SSUMF - Sumitomo Corporation: There Is Upside But It's For Large-Cap Allocators

2023-09-22 06:40:05 ET

Summary

- The TSE is requiring companies to disclose plans on how they are going to raise P/Bs if they're below 1x.

- Sumitomo is a very good vehicle for activists like Buffett to promote more aggressive shareholder payouts, which is a nice yield for shareholders and helps P/Bs rise.

- Shareholder friendliness means yield and capital appreciation, and it can be financed with very low Japanese debt, the only easy credit market in the world right now.

- The balance sheet is asset-rich with debt capacity to push payouts. However, the business isn't that exciting, even if it probably will not collapse in sequential results.

- Overall, it's a great play for large-cap allocators who rarely get a win off just financial optimization, which is usually never a value-add. But for us, it's not good enough at these prices.

Sumitomo Corporation (SSUMF) is a pretty commodity heavy exposure with a decent amount of current headwinds that have taken the business down a notch from last year. There is broad stability that we expect on a sequential basis, with give and take with the various commodities. We focus on the valuation angle. The company will have to achieve a 1x P/B to be comfortable with respect to TSE listing considerations. Moreover, there are angles to grow that P/B with attractive shareholder payouts, easily financed by their asset rich balance sheet, long history and the easy credit environment of Japan. There is upside. It's not huge, something beyond 10% from balance sheet optimization, but it's the sort of idea we pass on.

Quick Q1 Note

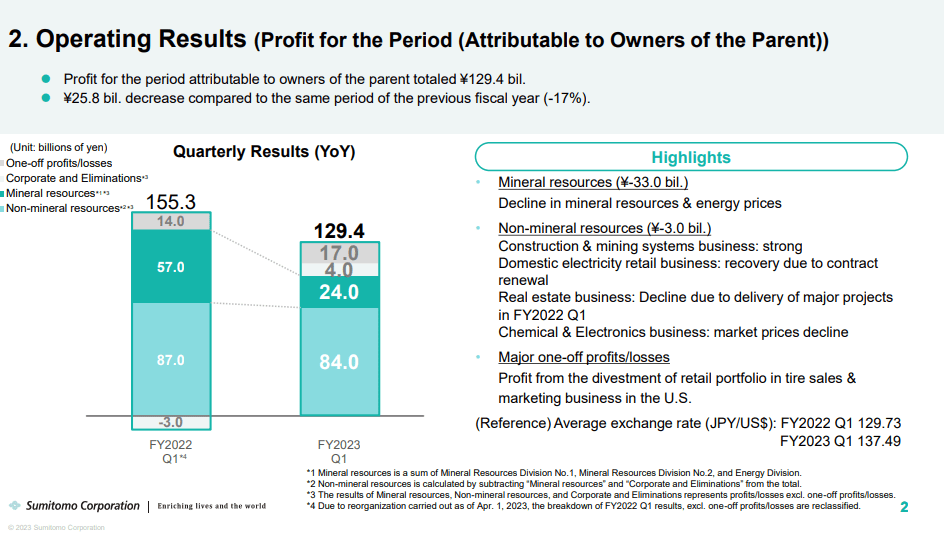

Profit performance wasn't too bad , but it was inflated by some one-offs, including from a disposal in the transportation and construction business, responsible for the extra 17 billion JPY in the profit line.

Operating Results (Q1 2023 Pres)

{kind=link}

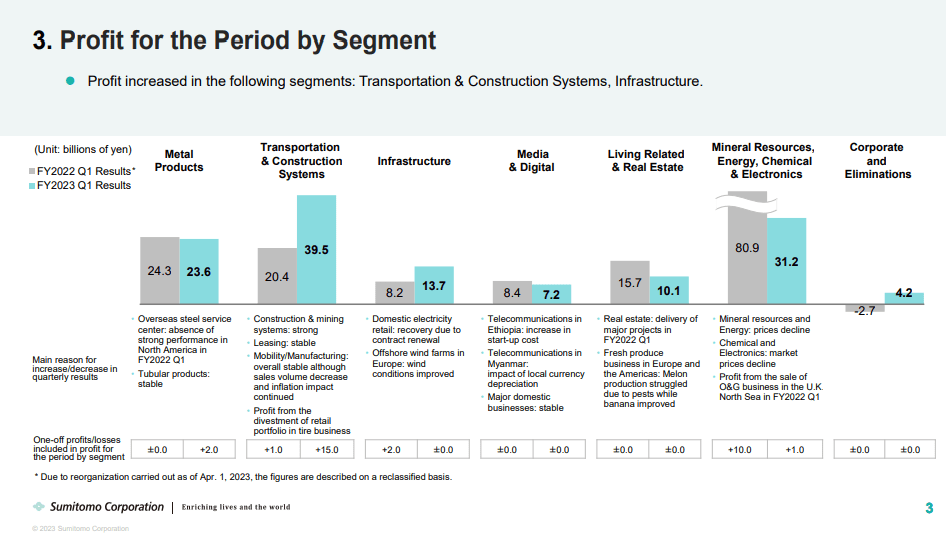

Media and digital saw some pressure from the new Ethiopian Telco launch. Comp effects hurt the living and real estate business, as well as pressure from pests on the melon harvests for the US and EU businesses.

There were the beginnings of slight pressure on metal products. We are a little worried about steel exposures. Demand from China in particular could affect the economics of global steel production, both from pressures on the Chinese economy but also from the fact that the demand for steel there has been in excess of supply for many years where it is anyway maturing now .

The big delta came in the mineral resources and energy business which is a large segment and very levered to commodity prices. Sumitomo is exposed to copper prices, which although quite resilient have come down a bit and haven't helped offset the more precipitous declines coming in coal. General economic pressure and the beginning of deflation in basic energy resources and chemicals have meaningfully hit the profits. A 10 billion JPY one off from last year's oil and gas disposal also made the comp a little more difficult.

Segment Profits (Q1 2023 Pres)

{kind=link}

Bottom Line

Warren Buffett continues to grow his exposures in the trading houses. There are better and cheaper businesses in Japanese than Sumitomo and the others, but for the purposes of a large investors they are perfect for harvesting low-hanging fruit of balance sheet optimization. Smaller companies may not have developed relationship with banks, and Sumitomo is very asset rich and capable of taking on a lot of debt, which in Japan is still at miniscule interest rates.

The TSE is requiring companies to disclose how they plan to get their P/Bs up to 1x, the threshold level, through management plans that either involve investment or capital payouts. Buffett is able to get the company to do buybacks with new debt and pay higher dividends if he wants to. Buybacks in other companies can run into issues. TSE is now requiring companies to have minimum tradeable share ratios. For smaller companies with more fixed ownership such as by families or cross held corporates, there is less space to do buybacks without infringing on this. Sumitomo does not have this problem, and since buybacks are an easy sell to boards in Japan, where they are more wary of dividends, the scope to optimise the balance sheet is pretty unhindered. Although the leverage is at pretty meaningful levels - thankfully the rates are so low. Still, the scope is of course not infinite.

Getting the P/B to 1x and stopping there implies about 10% yield assuming no incremental net losses. The gives and takes in the commodity exposures help that. We think this is a decent baseline. More likely Buffett will be able to push the P/B up further with capital payouts, and the balance sheet optimisation will add price appreciation on top of the declines in book values from payouts. It's not a bad setup at all for shareholders, but Sumitomo isn't the best business out there purely from a volatility and earnings power point of view. While following Buffett here makes sense, since it's a rare instance where his influence actually benefits the business performance, and not just the stock performance, we still prefer other parts of the Japanese market.

For further details see:

Sumitomo Corporation: There Is Upside But It's For Large-Cap Allocators