SMLP - Summit Midstream Partners: Can It Survive Low Utilization?

2023-06-06 05:06:04 ET

Summary

- Summit Midstream Partners continues to struggle with low utilization, even though capital spending is ramping up. However, the company remains profitable.

- The company has no way to handle paying off its debt due in 2025-2026 and it will need to roll it over. That's dangerous in a high-interest rate environment.

- The company's management is great and showed a def ability to handle 2020. That, combined with its valuation, makes the company an incredibly valuable investment.

Summit Midstream Partners ( SMLP ) is a strong midstream company with a tiny $160 million market capitalization. The company's debt load dwarfs its market capitalization, and it's remained that way since the COVID-19 capex collapse, when the company almost went bankrupt. However, the company has worked hard to recover, and with a strong management, we expect it to be able to drive substantial shareholder returns.

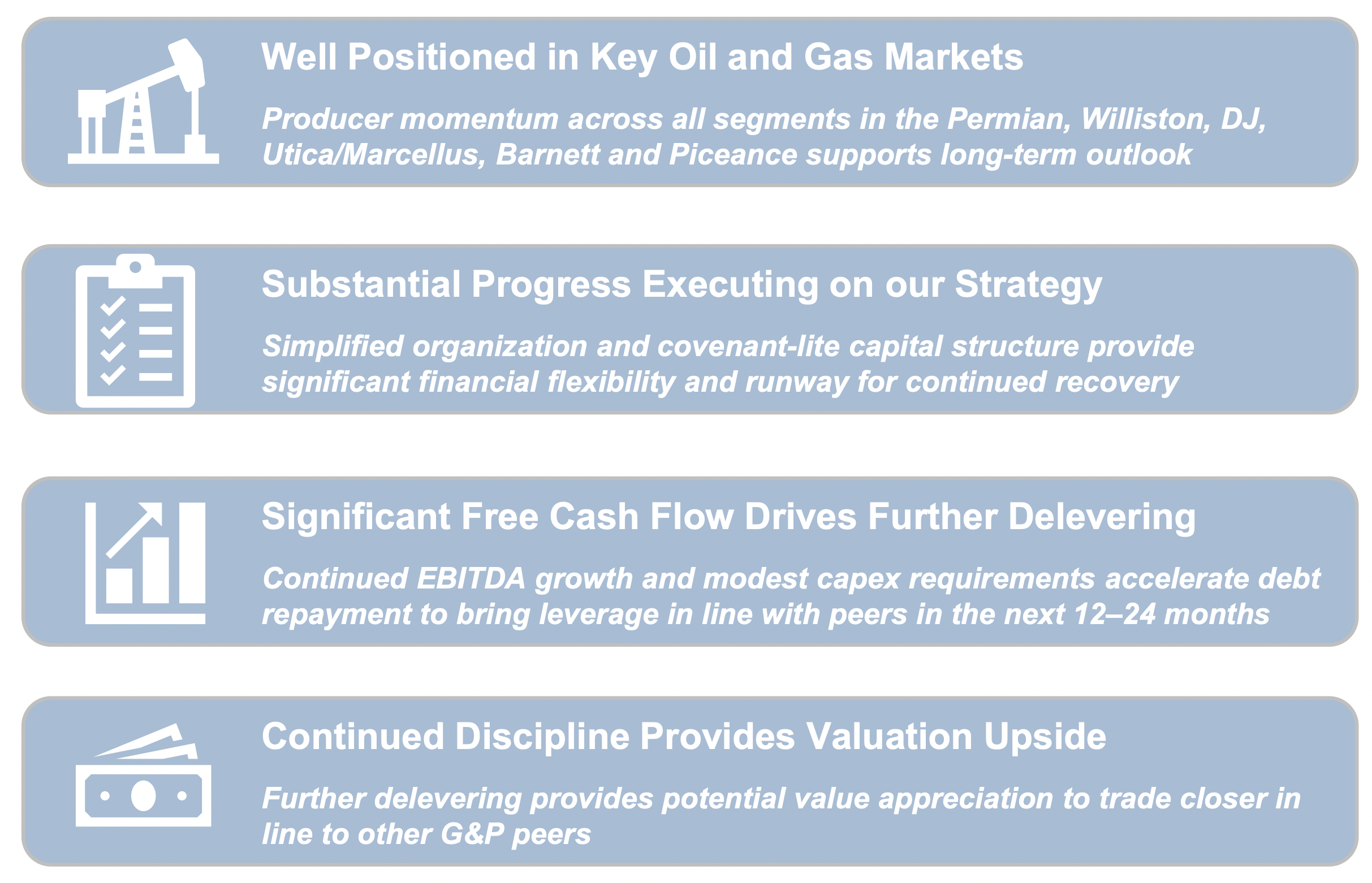

Summit Midstream Partners Highlights

The company has continued to perform well, and has a number of highlights that justify investing.

{kind=link}

The company remains incredibly well positioned in the industry. It has continued to see strong momentum and it has a long-term forecast for its assets. The company needs to see capital expenditures continue to grow, but at the end of the day, it's actively generating strong FCF. It expects to be able to bring leverage in line with peers in the next 12-24 months.

The company has an incredibly strong management team, one that showed a strong ability to handle the last downturn, which we expect will continue.

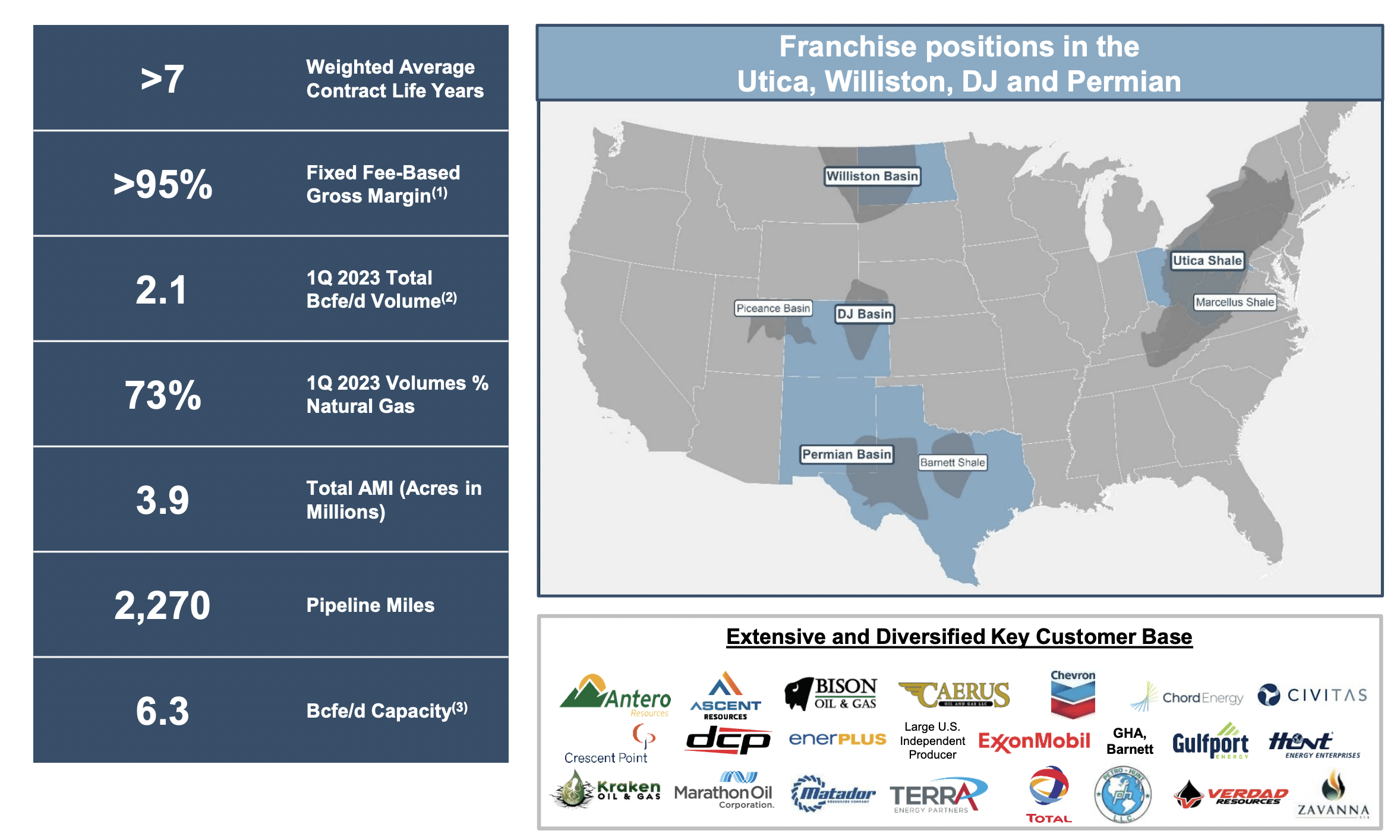

Summit Midstream Partners Overview

Overall, the company still has a reasonably strong portfolio of assets, that it's continued to grow.

{kind=link}

The company's assets have a >7 year average contract life with >95% fixed fee-based gross margin. The company had 2.1 billion cubic feet / day in total volume through the quarter with 73% natural gas volumes. The company has 3.9 million acres across 2270 pipeline miles. However, the company's key struggle is still that last number.

The company has 6.3 billion cubic feet / day in capacity. Underutilization is massive. The company needs a path to fixing that.

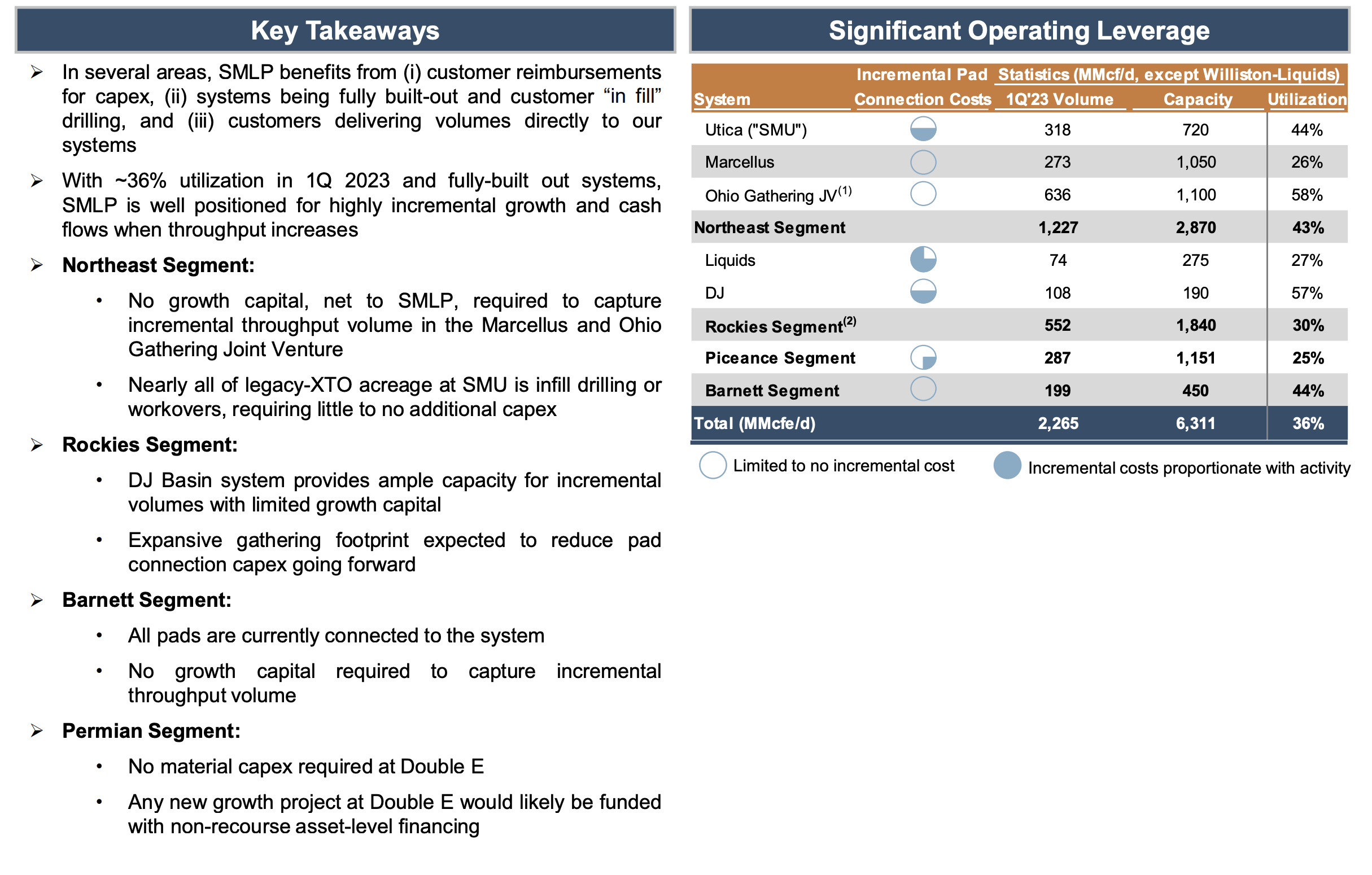

Summit Midstream Partners Utilization

The company's recent Double E pipeline in the Permian Basin is relatively much stronger. ExxonMobil's 30% ownership stake will help protect that.

{kind=link}

The company does have one benefit in its portfolio. Its underutilized assets need minimal incremental cost in order to be able to continue their growth. Some areas like the Marcellus / Ohio Gathering JV and Barnett segments that have some of its most substantial underutilized assets, need no extra capital spending effectively to grow volumes.

That means the company's earnings could grow dramatically with minimal cost. However, it also means that the company spent a lot of money on assets that currently, have no demand. However, the company also has minimal additional capital requirements, now that the Double E pipeline is setup, which will mean the ability to direct cash to returns.

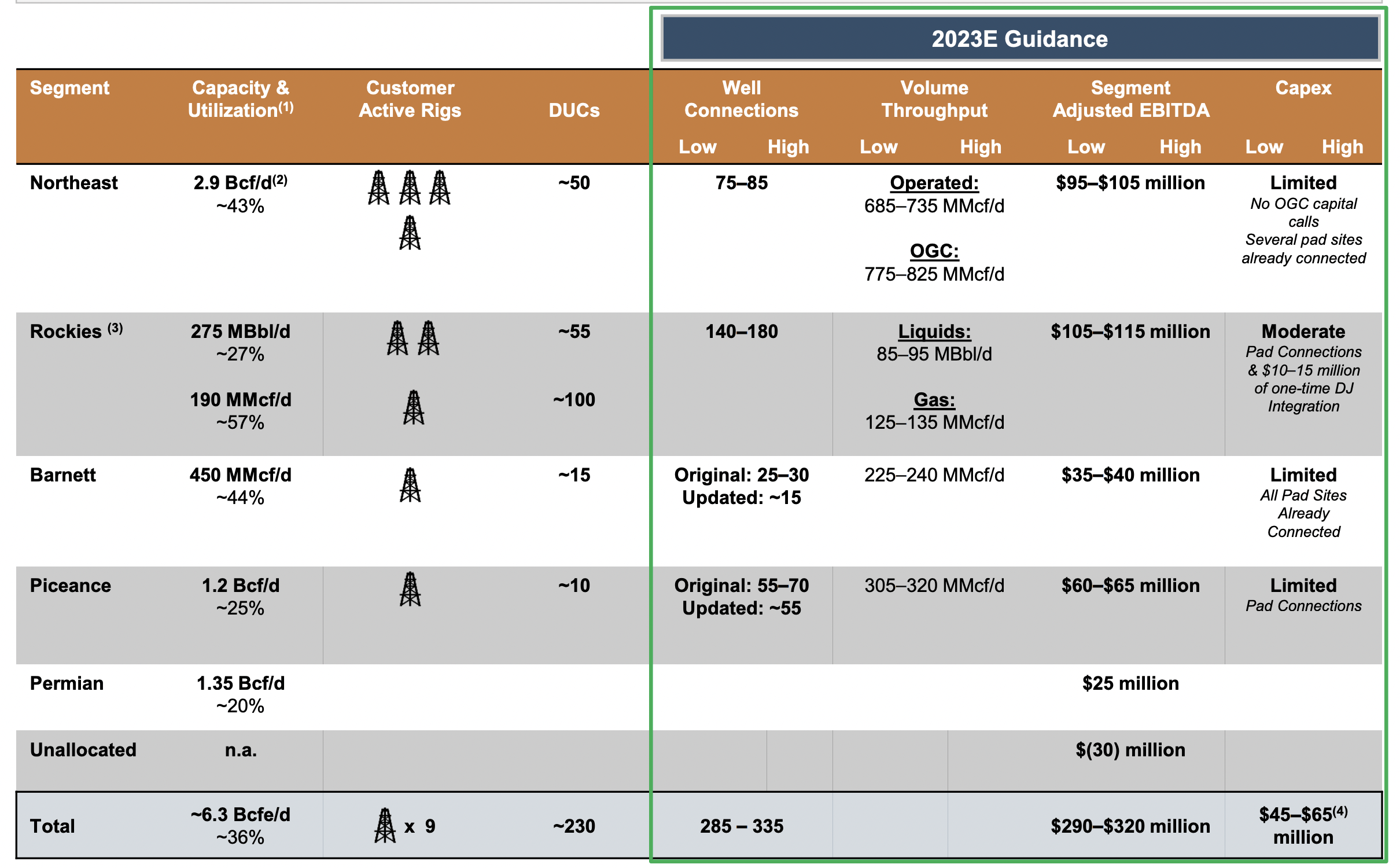

Summit Midstream Partners 2023 Guidance

The company's guidance shows a continued ability to perform in a normal market environment.

{kind=link}

The company earned $60 billion in EBITDA in 1Q 2023, with almost $10 billion going to interest expenditures. That shows the continuing cost of the company's debt. It also shows the company's EBITDA will increase into the next few quarters, with $305 million in forecast EBITDA for the quarter ($76 million average / quarter).

The company expects total capex requirements for the year to be $55 billion ($14 million / quarter). The company's YoY EBITDA growth is 40% and the company earned just under $75 million in FCF in 2022. We expect similarly strong and growing FCF in 2023, which combined with the company's strong guidance, will support growth.

We'd like to see the company continue to build up utilization across its assets and for the overall system, especially in the north-east.

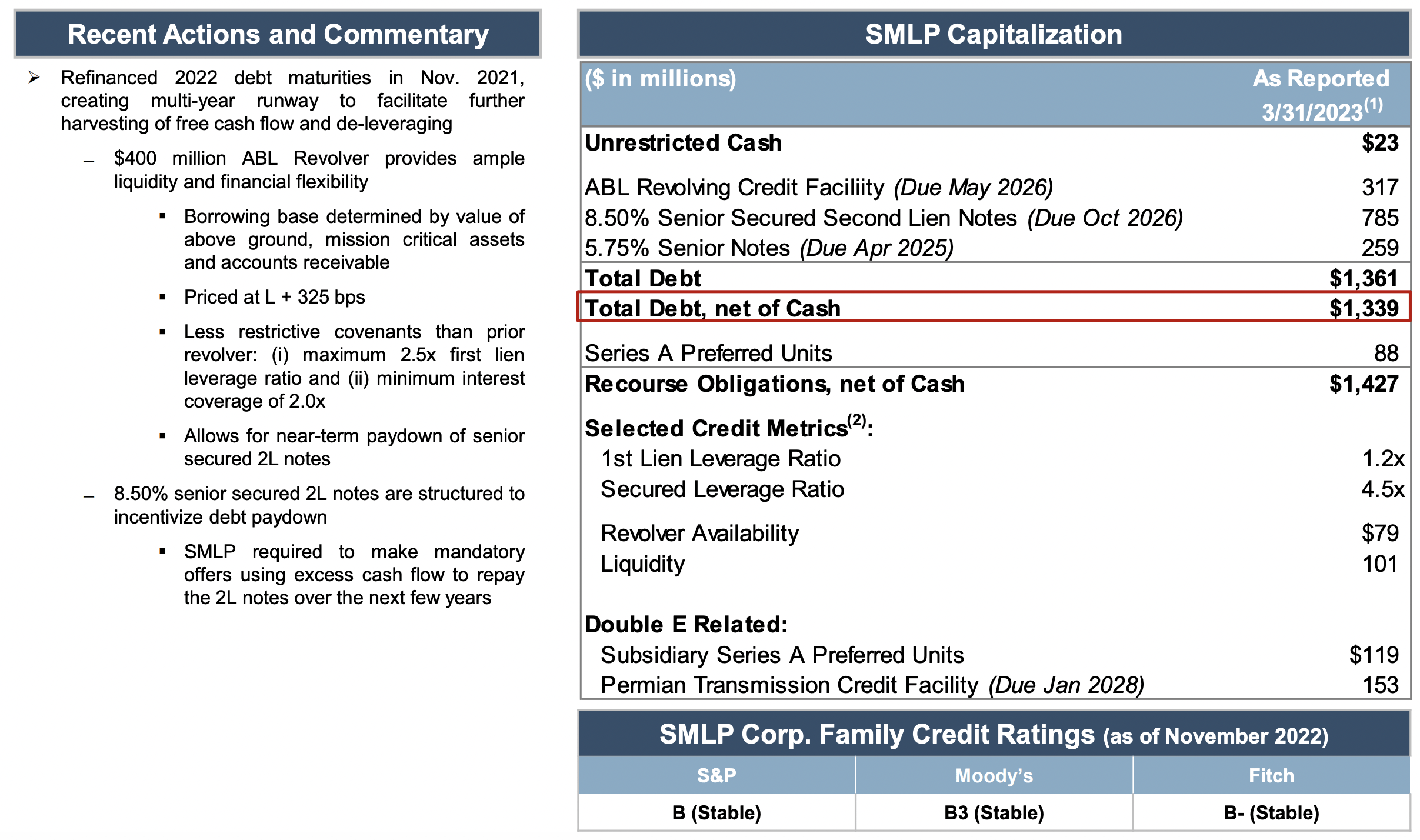

Summit Midstream Partners Debt

The company continues to have a hefty debt load it needs to solve.

{kind=link}

The company has $1.36 billion in total debt and $88 million in remaining Series A preferred units. The company's weighted interest rate on this debt is roughly $100 million per year, a massive amount. The company has substantially reduced its Series A preferred units, and we'd like to see that go to 0 to simplify the capital stack.

The reality of the matter is the company isn't earning the FCF to cover its debt. It will have to roll over the debt when it comes due in another 3 years. In a higher interest rate environment, with an unpopular company, that's dangerous. 8.5% was the best it could do in a low interest environment. Still, if the company could pay off debt and continue the stack, it'd be huge.

Thesis Risk

The company's largest risk is capital expenditures in the industry, but to a more substantial extent than many other companies. The company doesn't have the financial strength to handle one or two bad years, it can't handle another COVID-19-esque downturn realistically. We feel the risk-reward is strong, but the company needs several good years to generate returns.

Conclusion

Summit Midstream Partners has been through tough times and has yet to recover. The company's management managed to handle bankruptcy, but the company still has the problem of substantial built out assets with minimal utilization. However, despite that, the company continues to have positive FCF, which it can utilize to clean-up debt.

The company will need to rollover its debt in the next 2-3 years. Interest payments remain high and they have no sign of going down. The company's low market cap means it could have massive opportunity to pay down its debt towards $0, but it'll take the company close to a decade to handle it. The risk reward is there for patient investors, let us know your thoughts in the comments below.

For further details see:

Summit Midstream Partners: Can It Survive Low Utilization?