SUM - Summit Materials: Cyclical Market Exposure Keeps Me On The Sidelines

2023-04-24 10:54:34 ET

Summary

- Summit Materials should witness a slight decline YoY in the topline in FY2023 due to a slowdown in the residential end market.

- I anticipate margins to remain flat YoY in the coming quarters.

- Summit Materials' near-term headwinds and cyclical end-market exposure keep me on the sidelines.

Investment Thesis

Summit Materials, Inc. (SUM) is expected to witness a slight decline YoY in net sales in FY2023, due to a slowdown in the residential end market. Moreover, I expect no improvements in the margins due to volume deleverage outweighing the benefits from positive price/cost and SUM’s strategy in the coming quarters. The company’s exposure to cyclical end markets and potential risks from macroeconomic worsening keeps me on the sidelines.

Revenue Analysis & Outlook

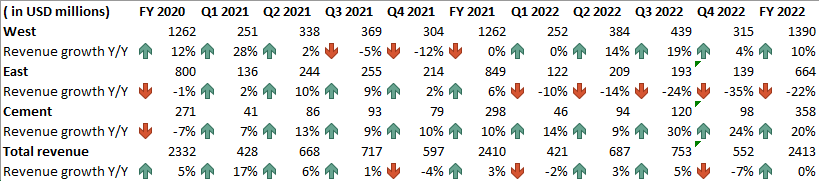

Summit Materials saw a YoY increase in total revenue in FY2021, with aggregates, cement, and ready-mix driving growth due to healthy demand conditions in end markets. While the organic volume growth was positive overall for the year, net sales declined YoY in the second half of FY2021 due to divestiture impacts. Moving into FY2022, there was a different scenario as organic sales volume decreased YoY across aggregates, ready-mix, and asphalt businesses. However, the revenue growth was fueled by price hikes, which more than compensated for the decline in volume sales.

SUM's Historical Revenue Growth (Company data, BI Insights )

{kind=link}

Declining sales volume

The residential end market is expected to face a slowdown in demand due to high-interest rates. To combat inflation, Federal Reverse have increased interest rates, which should create affordability concerns and discourage potential buyers from investing in new homes. Moreover, housing starts (a leading indicator of the residential end market) stood at a decline of ~17% YoY , as of March 23, also indicating lower near-term demand for the residential end market in the coming quarters.

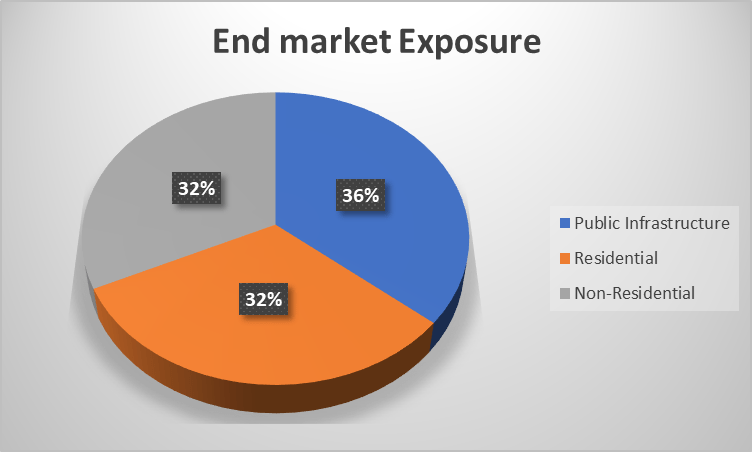

The non-residential end market is further divided into the heavy and light non-residential markets. I anticipate demand in heavy non-residential should be healthy, driven by onshoring of manufacturing facilities. Over a few years, supply chain disruption has impacted many industries across the USA, to mitigate these issues companies have started on-shoring critical parts manufacturing which calls for the construction of new facilities. For instance, spurred by CHIPS Act , Micron ( MU ) has announced $40 billion in investments in memory chip manufacturing. On the contrary, the light non-residential market is likely to face challenges in the coming quarters due to a slowdown in the residential end market. Development in the residential communities is very crucial for the construction in the hospital, retail, and hospitality sector. So a slowdown in the residential end market should have a subsequent negative impact in the light non-residential market.

Furthermore, I expect a positive trend of growth in the infrastructure end market in FY2023, driven by increased DOT’s budget and the Infrastructure Investment & Jobs Act (IIJA) . The 5 top states of SUM which account for 65% of net sales have increased their DOT budget by an average of 18% YoY for 2023. This should provide good growth opportunities for Summit Materials. Additionally, the US government has also announced IIJA which will invest $110 billion of new funds for roads, bridges and major projects. According to the management, the funds from IIJA should flow through in the second half of FY23 which should be beneficial for SUM’s top line.

For the FY2023 outlook, the management of SUM expects a 30% YoY decline in the sales volume of the residential end market, flattish YoY sales volume in the non-residential end market and mid-single-digit sales volume growth in the infrastructure end market. Considering the end market exposure, I anticipate overall sales volume should be down YoY in FY2023.

SUM's End Market Exposure (Company data, BI Insights )

{kind=link}

Benefits from Pricing Actions

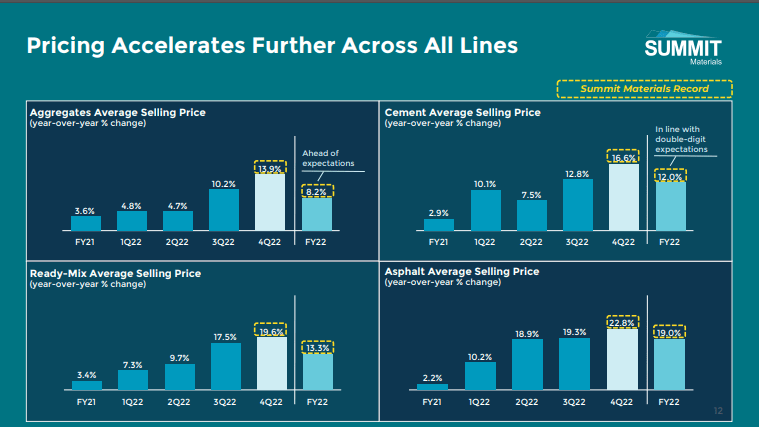

Throughout FY2022, SUM has increased prices across all its business lines to mitigate higher input costs. In the fourth quarter of FY22, the company increased ASP of aggregates by 13.9% YoY, followed by a 16.6% YoY increase in cement, a 19.6% YoY increase in Ready-Mix and a 22.8% YoY increase in the ASP of Asphalt. Therefore, I believe the carryover impact from previous price increases should benefit the company in a year-over-year net sales comparison.

Investor Presentation; Summit Materials

{kind=link}

Hence, I anticipate the positive impact of pricing actions should be more than offset by a decline in sales volume in the coming quarters. As a result, it is likely that there will be a slight year-over-year decrease in net sales for SUM in FY2023.

Margin Analysis Outlook

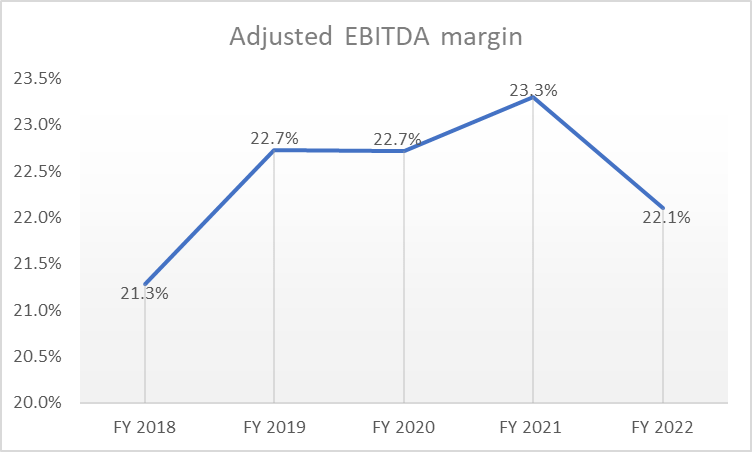

Summit Materials faced a decline of 120 bps YoY in the adjusted EBITDA margin in FY2022. This was primarily attributed to higher fuel, material, and energy costs which were driven by supply chain disruptions. Despite these challenges, the company was able to offset some of the negative impacts through price increases and portfolio optimization, including the divestiture of less profitable businesses and acquiring higher-margin businesses.

SUM's Historical margin (Company data, BI Insights)

{kind=link}

Looking ahead, I anticipate that there should be no improvements in the margins of SUM in FY23 as benefits from positive price/cost and SUM’s strategy should be offset by volume deleverage. The input cost inflation in fuel prices and energy costs has already reached its peak and now they have started to decline. This should help the company to achieve positive price/cost which should be accretive to the margins. Even if input cost inflation in labor and material persists, the management expects to increase the prices of its products and services to establish positive price/cost.

Furthermore, SUM is continuing with its North Star strategy which includes shifting the business portfolio mix towards material-led businesses. In this strategy, the company plans to divest lower-margin downstream businesses like services business (Gross profit margin - 17.4% as of FY22) and acquire higher-margin material-led businesses like aggregates (Gross profit margin - 48.5% as of FY22) and cement (Gross profit margin - 39.6% as of FY22).

On the other hand, volume is expected to be down (as previously explained in the revenue section) in FY2023 due to a slowdown in the residential end market which should result in volume deleverage and negatively impact the margins.

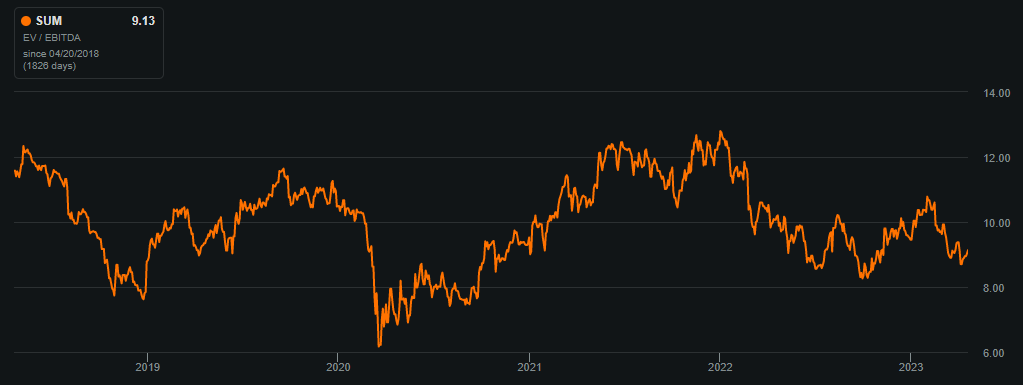

Valuation

During the last 10 years, the company had traded at an EV/EBITDA ((TTM)) level of ~6.17x (at the lower end of the range) in 2020 and at ~12.34x (higher end of the range) during 2018. SUM's stock is currently trading at an EV/EBITDA ((TTM)) of 9.12x which is in line with its 5-year average EV/EBITDA of 9.81x. Upon comparison to the sector median, the company is trading at a premium. The sector median EV/EBITDA is 8.04x which is approximately 12% lower at which SUM is trading.

SUM's EV/EBITDA (Seeking alpha)

{kind=link}

Conclusion

Summit Materials is a company that operates in end markets that are cyclical in nature indicating that the demand for their products and services tends to fluctuate with the overall economic conditions. While SUM is a good company, its cyclical end market exposure and potential risks from high-interest rates & worsening macroeconomic conditions could potentially have a negative impact on the performance of SUM’s stock. Moreover, the stock is trading in line with its 5-year average, leading me to conclude that it is reasonably priced and best to remain on the sidelines for now.

For further details see:

Summit Materials: Cyclical Market Exposure Keeps Me On The Sidelines