SMLP - Summit Midstream Partners Needs To Account For Rising Rates

2023-11-14 15:58:50 ET

Summary

- Summit Midstream Partners, LP is a small cap midstream producer with a debt load that exceeds its market value.

- The company has managed to survive thus far, but its ability to thrive in the future is uncertain due to higher interest rates.

- The next step for Summit Midstream Partners is to determine whether it can overcome its debt burden and continue to grow.

Summit Midstream Partners, LP (SMLP) is a small cap midstream producer worth a mere $200 million. You wouldn't be able to tell that from its debt load, though. The company has done an incredibly job of surviving, however, the next step, at current higher interest rates, is to tell whether it'll be able to thrive going forward.

To add a warning ahead of time, Summit Midstream Partners is a risky investment. Bankruptcy continues to hang as a cloud over the company. It's a risk we're comfortable with given the upside potential for multi-bagger potential. However, for those who invest, it's important to be comfortable with that risk as well.

Summit Midstream Partners Q3 2023

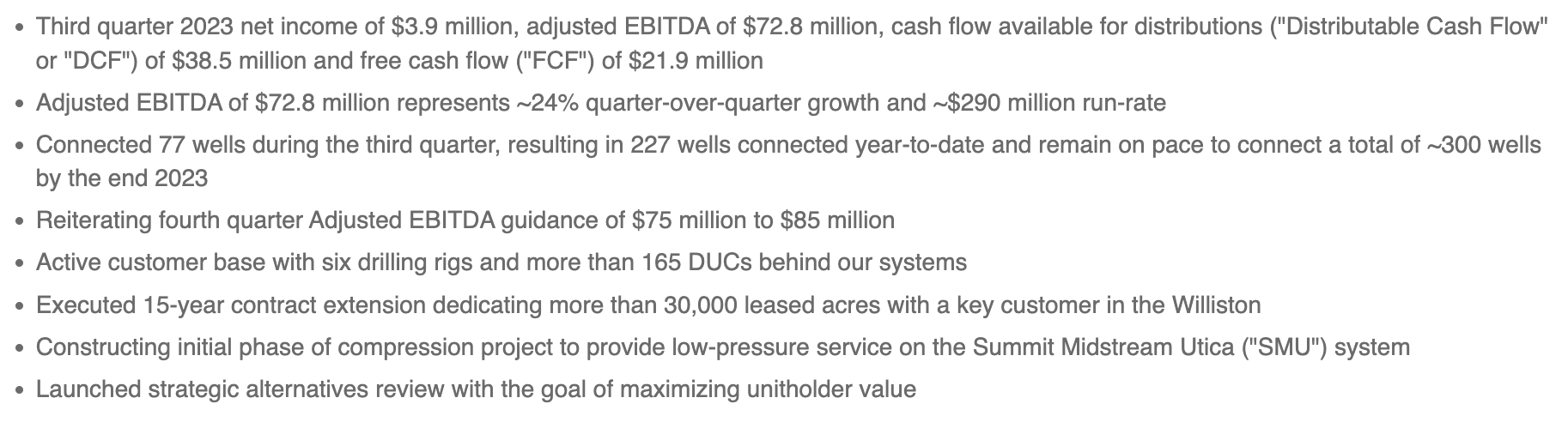

The company had $3.9 million in net income for the quarter off of $72.8 million in adjusted EBITDA.

{kind=link}

Discounted cash flow, or DCF, was $38.5 million and FCF was $21.9 million, both essential numbers to the company being able to pay off its debt. The company's adjusted EBITDA remains at a run-rate of just under $300 million. The company managed to connect 77 wells during the quarter, and annualized it's on a pace for 300 well connections.

The company expects to close out the year strong. Adjusted EBITDA is expected to be $80 million, and the company's customer base has 6 rigs and 165 DUCs. The company recently announced a contract extension in the Williston Basin, which is essential for its future, and looking at providing low-pressure SMU service.

The company's Q3 2023 shows continued success in all facets of its business.

From a volume perspective, throughput increased by 12% to 1.35 billion cubic feet / day, with liquids volumes increasing by 20% to 85 thousand barrels / day. Both of these improvements are incredibly impressive to see. The Double E pipeline saw volumes increase 34%. Weakness in natural gas prices is concerning on the horizon.

However, continued strong export demand, will help maintain prices and future returns.

Summit Midstream Partners Management Highlights

Management's number one concern, as highlighted in their highlights is maintaining volume in the system. That's not surprising given recent weakness in U.S. natural gas prices. The company does hope to hit $300 million in LTM adjusted EBITDA by mid-2024, showing modest growth, and it's guiding 220 new wells over the next 3 quarters.

That's in line for how the company did over the last 3 quarters. Management's guidance for the Williston Basin customer and acreage, is an additional rig of drilling, coming online mid-next year. That's versus 6 rigs currently, which is nice improvement and could result in a strong 2H 2024. The low compression project on SMU could had fees on 20 million cubic feet / day.

Summit Midstream Partners Throughput

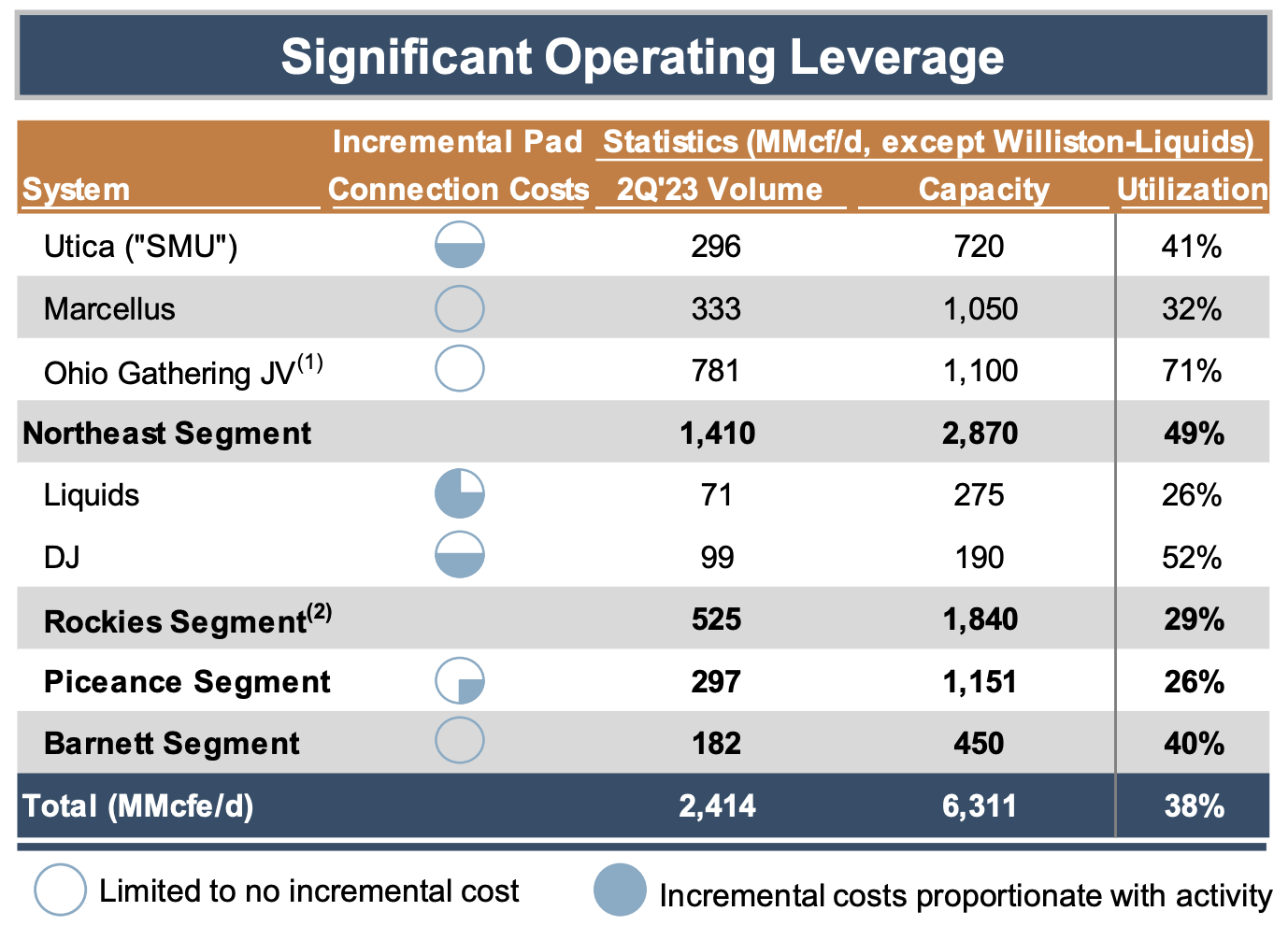

The company's throughput remains our largest concern about the company and its ability to succeed.

{kind=link}

The company has a substantial amount of assets it's built that aren't being utilized. The company's utilization in all of its segments is well below 50%. The dream for the company would be that volumes ramp up under its assets without it needing to have substantial connection costs. However, that remains a struggle.

Unfortunately, we don't have much guidance into being able to tell the company's path to resolving this problem and how significant it is long-term. The company does still have EBITDA from MVC, roughly 10% of its EBITDA in the most recent quarter, which has long-term staying risk and is worth paying close attention to.

Summit Midstream Partners Financials

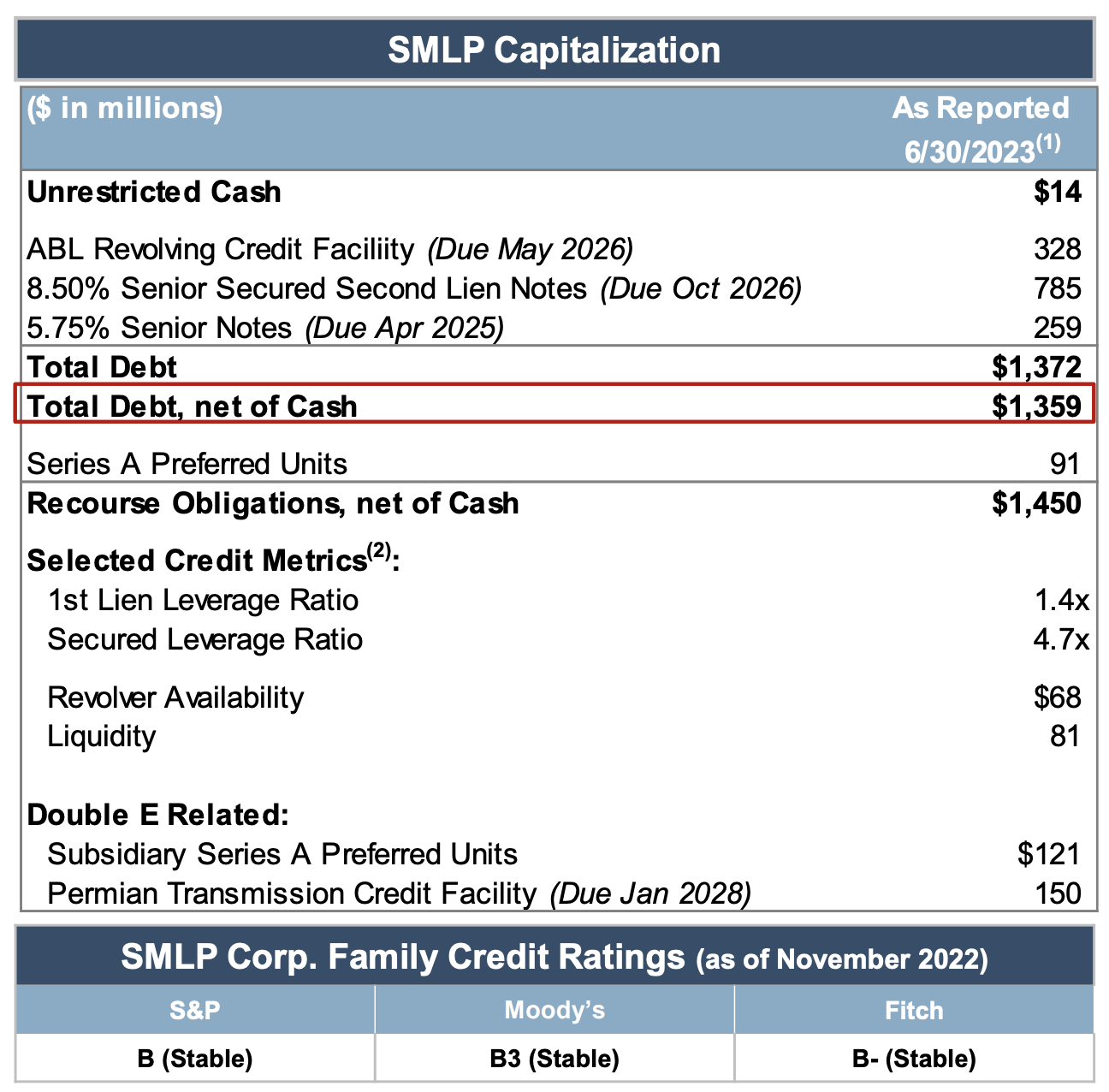

The company's financials and its ability to succeed over the long-term is dependent on the company's debt load.

{kind=link}

We'll ignore the company's preferred units for now, since while they are accumulating interest that will need to be handled at some point, they're not an existential threat. At 9.5% in interest, the accumulation is substantial and worth paying close attention to when it comes down to shareholder rewards for you.

The company's 3 sources of debt are its credit facility, its mid-2025 notes, and its late-2026 notes. The company's late-2026 notes have an 8.5% interest rate. The company's FCF enables it to pay down just over $100 million in debt annually. At current interest rates paying down mid-Apr 2025 is better to potentially avoid needing to roll it over.

That would give the company one more year. At the end though it'll need to rollover potentially $1 billion in debt. That's the company's biggest risk. Right now the company has just under $1.4 billion in debt. Interest expenditures are roughly ~$120 million annualized. Rates have gone up by ~4%. That means the company's interest expenditures could go up by $50 million.

That would cut the company's FCF in half. It could still pay down debt but of course the rate would slow down substantially. Still it's worth noting that debt is ~85% of the company's enterprise value. That's important because debt pay down saves on interest and rapidly translates to shareholder returns. With no debt the company's FCF would equal its market cap, a sign of its low value.

That helps highlight the opportunity within Summit Midstream Partners.

Thesis Risk

The largest risk to our thesis is the company's debt load, and the fact that it will have to roll over that debt in the next several years. There is no reasonable path to paying off that debt. In a higher than normal interest rate environment, the interest payments from rolling over the debt could harm the company's fiscal strength and ability to pay-off additional debt substantially.

The alternative is interest rates decline to 0%, but such a rapid decline is unlikely in our view without a market decline that substantially impacts the value of the company's assets.

Conclusion

Summit Midstream Partners was dealt a tough hand with its assets and the 2020 crude oil price collapse. The company's utilization remains weak, however, the company has worked hard to improve its FCF and manage its massive debt yield. The company's next largest obstacle is rolling over its debt in a world with higher interest rates.

Fortunately, we expect Summit Midstream Partners, LP will be able to comfortably handle that. Its incredibly low market cap means that the company will be able to see increased market cap from debt pay downs. Investors will need to be patient, but we expect strong shareholder returns for those who have the patience and are willing to handle the risk.

For further details see:

Summit Midstream Partners Needs To Account For Rising Rates