UMH - Sun Communities: Solid Company In A Market With Growing Demand

2023-06-01 10:34:19 ET

Summary

- Demand for manufactured housing is growing, with Sun Communities being the largest publicly traded manufactured housing REIT.

- SUI owns 671 properties, with rental rates increasing across all types of housing in the past year.

- Despite a low dividend, SUI is rated as a BUY due to increasing popularity of manufactured homes, expected FFO growth, and a stable balance sheet.

The demand for manufactured housing has been growing, especially in the US, as people are looking for more affordable places to live. With that, areas with such housing are now resort-like to be more attractive to the customer and a pleasant place to live. Moreover, manufactured housing represents a great business opportunity, because not only is there profit to be made at the time of sale of the property, but since the REIT retains the ownership of the land underneath the homes, they continue to collect rent from very sticky tenant relationships. This is because a tenant that has already invested significant amounts of money into the house sitting on the land is unlikely to want to leave, putting the landlord in a great position. Today, I would like to look at the biggest publicly traded manufactured housing REIT - Sun Communities ( SUI ).

SUI owns manufactured housing ("MH"), RVs, and marinas in the US, some parts of Canada, and the UK. They own a total of 671 properties with almost 180k MH and RV sites and 48k wet slips and dry storage spaces. 53% of the real property NOI comes from MH, 26% from RV's, and 21% from marinas. The rental rate increased for all of these types of housing in the last year. The average increase was 6.3% for manufactured housing in the US and 7.3% in the UK, for RV's it was 7.8%, and for marinas 7.5%.

The core FFO per share was $7.23 in the past year ($1.23 in the last quarter). Same store revenue has increased by 7.2% in the first quarter of 2023, the operating expenses increased by 8.2% and NOI by 6.7%. The guidance the company provided states that the core FFO per share is expected to be between $7.22 and $7.42 so pretty much the same as this year. The NOI is said to increase by 5-6%, driven by cost savings. Beyond this year, analysts expect FFO growth to pick up to 5-7% per year. Usually I’m skeptical of such forecasts that predict that things are going to improve materially next year unless I see clear evidence that indeed things could change. In case of SUI, I believe they can do it because they have a very interesting product that I expect to be in high demand and they also have ambitious expansion plans to grow their portfolio via new acquisitions.

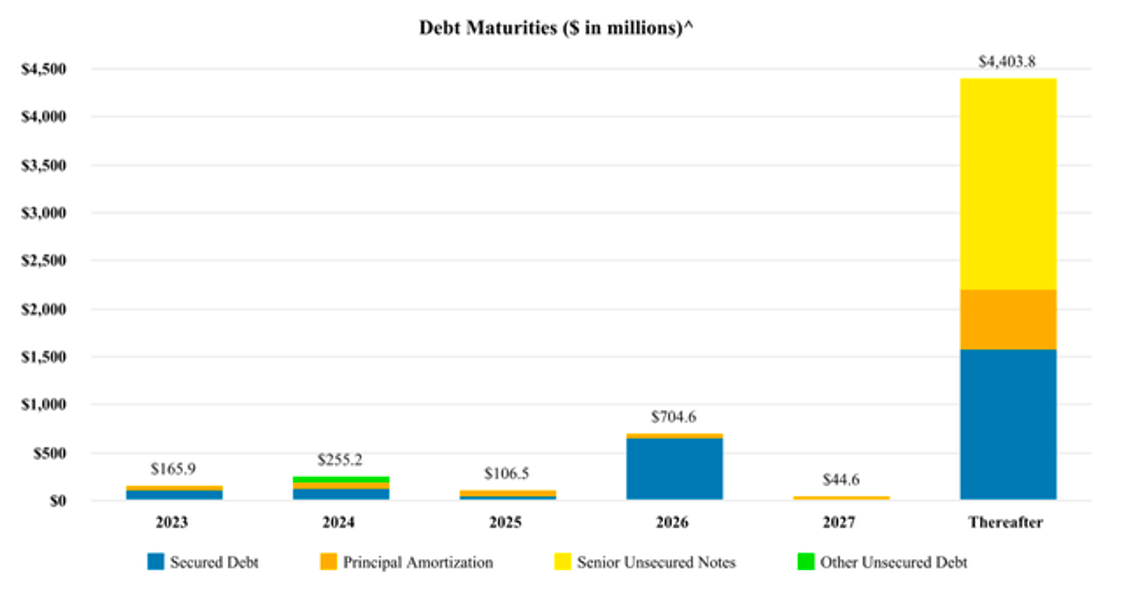

The outstanding debt of the company is $7.5 billion, 77% of it is fixed. The weighted average interest rate is 3.9%, the weighted average maturity is 7.4 years, and recurring EBITDA ratio is 6.1x. Even though the proportion of fixed rate debt is on the lower side, and they will have to refinance at a higher rate at some point, and the debt/EBITDA ratio is already pretty high, they have very little maturities for the next three years so it should not be a problem in the near future. After all, this is a solid BBB rated company.

{kind=link}

The dividend is currently sitting at $0.93 quarterly, $3.72 yearly. This translates to a dividend yield of 2.9% with a payout ratio of 51.4%. The dividend is therefore on the lower end. The company has been raising the dividend every year but by very small amounts. Consequently, the latest increase, which was 5%, was at the end of 2022 from $0.88 to the current $0.93. Going forward, further increases are likely, and I expect them to average 4-5% over the next 5 years.

The P/FFO is 17.5x with a historical average of 16.51x. It has been above the historical average since 2014 so it does not seem that cheap, however at its peak the company traded at 30x which is just crazy. Another thing I want to consider are peers that trade at the following multiples - Equity LifeStyle Properties ( ELS ) at 23.04x and UMH Properties ( UMH ) at 18.10x.

SUI is a bigger company than these peers. Its market cap is $16.27 billion while ELS's is $12.47 billion and UMH's is $922 million. So even though the company has been trading above the historical average, it still has a lower multiple than its peers. This suggests that SUI is undervalued compared to peers. So because manufactured homes have been getting more popular, the FFO is said to increase in the next years, and that the company has very little maturities, so the balance sheet is okay as of right now, I rate SUI as a BUY despite the low dividend.

{kind=link}

For further details see:

Sun Communities: Solid Company In A Market With Growing Demand