SMFG - Sumitomo Mitsui Financial Group: A More Favorable Outlook

Summary

- The BoJ's shift to a tighter monetary policy should benefit Sumitomo Mitsui's domestic operations.

- Its recent overseas momentum also bodes well for the outlook.

- Despite the upsized capital return, the book value discount remains wide.

With the BoJ officially tweaking its 'yield curve control' policy over the past week, Sumitomo Mitsui ( SMFG ), one of Japan's megabanks, looks well-positioned to outperform its full-year guidance. Alongside the benefits of a tighter monetary policy, the post-COVID momentum in its Asian operations and the recent success of SMFG's overseas ventures bode well for the capital return.

The domestic lending business will also be helped by easier YoY comparisons and a more favorable post-COVID backdrop for the aircraft leasing business, having cleared any lingering Russia-related impairment losses. With the P&L set for a stronger year ahead, the current book value discount seems unwarranted, presenting investors with compelling value at these levels.

Tighter Monetary Policy is a Tailwind

While inflation has emerged as a key economic issue in Japan this year, the recent policy change at the BoJ was still a surprise, given its steadfast commitment to monetary easing. In essence, the central bank will be moving away from its 'yield curve control' policy, paving the way for an exit from negative interest rates at its upcoming policy meetings. Banks typically benefit from higher rates, and given SMFG has substantial lending assets based on short-term variable interest rates, expect an immediate positive earnings impact in the coming quarters. Assuming rates sustain above zero in FY23 and beyond, SMFG's >15% exposure to prime interest rate lending (e.g., housing loans) also presents an incremental P&L tailwind.

The flip side of higher rates is the impact on the securities portfolio. Here, I am less concerned, as SMFG's diversified portfolio means any valuation losses from domestic bonds (sovereign and corporate) on balance sheets will be minor. Case in point - SMFG raised its profit guidance in H1 2023 despite the higher rates globally, with the upgrade even accounting for a -JPY60bn hit from additional impairment losses on aircraft leasing in Russia. Along with the -JPY25 bn profit hit from the market-rigging scandal at its securities division earlier this year, these one-offs will drop away as we move into FY24, presenting favorable YoY comparisons ahead.

{kind=link}

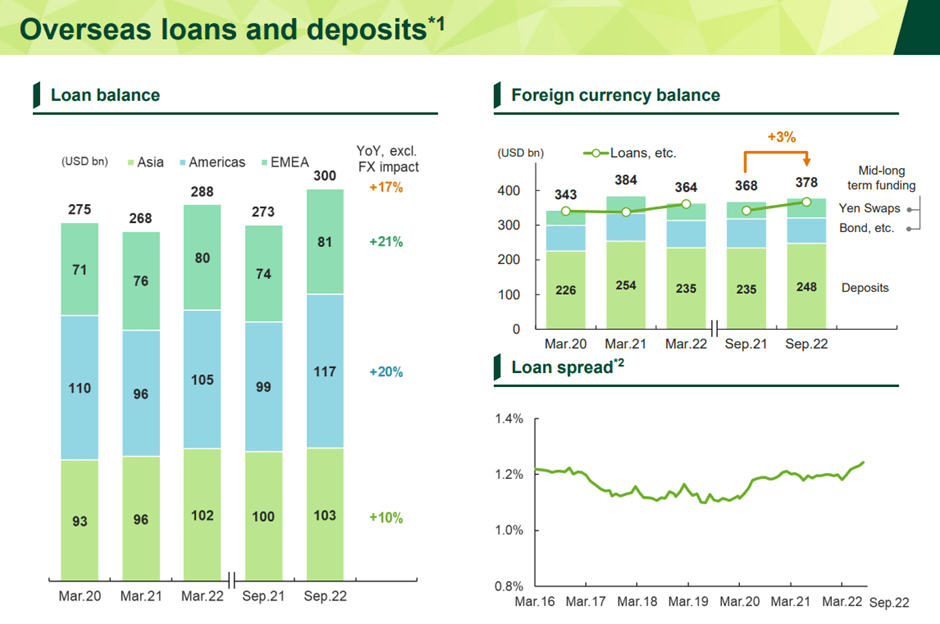

Ex-Japan Businesses Gaining Momentum

In response to the BoJ's negative interest rate policy in recent years, SMFG has ramped up its diversification efforts and now enjoys a large overseas and non-banking presence. In turn, this has reduced the banking group's sensitivity to domestic monetary policy changes relative to regional banks while also granting it exposure to external trends. Within Asia (ex-Japan), for instance, SMFG's commercial banking and consumer finance subsidiaries are positioned to benefit from a post-COVID rebound following the loosening of China's zero-COVID policy.

Efforts to build out strong enterprise-related operations in the US are also seeing positive results - the H1 2023 P&L benefited massively from higher FX and money transfer earnings in the wholesale business, as well as improved interest spreads on overseas lending. Backed by a strong balance sheet, there remains ample room for further inorganic growth outside Japan as well, with SMFG's purchase of a stake in Jefferies earlier this year pointing to the US as a key focus area.

{kind=link}

Gearing Up for More Capital Return

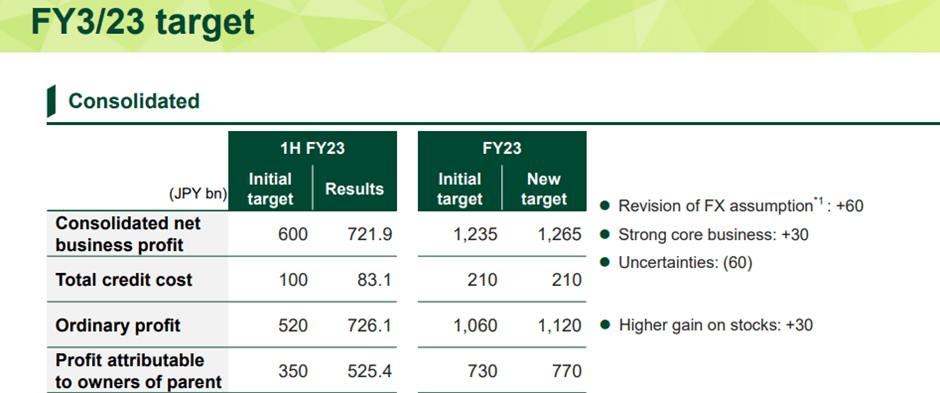

Coming off a great quarterly earnings report, the company's upsized capital return is well-supported. To recap, consolidated net business profits in H1 were up >20% YoY on well-balanced growth of +23% for net interest income and +6% for fee and commission income.

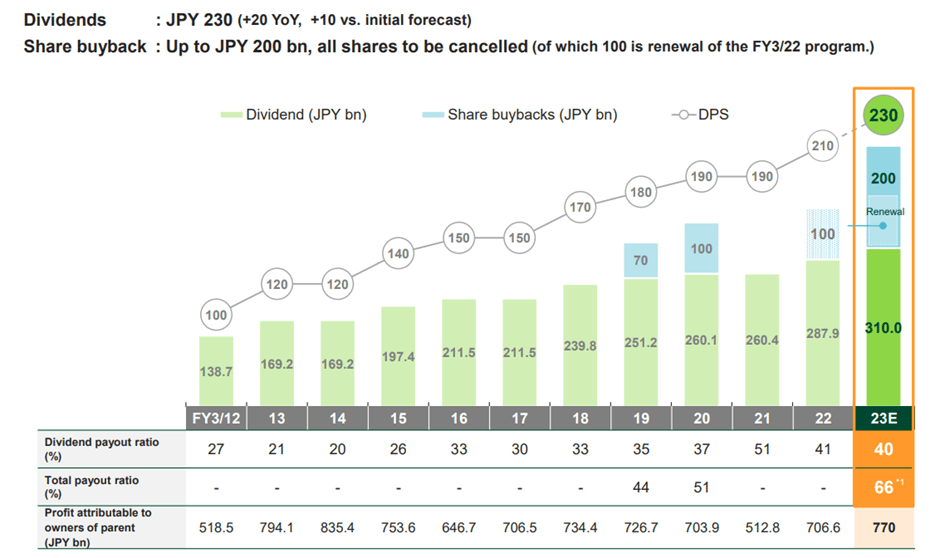

In tandem, the buyback program has been upgraded to JPY200bn (or >4% of shares in issue), while the dividend per share also saw a mid-year hike to JPY230/share (up from JPY220/share prior). The latter will be particularly well-received by the investor base, marking a positive mindset shift by management following shareholder calls for a higher dividend in line with the strong earnings performance.

While encouraging, a large part of the EPS beat in H1 was due to FX and other one-off stock-related gains, so the timing of the DPS hike seems slightly premature at first glance. That said, profit contribution from inorganic growth in FY24 could more than justify the dividend hike, so depending on what management has factored into its framework, we could see even more dividend upside ahead.

{kind=link}

Also positive is the decision to up the share buybacks to JPY200 bn, comprising the renewal of the previously mentioned buyback program at SMFG's last IR day and a JPY100bn addition for the fiscal year. Given the prior JPY100bn buyback was paused due to the Nikko Securities scandal, the renewal announcement will be well-received by investors.

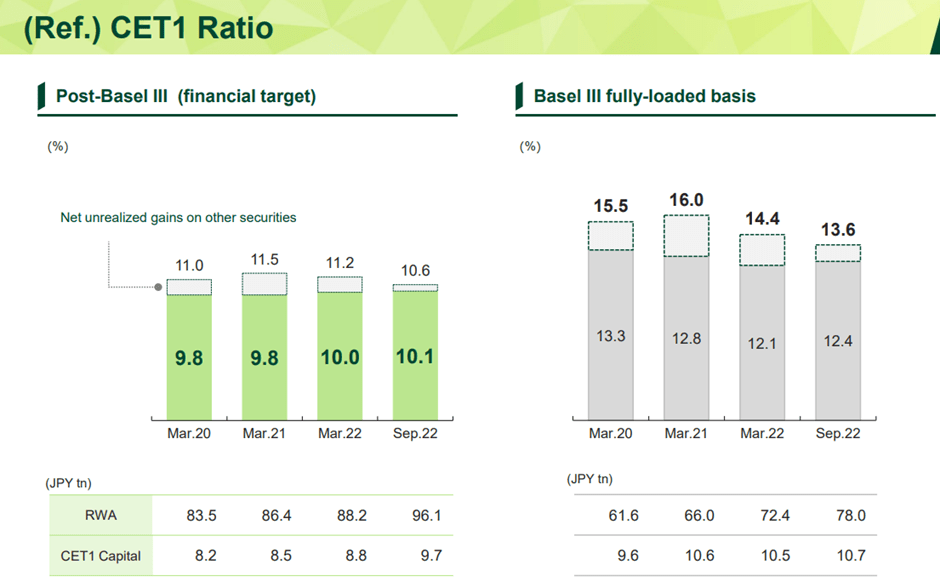

The capital position is also more than sufficient to support the program - the CET1 ratio (excluding accumulated other comprehensive income) was down ~10bps QoQ due to FX one-offs but still stands at a solid ~10%. With ample room for more capital return, SMFG's increasingly proactive stance should dispel any criticism of over-reliance on inorganic growth in its capital deployment framework.

{kind=link}

A More Favorable Outlook

This hasn't been an excellent year for SMFG - earnings were weighed down by the market-rigging scandal involving subsidiary SMBC Nikko Securities, along with Russia-related impairment losses in the aircraft leasing business. Now that these headwinds have cleared, though, the setup into the next fiscal year looks good.

SMFG has already responded to shareholder concerns with an upsized buyback and dividend based on its ample capital base. With the BoJ transitioning into a tightening phase to address inflation, expect more upward revisions to profit and ROE guidance and, by extension, even higher capital returns at the upcoming mid-term update. Net, I see a clear path to the stock's P/B valuation re-rating from currently discounted levels on upside catalysts such as a further improvement in the CET1 ratio, as well as additional shareholder return announcements.

For further details see:

Sumitomo Mitsui Financial Group: A More Favorable Outlook