INN - Summit Hotel Properties: A Lot Of Debt

2023-11-27 12:25:02 ET

Summary

- Summit Hotel Properties has a lot of debt and is stretching its limits with interest expenses pushing net income into negative territory.

- The post-pandemic recovery has supported revenue growth, but there are concerns about the impact of a worsening recession on discretionary markets.

- The company's debt load has increased significantly due to major acquisitions, interacting unfortunately with the higher interest rate environment.

- The REIT is levered to the rate situation quite meaningfully, and we think the stock is at risk in a mounting recession and with rates where they are, even if they are still producing the cash to pay.

Summit Hotel Properties ( INN ) is a lodging REIT that owns properties operated by various major franchises like Marriott ( MAR ). The locations seem to be fine, but the REIT has a lot of debt and it has been bloated on the acquisition of new property portfolios, really stretching it to the limit of what it can tolerate with interest expenses forcing net income into negative territory. While the post-pandemic recovery is supporting revenue growth, we are worried about what can happen to these discretionary markets if the recession continues to worsen.

Financial Comments

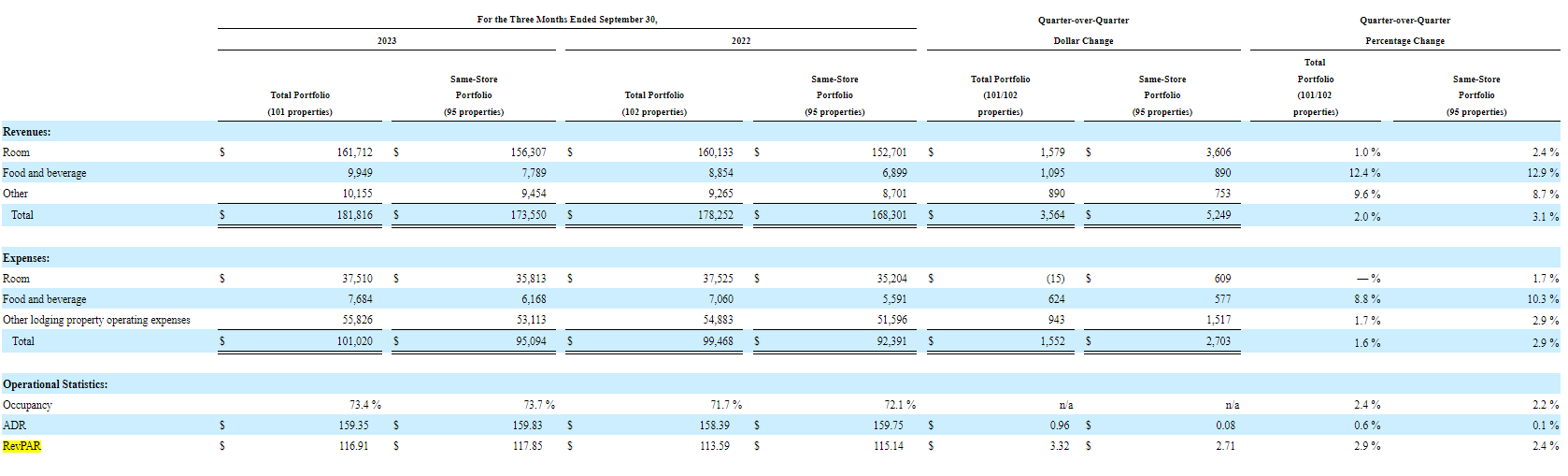

The recovery in the post-pandemic environment has been notable. Non-room revenues are up in the low double digits, signaling more recreational activity, and the RevPAR figures are up as well by a couple of points in the indices, 230 bps to be exact.

{kind=link}

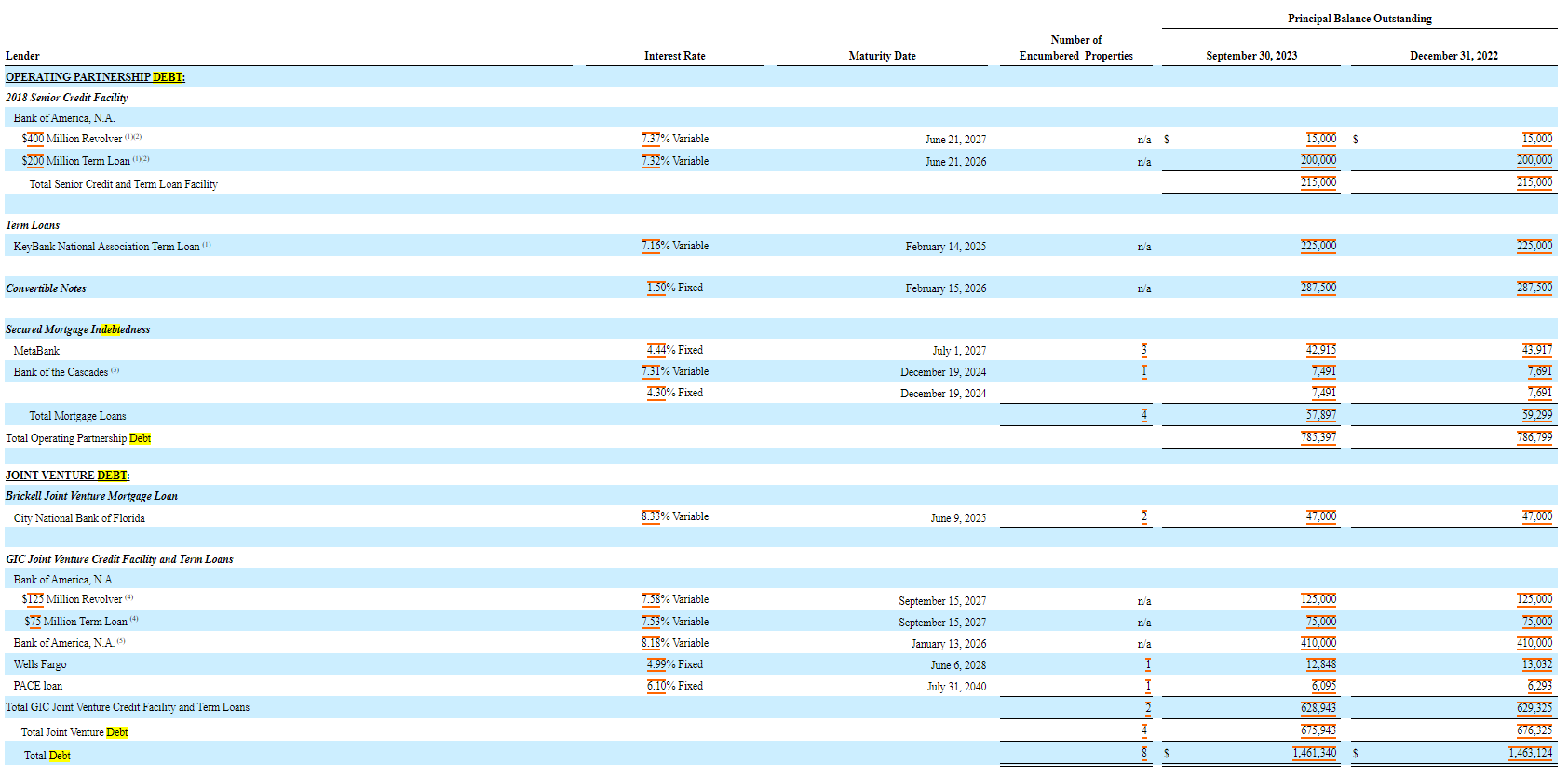

The issue is the debt. It's become substantial as the company continues to make major outlays in order to acquire large portfolios of lodgings. Last year their J.V with GIC paid almost $1 billion for around 3k guestrooms . The debt load went from $1 billion at the end of 2021 to around $1.5 billion as it currently stands. There have also been several smaller transactions in 2023 that add up to more than $50 million. There was also the need for substantial refinancing early this year, and rates have risen meaningfully. Where there was still some 4-5% rate debt on the balance sheet, all of that which has been refinanced is now at the 7% mark.

{kind=link}

The higher interest expenses have begun to come down to the bottom line, which now lies in negative territory in terms of earnings.

IS (SEC.gov)

Naturally, depreciation is high and free cash flow will typically go far ahead of earnings figures, but it is nonetheless an issue. Moreover, inorganic growth tends to be pretty expensive. Operating margins on a property like this tend to be around 10%. Paying $256k per guestroom in a facility, where their assets are mostly located in Texas and Louisiana, strikes us as still pretty expensive and is the reason for the rapid rise in debt and the relative difficulty in keeping INN's head above the interest expenses that are mounting. However, we acknowledge that these seem to be what the market considers fair multiples. We just don't like their absolute position especially with the debt burden it creates. While there still is cash being produced all the time to repay the debt, since there are substantial non-cash expenses bringing down earnings too, it's not a mortal and immediate problem, but it is a massive weight that the company will be under for some time. When rates come down there doesn't seem to be anything precluding a more favourable refinancing, but we have concerns.

Bottom Line

Average useful lives are around 20 years, so using depreciation expenses as a proxy for cash investment assuming also no more acquisitions, the income to cover interest is something around $70 million. At any rate, interest coverage is very low for INN, it's actually less than 1x. The debt is definitely very high and investors should take note of that, even if technically the FFOs are quite positive. It also leads to a reasonably low price for the REIT at around 7x P/FFO which is not high. However, it's because of the strain and leverage imposed by the debt. With recreational expenditure ultimately being discretionary, there are still risks that declines in activity occur over the coming 6-12 months, which would likely lead to strain on the stock as markets clearly recognise that the balance sheet is somewhat heavy. Overall there are too many concerns, and debt can be mortally dangerous for investors.

For further details see:

Summit Hotel Properties: A Lot Of Debt