ELS - Sun Communities: Attractive Growth But Valuation Creates A Risk

2023-11-07 15:53:11 ET

Summary

- Sun Communities owns and operates manufactured home, RV, and marina communities.

- The REIT has been enjoying high operational growth, has low leverage, and high liquidity.

- Though it also provides us with a consistent dividend payment and growth record, the yield is too low to be attractive.

- There is also a lack of consistency in the picture provided by valuation; a margin of safety is not present.

- Regardless, investors may make a different conclusion after reading this article as individual needs and resulting criteria vary.

Sun Communities, Inc. ( SUI ), founded in 1975 and headquartered in Southfield, Michigan, acquires and operates Manufactured Home (MH) and Recreational Vehicle (RV) communities, as well as marinas. More specifically, they lease the sites that provide utilities for the installment of the MHs, RVs, and boats.

This REIT is the largest publicly traded owner of MH communities in North America and the second largest in the U.K., as well as the largest and most diversified owner of Marinas in the U.S. And though the fundamentals are sound (diversified portfolio, a lot of growth, low leverage, and high liquidity), there is no sign that the shares are currently undervalued on an absolute basis.

However, the dividend is safe and growing. Relative to a couple of competitors, SUI appears undervalued. So make sure to read what follows below because you may develop a bullish conviction that my personal needs prevent me from.

Portfolio

Sun Communities owns a portfolio of 670 developed properties located in the U.S., the U.K., and Canada which are split into 353 MH communities, 182 RV ones, and 135 marinas.

Based on revenue generated in the third quarter of 2023, 88.67% came from North America and 11.33% from the U.K. Further, 45.65% of rental revenue was generated from MH communities, 34.02% from RV ones, and 20.33% from Marinas.

As you can see, there is both geographical and site-type diversification here and there's a case to be made about MHs and RVs being alternative budget-friendly options, to which it wouldn't be wrong to ascribe the recent operating growth you will notice next.

Performance

When it comes to the occupancy rate, the weighted average was 95.4% in the third quarter of this year and 96.4% in the third quarter of 2022. Further, it was 96.3% for North America markets and 90.6% for the U.K. in 3Q23.

Regarding the long-term historical operating performance, Sun Communities has experienced great growth, with most of it observed in the last couple of years:

More recent results illustrate this exponential growth well. The rental revenue in the third quarter annualized represents a 60.36% increase from the average annual figure of the last 3 fiscal years. Based on the same methodology, the most recent quarterly same-property cash NOI annualized reflects an increase of 81.38% and, similarly, AFFO one of 82.79%.

Leverage

What's even more impressive is the very low leverage the REIT uses and the level it has been working toward over the years:

Aside from the ~40% debt-to-assets ratio, the REIT's debt-to-EBITDA ratio is at 5.8x. Coupled with the interest coverage of 2.5x, liquidity looks more than adequate.

Further, its long-term liabilities consisting of ~$3.3 billion in secured debt and ~$4.3 billion in unsecured debt carry a weighted average interest rate of 4.13%, which represents a modest cost.

It's also very good to see that maturities for the next two years don't suggest a potential increase in the weighted average interest rate since only 2.3% of total debt or $128 million matures in 2024 and an even lower amount of $51 million which represents 0.9% of the debt matures in 2025. However, we should note that in 2026 comes a balloon payment of $658 million which is 11.7% of the total debt; but that may not be a big problem for refinancing as I find it unlikely for interest rates to be as high as they are today.

Dividend & Valuation

Currently, the REIT pays a $0.93 quarterly dividend per share which suggests a 3.13% forward yield. While that is too low to pique anyone's interest, I want to be fair and say a few things here.

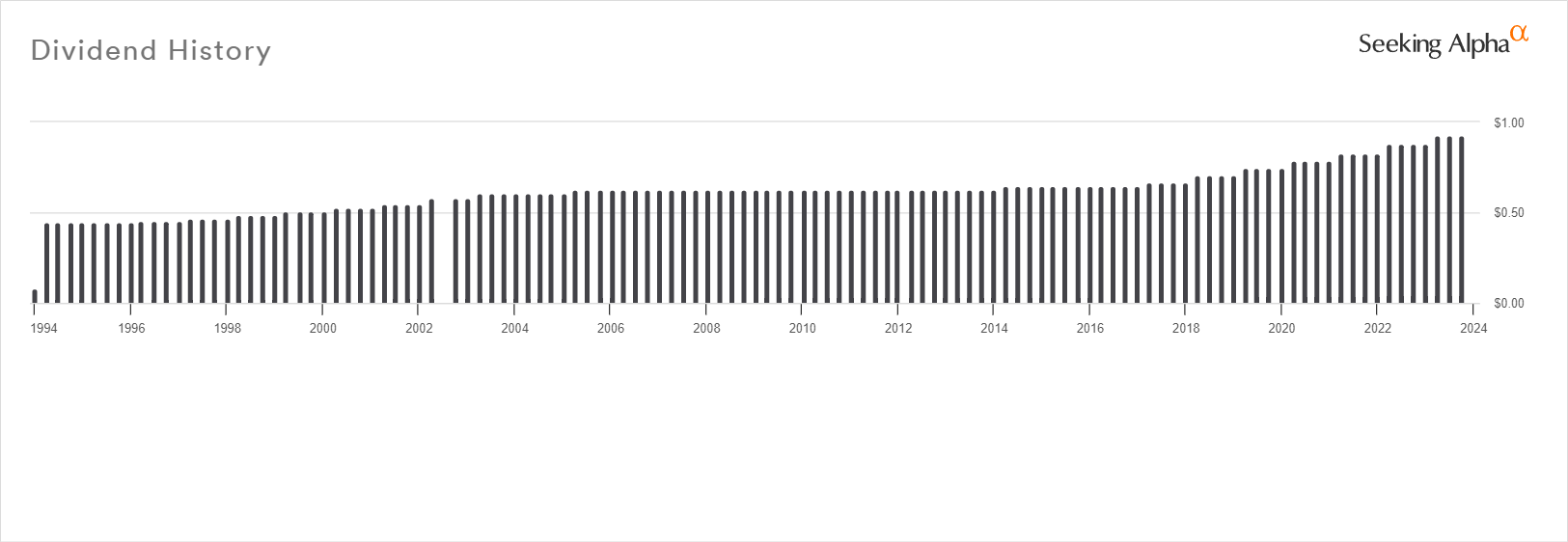

First, we should note that the company has been paying a dividend for the last 19 years:

{kind=link}

Seeking Alpha

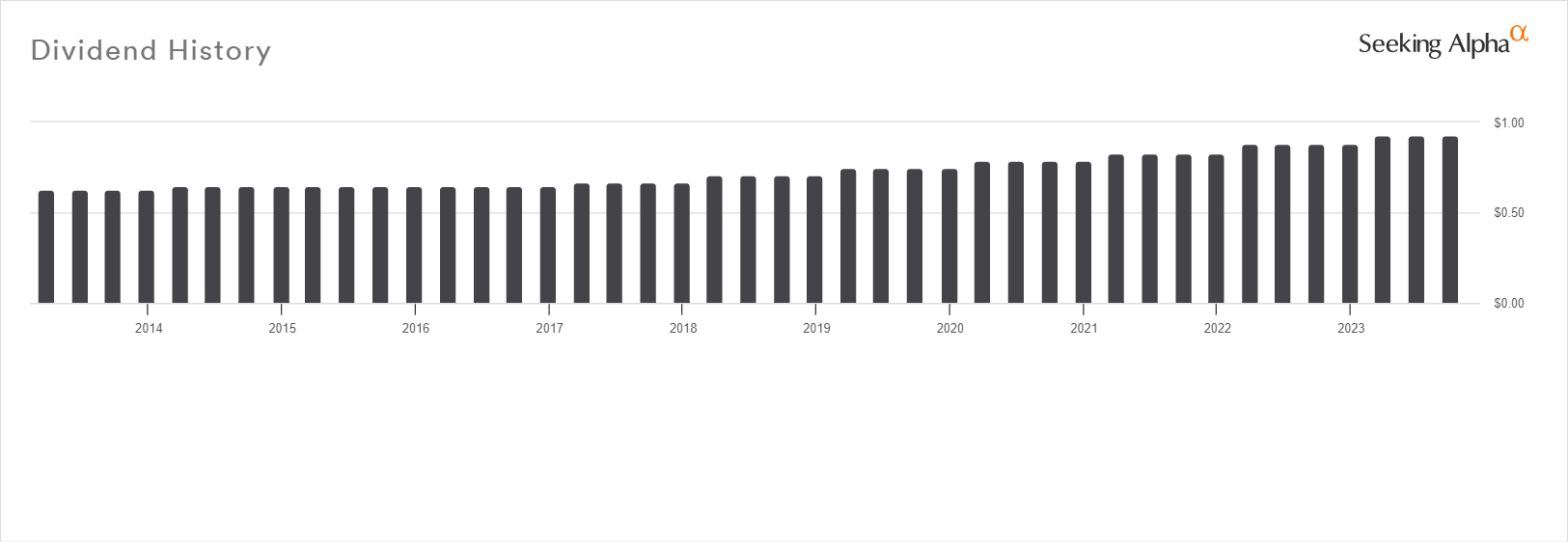

But more importantly, it has been increasing it for 6 straight years:

{kind=link}

Seeking Alpha

And for what it's worth, the payout ratio based on the last quarterly AFFO per share sits at 37.49%. Now, if the strong trend of AFFO growth persists, there's no reason why dividend increases won't continue to keep coming.

That said, the current dividend yield doesn't represent good value. Its FFO multiple disagrees with this, however, as indicated by the discount to the multiples of two close competitors:

The geographical and site type diversification makes this relative undervaluation even more interesting.

But here is where it gets personal. Currently, SUI is trading at a 6.91% implied cap rate. This seems more or less appropriate for MH and VR sites these days; I know I wouldn't use a lower cap rate to value its assets. Therefore, on an absolute basis, I do not see any discount here.

Risks

As you can see, the uncertainty related to valuing SUI creates a risk here. Even if overvaluation is not apparent either in this case, the lack of a definite undervaluation is enough to fill potential shareholders with uncertainty. And conviction is the key to a long-term position and the gains that may result from it.

If you are looking for a dividend grower, also remember that there are REITs out there that have been increasing the payout for a much longer time and currently provide higher dividend yields. So, this is also a contributing factor to the opportunity risk we are faced with here.

Verdict

For these reasons, I assign a HOLD rating to SUI. The growth is impressive and the low leverage coupled with high liquidity could provide a lot of assurance for someone looking to hold this REIT for the long term.

But the dividend yield is too low and undervaluation is not present on an absolute basis, something to which I place the most weight. So, consider the context that influences my HOLD rating before you make a decision.

Do you agree with this thesis? I would like to know your thoughts. Let me know in the comments below and I'll get back to you as soon as I can. Thank you for reading.

For further details see:

Sun Communities: Attractive Growth, But Valuation Creates A Risk