MHO - Strong Demand Helps M/I Homes Q3 Outperform With Record Revenue And Net Income

2023-10-26 01:42:44 ET

Summary

- M/I Homes continues to outperform its peers and thrive on an absolute basis, with record quarterly revenue and strong margins.

- The success of M/I Homes is attributed to a focus on more affordable homes, particularly the SmartSeries homes, which have lower cycle times and are attractive to Millennial households.

- Despite higher mortgage rates, M/I Homes has seen strong demand and a decrease in cancellation rates, although a slight slowdown in activity was observed in October.

Based on this important juncture for trading and investing in home builders, I approached the Q3 earnings report for M/I Homes ( MHO ) with a microscope in hand looking for telling blemishes. I went looking for key signs of weakness that would unleash downgrades for MHO. Instead, what I found was a home builder that not only continues to outperform its peers but also is thriving on an absolute basis.

Revenue growth and margins

I earlier looked at revenue growth and margin trends as key correlates for analyst ratings. MHO continues to perform well on both counts although as a whole analysts have rated MHO as a hold over the past 5 months. The builder reported record quarterly revenue of $1.0B, a 3% year-over-year gain. This achievement will keep the trailing twelve month ((TTM)) revenue moving up and to the right. Gross margins increased despite on-going rate buydowns and incentives to motivate buyers (interest rate locks and forward commitments). The 27% gross margin represents an increase year-over-year and sequentially, 26.8% a year ago and 26% in Q2 . All these margins are above the 25% threshold that seems to divide the buys from holds for analysts. Thus, MHO is a slight anomaly (and thus an interesting potential value).

Record revenues and strong margins generated record quarterly net income of $139.0M ($4.82 per diluted share), up 6% year-over-year from $131.6M. Diluted earnings per share increased 3.2% year-over-year.

Drivers of Success

On the conference call , management credited their success to a focus on more affordable homes that started “several years ago.” M/I Homes’ SmartSeries homes deliver the best margins in the portfolio and have lower cycle times. Overall cycle times improved in the third quarter and are down a whopping 50 days year-over-year. The SmartSeries is currently 55% of MHO sales and apparently particularly attractive to Millennial households. The builder expects the share of sales could get as high as 60-65%. The company plans to maintain portfolio diversity with its move-up and “empty nester” homes. The builder provided little else in terms of guidance.

Strong Demand

Even cancellation rates are down year-over-year from 17% to 10%. Incredibly, overall demand and business looks better for MHI at 7%+ mortgage rates than it looked with much lower mortgage rates as recently as the start of this year. Management described the last 6 months of 2022 as “rough.” The builder did 380 to 390 sales a month at that time. Now, MHO “sales since January and through September have averaged in the high sixes, low sevens, 100 a month.”

I am suspecting that a rate of change effect is influencing market behaviors. Last year’s mortgage spike was a shock. Rates went from 3% to 7% in just 10 months. This year, rates have gone from 6.5% to 8%. This slower movement gives builders and buyers more time to adjust and anticipate. In other words, the market has moved from shock to acceptance.

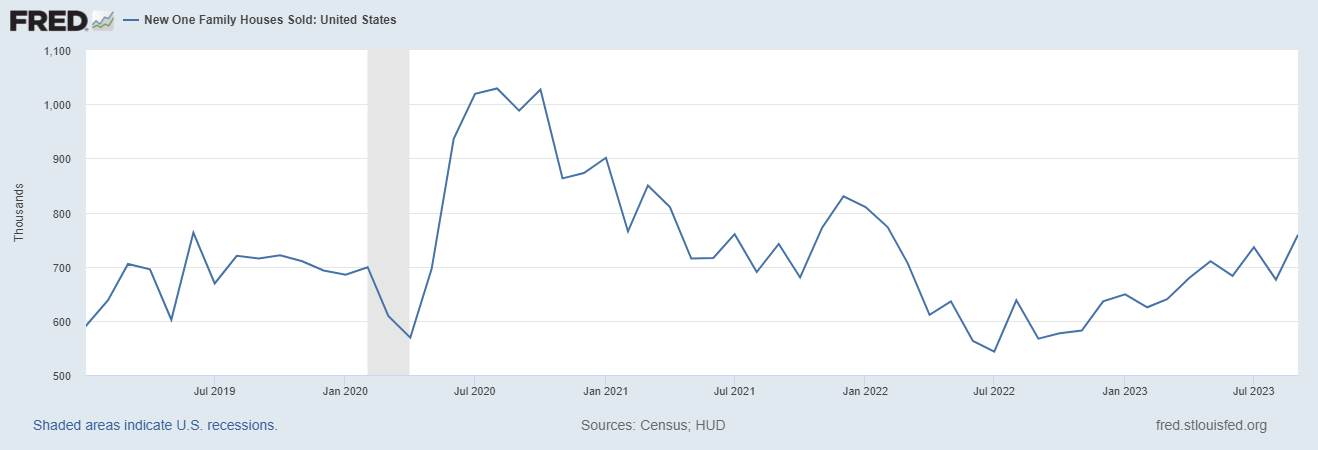

Yet, mortgage rates at 8% may deliver a fresh test of the robustness of demand. MHO management noted that rates at or around 8% have impacted demand with a “slight slowdown in activity.” Market activity slowed down a bit in October. This fresh data point is important given sales of new single-family homes were quite strong in September. Sales were last this high the month before the Federal Reserve started hiking interest rates in 2022!

U.S. Census Bureau and U.S. Department of Housing and Urban Development, New One Family Houses Sold: United States [HSN1F], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/HSN1F, October 25, 2023

{kind=link}

MHO will continue to focus on below market rate mortgages to incent sales. Currently, about 80% of MHO’s customers are taking advantage of financial incentives though M/I Financial. The mortgage business captured 86% of all MHO home sales versus 76% a year ago.

The Trade

M/I Homes did not provide much guidance on the conference call, but results to-date make the future look strong, especially with a strong balance sheet and healthy land position. The company is focused on growing revenues and taking market share. Accordingly, it plans on adding communities next year; average community count increased from 173 to 200 year-over-year.

So with a low valuation below 1.0 price/book , MHO looks like a buy assuming the housing market can at least stay stable (note sellers pushed MHO to a 0.5 P/B ratio at last year’s trough). In other words, of the universe I follow, MHO is first on the list for jumping into the seasonal trade on home builders.

MHO also stands out with a strong buy quant rating while analysts rate it at a hold. This wide divergence is surprising but indicative of the potential value locked up in MHO.

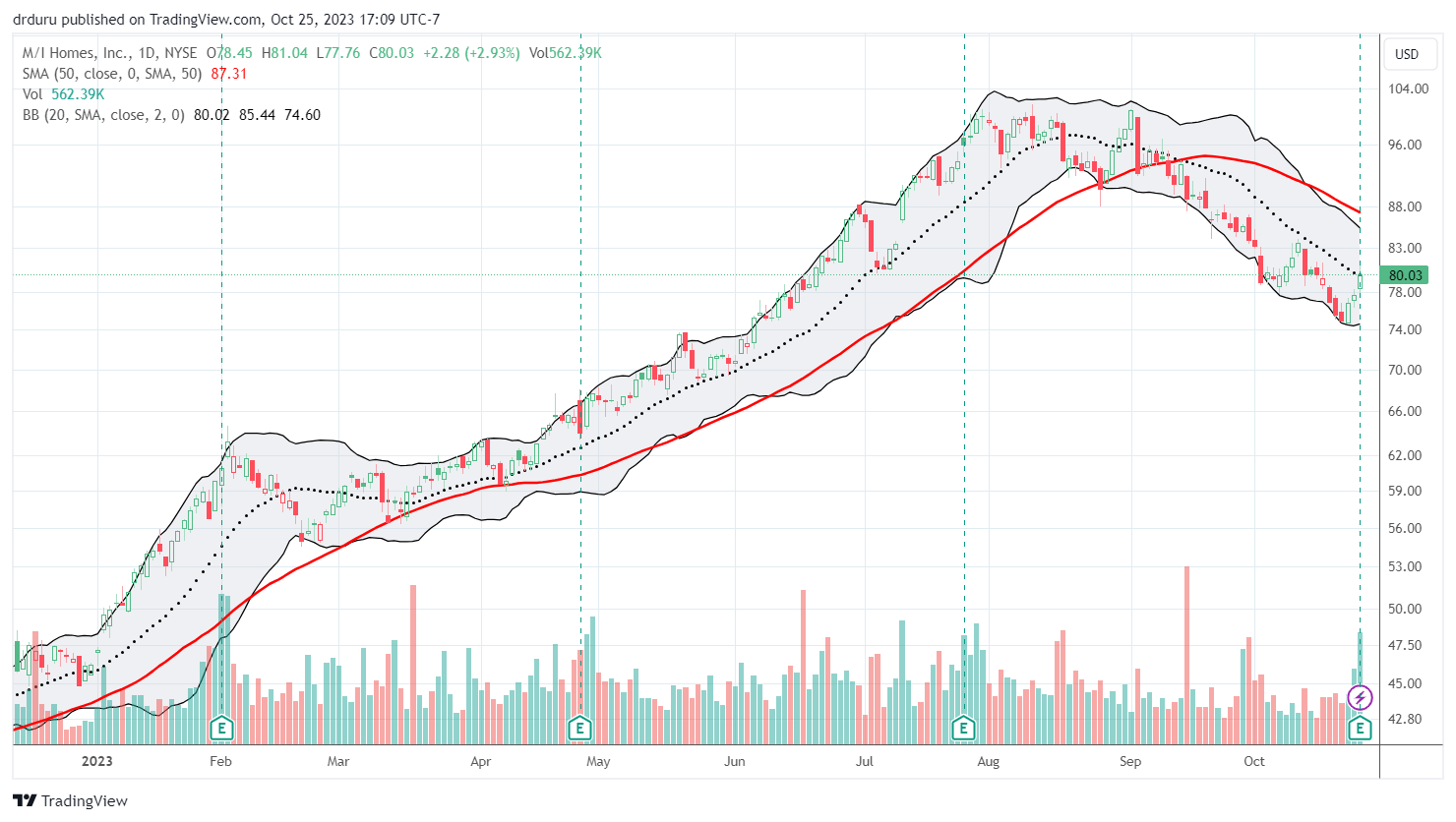

From a technical standpoint, MHO is locked into a firm downtrend defined by its 20-day moving average ((DMA)) (the dotted line below). The stock’s 2.9% post-earnings gain closed right on top of this downtrend. I prefer to start nibbling on the stock after it makes a higher close. However, I suspect the downtrending 50DMA (the red line) will present its own stiff resistance. Thus, my upside expectations in the near-term are very modest. Note that MHO outperformed most home builders on the day as iShares U.S. Home Construction ETF ( ITB ) declined 1.6% to a fresh 6-month low. The overall selling in the sector could easily weigh on MHO which traded at a 4 1/2 month low last week. Fortunately, near-term downside is limited by current oversold trading conditions in the stock market.

Given MHO is up 73.3% year-to-date, I will avoid getting aggressive and prepare to buy at lower price points all else being equal. Fortunately, MHO has such a strong balance sheet that it has a standing authorization to repurchase shares. MHO spent $25M repurchasing stock in Q3 and has $53M remaining in its authorization. The company holds $736M in cash (up significantly from $68K a year ago) and an attractive homebuilding debt to capital ratio of 22% (down from 26% a year ago).

MHO has had a strong run-up in 2023 even with the recent drawdown. (Tradingview.com)

{kind=link}

Be careful out there!

For further details see:

Strong Demand Helps M/I Homes Q3 Outperform With Record Revenue And Net Income