INN - Summit Hotel Properties: Well-Covered Dividends; Attractive Valuation

2023-08-09 17:34:53 ET

Summary

- Summit Hotel Properties is a select-service hospitality REIT with a portfolio of 100 hotels and 15,000 rooms.

- The company has a conservative dividend payout ratio, with the potential for further increases.

- The company's stock is also undervalued compared to its peers, making for an attractive investment.

Introduction

I have written about several hospitality REITs in recent months, with my most recent article on Braemar Hotels & Resorts ( BHR ), a full-service hospitality REIT. Similarly, the focus of this article, Summit Hotel Properties ( INN ), is a hospitality REIT as well. Unlike Braemar Hotels & Resorts, however, Summit Hotel Properties is a select-service REIT.

I last covered Summit Hotel Properties a few months ago , after the company had announced its earnings for Q1 2023, with a "Buy" rating for the company. Unfortunately, the stock hasn't performed as I had hoped, with a 9% loss compared to a 6.5% gain for the S&P 500 over the same period. Nevertheless, the release of the company's Q2 2023 earnings last week gives me the opportunity to re-evaluate the company to determine if my rating for the company remains a "Buy".

Seeking Alpha

The Portfolio

Summit Hotel Properties is a select-service hospitality REIT, which has a more streamlined operational structure compared to full-service and luxury REITs. This structure, characterized by a focus on providing essential room offerings rather than an array of amenities, provides several benefits. By concentrating on the core aspect of rooms, capital requirements are reduced, resulting in a leaner cost structure and ultimately higher operating margins.

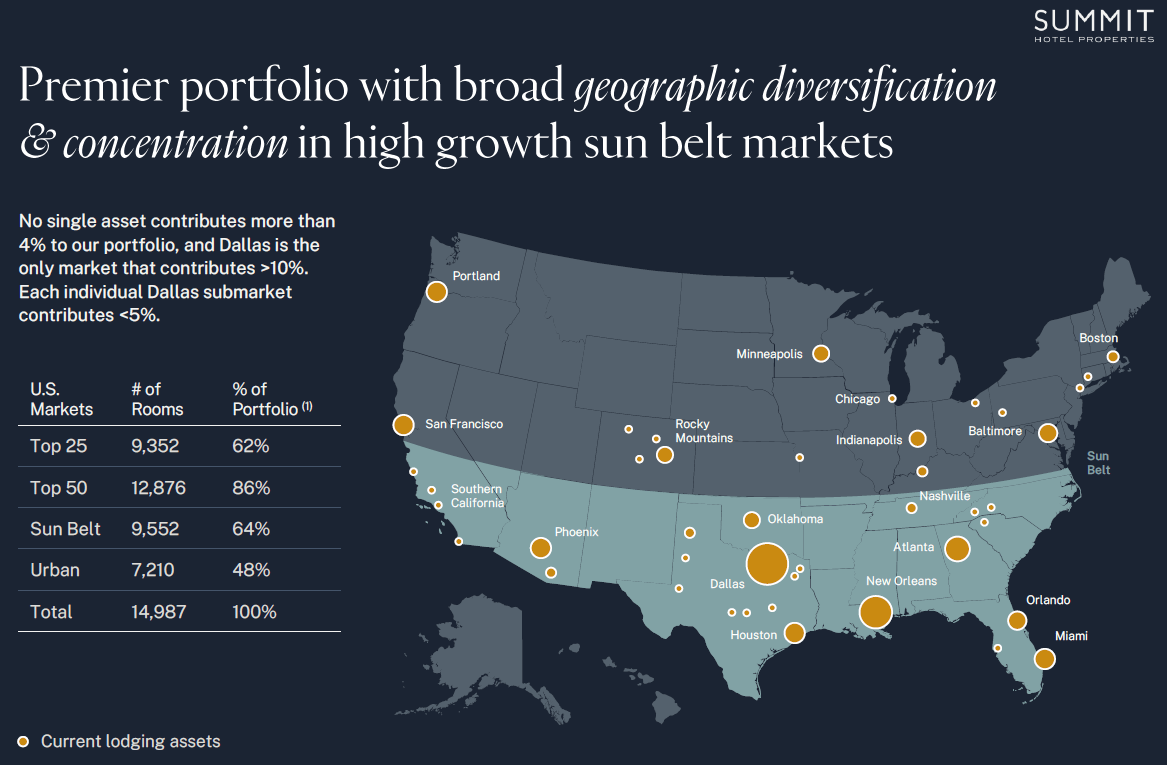

As at Q2 2023, the company's portfolio comprises close to 15,000 rooms in 100 hotels. These hotels are geographically diversified throughout the country, with no single hotel contributing more than 4% to the company's portfolio. Crucially, a significant portion of the company's portfolio is located in regions with a high population density, ensuring strong demand. The majority of the portfolio operates under prestigious names like Marriott, Hilton, Hyatt and IHG, reinforcing the quality and reliability of the company's hotels.

{kind=link}

Q2 2023 Earnings

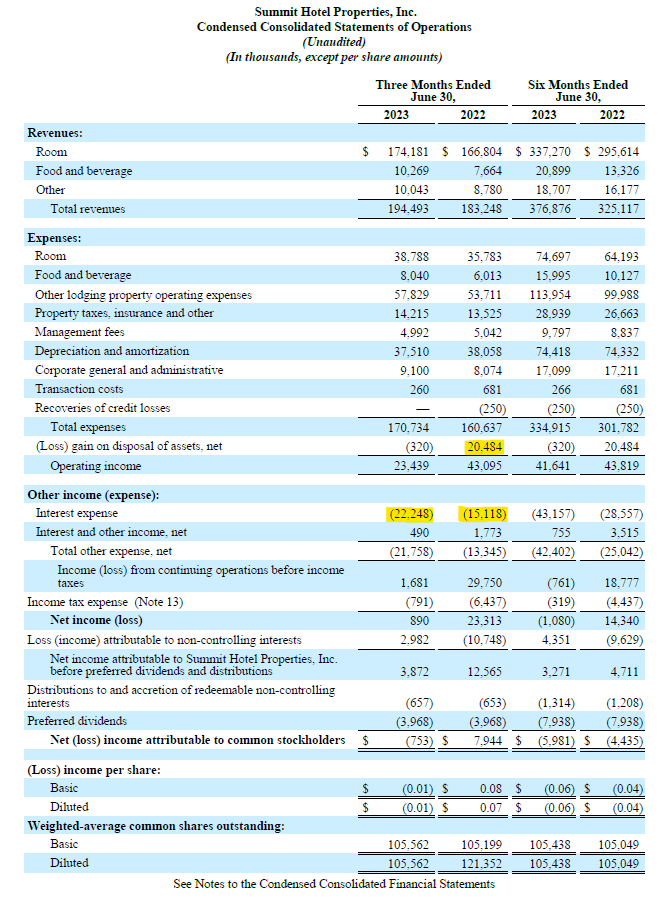

The company released its Q2 2023 earnings results last week, reporting a net loss of $0.8 million or $0.01/share. This is in stark contrast to the same period the previous year, which saw a net income of $7.9 million, or $0.07/share. It should be noted that in Q2 2022, the company experienced a significant boost to its bottom line due to a gain on disposal of assets of approximately $20.5 million. Additionally, there was a substantial increase in the company's interest expense, largely due to the rising interest rates over the past year. Nevertheless, the company remained in an operating profit, with the main factor for its net loss stemming from the preferred dividends.

The company's revenue per available room (RevPAR) reached a new high since the onset of the pandemic. This growth in RevPAR was driven by both an increase in occupancy rates as well as an increase in the average daily rate (ADR). Apart from this, the company also saw improvements in various key metrics, which bodes well for the future.

{kind=link}

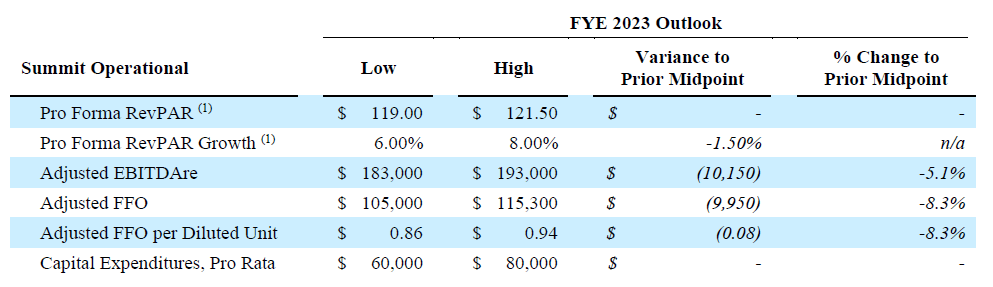

The company's performance in terms of adjusted funds from operations ((AFFO)) remained relatively stable, reporting an AFFO of $33.2 million or $0.27/share compared to the $32.6 million or $0.27/share reported in Q2 2022. However, it should be noted that the company has lowered its outlook for the FY 2023. The revised guidance indicates an AFFO of between $0.86/share and $0.94/share, with the midpoint of $0.90/share an 8% decrease from the previous projection. During the earnings call , management highlighted the reason for the revised guidance:

Roughly 7 months into the year, we have seen demand patterns across the industry normalize to more typical seasonal trends. While leisure demand remains strong in any normal historical context, a portion of last year's highly resort-oriented compressed demand is finding alternatives in urban markets, cruises and abroad.

And while urban markets broadly continue to recover, several markets within our portfolio continue to experience typically soft demand trends, most notably San Francisco, San Jose and Minneapolis. We are maintaining the low end of our RevPAR growth guidance range while reducing the midpoint by 150 basis points to 7%. The midpoint of our adjusted EBITDAre guidance range is being reduced by approximately 4% after adjusting for second quarter transaction activity that reduced our full year adjusted EBITDA by approximately $2 million.

Our guidance range assumes easier expense comparisons in the second half of the year when current operating models better align with last year's practices, but we continue to operate in a tight labor market that we expect to pressure margins. For the full year, we expect operating margins to be roughly flat at the high end of our guidance range and down approximately 150 basis points at the low end.

{kind=link}

Balance Sheet

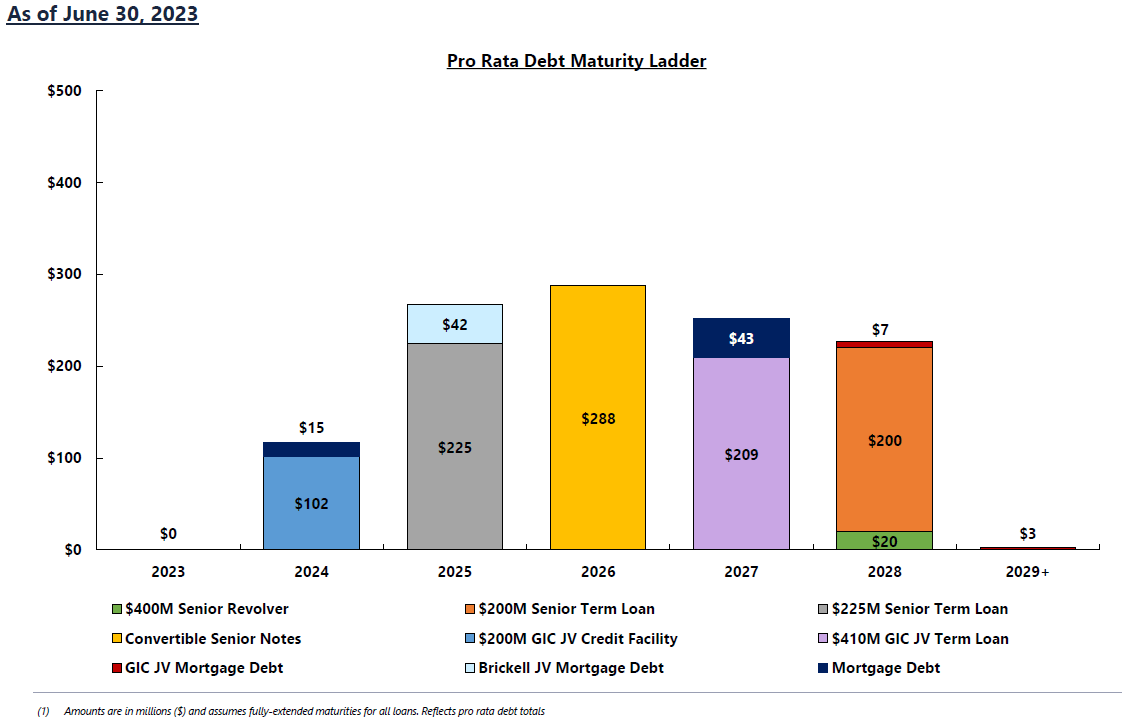

As of Q2 2023, Summit Hotel Properties has a total debt of approximately $1.2 billion and a liquidity of $420 million. Around 74% of this debt is fixed at an interest rate of approximately 4.8%, a relatively low and favorable rate given the prevailing interest rate environment. The remaining 26% of the debt is floating rate, which is subject to fluctuations in the interest rate. Notably, during the quarter, the company refinanced its $600 million senior unsecured credit facility , with the new maturity date, assuming all extension options are utilized, set for June 2028. This has contributed to an increase in the company's average length to maturity of the debt to over 3 years.

The company's debt obligations are fairly spread out over the next few years. Crucially, the company has no debt due until Q4 2024, over a year from now. Without the immediate need to fulfill its debt obligations, the company seems well-positioned to be able to utilize its existing liquidity for future growth prospects if the opportunity arises.

{kind=link}

Dividend

Earlier this year, the company raised its quarterly dividend by 50%, from $0.04/share to $0.06/share. The company has maintained this dividend for the second quarter as well, resulting in an annualized dividend of $0.24/share. With the latest share price hovering around $5.90, this gives the company a forward dividend yield of slightly over 4%.

The company has a very conservative dividend payout ratio of 22%. In fact, the AFFO generated in Q2 2023 alone is able to cover the entire annual dividend of $0.24/share. This not only highlights the safety of the company's dividend, it also positions the company strongly for potential dividend increases in the future. This was hinted at during the earnings call, when it was mentioned that the current dividend payout ratio was "prudent" and that there was "room for increases over time".

While the company's current quarterly dividend of $0.06/share still falls short of its pre-pandemic level of $0.18/share, the fact that the company had increased its dividend recently and has hinted at the possibility of further increases bodes well for the future.

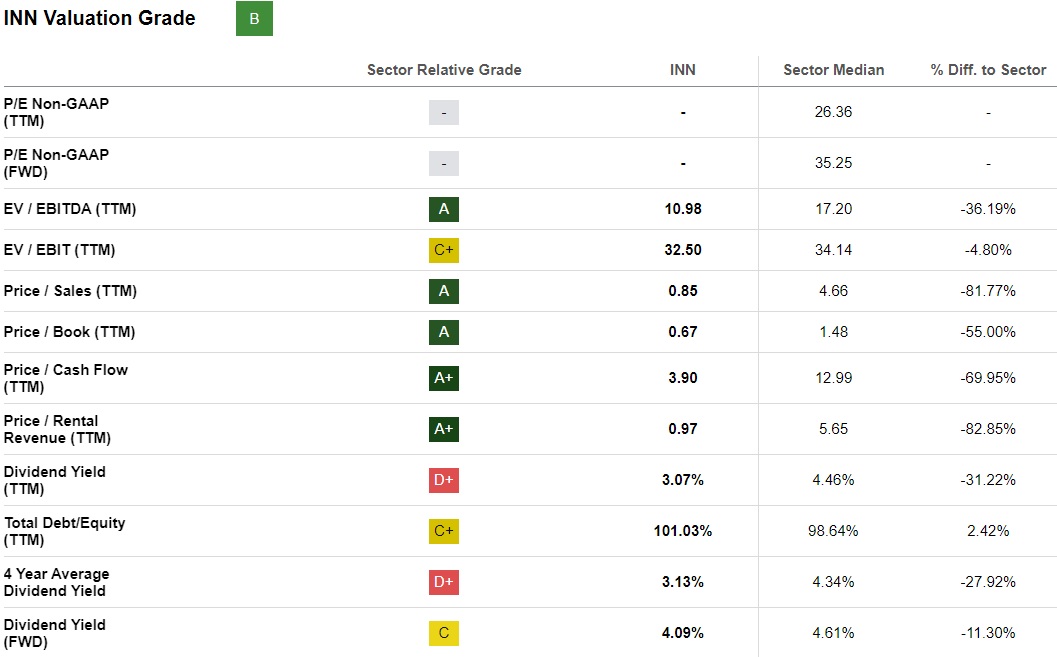

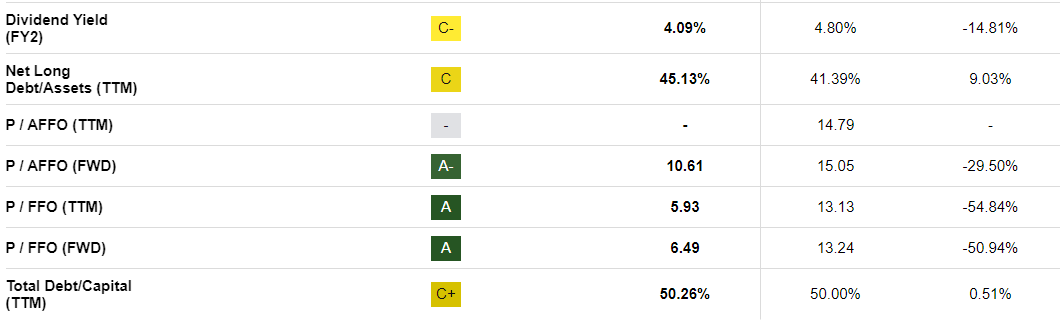

Valuation

The Seeking Alpha quant system gives the company a "B" for valuation. Interestingly, the company excels in certain valuation metrics, with an "A" for both its price-to-book ratio (P/B ratio) and price-to-AFFO (P/AFFO ratio). Both of these metrics are substantially below that of its peers in the hospitality sector, indicating an undervalued stock.

The main factor that gives the company a "B" rating instead of "A" is its dividend yield, which received a "D+" from the system. This is because the company's dividend yield, while still at a respectable 4%, is comparatively lower than its peers. Nevertheless, as previously established, management has demonstrated both the capability and the inclination to increase its dividends, thus this should not be an issue.

{kind=link}

{kind=link}

Conclusion

Summit Hotel Properties had a decent second quarter, seeing improvements in various key metrics. The company has also taken steps to manage its debt schedule, with no obligations due until the end of next year. While the company did lower its guidance for the rest of the year, this should not affect its dividends. Given the company's conservative dividend payout ratio, the company is certainly able to increase its dividends in the near future. Additionally, the company's shares are undervalued compared to its peers, which makes the current entry point an attractive one. While the company's share prices have decreased since my last article, I have seen no change in the company's fundamentals that will affect my original rating on the company. Hence, I continue to rate this company a "Buy".

For further details see:

Summit Hotel Properties: Well-Covered Dividends; Attractive Valuation