SMLP - Summit Midstream Partners Is Risky

2023-09-29 10:37:37 ET

Summary

- Summit Midstream Partners stock has underperformed the market and its sector this year.

- The company has exhibited mediocre operating performance and is on track to post an annual loss for the fourth year in the last five years.

- Summit Midstream Partners has an excessive debt load and its interest expense exceeds its operating income.

The stock of Summit Midstream Partners ( SMLP ) has underperformed the broad market and its sector by a wide margin this year. The stock has declined 14% whereas the S&P 500 and the Energy Select Sector SPDR Fund ETF ( XLE ) have gained 9% and 13%, respectively. This underperformance may lead some investors to think that Summit Midstream Partners has become oversold and attractive. However, the stock has some significant risks and hence it is unsuitable for conservative investors.

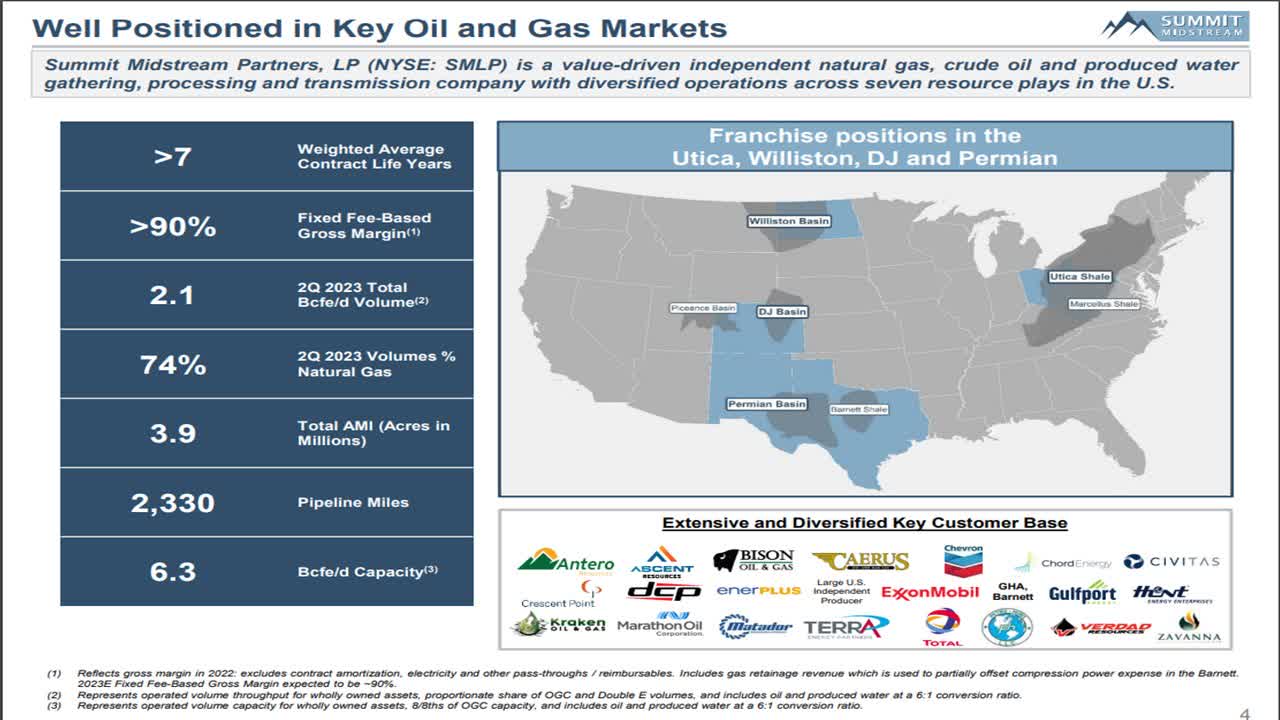

Business overview

Summit Midstream Partners is an independent midstream company, which gathers, processes and transmits primarily natural gas, with diversified operations across seven gas producing areas in the U.S.

{kind=link}

Natural gas comprises 74% of the volumes gathered and transported through the network of Summit Midstream Partners. It is also remarkable that the company boasts of having a fixed fee-based gross margin in excess of 90%. In addition, natural gas is considered a cleaner and more environmentally friendly fuel than coal and oil products. As a result, natural gas is much more resilient than other fuels to the ongoing shift of the entire world from fossil fuels to renewable energy sources. Therefore, the business model of Summit Midstream Partners seems quite attractive, at least on the surface.

Unfortunately, the company exhibited mediocre operating performance in the first half of the year. It connected just under 150 new wells during this period. This number is lower than the approximately 200 connections that management expected in the beginning of the year, but the company has connected an additional 45 wells in recent weeks, and thus it expects to meet its annual guidance of about 300 new connections in the full year.

However, management lowered its guidance for annual adjusted EBITDA from $290-$320 million to $260-$280 million, primarily due to extended delays in well completion dates. It is also important to note that the company has incurred losses per share of -$3.73 in the first half of the year. It is thus on track to post an annual loss for a fourth year in the last five years. Given also the persistent focus of management on EBITDA, it is safe to conclude that the company is far from becoming consistently profitable. As legendary investor Warren Buffett has repeatedly stated , in principle, investors should stay away from companies that focus on EBITDA instead of earnings.

It is also remarkable that Summit Midstream Partners suffers from a pronouncedly low utilization of its assets. To be sure, as shown in the above slide, the company has a total capacity of 6.3 Bcf per day, but it posted average volume of only 2.1 Bcf per day in the second quarter. As utilization has remained far below 50% for several quarters in a row, it is evident that Summit Midstream Partners cannot increase its utilization meaningfully. This is unfortunate, as higher utilization rates would enhance cash flows with only marginal increases in costs.

Debt

Summit Midstream Partners has an extremely weak balance sheet . Its current assets ($83 million) are lower than its current liabilities ($110 million), which are due within the next 12 months. In addition, its net debt (as per Buffett, net debt = total liabilities - cash - receivables) is standing at $1.6 billion. This amount is approximately 6.0 times the annual EBITDA and more than 11 times the current market capitalization of the stock ( $141 million ). Therefore, the company has an excessive debt pile.

Due to the high debt load of Summit Midstream Partners, its interest expense currently exceeds its operating income by a wide margin ($115 million vs. $53 million). It is thus obvious that the high debt load is a great burden for the company, making it harder to become profitable.

The weak balance sheet of Summit Midstream Partners and its recurring losses easily help explain the absence of dividend payments. Some companies do not pay a dividend because they find it more efficient and profitable to reinvest their earnings in their business. Unfortunately, this is not the case for Summit Midstream Partners, which has suspended its dividend in recent years due to its recurring losses and its material debt load.

On the bright side, the losses of Summit Midstream Partners have resulted in part from high depreciation amounts. As depreciation is a non-cash charge, at least in the short run, the company has posted positive free cash flows in each of the last three years. As a result, it may be able to reduce its debt to a manageable level in the upcoming years. Nevertheless, if the midstream company faces a severe downturn in its business in the near future, such as a recession, it will be caught with a high debt load and hence it will probably struggle.

Investors should also be aware that highly indebted companies tend to underperform the broad market by a wide margin over the long run. This has certainly proved to be the case for Summit Midstream Partners. The stock has plunged 94% over the last five years, whereas the S&P 500 has rallied 47% over the same period. In other words, during a favorable period for the broad stock market, the long-term shareholders of Summit Midstream Partners have incurred devastating losses.

Final thoughts

Summit Midstream Partners has the advantage of being engaged in the business of natural gas, which is much more resilient than the other fossil fuels to the ongoing transition of the vast majority of countries towards clean energy sources. It is also a midstream company, and hence it is much less exposed than pure upstream producers to the dramatic cycles of gas prices.

However, the stock has some red flags. It has posted material losses in 4 of the last 5 years and is probably far from becoming profitable, given the repeated focus of its management on EBITDA instead of earnings. Moreover, the company carries an excessive debt load, which renders the company vulnerable to a potential downturn in its business. Furthermore, the stock has caused devastating losses to its long-term shareholders over the last five years. All these characteristics render Summit Midstream Partners highly risky and unsuitable for conservative investors.

For further details see:

Summit Midstream Partners Is Risky