SMMT - Summit Therapeutics: Ivonescimab Deal Potential Mid-Term Growth Driver

Summary

- Summit Therapeutics rallied hard off 52-week lows in December after its licensing deal for Ivonescimab was announced.

- Gains have extended into the new year, which is promising for those seeking to enter long at the current market value.

- Moreover, Ivonescimab is building a robust safety and efficacy profile, challenging current treatment paradigms as a monotherapy.

- Net-net, we rate SMMT a buy, seeking targets to $5 then $10.

Investment Summary

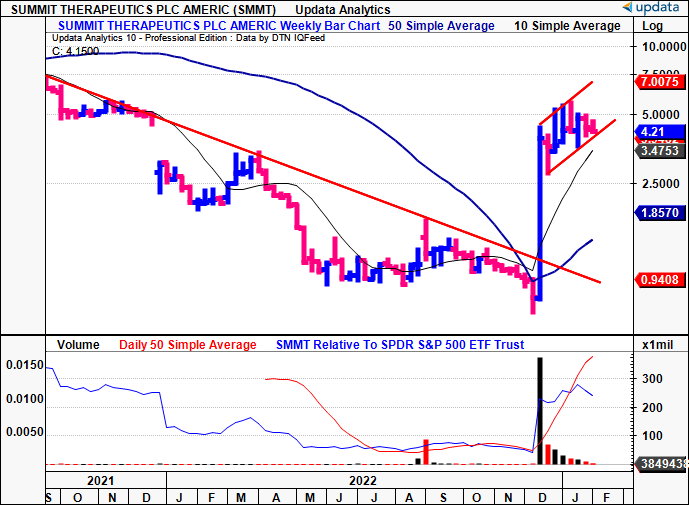

Following its recent thrust and breakout from 52-week lows, we are constructive on the mid-term outlook for Summit Therapeutics Inc ( SMMT ). It's recent licensing deal for the drug Ivonescimab was the catalyst to bring price levels back to FY21' highs [Exhibit 1], and we feel there's enough market support for this to extend higher. Moreover, the underlying drug in question is building a robust safety and efficacy profile, aiming to address a difficult to treat portion of the lung carcinoma populous. Net-net, we rate SMMT a buy, seeking price objectives to $5 then $10.

Before continuing, investors should understand that the key downside risk to our investment thesis is that the market may have overshot its reward for SMMT following the announcement. Moreover, there are numerous company-specific risks that challenge our investment thesis.

Firstly, Ivonescimab is still subject to approval from U.S. and EU regulatory authorities , and delays or rejection of these approvals could adversely affect SMMT's share price and operating performance, especially given the price paid for the license. On this note, Ivonsecimab's [and ultimately SMMT's] growth is heavily dependent on the drug successfully completing the remainder of its clinical trials. It should be noted that there is no guarantee that either the trials will be successful or that the products will be approved.

This extends to SMMT's competitors in this domain, which may prevail as the dominant therapy even if approval is obtained. What's more, is given the chance of this failure, the concentration risk of SMMT's portfolio means it has little to fall back to in terms of generating revenues of post-tax profits. Each of these risks are very real, and would nullify our investment thesis should they pull through.

Alas, there's quite a scope for a market selloff, that could result in downside risk, and negative price action given SMMT's ~$920mm market cap. Hence why we rate SMMT a speculative buy. Investors should recognize these risks before reading any further.

Exhibit 1. Thrust off 52-week lows following announcement to license Ivonescimab

{kind=link}

Catalyst for December rally: Ivonescimab licensing deal

In December last year SMMT entered into a collaboration and license agreement with Akeso, Inc ( AKESF ) to partner up in licensing the latter's Ivonescimab. The collaboration also includes a supply agreement, where SMMT will purchase a certain portion of the drug substance for both clinical and commercial purposes. In accordance with the terms of the agreement, and in exchange for the rights, AKESF will receive an initial payment of $500mm. Noteworthy, is that AKESF is also be eligible to receive regulatory and commercial performance-based payments of up to an additional $4.5Bn. Hence, when factoring in all regulatory and commercial performance-based payments, the deal's potential value could to be worth up to $5Bn for AKESF. Per the partnership, SMMT has been granted the rights to develop and commercialize Ivonescimab within the U.S., Canada, Europe, and Japan. Meanwhile, AKESF retains the rights to develop and commercialize the product across the rest of the world, along with the key China market.

Furthermore, AKESF shall be entitled to receive "low double-digit percentage royalties " as a percentage of Ivonescimab's net sales. To finance the transaction, the company approved a rights offering to shareholders, hoping to raise $500mm. In addition, it also entered into a note purchase agreement with CEO Robert Duggan, and CFO Dr. Maky Zanganeh. Per the prospectus:

"Pursuant to the Note Purchase Agreement, the Company agreed to sell to Mr. Duggan and Dr. Zanganeh unsecured promissory notes in the aggregate amount of $520 million. The Company expects to use the proceeds of the Note Purchase Agreement for payment of the upfront obligation associated with the License Agreement, for activities to support clinical development and regulatory approval for [Iveonescimab] to pursue business development opportunities to expand our pipeline of drug candidates; and for general corporate purposes.

[T]he Company has issued to Mr. Duggan and Dr. Zanganeh unsecured promissory notes in the amount of $400 million and $20 million, respectively, which will mature and become due on February 15, 2023, and an unsecured promissory note to Mr. Duggan in the amount of $100 million, which will mature and become due on September 15, 2023."

In lieu of this, the both parties have since closed the transaction . The first tranche of $300mm was paid at closing, where AKESF elected to convert $25.1mm into 10mm common shares of SMMT, with the remaining $274.9mm a cash consideration. The second instalment of $200mm is due on March 5 is also an all-cash consideration.

Understanding SMMT's strong bid post-announcement

The question then turns to what caused SMMT to catch such a strong bid on this deal in the first place. Here I'll explain to readers why the market was so generous in its reward to the stock.

It's important to know that, pulmonary neoplasia, characterized by resistance to checkpoint inhibitors targeting the programmed cell death-1/programmed death-ligand 1 axis, are known as PD-L1/PD-1-resistant lung carcinomas. Patients in this cohort represent a clinically significant subpopulation of lung carcinoma. For reference, the PD-1/PD-L1 pathway is a crucial mechanism of immune evasion in cancer. To date, development of monoclonal antibodies targeting this axis have resulted in substantial advancements in treatment paradigms in lung carcinoma. However, complexities still exist, as a further substrata of patients with lung metastasis exhibit an acquired resistance to these therapies. Hence the drive to establish alternative treatment pathways to address these complexities.

Here is where AKESF's Ivonescimab marks its entrance onto the scene. It received breakthrough therapy design ("BTD") in China, and, per the company, is the only drug candidate to receive this designation for PD-L1/PD-1–resistant lung cancer in China. It's propose that Ivonescimab works by blocking PD-1, binding to PD-L1 and PD-L2, whilst concurrently blocking vascular endothelial growth factor ("VEGF") by binding to VEGF receptors. Carmeliet (2005) explains that VEGF is "the key mediator of angiogenesis in cancer, in which it is up-regulated by oncogene expression...[a]ngiogenesis is essential for cancer development and growth".

AKESF suggests its use as a monotherapy to inhibit PD-1/VEGF co-expression may be more effective in blocking these two pathways, enhancing anti-tumor activity when compared to combination therapy [current standard of care]. To investigate this, AKESF conducted a multi-center, phase 1b/2 trial to evaluate the safety and efficacy of Ivonescimab as a monotherapy in patients with advanced non-small cell lung cancer ("NSCLC"). Findings demonstrated the monotherapy was safe and well-tolerated regardless of histological sub-type, with an objective response rate ("ORR") of 50% and a disease control rate ("DCR") of 93%. As such, there's now fairly robust evidence supporting the above hypothesis.

Two drugs that already target this pathway, pembrolizumab [brand name Keytruda, from Merck] and Bristol-Myers Squibb's ( BMY ) Opdivo [drug name nivolumab], have already been approved by the FDA for the treatment of lung metastases. Consequently, based on its phase 1/2 trial results, AKESF is now conducting a phase 3 trial, comparing Ivonescimab as a monotherapy versus Pembrolizumab as a first-line treatment for patients with PD-L1 positive NSCLC. In addition, it is investigating the drug in an ongoing phase 3 trial of Ivonescimab plus chemotherapy, comparing it to chemotherapy alone in patients who failed prior epidermal growth factor receptor tyrosine kinase inhibitors ("EGFR TKI"). If successful, outcomes of these studies are set to be quite a disruption to the current standard of treatment, in our opinion.

Where to next for SMMT?

It's still very early days in terms of Ivonescomib's approval and commercial status. Keytruda booked $5.4Bn in quarterly gross sales in Q3 FY22', however, it has a broad application across several carcinoma sub-types. Hence, we're not confident in forecasting the launch curve for SMMT until we have more data on the entire situation, and some more language from management.

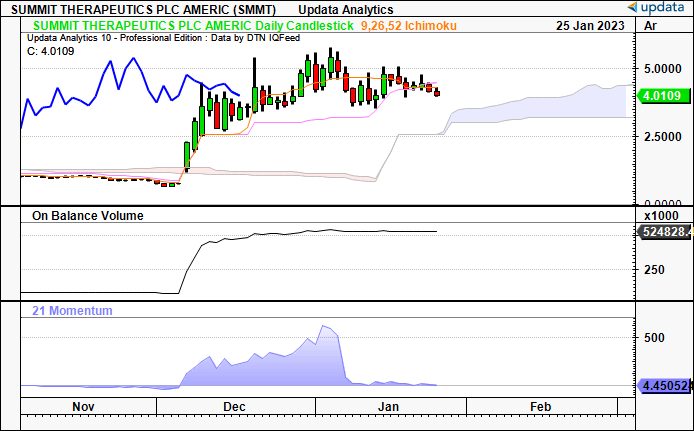

In the meantime, we are still bullish on SMMT in the mid-term, as shares are positioned above cloud support on the ichimoku chart below, suggesting potential support levels at ~$4.50 into February.

Exhibit 2. Bullish above the cloud, with potential support zones at $4.50 into the coming month

{kind=link}

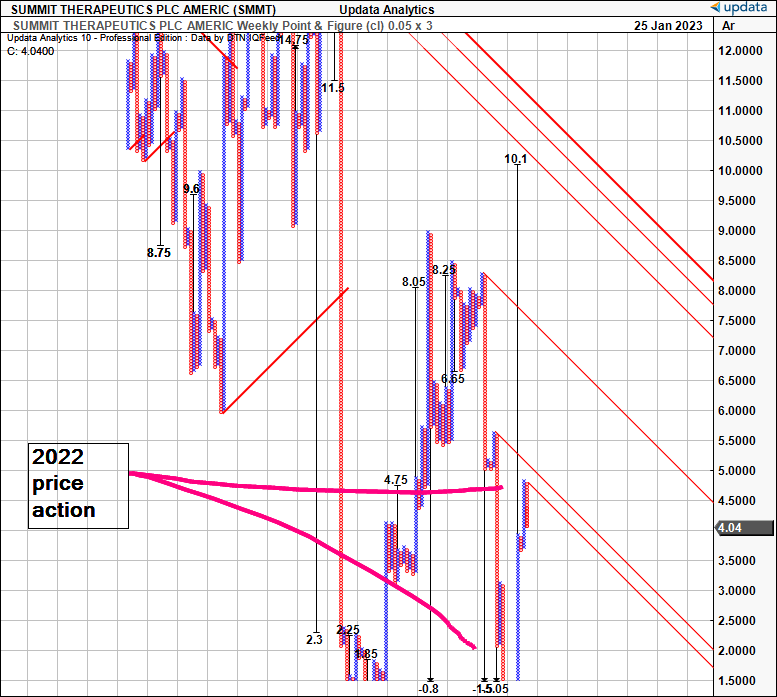

In addition, we have longer-term price targets to $5 and then ~$10, implying a tremendous re-rating should this come through. On this basis, and the momentum building from the licensing deal, we are bullish on SMMT.

Exhibit 3. Upside targets to $5 then $10

{kind=link}

In short

Net-net, we rate SMMT a speculative buy, as a play on the licensing deal and corresponding market reaction to this. Meanwhile, there's a robust evidence profile building around the underlying drug. These factors combined, along with pricing studies above, means we are bullish on the stock. Rate buy, seeking price objectives to $5 then $10.

For further details see:

Summit Therapeutics: Ivonescimab Deal Potential Mid-Term Growth Driver