SMFG - Sumitomo Mitsui Financial: Shares Are Fairly Valued

2023-12-10 20:43:47 ET

Summary

- Sumitomo Mitsui's reduction of cross-shareholdings and its progressive dividend policy are positive factors for the stock.

- But the company's share repurchases and financial targets are unimpressive, and the stock's current P/B multiple appears fair considering the long-term ROE target.

- I think that a Hold investment rating for Sumitomo Mitsui Financial is justified, considering its equity holdings reduction plan, shareholder capital return framework, and financial goals.

Elevator Pitch

I have a Hold investment rating for Sumitomo Mitsui Financial Group, Inc. ( SMFG ) [8316:JP] stock. The aggressive cross-shareholdings reduction plan and a progressive dividend policy are the key positive valuation re-rating drivers for SMFG. On the flip side, Sumitomo Mitsui Financial's share repurchases and financial goals are unimpressive. SMFG's current P/B multiple of 0.74 times appears to be fair considering its long-term ROE target of 8% based on my calculations using the Gordon Growth Model.

Company Overview

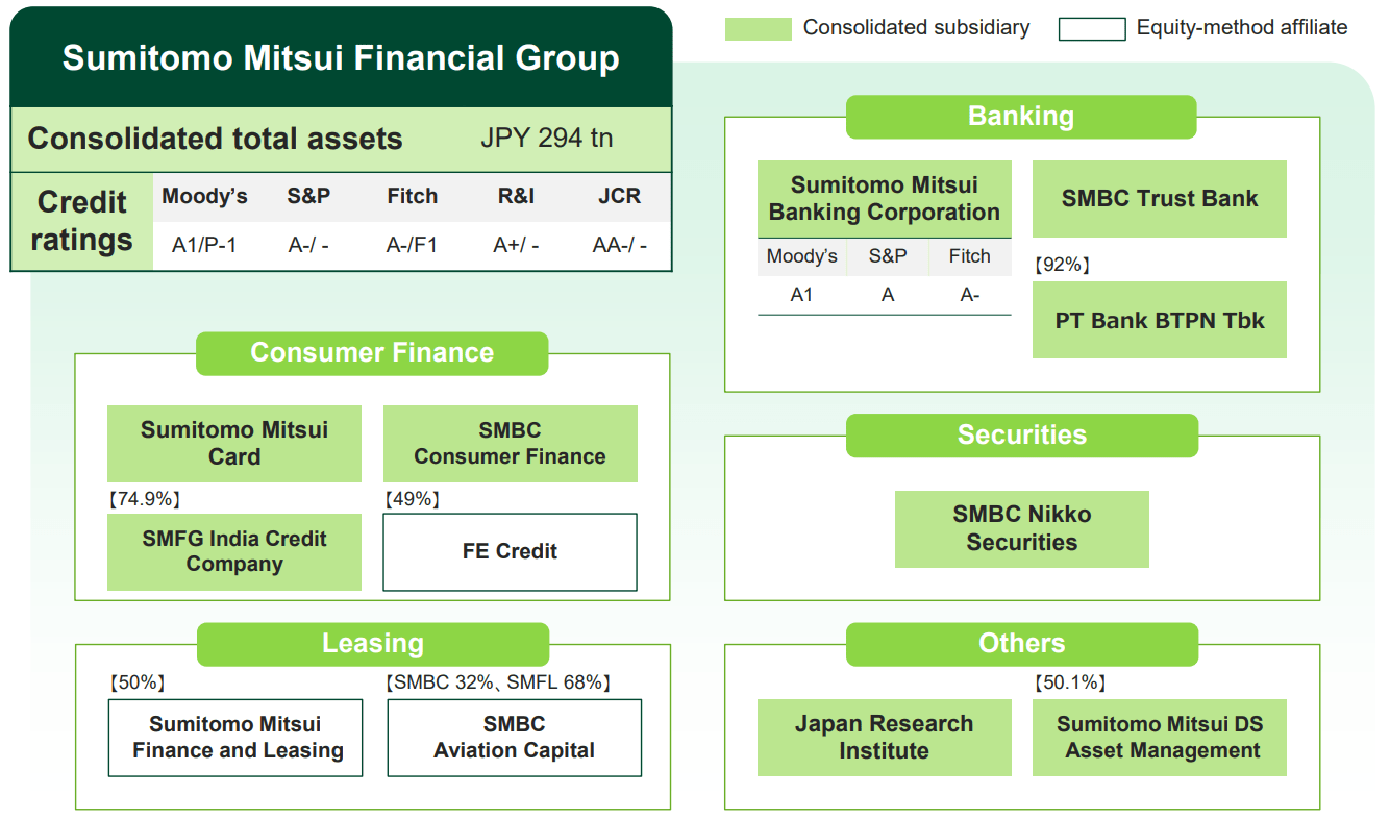

In its press releases , SMFG describes itself "the holding company of SMBC Group", "one of the three largest banking groups in Japan" which provides a "range of financial services, including banking, leasing, securities, credit cards, and consumer finance" in "nearly 40 countries" globally. The other two major Japanese banks are Mitsubishi UFJ Financial Group, Inc. ( MUFG ) [8306:JP] and Mizuho Financial Group, Inc. ( MFG ) [8411:JP].

Sumitomo Mitsui Financial's Corporate Structure

{kind=link}

SMFG's November 2023 Investor Presentation Slides

In the first half of fiscal 2024 (YE March 31, 2024), Sumitomo Mitsui Financial generated 33%, 32%, 24%, and 11% of the company's net business profit from its Global, Wholesale, Global Market, and Retail business segments, respectively. Separately, Japan and foreign markets contributed 47% and 53% of SMFG's revenue, respectively for full-year FY 2023.

Sumitomo Mitsui Financial currently trades at a trailing price-to-book or P/B valuation ratio of 0.71 times as per S&P Capital IQ data. In comparison, its peer MUFG's P/B, Sumitomo Mitsui Financial's historical 15-year mean P/B, and SMFG's internal P/B target are relatively higher at 0.82 times, 0.84 times (source: S&P Capital IQ ), and 1.00 times (source: corporate disclosures), respectively.

In the subsequent sections, I touch on the potential valuation re-rating drivers for SMFG.

Cross-Shareholdings

The market typically assigns a substantial conglomerate or holding company discount to stocks with significant cross-shareholdings on their books, and this is one of the key reasons for SMFG's meaningful 29% discount to book value (or 0.71 times P/B).

It is encouraging that Sumitomo Mitsui Financial has plans in place to reduce its cross-shareholdings. At its 2023 Investor Day in August this year, SMFG outlined its target for the reduction in equity holdings.

As indicated in its 2023 Investor Day presentation slides , Sumitomo Mitsui Financial's equity holdings on its balance sheet had been lowered by -JPY180 billion from JPY1.33 trillion as of March 31, 2020 to JPY1.15 trillion as of March 31, 2023, which is equivalent to market value to consolidated net assets ratio of 0.30 times. SMFG's goal is to reduce its equity holdings by another -JPY200 billion between FY 2024 and FY 2026 to JPY950 billion as of March 31, 2026. The company also aims to decrease the market value-to-consolidated net assets ratio for its equity holdings from 0.30 times as of end-FY 2023 to under 0.20 times for the FY 2027-2029 time period.

The company has achieved good progress in lowering its equity holdings. In the first half of FY 2024, SMFG has delivered JPY120 billion of actual or planned equity holding sales which represents 60% of its JPY200 billion target as revealed in its Q2 FY 2024 results presentation .

SMFG might even do better than what it is currently targeting. At its 2023 Investor Day Q&A session , stressed that "we aim to accelerate the reduction speed (for cross-shareholdings) and exceed the revised (equity holdings reduction) plan (outlined at Investor Day) as much as possible."

Dividends

I am impressed with Sumitomo Mitsui Financial's dividend policy, dividend track record, and dividend yield.

In the company's Q2 FY 2024 earnings presentation, SMFG stated its dividend policy of "progressive dividends." This implies that Sumitomo Mitsui Financial's shareholders are expected to receive higher dividends every year going forward, notwithstanding the company's actual financial performance.

Also, SMFG has never cut its dividend for the past decade, while its annual dividend payout ratio has been at least 30% for the last 8 years.

Sumitomo Mitsui Financial's consensus forward next twelve months' dividend yield is 3.73% (source: S&P Capital IQ ), which is superior to its closest peer, Mitsubishi UFJ Financial Group's 3.48% consensus forward dividend yield.

Share Repurchases

I like the fact that SMFG is distributing a reasonably generous amount of dividends to its shareholders, but I would have liked the company to allocate more capital to share repurchases since the stock is trading at a discount to book value.

However, there is greater uncertainty associated with Sumitomo Mitsui Financial's share buybacks as compared to its dividend distributions.

For the FY 2021-2023 period, SMFG paid out dividends amounting to JPY0.9 trillion, but it only spent JPY0.1 trillion on buybacks as detailed in its Q2 FY 2024 results presentation. Also, Sumitomo Mitsui Financial has bought back its own shares in three of the past 10 years, while it paid out dividends consistently every year for the last decade.

At the company's recent Q2 FY 2024 results briefing Q&A session last month, Sumitomo Mitsui Financial noted the company's shareholder capital return approach revolves around "dividends in principle, and flexible share buybacks", and it emphasized that it will "flexibly implement share buybacks with excess capital." SMFG also highlighted at its earlier 2023 Investor Day Q&A session that its "decision to announce share buybacks was held off in May (2023) due to the uncertain business environment."

Although SMFG has set a target of allocating JPY150 billion to share repurchases for full-year FY 2024, this is lower than its dividend guidance amounting to JPY360 billion. More importantly, there is limited visibility regarding Sumitomo Mitsui Financial's future share buybacks, considering its "flexible" approach towards repurchases.

Financial Targets

Sumitomo Mitsui Financial's intermediate-to-long-term financial targets are disappointing in my opinion.

In its September 2023 BofA ( BAC ) Securities Japan Conference presentation , SMFG shared its goals of increasing its net profit from JPY805.8 billion for FY 2023 to JPY900 billion and JPY1 trillion in FY 2026 and FY 2029, respectively. The company also hopes to improve its ROE from 6.5% in FY 2023 to 8.0% in the long run.

Sumitomo Mitsui Financial's bottom line targets translate into a three-year CAGR of +3.75%, and a six-year CAGR of +3.66%. These implied earnings growth rates in the low single-digit percentage range are unlikely to impress the market.

The 8% ROE target also seems too low to justify a P/B ratio of 1 times for SMFG. Based on the Gordon Growth Model, a 1 times P/B multiple requires an ROE of 10%, assuming a 10% cost of equity and a 0% perpetuity growth rate. This also implies that an ROE of 8% can only support a P/B valuation ratio of 0.80 times. The Gordon Growth Model calculates the P/B ratio as ROE minus perpetuity growth rate divided by the cost of equity minus perpetuity growth rate.

Final Thoughts

I think that SMFG warrants a Hold rating. Sumitomo Mitsui Financial's valuations are fair in my opinion. The company's buybacks are uncertain and its financial outlook is lackluster, which places a cap on the stock's potential capital appreciation.

For further details see:

Sumitomo Mitsui Financial: Shares Are Fairly Valued