FUJHF - Subaru: Strong Margins With Scope For Improvement

2023-05-19 13:59:02 ET

Summary

- Subaru Corporation is a Japanese company that produces and sells cars, aircraft, aerospace-related machinery, and related components.

- Revenue growth has been mild, having struggled in recent years. The outlook is far more positive.

- Margins are attractive and look sticky, with the business in the top percentile of its peers.

- Subaru is currently trading below its equity value and historical trading average.

Investment thesis

Our current investment thesis is:

- Subaru has steady growth potential and is a quality brand. Market share growth in the US reflects this.

- Margins are leading compared to other peers, which should allow for continued dividend growth.

- Subaru's valuation is too low to ignore, relative to its historical trading average.

Company description

Subaru Corporation ( FUJHF / FUJHY ) is a Japanese company that produces and sells cars, aircraft, aerospace-related machinery, and related components.

Its operations are divided into three segments: Automotive, Aerospace, and Others. The company is also involved in real estate, shipping, land freight, warehousing, leasing, rental, credit, financing, inspection, service, maintenance, and IT system development and operation services.

Share price

Subaru's share price performed well for most of the last decade, generating substantial returns as prospects look positive and growth was strong. Since 2017, the share price has rerated and begun a steep decline, as all the positives which generated returns turned negative.

This represents a potential opportunity for investors. Most mature stocks have experienced a period of difficulty yet markets are unforgiving. Having lost over 50% since its ATH, there could be scope for alpha here.

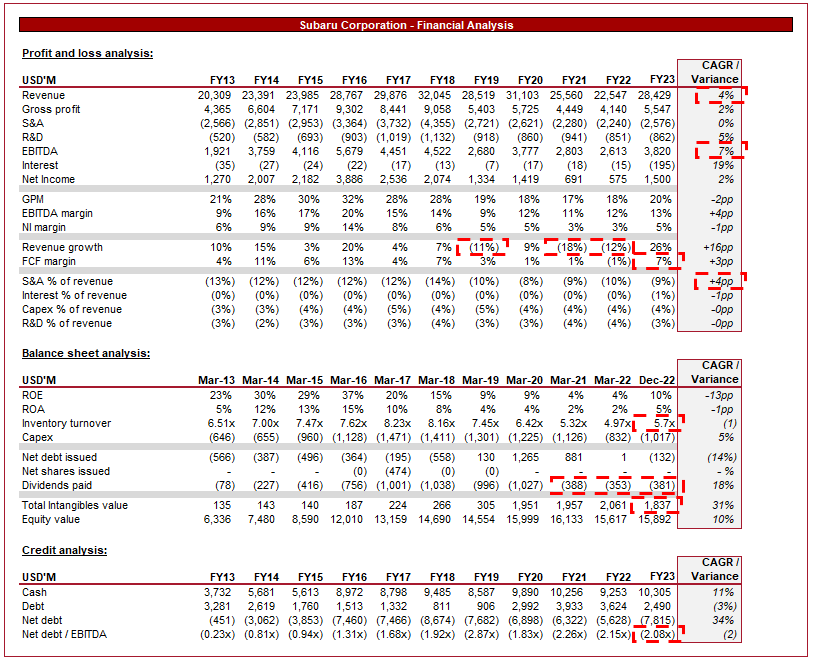

Financial analysis

Subaru Financial performance (Tikr Terminal)

{kind=link}

Presented above is Subaru's financial performance for the last decade.

Revenue

Subaru's revenue has grown at a CAGR of 4%, driven in large part by its automotive business. This growth rate does conceal the performance since FY18, as the company experienced 3 periods of decline in 4 years.

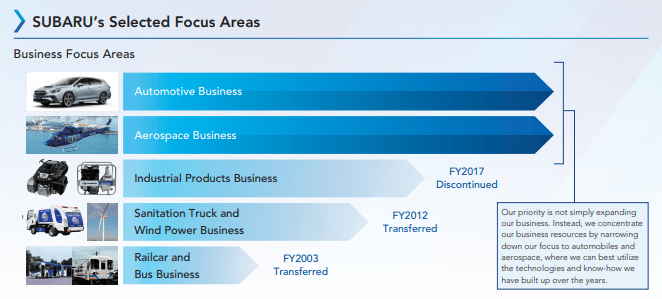

Subaru's current offering encompasses two segments, automotive and aerospace, having discontinued or transferred other parts of the business. Management's current strategy is the opposite of most, they are avoiding mass market and diversification, looking to narrow in and focus on specific segments of their market.

{kind=link}

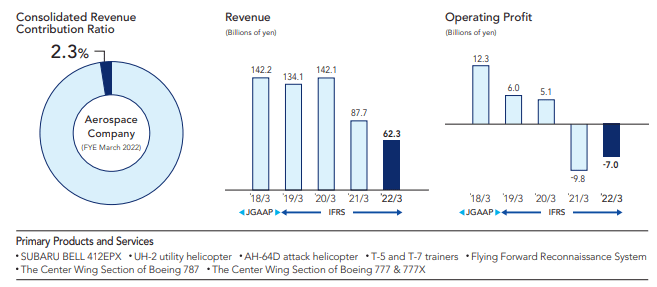

The aerospace business requires a strategic overhaul, experiencing a decline in revenue following the impact of Covid-19, which has yet to recover. This business is now loss-making and acting as a drag on margins. Management believes the signs of a demand recovery are here, preparing for the recovery by investing in both defense and helicopter programs.

{kind=link}

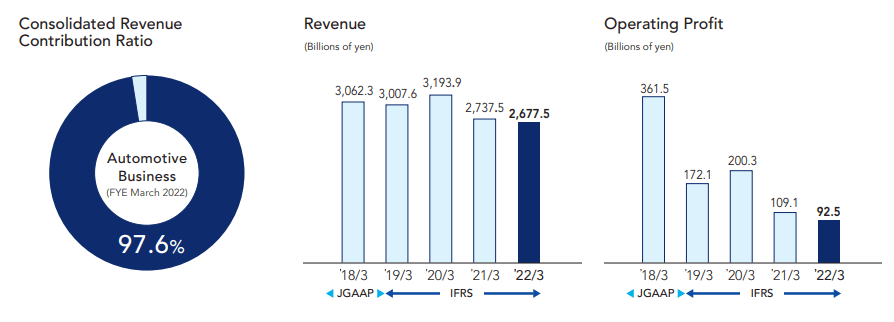

For this reason, Subaru is essentially its Automotive business today. Revenue has remained relatively robust in the last few quarters, showing signs of improvement before the impact of Covid.

Automotive financials (Subaru)

{kind=link}

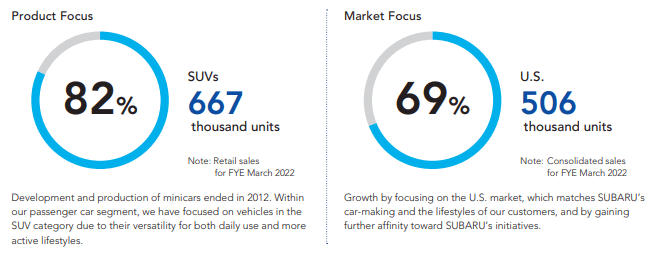

As stated prior, Management is looking to refine its approach to growth. This involves focusing on SUVs and the US vehicle market. Both strategies look reasonable in our view. SUVs are currently the car of choice, owing to their convenience and lifestyle longevity. Further, the US market is the second largest automotive market in the world, with a wide variety of businesses allowing for competition.

Product and market focus (Subaru)

{kind=link}

Subaru estimate that they have gained c.1.8ppts of market share in the last decade, rising to 3.9%. Their most popular SUV on the market is currently the 11th most popular in the US . This is a reflection of strong innovation in product design and also an improvement in brand image. It is clear that the automotive business is fundamentally attractive to what is a highly competitive market.

Market share (Subaru)

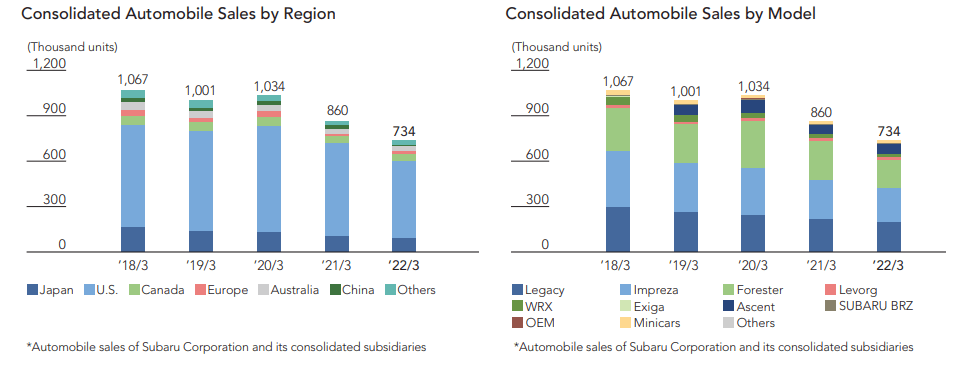

The degree to which Subaru is dependent on the US and SUVs is reflected below, with all other segments representing a minority share. Our usual argument here would be to caution risk, as the business is highly susceptible to a change in conditions. This said it is a clear objective of management to increase this dependency and so the question is more so to consider the underlying risk. The US market should be robust in our view, the country is built for vehicles and lacks the infrastructure to materially dislodge the dominance of cars. Market share is increasing which should mean the development of the brand. The SUV market is what we are less sure of. The segment is riding a high and no end looks clearly in sight, yet consumer trends are quick to change and rarely remain the same beyond a decade or two. Therefore, we would like to see the model diversification increase and there should be scope for this, as the WRX, Impreza, and Levorg are highly regarded globally.

Sales by region / model (Subaru)

{kind=link}

One of the most significant trends impacting the automotive industry is the shift toward electric vehicles. As consumers become more concerned about the environment and the cost of fuel, as well as Governments looking to clean up energy consumption, there is a growing demand for vehicles that are electric or hybrid. Subaru is committed to the transition, although unlike many of its European peers, the full transition is not expected until after 2030. This is likely a reflection of being primarily in the US market, where the pressure to transition is far less immediate.

CO2 consumption (Subaru)

Looking more long term, we are seeing the development of autonomous driving technology. There is a growing interest among consumers for vehicles with these capabilities and discussions around improving safety on the road. Not to mention, the end goal of this technology has the opportunity to eliminate the concept of a "driver" and revolutionize the ride-sharing market. Subaru is developing its own advanced driver-assistance system called EyeSight , which uses stereo cameras to detect objects and assist drivers with safety features.

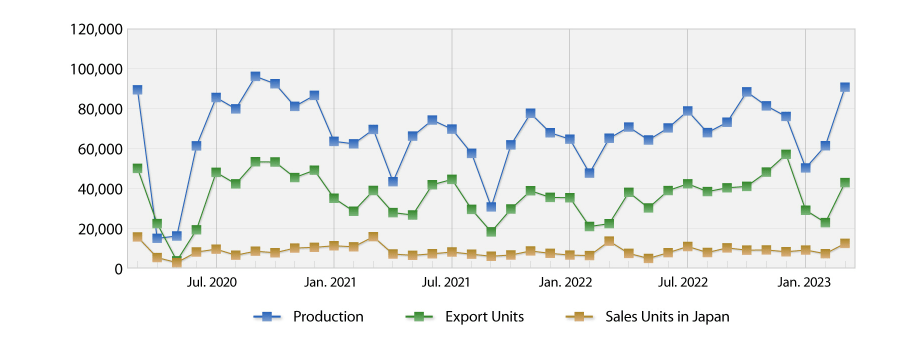

The COVID-19 pandemic materially impacted the supply chain of automotive vehicles. It experienced an extreme shortage of microchips and other components, which continues to be an issue although not to the same degree. Subaru was also impacted but as a non-leading brand, it likely saw a degree of improving demand as consumers were unable to get their preferred choice.

Production and export (Subaru)

{kind=link}

Economic considerations

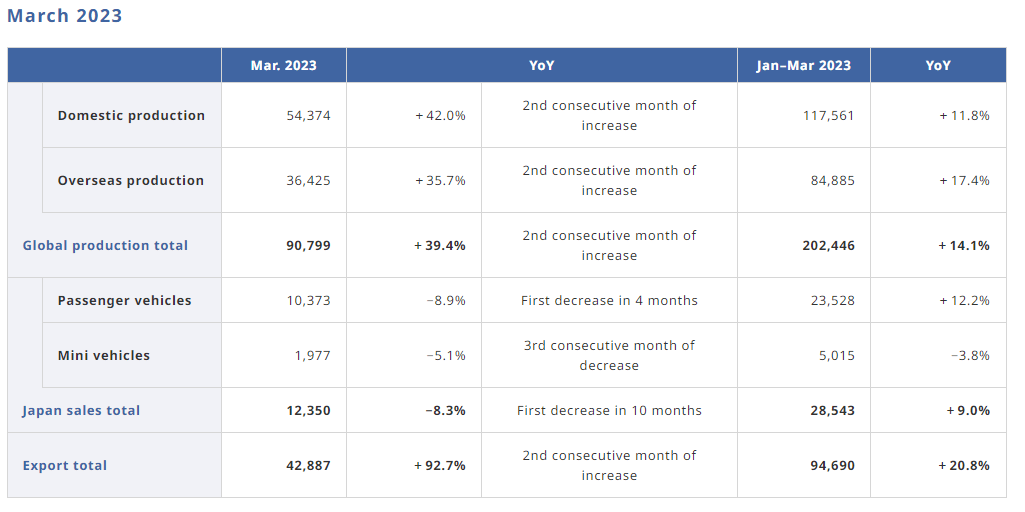

The US is currently experiencing a period of economic weakening, driven by what has been rampant inflation and historic rate rises in response. This has led to a slowdown in discretionary spending across many sectors as consumers see their cost of living rapidly rising.

Vehicle sales look to be resilient so far in the US, which is not usual when compared to many other industries. Rate hikes have not totally killed demand as many had forecast.

Subaru's data support this, with a large production expansion Y/Y. This has the potential to drive an impressive FY24 should demand remain at similar levels throughout the year.

{kind=link}

Margin

Subaru's margins have slipped from their all-time high levels between FY13-FY17, however, remain relatively strong on an absolute level. Further, they have remained sticky despite the current economic conditions, inflationary pressures, and Covid-19 impact. At these levels, strong distributions should be possible and consistent.

Balance sheet

Similar to other Japanese businesses, Subaru is cash-heavy with a low amount of debt. This is primarily why its efficiency ratios are poor, the business has a bloated balance sheet, at least from a Western perspective.

Inventory turnover surprisingly increased in FY23, reflecting what is resilient demand and likely to a level unexpected from Management.

Management's current capital policy is reflected below, with dividends a mainstay and repurchases possible.

Capital policy (Subaru)

With the level of cash the business has, its current equity value is $15.6BN, or $14.1BN when adjusted for intangibles. This is compared to a current market cap of $12.7BN and an EV of $5.0BN.

Outlook

Outlook (Subaru)

Presented above is Wall St.'s consensus forecast for the coming 5 years.

FY24 looks to be well ahead of FY23, suggesting Analysts are highly bullish on this last quarter, expecting things to continue.

Unfortunately, margins are expected to decline, although the forecasts suggest Analysts are less certain regarding this.

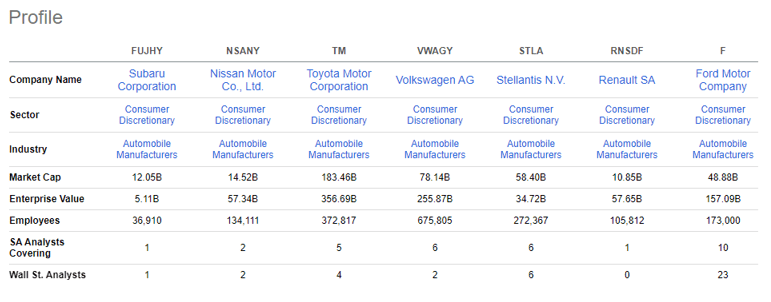

Peer analysis

Automotive industry (Seeking Alpha)

{kind=link}

In order to assess Subaru's relative performance, we have compared the business to a cohort of other global automotive businesses.

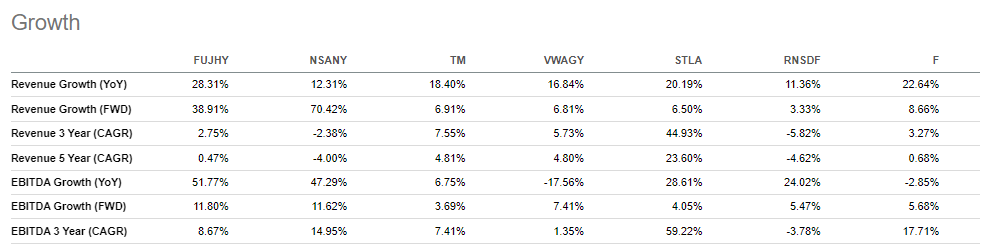

{kind=link}

Subaru growth has been uninspiring in the last 5 years, a reflection of the difficulties the company has faced. During this time, its peers have not set the world on fire. This is likely a reflection of the rise of EVs, as the traditional producers lag behind.

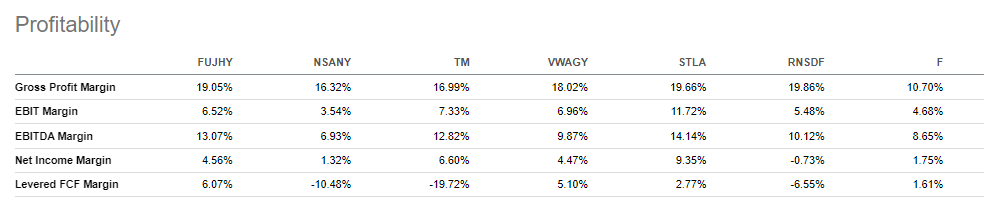

{kind=link}

Subaru is far stronger from a Profitability perspective, in line with the top performers highlighted. Despite the margin slippage, the business is still attractive for its returns.

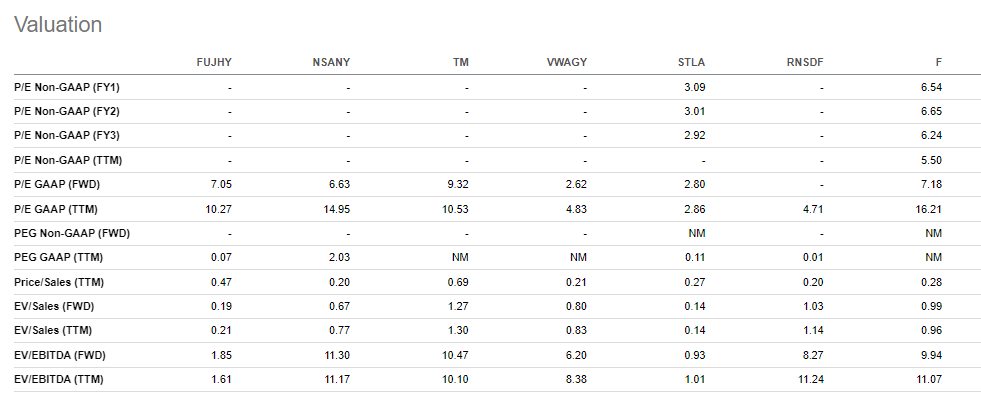

Valuation

{kind=link}

Subaru is currently trading at 1.6x its EBITDA, a monumental discount relative to its peers. Stellantis ( STLA ) is the only comparable business when it comes to a discount and this is a stock we rated a strong buy .

This valuation can be deceiving as due to the amount of cash the business holds, you are essentially buying the profits and cash, which is not generating any material returns.

With this in mind, our view is that the business is still attractively valued. Between Jan 2017 and now, the company's average NTM EV/EBITDA multiple is 3.1x, substantially above the current valuation. Even if we take the period post-Nov 2020, the company traded at 2.4x. Our view is that there is no evidence to suggest a further discount is warranted.

Key risks with our thesis

The risks to our current thesis are:

- A decline in demand in the coming months due to current economic conditions, impacting the FY24 performance.

- A material loss of market share during the EV transition.

- Consumer trends change away from SUVs.

Final thoughts

Subaru is a quality business. The brand is strong globally due to its historical achievements with the Impreza WRX, and currently makes high quality vehicles and is gaining market share. Revenue growth has been weak in the last few years but there are positives to suggest this should improve. Margins are strong currently and the key should be to remain at these levels as a minimum.

The company's valuation makes this a low-risk pick in our view, with consistent distributions supporting the current share price.

For further details see:

Subaru: Strong Margins With Scope For Improvement