CMTOY - Summit Materials And Cementos Argos Merger: Potential Value Accretive Deal

2023-09-09 07:39:12 ET

Summary

- Summit Materials shares dropped 7.2% after announcing a merger with Argos USA, but the deal is appealing.

- Summit Materials is a major player in the construction materials market in the US, providing aggregates and cement, but its move in the direction of more cement is interesting.

- The merger with Argos USA should generate significant synergies, but even without those the deal is logical.

September 7th ended up being a very interesting day for shareholders and market watchers of Summit Materials (SUM). Shares of the company plunged, dropping 7.2%, after news broke that the business had agreed to merge with Argos USA, a subsidiary of Cementos Argos ( CMTOY ), in a multibillion dollar cash and stock transaction. Although the market has a negative view of this development, my overall assessment is that, at worst, the deal is fine. And at best, it is quite appealing. Based on these factors, combined with how shares of Summit Materials are priced already, I believe that a soft ‘buy’ rating is appropriate for the firm at this time.

A brief refresher on Summit Materials

Before we get into the fun side of this article, it might be helpful to dig in a bit to understand more about Summit Materials and what it does. At its core, the company is a vital player in the construction materials market in the US. It essentially provides customers with aggregates and cement, both of which are necessary in order for many construction related activities like the building of roads, the construction of skyscrapers, and more, to take place. As of the end of the 2022 fiscal year, the company considered itself to be in the top 10 largest suppliers of aggregates in the country and to be in the top 15 when it comes to cement production. It also produces ready-mix concrete and asphalt paving mix. All combined last year, the company was responsible for extracting and selling 59.5 million tons of aggregates, 2.5 million tons of cement, 5 million cubic yards of ready-mix concrete, and 3.7 million tons of asphalt paving mix from the roughly 400 sites and plants that it has in operation.

{kind=link}

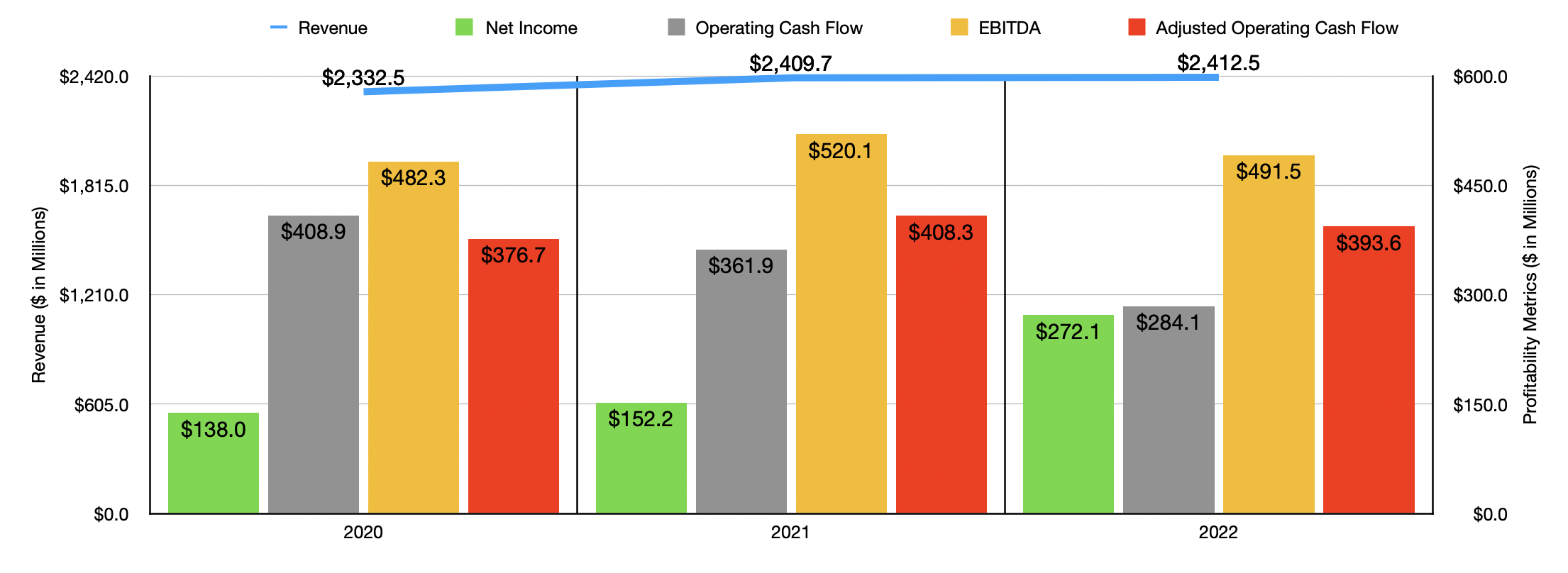

In recent years, financial performance for the business has been decent, but not great. Revenue has risen year after year, climbing from $2.33 billion in 2020 to $2.41 billion in 2022. Management has been working on a major project called ‘Elevate Summit’, which has been focused on significantly improving the company's competitive position and boosting profitability. We do know that, over the past three years, net profits have grown from $138 million to $277.1 million. Other profitability metrics, however, have been mixed. Operating cash flow has actually declined from $408.9 million to $284.1 million. Though if we adjust for changes in working capital, we would see that it has remained more or less flat at between $376.7 million and $408.3 million. A similar trend can be seen, in the chart above, when it comes to EBITDA.

{kind=link}

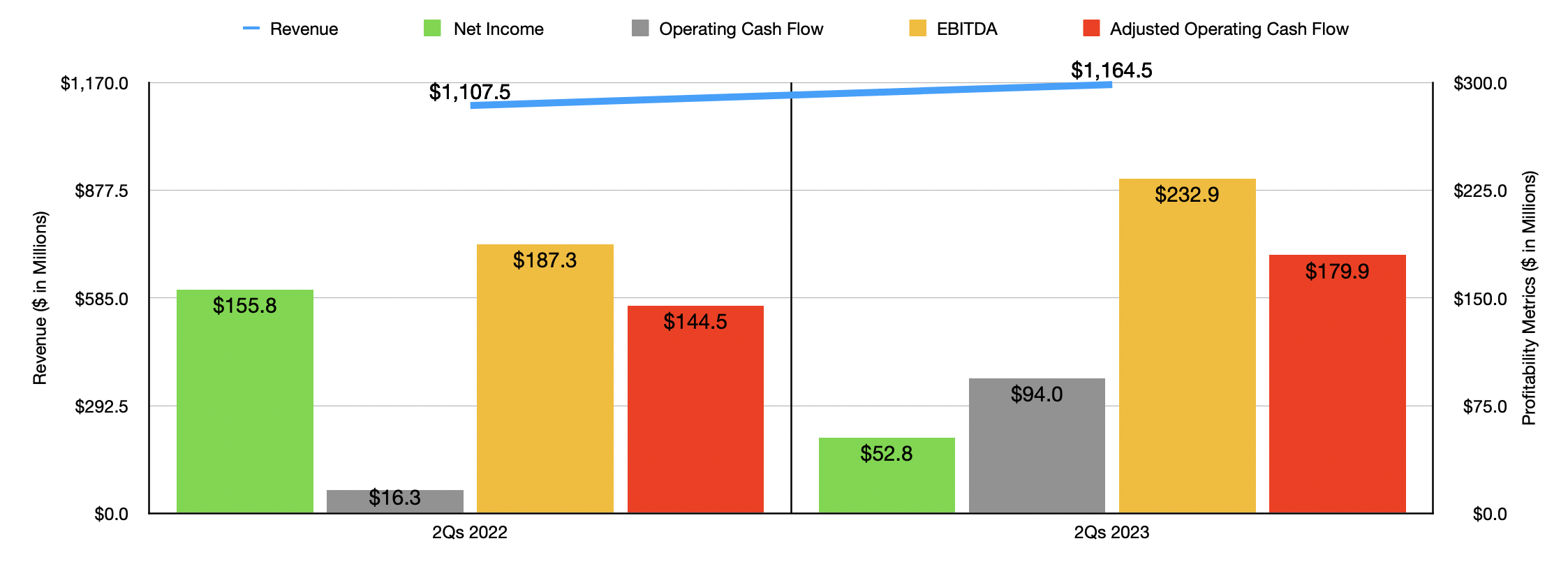

This year, the picture for the company has definitely been improving. Revenue of $1.16 billion beat out the $1.11 billion reported for the first half of 2022. It is true that net profits declined from $155.8 million to $52.8 million. But the big portion of this change involved a $170.3 million gain on asset sales that the business recorded in the first half of last year. Operating cash flow actually managed to jump from $16.3 million to $94 million. And on an adjusted basis, that metric grew from $144.5 million to $179.9 million. Meanwhile, EBITDA jumped from $187.3 million to $232.9 million.

A transformative transaction

In an effort to accelerate its transformation , the management team at Summit Materials announced, on September 7th, that the company had agreed to merge with Argos USA in a deal valued at $3.2 billion. This transaction will involve Summit Materials paying to Argos USA’s parent company, Cementos Argos, $1.2 billion in cash and transferring over 54.7 million new shares of stock that is valued at around $2 billion as of the close of business on September 6th. Upon completion of the merger, which is expected to occur in the first half of 2024, Cementos Argos will own 31% of the combined company while current shareholders of Summit Materials will own the remaining 69%.

{kind=link}

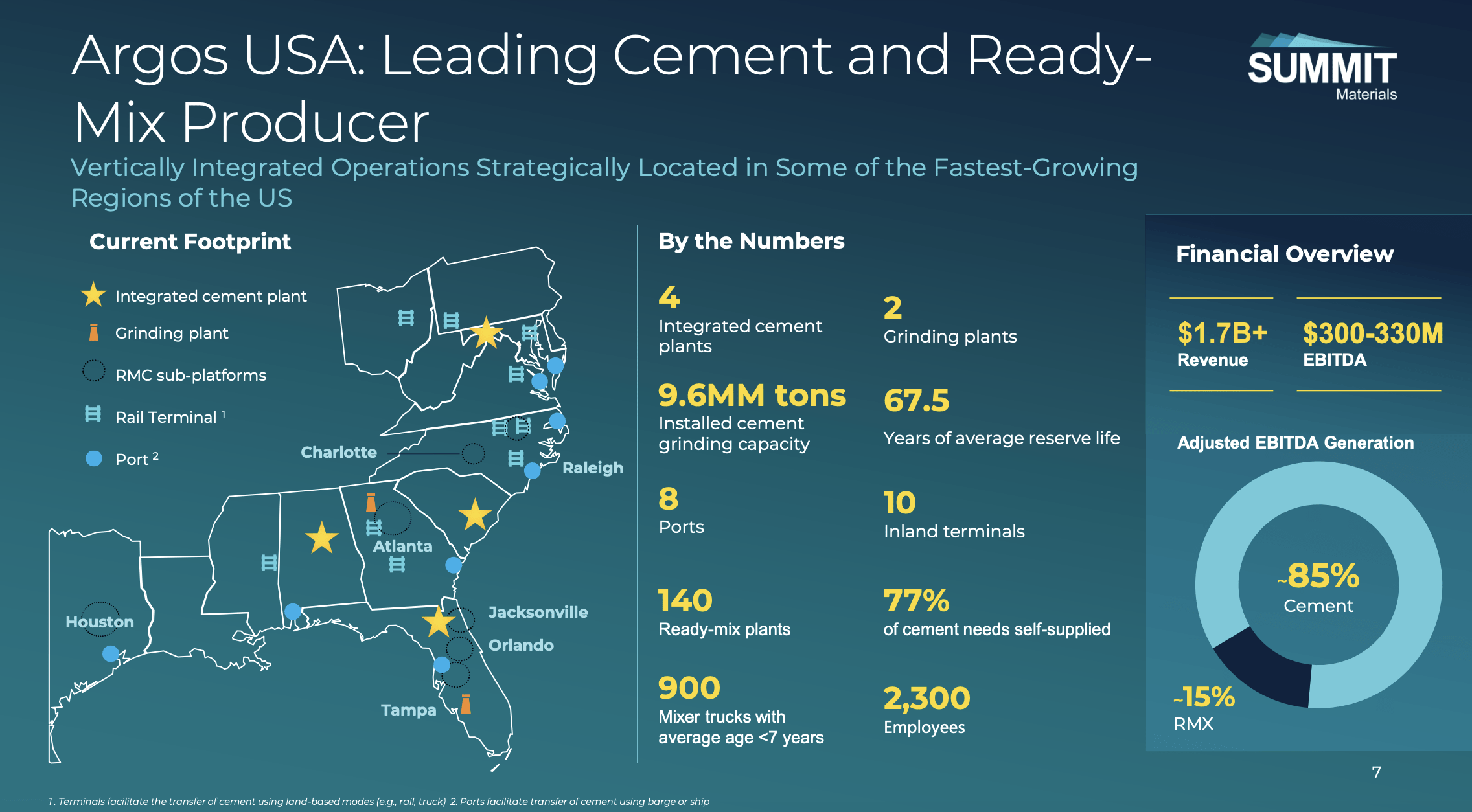

Operationally speaking, this transaction makes a lot of sense. Argos USA is a major company that's focused largely on the production of cement. Amongst other assets, it owns 140 ready mix plants, 4 integrated cement plants, 8 ports, 10 inland terminals, and 2 grinding plants. All combined, the company has 9.6 million metric tons of installed cement grinding capacity, and it boasts material reserves of 67.5 years. Its operations are focused largely across many southern states, ranging from Texas through South Carolina. It also has operations in Ohio, Pennsylvania, West Virginia, Virginia, and North Carolina. These represent some of the fastest growing states in the country, and that trend is unlikely to change. Based on management's own estimates, Argos USA generates over $1.7 billion worth of revenue each year, and it generates EBITDA of between $300 million and $330 million. Of this, 85% comes from its cement operations, with the remaining 15% attributable to its ready-mix business.

{kind=link}

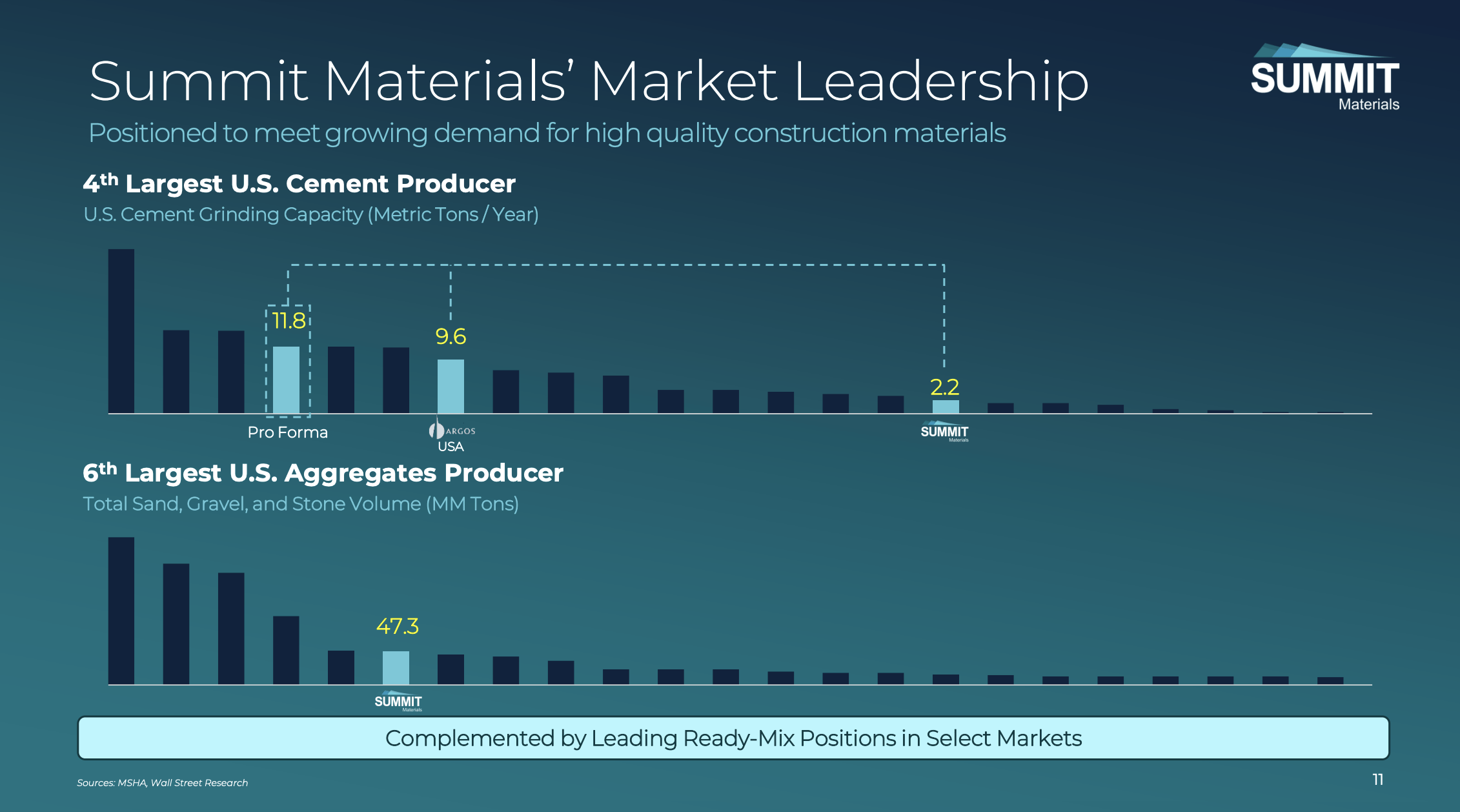

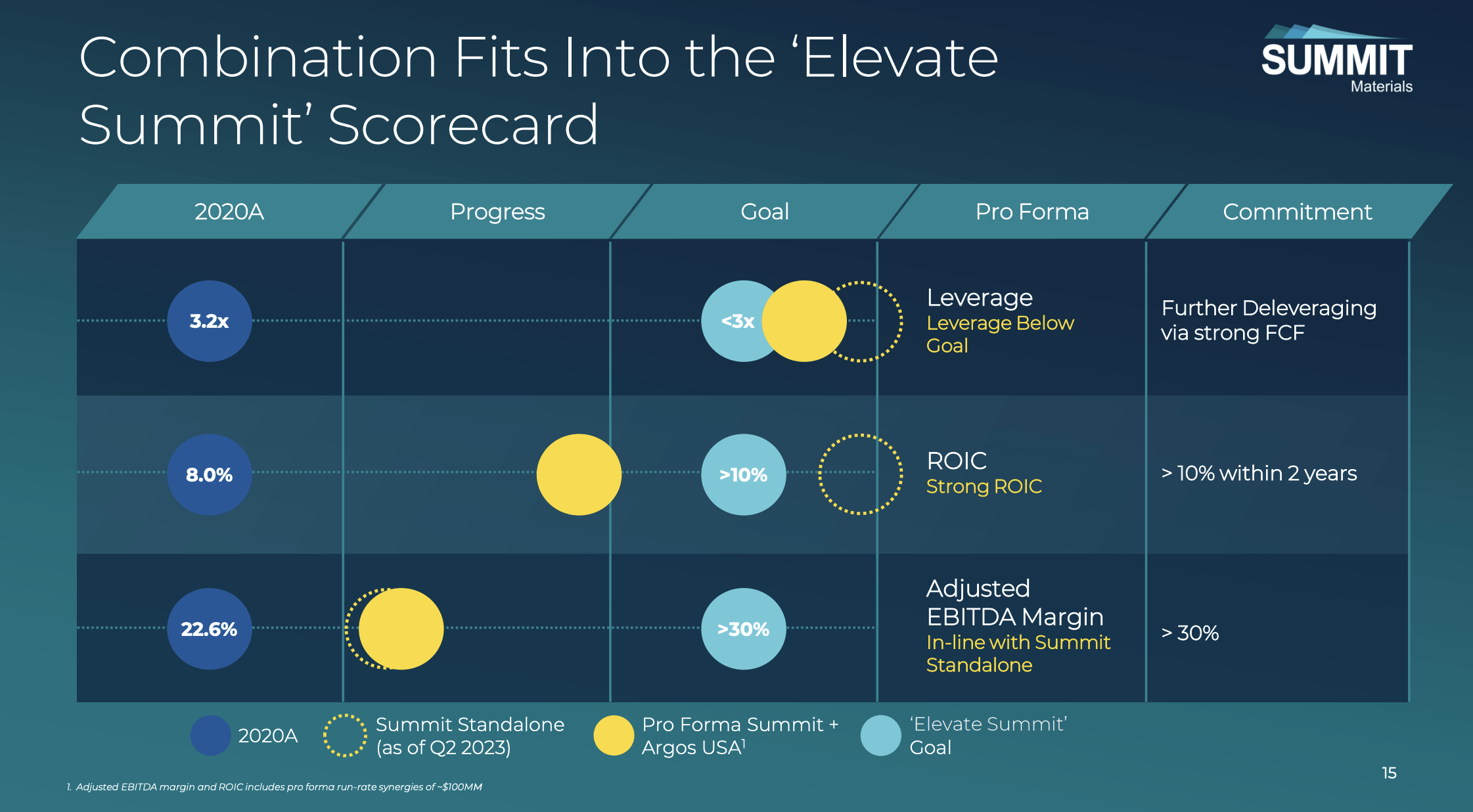

On its own, Argos USA is the 7th largest producer of cement in the country. But when you add the 9.6 million metric tons of output that it's responsible for each year to the 2.2 million metric tons put out by Summit Materials, that will increase total capacity to 11.8 million. That would make it the 4th largest player in the US market. With its dedication to the aggregate space, the combined company will remain the 6th largest aggregates producer in the country. As I mentioned earlier in this article, Summit Materials is currently undergoing a transformation. As you can see in the image below, this transaction will help to reduce leverage while growing the company’s EBITDA margin. It will, unfortunately, reduce the company’s return on invested capital. But management still believes that achieving its target of more than 10% is possible within the next two years.

{kind=link}

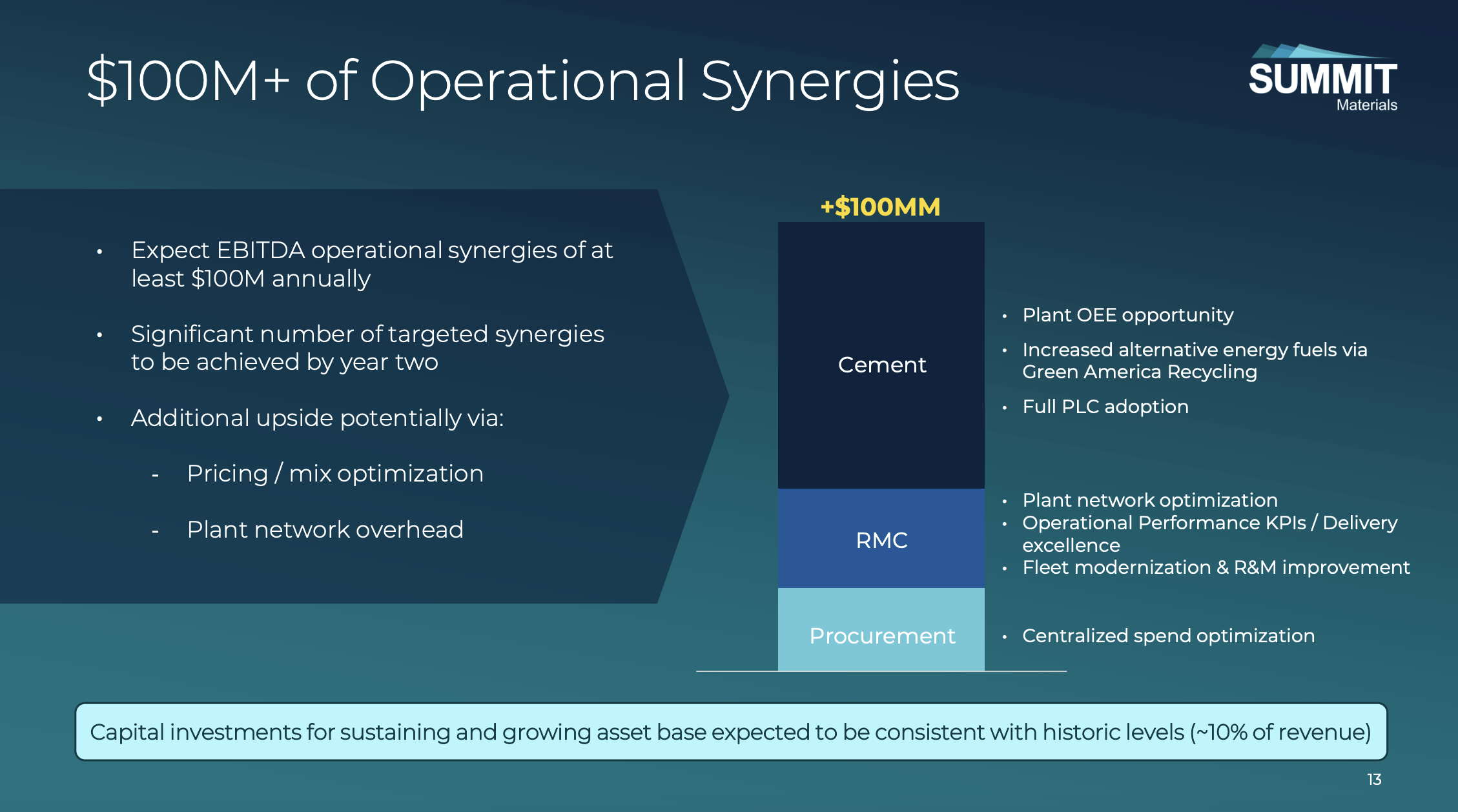

As with any major financial transaction, synergies are being forecasted. Management expects to achieve $100 million in annual run rate synergies within two years of the deal closing. Even if this does not come to pass, the transaction could still be quite logical. At present, Summit Materials believes that its EBITDA this year will be between $550 million and $570 million. At the midpoint, that is $560 million. The midpoint for Argos USA is $315 million. Even if we ignore the prospect of the other $100 million of potential cost savings, that brings us up to $875 million annually. 64% of that $875 million number comes from Summit Materials. And yet, shareholders of Summit Materials get 69% of the combined business. If we assume that the full $1.2 billion in cash is funded by debt, and we use a 6% interest rate that is in line with current financing on the company's books, we would end up with operating cash flow of $243 million for Argos USA. That compares to my estimate for Summit Materials of $448.5 million. If this comes to fruition, then Summit Materials would be responsible for 64.9% of the combined company’s operating cash flow.

{kind=link}

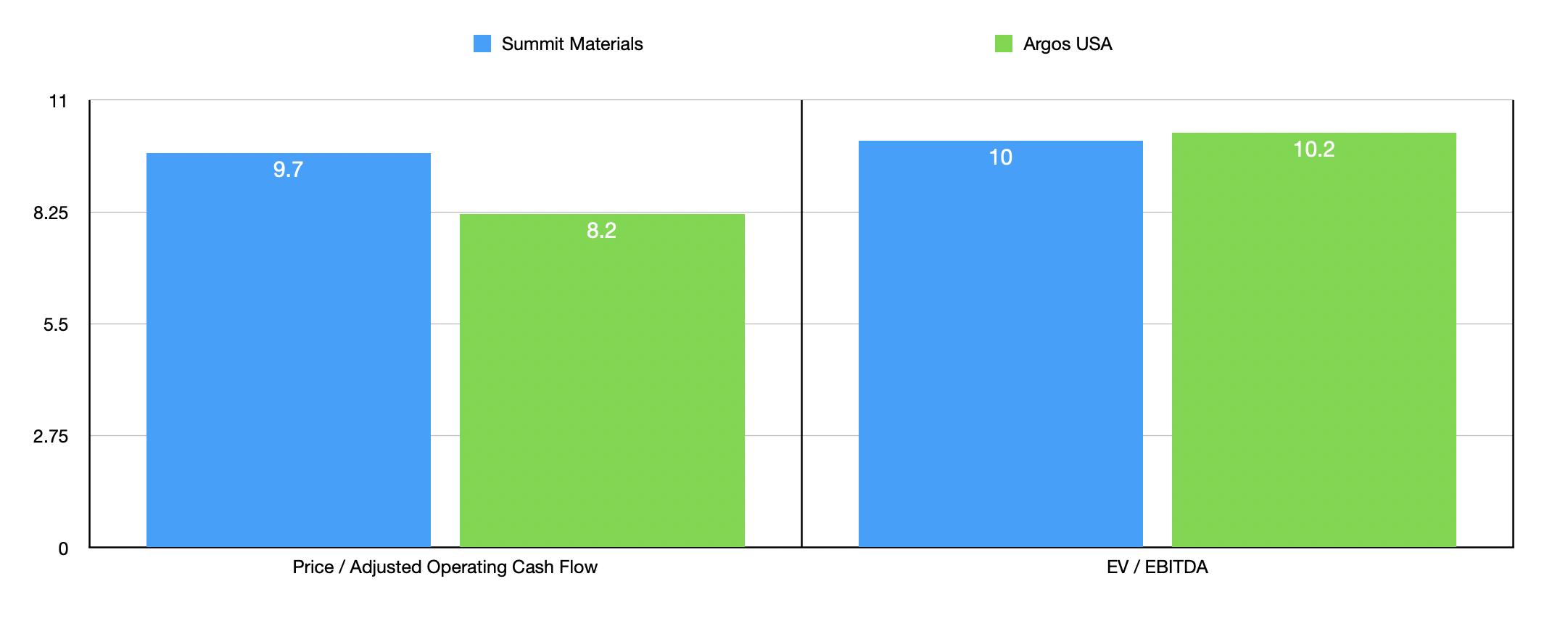

Another way to look at this is through the lens of valuation. Using the forward estimates, Summit Materials is trading at a price to adjusted operating cash flow multiple of 9.7, and it is trading at an EV to EBITDA multiple of 10. Based on my own calculations, these numbers for Argos USA are 8.2 and 10.2, respectively. So the purchase is a bit more expensive on an EBITDA basis. However, it is definitely cheaper on an operating cash flow basis. Between the two, I prefer the latter.

{kind=link}

Takeaway

All things considered, this looks to be an interesting and potentially value accretive deal for Summit Materials. It's not a fantastic deal unless the synergies come to fruition. But even if they don't, I can see that this makes decent financial sense. Because of this, I've decided to rate Summit Materials a soft ‘buy’ at this time.

For further details see:

Summit Materials And Cementos Argos Merger: Potential Value Accretive Deal