SMLP - Summit Midstream Partners: Lofty Goals For 2023

Summary

- Summit Midstream Partners is struggling with debt, as it has for years now.

- They recently undertook a sizable acquisition they hope will expedite deleveraging, but at the time, I remained skeptical.

- They have since updated their guidance for 2023, which sets lofty goals regarding their free cash flow that is far more than was expected.

- Apart from helping deleverage, this would see their units trading with a seldom-ever-seen free cash flow yield of circa 75% on current cost.

- Only time will tell how they perform and thus in the meantime, I am upgrading from a sell rating to a hold rating whilst awaiting their future results.

Introduction

When last discussing the struggling Summit Midstream Partners ( SMLP ), they were trying to spend their way out of overleverage but as my previous article warned, I was skeptical their DJ basin acquisition would achieve this goal. Fast forward to the closing days of 2022 and they have subsequently released further guidance for the year ahead, which sets lofty goals for 2023 for their free cash flow that is far more than was expected when conducting my previous.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

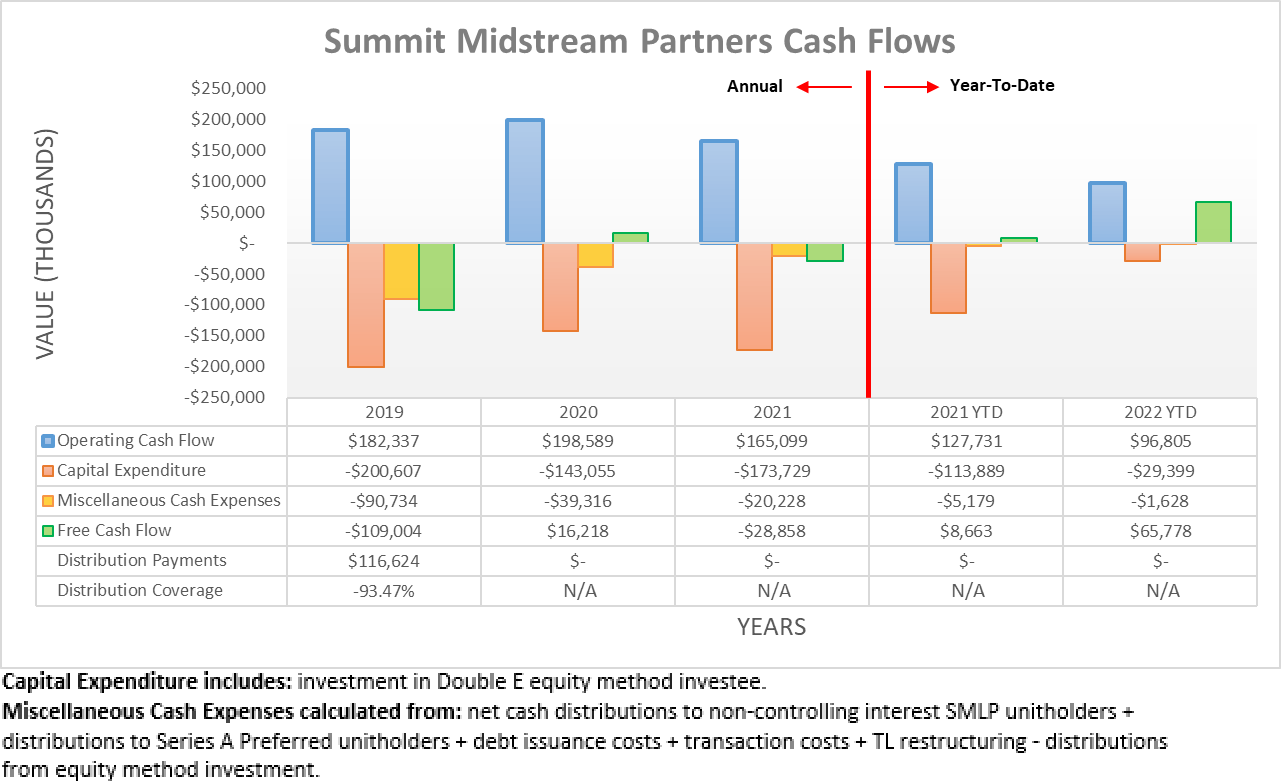

The first half of 2022 was marred by weak cash flow performance and seeing as this was heavily influenced by higher interest expenses, expectations for the third quarter were not high. Alas, this proved apt with their operating cash flow now landing at $96.8m during the first nine months, which similar to earlier in the year, sits around 24% lower year-on-year versus their previous result of $127.7m during the first nine months of 2021. If nothing else, one small saving grace was their very low capital expenditure of only $6.2m during the third quarter of 2022, which nevertheless helped maximize their free cash flow from an otherwise lackluster starting point. This ultimately saw their free cash flow increase to $65.8m during the first nine months, up from $36.9m during the first half and thus making the best out of a bad situation.

{kind=link}

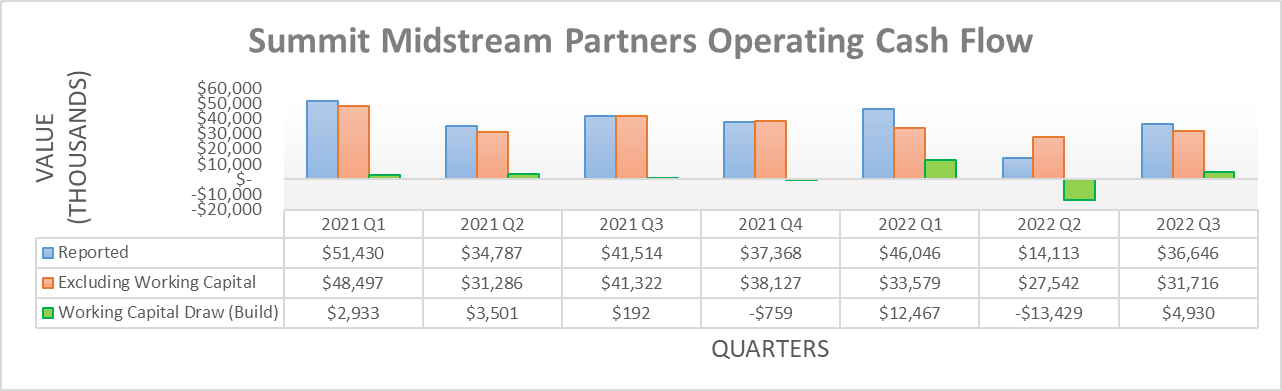

If viewed on a quarterly basis, their operating cash flow of $36.6m during the third quarter of 2022 was far better than their previous result of $14.1m during the second quarter, although this was mostly due to working capital movements. If these are excluded, their underlying results change to $31.7m and $27.5m respectively for these same two periods of time and whilst this still leaves the third quarter showing an improvement, it remains below their other previous result of $33.6m during the first quarter. At the end of the day when everything is said and done, it was not a terrible quarter but at the same time, it will not be remembered well into the future, thereby leaving their updated guidance for 2023 more interesting and obviously, far more important.

When conducting the previous analysis, their guidance for 2023 was already mentioned, despite not being the primary focus at the time and subsequently, they have now released more details. If the first element of their guidance comes to fruition, it sees their adjusted EBITDA climbing to $300m+ during 2023, which would be a significantly circa 40% higher year-on-year versus their forecast of $217.5m at the midpoint for 2022. Even though this remains unchanged compared to the previous analysis, very interestingly, they have now included further guidance for accompanying free cash flow of $125m+.

Summit Midstream Partners December 2022 Wells Fargo Presentation

If this free cash flow guidance for 2023 comes to fruition, it produces an insane, seldom-ever-seen free cash flow yield of circa 75% against their current market capitalization of approximately $165m and if achieved, their unit price is almost certain to rally much higher as the year progresses. Whilst this represents a massive improvement and far more than was expected when conducting my previous analysis, more years of deleveraging would still be ahead. Firstly, their unpaid preferred distributions are still accruing with a balance now north of $100m and as discussed within my earlier article , these must be made whole before returning cash to common unitholders. Secondarily, their financial position is burdened with excessive overleverage and thus as subsequently discussed, this short-term boost to their financial performance cannot sufficiently restore complete financial health.

{kind=link}

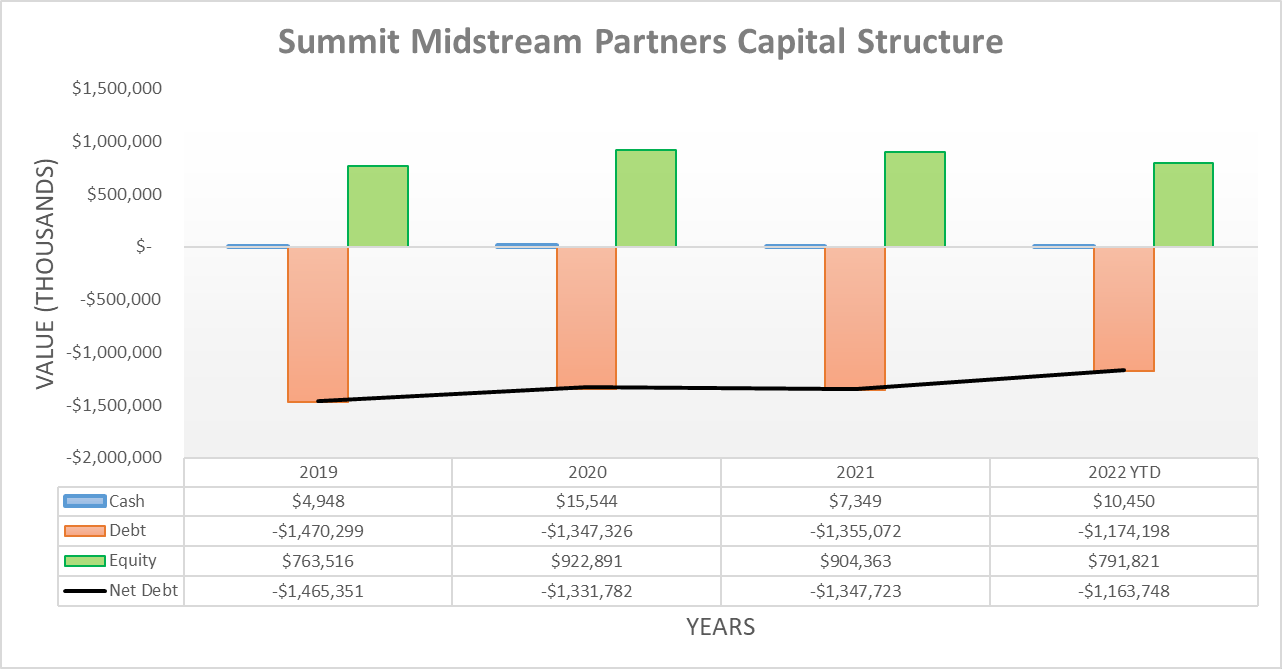

Despite their operating cash flow being anything but astounding during the third quarter of 2022, their net debt still decreased modestly to $1.164b versus its previous level of $1.228b following the second quarter. This primarily arose due to their very low capital expenditure that maximized free cash flow as well as the $36.7m of proceeds from their Bison gas gathering system divestiture, as expected when conducting the previous analysis. This is noticeably below where it ended 2021 at $1.348b, although the $305m cost of their DJ Basin acquisition during the soon-to-end fourth quarter of 2022 will instead ensure they end the year with net debt of more than $1.4b, depending upon their concurrent free cash flow.

As for 2023, they should shave away around 9% of their net debt if their free cash flow guidance comes to fruition, barring any further acquisitions or divestitures. Even though this would help, the far bigger impact to their leverage would come from the accompanying stronger financial performance, once again, assuming their guidance pans out as expected.

{kind=link}

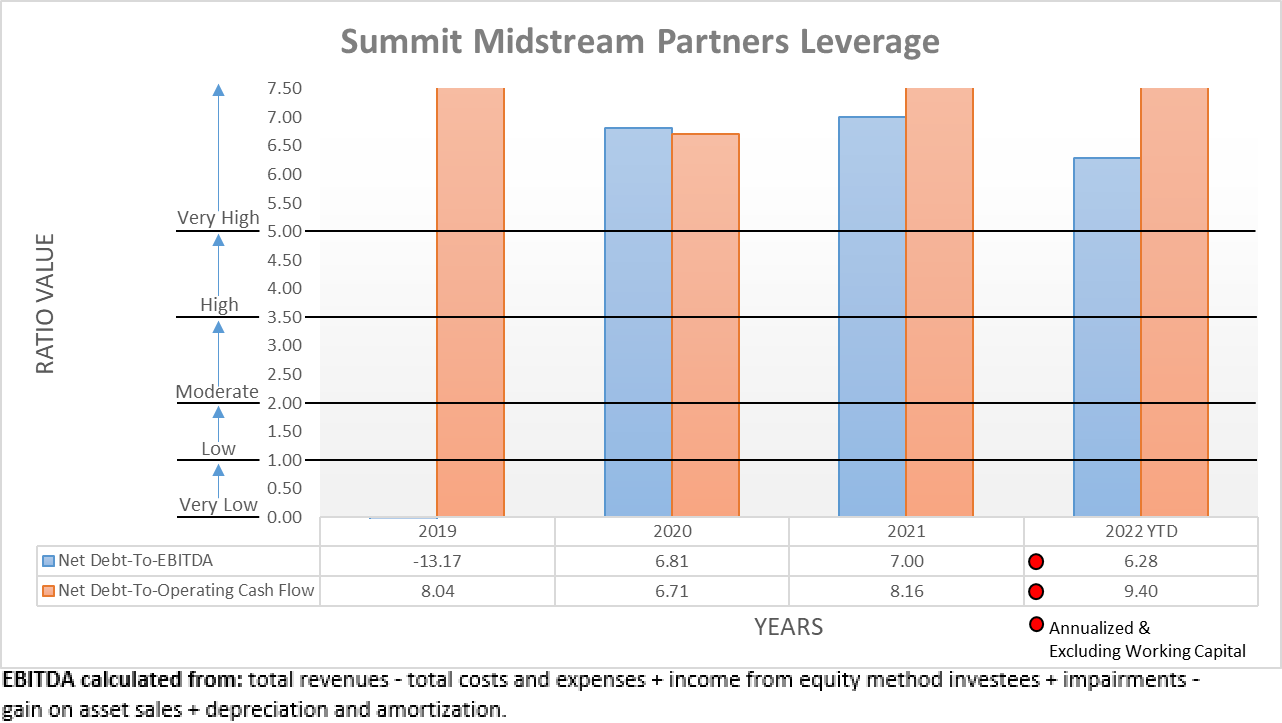

Thanks to their lower net debt, their leverage continues to decrease with their net debt-to-EBITDA now at 6.28 and net debt-to-operating cash flow came along at 9.40 following the third quarter of 2022. Whilst these mark improvements against their previous respective results of 6.93 and 10.04 following the second quarter, they nevertheless remain far above the threshold of 5.01 for the very high territory.

Even though their guidance for significantly higher adjusted EBITDA stands to see this improve during 2023, there is still an important caveat to consider, even if their forecast comes to fruition. When looking at their net debt-to-EBITDA and net debt-to-operating cash flow, there is an uncommonly large gap between their results with the latter far higher than the former, mostly because operating cash flow includes interest expense, unlike EBITDA. In my eyes, this makes comparing net debt against operating cash flow a superior measurement, especially when also considering the lack of accounting complexities with cash-based accounting instead of accrual-based accounting.

Since the pressure they face on this front is not likely to ease in the foreseeable future, their net debt-to-operating cash flow will remain far higher than their accompanying net debt-to-EBITDA during 2023. To this point, even if their operating cash flow scales 40% higher in tandem with their adjusted EBITDA guidance, their net debt-to-operating cash flow would only decrease to 6.72 at their current net debt, thereby remaining well into the very high territory. Since their net debt is about to jump around $300m higher following their acquisition that is actually driving most of this higher forecast financial performance, their future result would obviously sit even higher, likely over 7.00. This means that regardless if they see a short-term boost in 2023 from their DJ basin acquisition, there are still more years ahead deleveraging to restore complete financial health.

{kind=link}

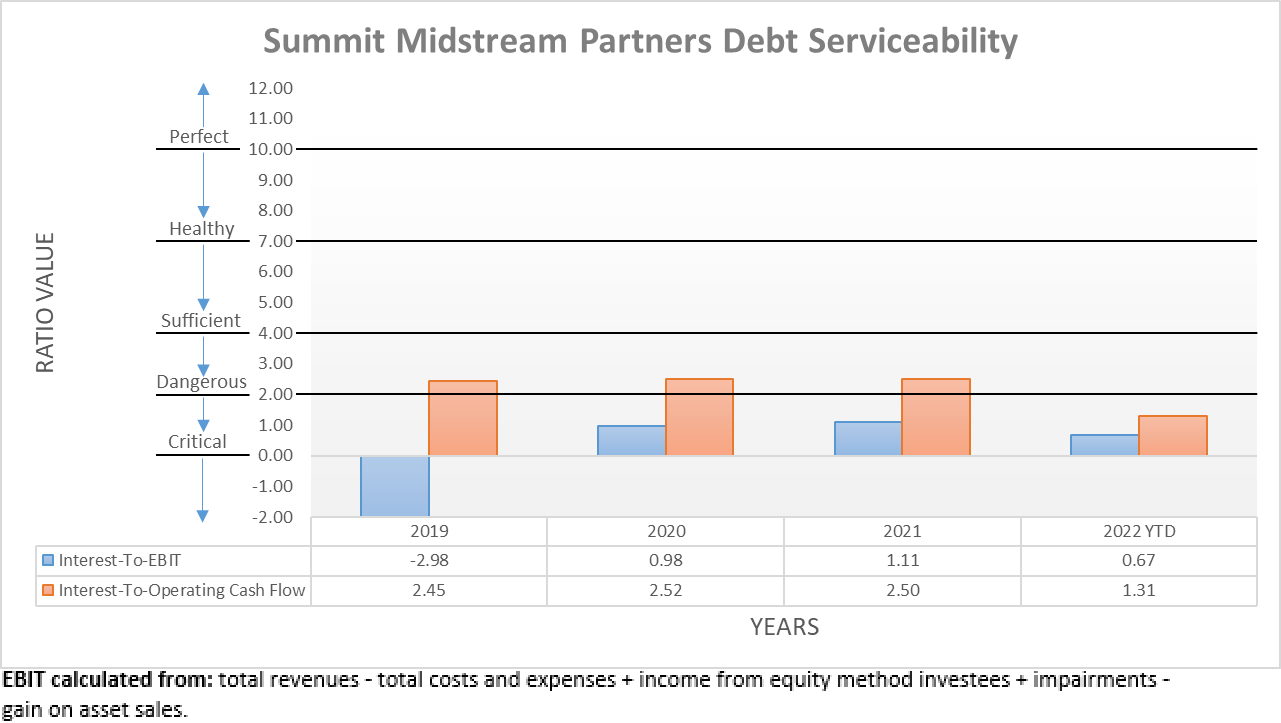

Following the analysis thus far, it should be no surprise to see their debt serviceability under immense pressure. Even after seeing a small improvement during the third quarter of 2022, their interest coverage is only 0.67 when compared against their EBIT and thus only slightly above their previous result of 0.57 following the second quarter. Meanwhile, their interest coverage when compared against their operating cash flow only sees a result of 1.31, which despite being higher is nevertheless still dangerous.

Whilst their interest coverage should improve during 2023 if their guidance comes to fruition, even their significantly higher 40% improvement would only lift their results to 0.94 and 1.83 when compared against EBIT and operating cash flow, respectively. Since both would still be dangerous, it means that similar to their leverage, this further confirms they have more years of work ahead to restore complete financial health. Due to most of their debt carrying fixed interest rates, even if the Federal Reserve were to begin easing monetary policy in late 2023 or 2024, it would not significantly help this problem that is only solved via reducing net debt across time.

{kind=link}

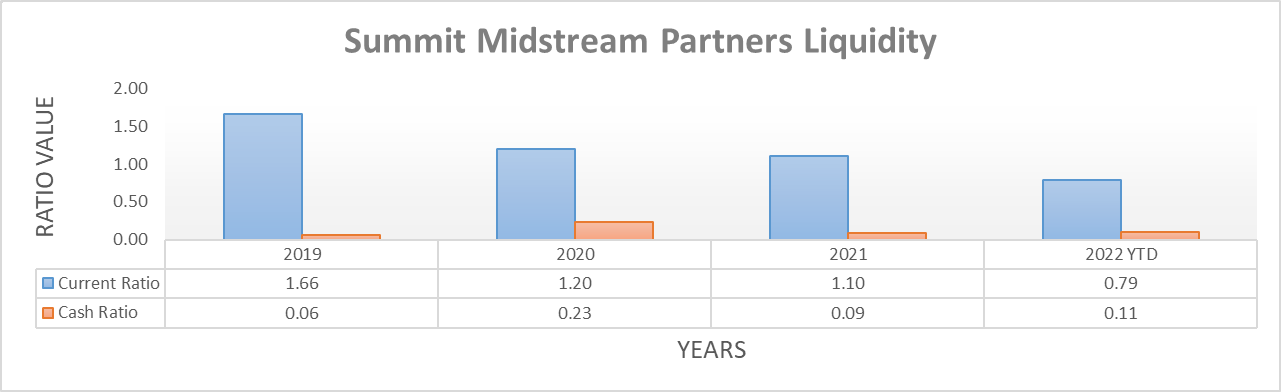

Despite other parts of their financial position improving during the third quarter of 2022, their liquidity did not follow in tandem with their respective current and cash ratios decreasing modestly to 0.79 and 0.11 versus their previous respective results of 0.91 and 0.14 following the second quarter. Even though not ideal, this was simply due to the usual fluctuations within their current assets and liabilities and thus, thankfully their liquidity remains adequate and due to their free cash flow, they are not necessarily reliant upon their credit facility.

This last point will be particularly important following the soon-to-end fourth quarter of 2022, as they utilized a large portion of their $400m credit facility to fund their DJ basin acquisition. When reading their latest transaction details , they issued $85m of senior secured second lien notes due in 2026 with the remaining $220m coming from their credit facility. Since they had already drawn $85m following the third quarter, it only leaves $95m of availability, not counting any concurrent repayments during the soon-to-end fourth quarter from their free cash flow.

On an adjacent topic, whilst 2026 is still quite a number of years away, they are oddly stacking up quite a lot of debt maturities in this one year. Apart from these new senior secured second lien notes, their credit facility also matures in May 2026 and most worryingly, their $700m of secured notes follow along in October 2026. Even though they have a number of years to address this issue, as it stands right now, it leaves a potential landmine sitting on the horizon.

Summit Midstream Partners Q3 2022 10-Q

Conclusion

If their guidance for 2023 comes to fruition, their units are trading with a free cash flow yield of circa 75% on current cost, which is effectively off-the-chart and almost unimaginable. Whilst yes, this would provide an immense short-term boost to help their excessively overleveraged financial position, it would still take more years of deleveraging to restore complete financial health, the length of time heavily dependent upon how long they can keep their capital expenditure at these rock bottom levels to maximize free cash flow. Whilst I am still cautious, I must admit their new free cash flow guidance for 2023 is higher than envisioned when conducting my previous analysis and thus, I believe that upgrading to a hold rating is now appropriate whilst awaiting to see whether their lofty goals for 2023 are achieved.

Notes: Unless specified otherwise, all figures in this article were taken from Summit Midstream Partners’ SEC filings , all calculated figures were performed by the author.

For further details see:

Summit Midstream Partners: Lofty Goals For 2023