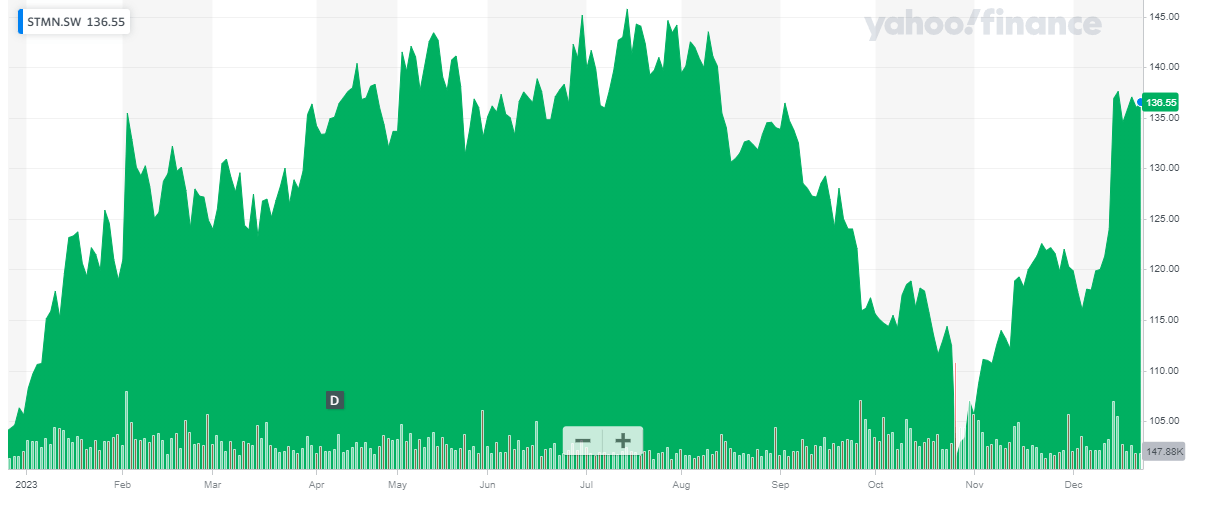

Straumann has its primary listing is in Switzerland where the stock is trading with STMN as ticker symbol. The average daily volume is approximately 290,000 shares. As Straumann's shares trade in Swiss Francs and the company also releases its results in Swiss Francs, I will use the CHF as base currency throughout this article.

A robust performance so far in 2023

Straumann only publishes detailed financial statements on a six monthly basis and the financial markets are kept up to date with trading updates on a quarterly basis. In this article I will first have a look back at the H1 results before seeing how the company performed in the third quarter of the current financial year.

{kind=link}

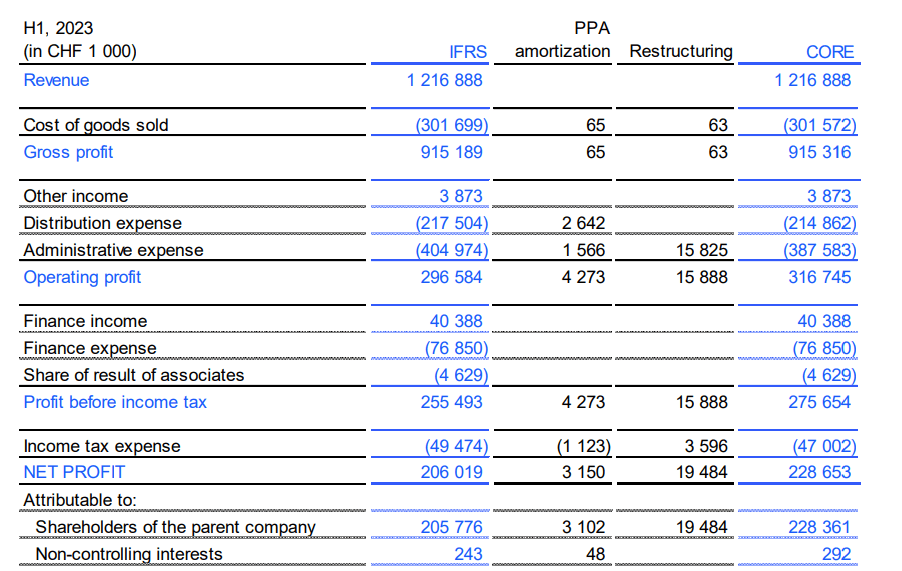

In the first half of 2023, Straumann reported a total revenue of just over 1.2B CHF , representing an organic growth rate of 7.5%. The company's gross margin remained exceptionally strong at in excess of 75%. As you can see below, Straumann generated a gross profit of in excess of 900M CHF on the 1.217B CHF in revenue.

{kind=link}

Of course, the operating profit is substantially lower as Straumann's distribution and G&A expenses are relatively high but with an operating profit of 297M CHF on an IFRS basis and 317M CHF on an underlying basis, the company's performance remained exceptionally strong.

The image above also shows the net profit was 206M CHF of which 205.8M CHF was attributable to the shareholders of Straumann and looking at the core results, the net attributable income was just over 228M CHF which represented an EPS of 1.43 CHF per share.

The EBITDA on a reported basis in the first semester was approximately 366M CHF while on an adjusted basis, the EBITDA was slightly higher at almost 376M CHF.

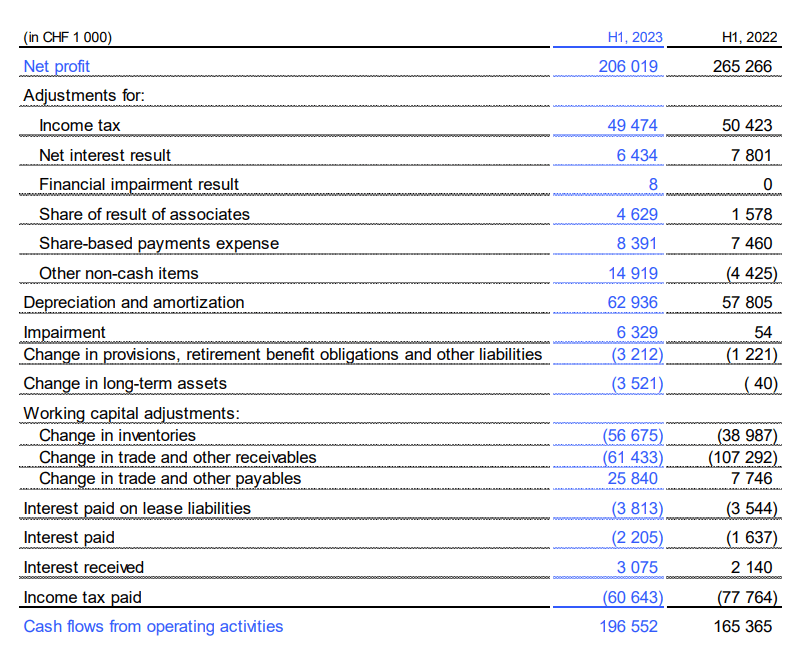

The company reported an operating cash flow of almost 197M CHF in the first half of this year, but this includes a net working capital investment of approximately 92.3M CHF. Additionally, Straumann paid almost 61M CHF in cash taxes although only 49.5M CHF was due based on the H1 income statement. This means the underlying operating cash flow was actually 300M CHF.

{kind=link}

From that 300M CHF, we should also deduct the 13M CHF in lease payments and cash payments to non-controlling interests. This means the underlying operating cash flow was 287M CHF. The total capex was approximately 87M CHF (excluding the 6.7M CHF spent on the purchase of investments in associates and excluding the 53M CHF in M&A related cash payments of which 21.75M CHF was related to a contingent consideration that was paid out in the first half of this year.

{kind=link}

This means the underlying free cash flow was approximately 200M CHF or 1.25 CHF per share. Keep in mind the company continues to invest in expansion and its 87M CHF spent on capital expenditures is substantially higher than the 63M EUR in depreciation and amortization expenses. If we would also deduct the 13.8M CHF in lease payments from that EBITDA result, Straumann's capex comes in at almost 1.8 times the underlying depreciation expenses.

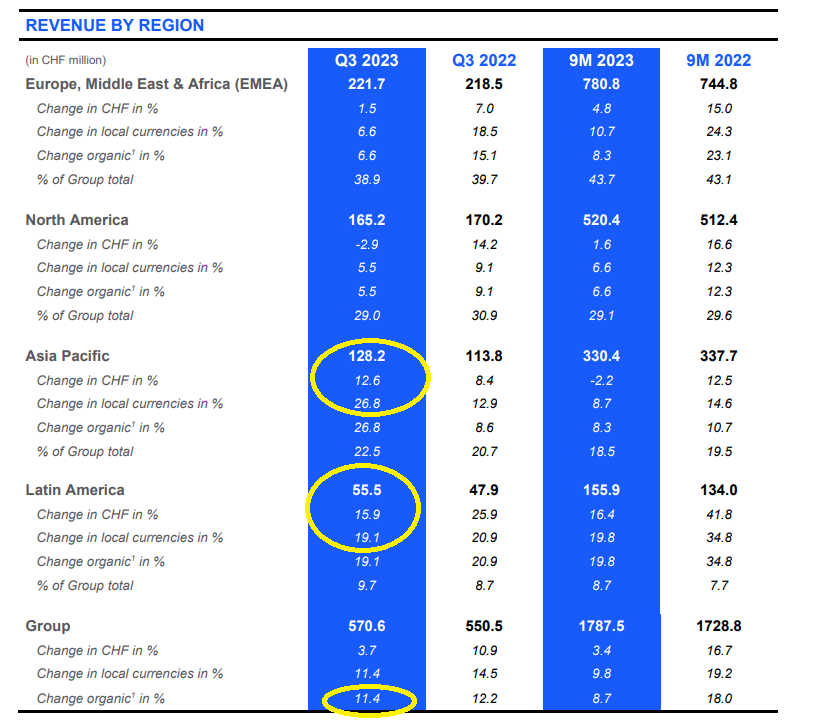

A strong result in the first half of the year, and Straumann's organic growth results continue to be pretty strong. In the third quarter of this year, Straumann reported an 11% organic revenue growth to 571M CHF. This resulted in a reported revenue of 1.8B CHF in the first nine months of the year. As you can see below, the Asia Pacific markets showed very strong growth results with a 26.8% revenue growth in local currencies (and 12.6% when reported in CHF)

{kind=link}

This means the company remains well on track to meet its guidance of a high single digit organic revenue growth (the organic revenue growth in the first nine months of the year was 8.7%) while its EBIT margin of 25% also appears to be very achievable.

Investment thesis

I obviously do like companies with a strong position in the markets it operates in and the very high gross margin (and robust EBITDA margin of just over 30%) is very appealing as well. Throw in the fact that Straumann estimates the size of its addressable market at 19B CHF and its expectation to continue to increase its market share and it is understandable to see Straumann trading at a premium valuation.

About that valuation: looking at the consensus estimates , analysts are expecting a double-digit EBITDA growth throughout 2024 and 2025 and are aiming for a 922M CHF EBITDA in FY 2025. While those are impressive growth numbers, the EV/EBITDA multiple would still exceed 20 while the free cash flow yield will likely still come in below 3%. Although that still is somewhat decent compared to the risk-free interest rate (the 5-year Swiss government bond currently has a yield of just 0.75%), there are some other Swiss quality companies like SGS I would rather put my money in. Unfortunately, there are no good comparables for Straumann due to its leadership position as other medical supply companies generally don't enjoy the same qualities.

On its Q3 conference call , Straumann's management mentioned that while it didn't want to provide any guidance for 2024 just yet, it was 'very optimistic about 2024 in its way to be able to counter some softness' but Straumann first wanted to get through Q4 2023 before providing guidance.

And that's why I'm currently on the sidelines. It's a great company with a strong management team but the valuation is still a bit too rich . I am however keeping track of Straumann as every once in a while there are opportunities to take a position at a more reasonable valuation and unfortunately I completely missed such entry point in October when the stock traded down to around 100 CHF. At that price point, the stock was trading at approximately 16 times the 2025 EBITDA which of course is a much more reasonable valuation and a multiple I would find acceptable for a company like Straumann.

For further details see:

Straumann: Expect Double-Digit EBITDA Growth In 2024 And 2025