SMLP - Summit Midstream Partners' Recent Earnings Are Just The Start

2023-10-09 12:43:27 ET

Summary

- Summit Midstream Partners, LP's share price is highly impacted by its substantial debt load in relation to its market cap.

- The company has announced strong volume growth and expects significant earnings and results.

- The company's assets have substantial capacity for minimal cost, but its utilization remains low and it needs long-term demand for its assets.

Summit Midstream Partners, LP ( SMLP ) had a great week on the back of a strong earnings update . The volatility in the company's share price is primarily due to its substantial debt load in relation to its market cap, which means movements in value impact its share price dramatically more. As we'll see throughout this article, recovering volumes should enable the company to drive substantial shareholder returns.

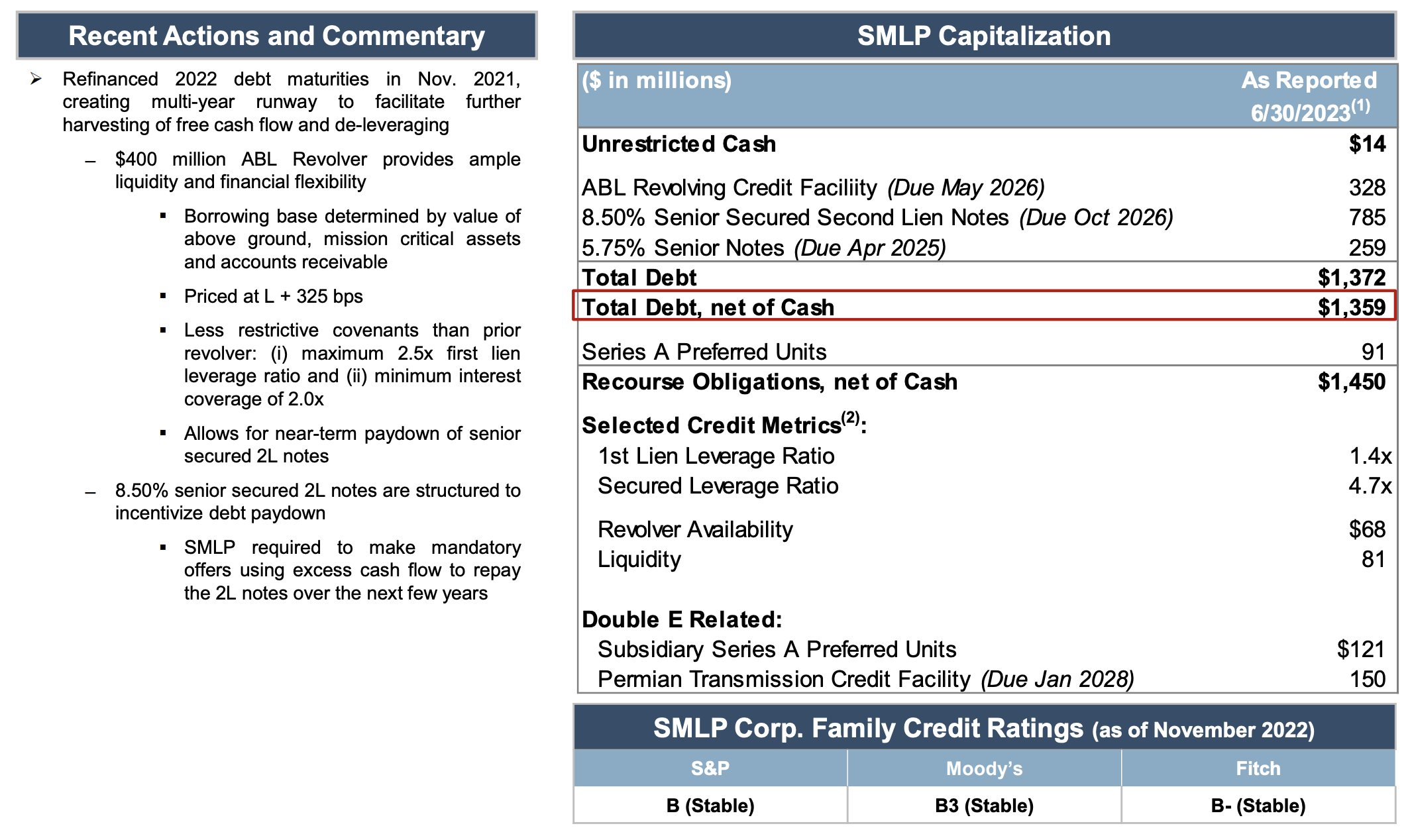

Summit Midstream Partners Debt

The company's largest source of weakness continues to be its debt load.

{kind=link}

The company has a massive debt load that drowns out its market cap. The company's revolving credit facility has $328 million borrowed. On top of that, the company has 8.5% in senior secured second lien notes due October 2026, for a total of $785 million, and lastly 5.75% in Apr 2025 senior notes, with a total of $259 million. Total debt net of cash is a staggering $1.359 billion.

For perspective, the company's market cap is a hair over $200 million. There's another risk here in the rising interest rate environment. The company managed to raise its recent debt at much lower interest rates. The company's annual interest obligations are roughly $100 million. Once it has to roll over its debt, and it will have to, its interest could increase substantially.

The company needs to pay down as much debt as it can before refinancing.

Summit Midstream Partners Earnings

The company has announced a rough guidance of its earnings and results.

{kind=link}

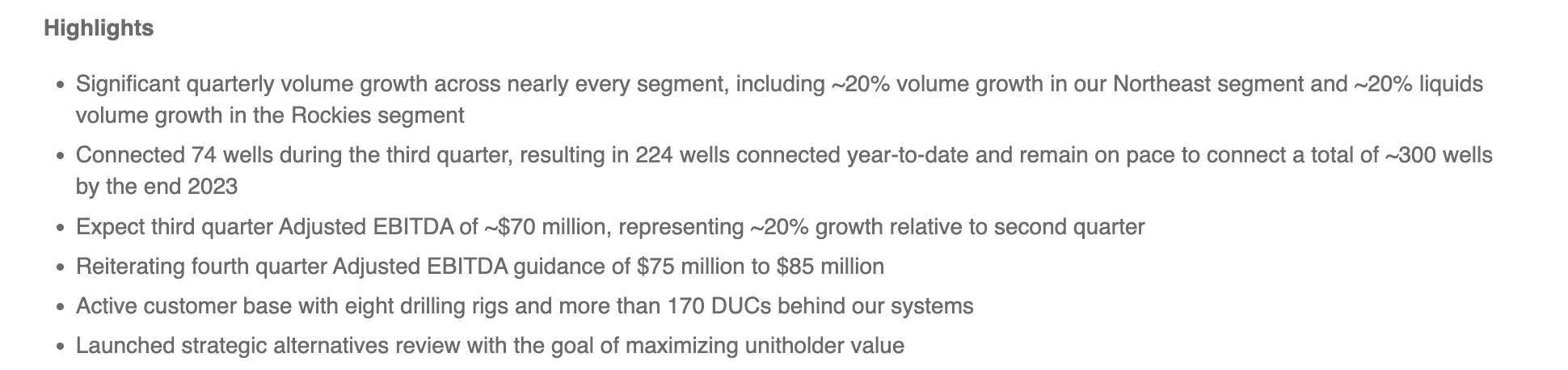

The company announced massive volume growth across its business. That includes 20% Northeast volume growth and 20% Rockies liquids volume growth. That massive volume growth shows a recovery in demand for the company's assets, the most important part of success for any midstream company.

The company saw 74 wells connected during the quarter, with 224 YTD, targeting 300 for the year. That's as many well connects as the company saw in the 2018 peak, and more than 2019. This is supported by strength in the company's segments. The company expects $70 million in EBITDA for the quarter, up 20% QoQ, and is guiding $80 million for the last quarter.

The company's customer base has 8 rigs and 170 DUCs, which will help support additional drilling completion. The company has yet to set the 2024 guidance, but 1H 2023 guidance is ~$300 million. The company's guidance for these connections is $55 million.

{kind=link}

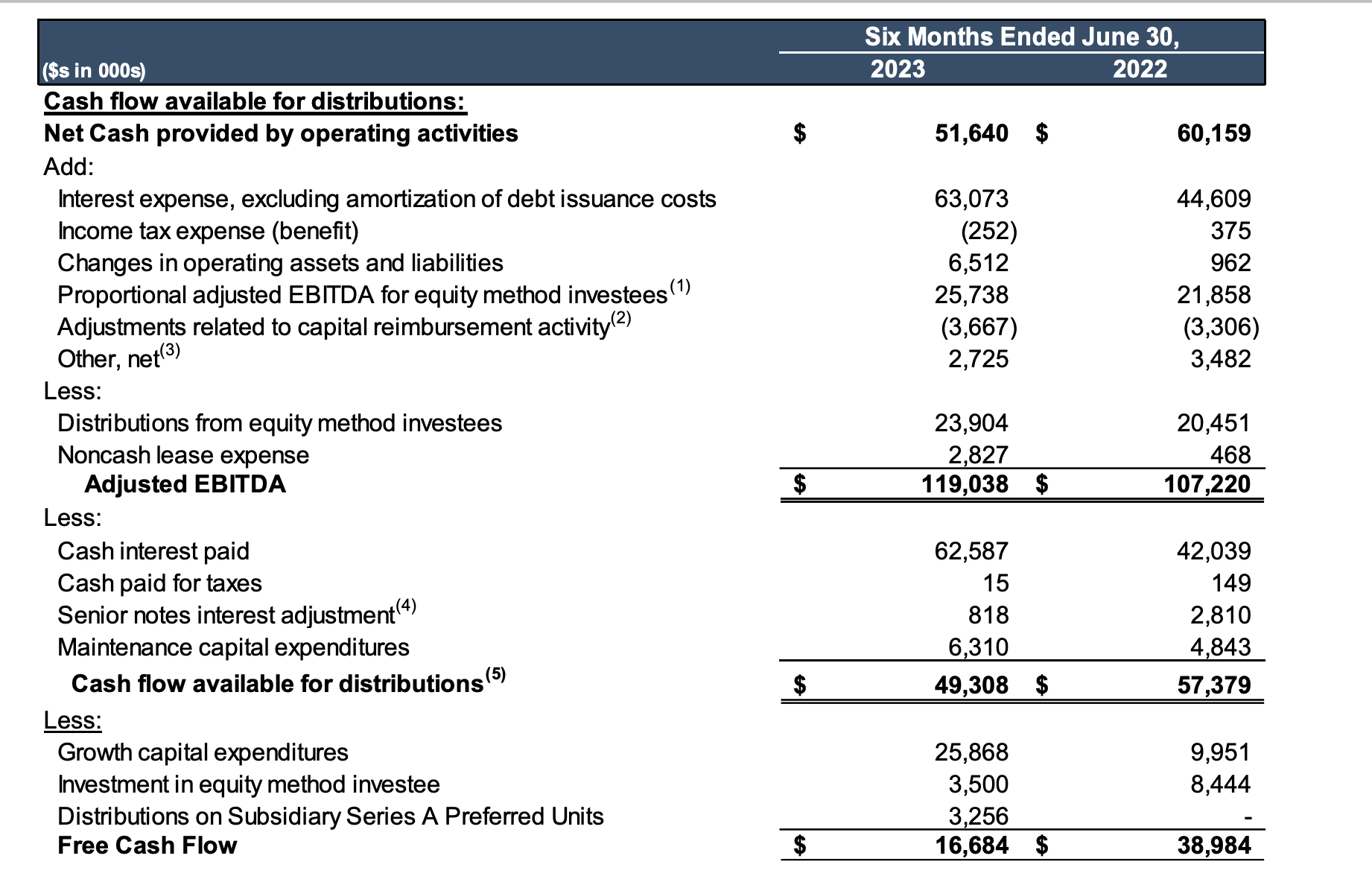

Financially, what matters for the company at the end of the day is whether it can turn its EBITDA into free cash flow ("FCF"). The company's $107 million in 6 month adjusted EBITDA turns into $57 million in cash flow for distributions and $40 million in FCF. Triple that EBITDA and remove the $40 million in extra interest, and you get ~$120 million in FCF off of $300 million in EBITDA.

That means from 2024-2026, the company will earn ~$350 million in FCF. That's ~25% of its debt. We expect all cash flow will go towards this goal.

Summit Midstream Partners Assets

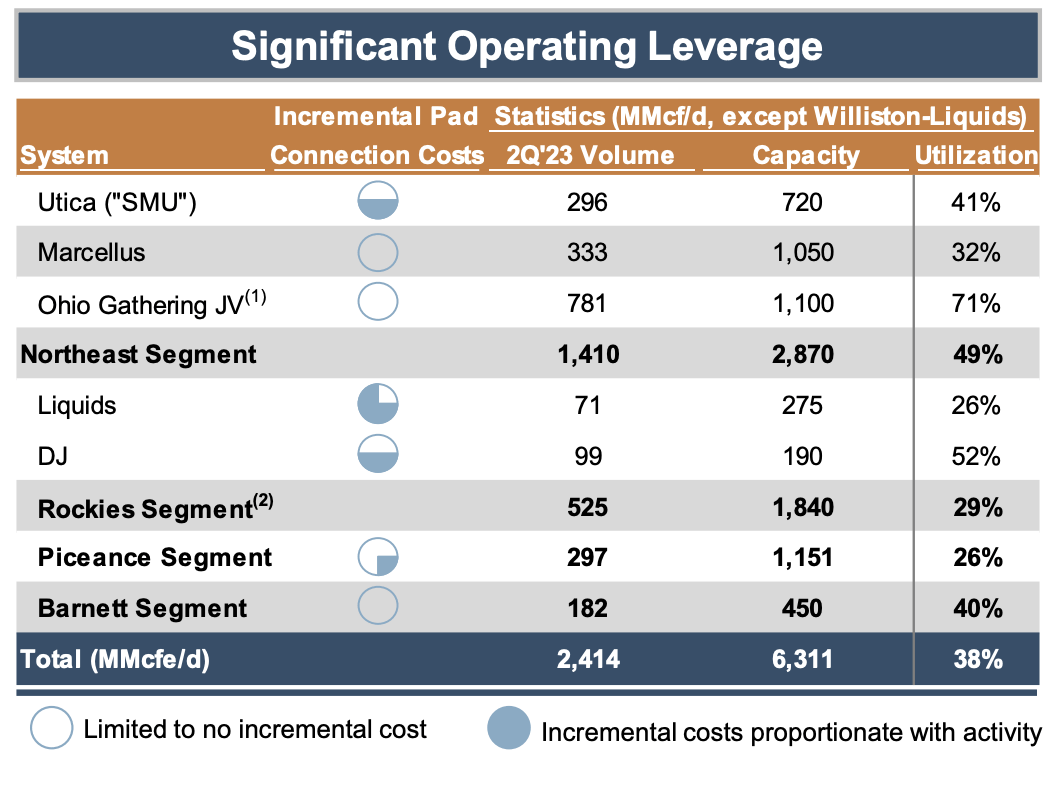

The company's assets have substantial capacity for minimal cost.

{kind=link}

The asset location informs the incremental cost to add volume. In Marcellus and the Ohio Gathering JV, the company's cost to add incremental pads is almost 0. For Liquids in the Northeast, it's much higher. Across the company's assets, its utilization is 38% meaning that there's substantial room to increase utilization.

The overall system can support almost 4 billion cubic feet / day in additional incremental capacity. The company's survival is based on whether drilling continues in its segments. It continues to receive MVC shortfall payments, and while those are closing down, it will not continue forever.

The company's new Double E pipeline is backed by 13 rigs and the company believes in the long-term potential here, but its other assets combined have 8 rigs, not a ton for long-term support. As long as the company's utilization remains low, its earning potential remains lower. The company fundamentally needs long-term demand for its assets.

Summit Midstream Partners Future

The most important note in the company's update was that it's started to review strategic updates.

Based on the Partnership's recent and expected financial performance, as well as interest recently received from third parties for potential transactions?, ranging from the sale of specific assets to consideration for the whole Partnership,? SMLP is announcing that its Board of Directors has engaged external advisors to evaluate strategic alternatives for the Partnership with the goal of maximizing value for the Partnership's unitholders.

That's not surprising. The company continues to trade in an incredibly low valuation because of fear over its debt load and whether the company can refinance it. A large company that could handle that debt load, especially one with the gathering assets, could integrate and receive strong overall integrated assets.

How that future pans out remains to be seen, but the market is clearly optimistic. We expect the company to get a strong premium.

Thesis Risk

The largest risk to thesis is whether the company can continue to maintain utilization and see wells completed. That relies on higher prices. Natural gas prices have had some strength recently. We expect this strength to continue as natural gas prices have strong demand, however, whether that pans out remains to be seen.

Conclusion

Summit Midstream Partners has had some strong performance recently. The company has a strong portfolio of assets and the market has been strong recently. However, the company remains susceptible to its massive debt yield, paying off as much as it can before the next rollover. Higher interest rates present a massive threat.

However, despite that threat, Summit Midstream Partners, LP has the cash flow to drive substantial shareholder returns long term. A strategic acquisition could provide a strong short-term return. The company's rollovers continue to remain important for its long-term returns. Let us know your thoughts in the comments below.

For further details see:

Summit Midstream Partners' Recent Earnings Are Just The Start