NCR - Structural Changes Could Make NCR Less Boring

2023-08-04 19:04:18 ET

Summary

- NCR Corporation offers banking and fund transaction services.

- The company has a very high level of debt, increasing the risk level for investors.

- A spinoff or other possible structural changes could create shareholder value, although investors currently have limited visibility of such moves.

- The company's stock is currently priced reasonably according to my DCF estimates, which is why I have a hold-rating for the stock.

NCR Corporation ( NCR ) is a company that offers services around banking and fund transactions. For example, the company has an ATM-as-a-service solution. The company has a high level of debt, which increases NCR’ the risk level for investors substantially. I believe the current stock level prices in reasonable figures from NCR, which is why I have a hold-rating for the stock.

The Company

NCR has solutions around digital banking, transaction processing, ATMs, and POS software across different industries:

NCR's Offering (ncr.com)

The company’s largest single vertical is self-service banking, which contributed $661 million in revenue and $169 million in adjusted EBITDA in Q2, compared to the company’s revenue of $1986 million and $389 million adjusted EBITDA – self-service banking contributes around 43% of the company’s EBITDA:

{kind=link}

Financials

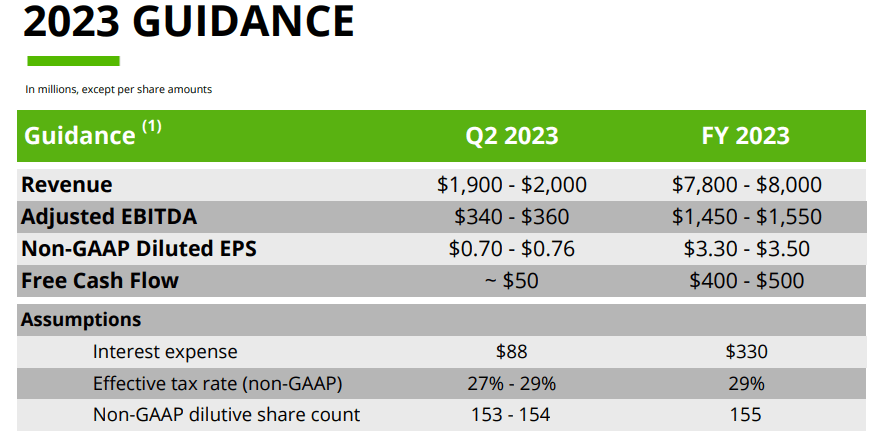

NCR guides towards a revenue of $7800-8000 million for 2023:

2023 Guidance (NCR Q1 Earnings Presentation)

{kind=link}

The guidance was maintained in the company's recently released Q2 results presentation.

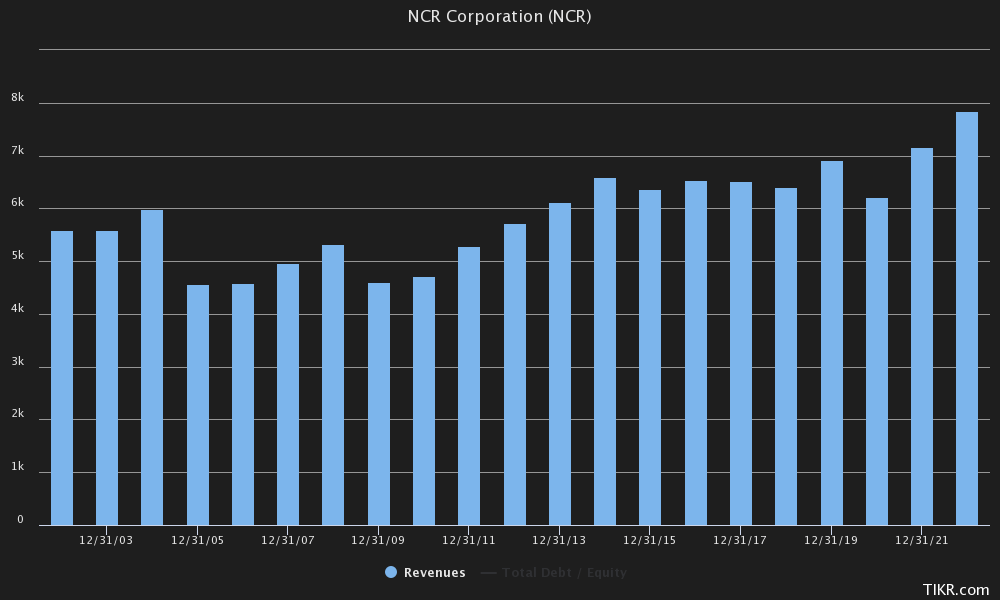

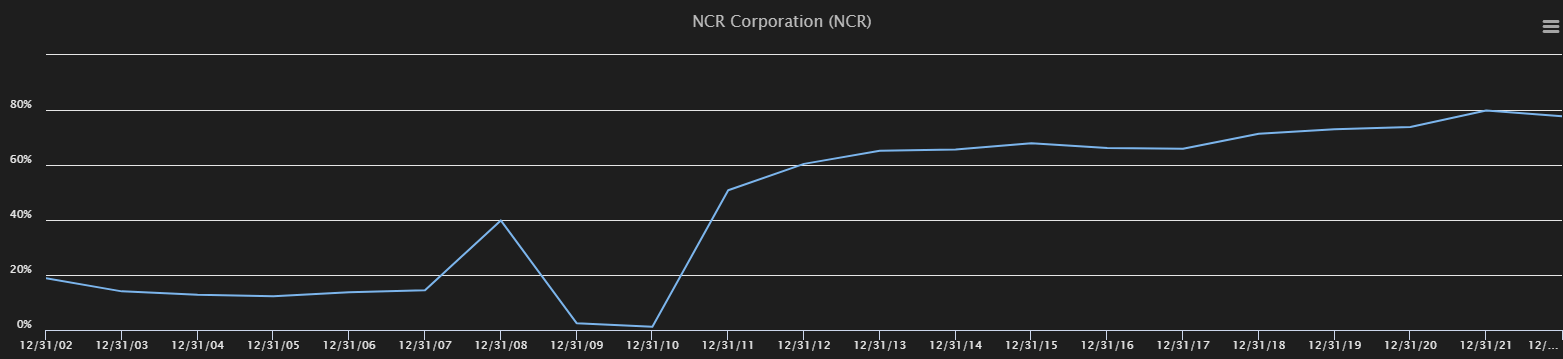

The middlepoint of the guidance represents a 0.7% growth from the prior year. Historically NCR’s growth has been very modest at 1.7% from 2002 to 2022 , basically at the level of the inflation for the period:

{kind=link}

The guidance doesn’t really change my perception of the company’s future growth – the slow rate should continue far into the future.

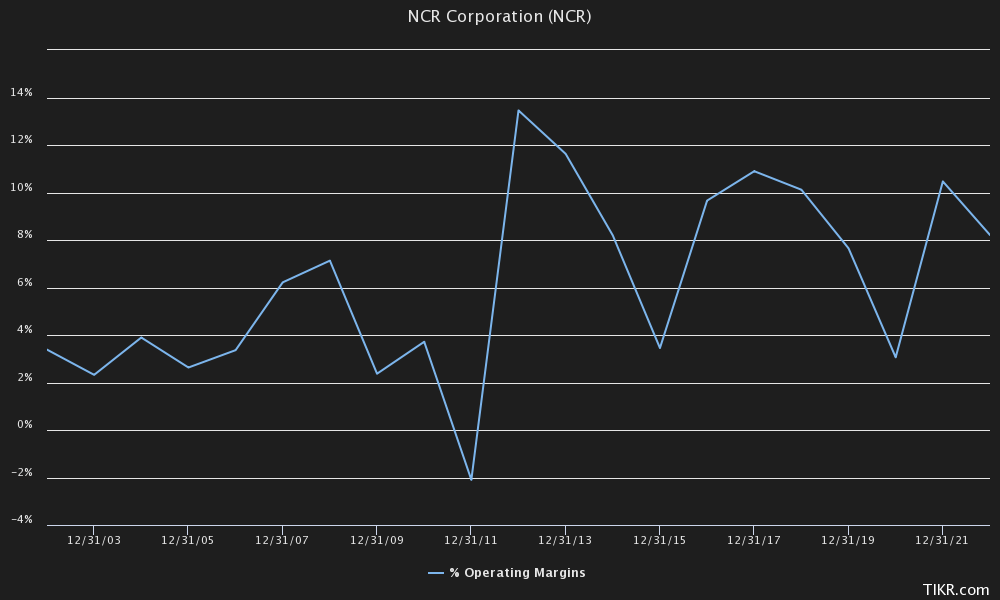

NCR’s trailing operating margin is at 9.4% . This is near the company’s historical level:

{kind=link}

The current year’s guidance has adjusted EBITDA at $1450-1550 million, of which the middlepoint is a growth of $130 million from 2022’s $1370 million adjusted EBITDA. This suggests that the company’s margin should increase in the current year, as revenues should only grow very slightly.

NCR’s balance sheet reveals a huge debt balance of $5429 million in interest-bearing debt. Most of this debt is in long-term debt – around $105 million is in either short-term borrowings or in current portions of long-term debt, needed to paid within a year. This amount of debt is in my opinion too high for the company – with the company’s trailing free cash flow the company would need nine years to pay off its debt. The debt is at a surprisingly low interest rate, though, as the company expects interest expenses of $330 million, meaning around a 6% interest rate. The amount of debt as a form of financing has been on the increase in the last years:

NCR's Debt-to-Capital History (Tikr)

{kind=link}

On the other side of the balance sheet, NCR has a cash balance of $547 million. This somewhat balances the balance sheet and provides safety for the company’s operations, although the outstanding debt is still a heavy burden for NCR.

Valuation

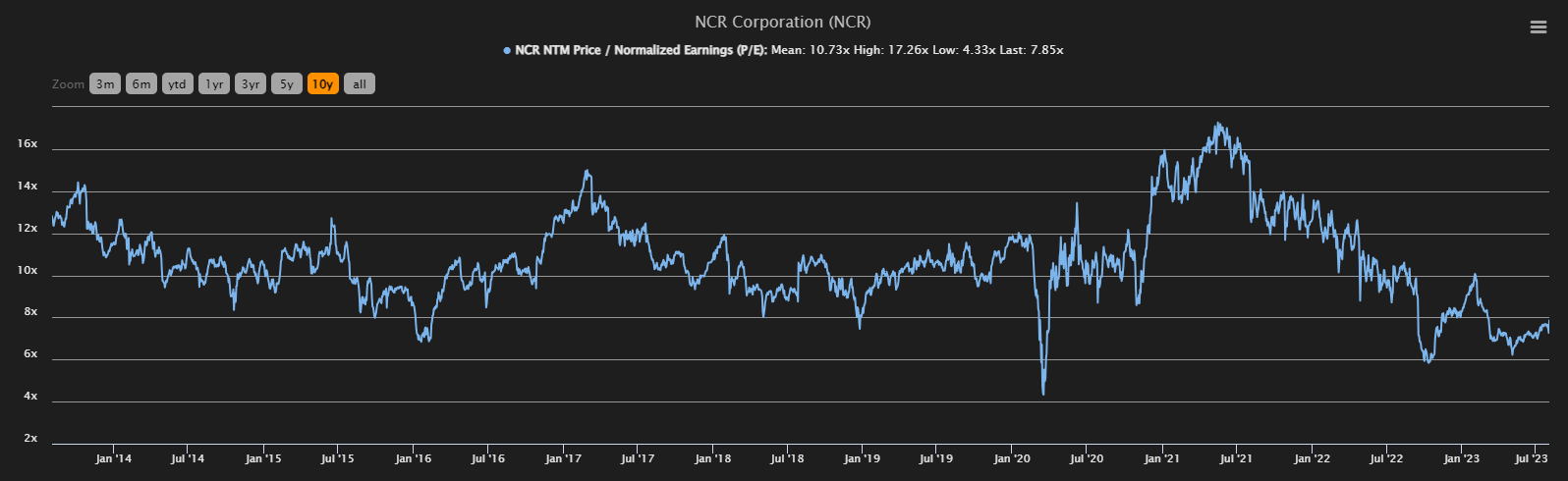

Currently NCR has a NTM price-to-earnings ratio of 7.85 – a figure that’s well below the company’s mean figure of 10.73:

{kind=link}

I believe this should be somewhat justified, as the company’s risk profile has significantly increased due to its increasing amount of debt. To simulate a scenario to get an estimate for the stock’s fair value, I constructed a discounted cash flow model as usual.

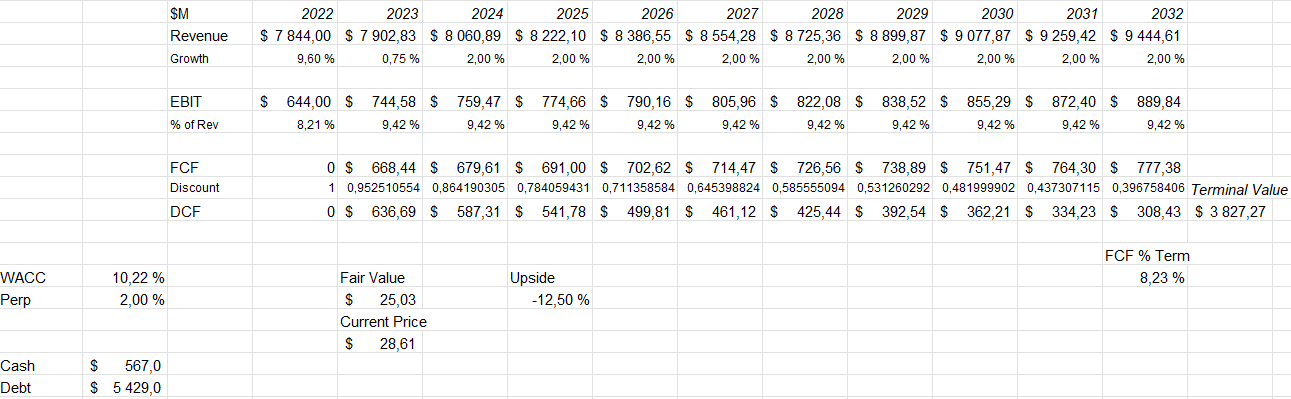

For the current year I expect the company to hit around the midpoint of their guidance in terms of revenue. Going further, I believe the company’s margin should stay stable with a revenue growth of two percent – a rate around inflation. The company has good free cash flow, as NCR doesn’t need to invest extensively. These expectations put the stock’s estimated fair value at $25.03, 12% below the current price of $28.61.

{kind=link}

The expectations also include a weighed average cost of capital of 10.22%, estimated using a capital asset pricing model:

CAPM of NCR (Author's Calculation)

The company’s last quarter’s interest expense was $83 million. With outstanding debts of $5511 million, this represents a 6.02% interest rate, which I used in the CAPM. The company also expects their interest expenses to be around $330 million for 2023, in line with Q1’s $83 million. The company has had a historically high amount of debt, which is why I expect a long-term debt-to-equity ratio of 40%.

NCR’s cost of equity is high at 14.03%. This is explained by the company’s large beta of 1.65, approximated by Tikr . I use the United States’ 10-year bond yield as the risk-free rate, with the yield standing at 4.03% at the time of writing. The equity risk premium of 5.91% is Aswath Damodaran’s July estimate for the United States.

These estimates put NCR’s WACC at 10.22%, which is used in the DCF model.

A Spinoff Incoming?

NCR plans to spin off part of its company into a separate public company – one of the two new companies would be focused on digital commerce , other on ATMs. The company is also open to selling parts of its business, as told on Joshua Fineman’s news piece. The proposed spinoff would happen in late 2023 according to the company. Structural changes in the company such as the spinoff or possible sales could create shareholder value, as the two new companies could be more focused on their core expertise and business; the spinoff could represent investors with upside. An investor day is scheduled for September 5th according to the company's Q2 presentation - investors should hear more about strategic moves in a couple of months.

Risks

The main risk with NCR is its amount of debt. The payments could cripple the company’s ability to pay out dividends, or even to create cash flows, for shareholders. Although almost all of the debt is in long-term debt, it is highly risky to leverage debt to such an extent.

Takeaway

At $28.61, I believe NCR is fairly valued given current financials. The company is risky for shareholders as the company has a hefty debt balance, but a spinoff in the future could create upside for shareholders. Until the company’s share price or financials turn significantly in one direction, or investors have greater visibility into structural changes in the company, I have a hold-rating for the stock

For further details see:

Structural Changes Could Make NCR Less Boring